Market Overview: Ultra-Thin Battery Architectures and High-Frequency Signal Integrity Are Structurally Re-Rating the High-End Copper Foil Market

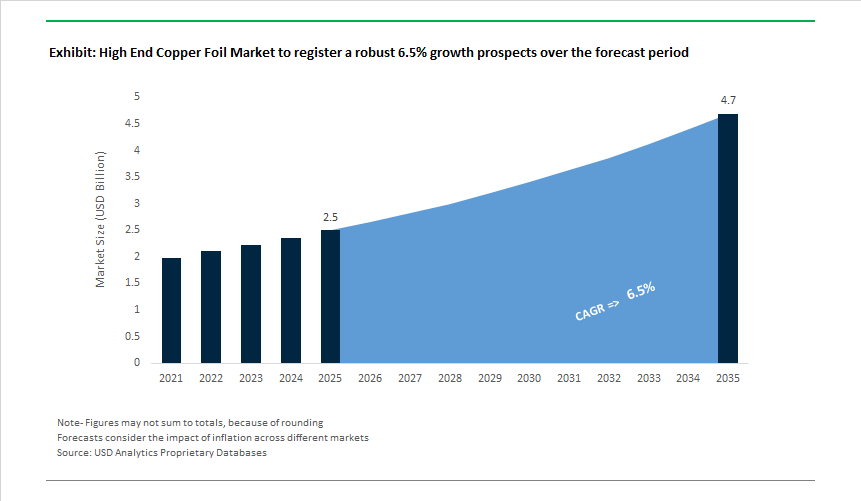

The Global High-End Copper Foil Market is valued at USD 2.5 billion in 2025 and is projected to reach USD 4.7 billion by 2035, expanding at a 6.5% CAGR as copper foil shifts from a semi-commodity input to a performance-critical material for electrification and digital infrastructure. Today, demand is no longer volume-led; it is being shaped by thickness limits, surface morphology, thermal resilience, and yield economics, all of which directly influence battery energy density and high-frequency signal performance.

A primary growth engine is lithium-ion battery scaling. Ultra-thin copper foils-below 6 µm-are now becoming standard in premium EV and energy storage platforms because they enable higher active-material loading and measurable gains in gravimetric and volumetric energy density. As EV OEMs push for longer range without increasing pack size, copper foil thickness is increasingly treated as a design variable, not a procurement afterthought. This structurally raises the value of high-precision electrodeposited and rolled foils that can maintain mechanical integrity and elongation at elevated temperatures during electrode processing.

In parallel, high-frequency electronics are redefining copper foil specifications. The rapid expansion of 5G/6G telecom infrastructure, AI servers, and hyperscale data centers is driving demand for very-low-profile (VLP) and high-voltage low-profile (HVLP) foils with surface roughness below 0.5 µm (Ra/Rq). At millimeter-wave frequencies, surface smoothness directly determines insertion loss, signal attenuation, and thermal noise. As a result, copper foil selection is increasingly dictated by signal-integrity budgets, elevating foil suppliers into strategic partners for PCB laminators and system OEMs.

Manufacturing economics are becoming a decisive differentiator. In high-end foil production, yield is value. Small improvements in defect density-such as reducing defects from 0.2 to 0.05 per m²-can lift saleable output by 15-20%, materially improving margins in a capital-intensive process environment. This places outsized importance on advanced electrodeposition control, inline optical inspection, surface treatment uniformity, and thermal-mechanical consistency, rather than raw copper input costs.

Thermal and mechanical performance thresholds are also tightening. High-layer-count PCBs and advanced battery electrodes require foils that retain 3-5% elongation at lamination temperatures approaching 180°C, preventing barrel cracking and delamination during multi-step processing. These requirements are pushing suppliers to invest in heat-tolerant foil chemistries, controlled grain structures, and optimized annealing profiles, further widening the gap between commodity and high-end producers.

Geography is now a strategic variable. Battery gigafactories and high-frequency electronics manufacturing hubs increasingly prioritize near-market copper foil capacity to shorten lead times, stabilize quality, and reduce geopolitical exposure. As a result, capacity additions in North America, Europe, and Southeast Asia are becoming procurement enablers rather than cost disadvantages, particularly for OEMs seeking supply security and qualification continuity.

Market Analysis: Capacity Builds, Material Innovations and Trade Policy Shifts Shaping Market Dynamics

The high-end copper foil industry has been marked by strategic capacity expansions, new material pilots, and regulatory shifts that collectively re-shaped supply-demand balances. In November 2025, Volta Energy Solutions completed the structural phase of its new Quebec plant targeting North American EV battery current collector demand - a clear signal that regional onshoring for battery foil is accelerating. Earlier in May 2025, Lotte Energy Materials began construction on its second high-end copper foil plant in Malaysia to serve Southeast Asian gigafactories, illustrating supplier moves to diversify geography and reduce reliance on single-source regions. These capacity additions coincide with strategic M&A and European consolidation: January 2025 saw Doosan Group integrate Circuit Foil Luxembourg’s specialty rolled foil lines, bringing advanced ultra-thin rolling expertise into a larger industrial platform.

Technology and input innovations also influenced market positioning. September 2025 brought a notable pilot from LS Cable & System on a CuFlake raw material for electrodeposition, aiming to lower input costs and improve sustainability. July 2025 Mitsui Kinzoku launched a new HVLP foil product (Rz ≈ 0.7 µm) targeting high-frequency PCB demands and autonomous driving electronics. Conversely, policy and quality controls affected trade flows: March 2025 Chinese export controls tightened thickness and quality requirements for exported copper foil to prioritize domestic EV and electronics assembly, while October 2025 strategic offtake agreements (e.g., LG Energy Solution securing multi-year supply from an Asian supplier for US gigafactories) illustrate how battery OEMs are locking supply via long-term contracts.

High End Copper Foil Market Trends and Opportunities

Trend 1: Ultra-Thin, Low-Profile Copper Foils Enabling Advanced Chip Packaging Architectures

The rapid shift toward 2.5D/3D chiplet architectures, Fan-Out Wafer-Level Packaging (FOWLP), and heterogeneous integration is structurally increasing demand for ultra-thin, low-profile copper foils that can function reliably as redistribution layers (RDLs) at sub-micron design rules. As semiconductor packages move away from monolithic dies toward stacked and laterally interconnected chiplets, copper foil is no longer a passive conductor—it has become a precision-engineered interface material that directly influences electrical performance, thermal dissipation, and yield. By late 2025, manufacturers such as Mitsui Kinzoku had expanded production of carrier-supported MicroThin™ foils, where a 5 µm functional copper layer is temporarily supported by an 18 µm carrier to enable defect-free handling during lithography and etching. This approach allows line/space patterning at scales required for smartphone application processors and AI accelerators without mechanical deformation or wrinkling. At the same time, thermal considerations are becoming decisive. Advanced packaging studies published in 2025 show that buried interfaces within 3D stacks account for up to 40% of total junction-to-ambient thermal resistance. Ultra-low-profile copper foils with controlled surface roughness (Rz) significantly reduce interfacial spreading resistance, preserving copper’s intrinsic thermal conductivity of roughly 385–401 W/m·K—orders of magnitude higher than organic substrates such as FR-4. Equally critical is yield stability at scale. Leading foil suppliers have achieved unprecedented uniformity in release strength across kilometer-scale rolls exceeding one meter in width, preventing peel-induced defects during carrier removal. This capability is now a prerequisite for high-volume manufacturing of fine-line interposers used in AI GPUs, where even microscopic delamination can translate into catastrophic yield loss.

Trend 2: Double-Treated Copper Foils for High-Capacity Lithium-Ion Battery Anodes

In parallel with semiconductor demand, the electrification of transport and the push toward higher energy-density lithium-ion batteries are reshaping requirements for copper foil used as anode current collectors. As battery developers transition from graphite-dominant anodes to silicon-oxide (SiOx), silicon-carbide, and composite silicon systems, mechanical and interfacial stresses on the copper foil have increased dramatically due to silicon’s large volumetric expansion during lithiation. In response, the market is moving toward double-treated and nano-engineered copper foils that deliver both high peel strength and thermal stability. In 2025, specialized double-sided, nickel-treated copper foils were commercialized with tensile strengths exceeding 50 kgf/mm², specifically to suppress electrode cracking during calendaring and long-term cycling. Electrochemical studies published during 2024–2025 further demonstrated that heat-treated and double-treated foils promote the formation of a more stable, Li₂O-rich solid electrolyte interphase (SEI), slowing lithium consumption and improving capacity retention—62% after 100 cycles compared to 43% for conventional foils in comparable anode-free cell configurations. Beyond metals alone, hybrid current collectors are emerging as a complementary trend. Polymer-based collectors reinforced with halloysite nanotubes and coated with dual copper layers have achieved interfacial adhesion forces of approximately 4 N/cm, roughly double that of traditional foil-polymer interfaces. This evolution is particularly relevant for flexible pouch cells, where copper foil must simultaneously accommodate mechanical flexing, thermal cycling, and aggressive electrochemical environments without delamination or loss of conductivity.

Opportunity 1: Very-Low-Profile Copper Foils for AI Data Centers and 6G Infrastructure

The acceleration of AI workloads and the early deployment of 6G millimeter-wave infrastructure are opening a high-value opportunity for very-low-profile (VLP) and hyper-very-low-profile (HVLP) copper foils engineered to mitigate high-frequency signal losses. As data rates climb beyond 200 Gbps in AI servers and network switches, the skin effect and conductor surface roughness have become dominant contributors to insertion loss. In response, HVLP grades (HVLP3 to HVLP5) are being qualified to reduce signal attenuation by up to 40% compared to standard electrodeposited foils. By December 2025, suppliers such as Co-tech Development reported record revenues driven by structural shortages of HVLP4 foils, as only a limited number of manufacturers globally possess the process control needed to mass-produce these ultra-smooth surfaces. Industry projections point to a potential supply deficit of up to 600,000 kg per month starting in mid-2026 as hyperscale data centers scale 800G and prepare for 1.6T architectures. This demand is tightly coupled with advances in low-loss laminate materials. Capacity expansions announced in late 2025 for PPE oligomers and other high-frequency resin systems are specifically designed to pair with HVLP foils, ensuring signal integrity in 5G/6G base stations operating at frequencies approaching 100 GHz. Together, these developments position high-end copper foil as a strategic enabler of next-generation digital infrastructure rather than a commoditized PCB input.

Opportunity 2: Direct Plated Copper for Wide-Bandgap Power Electronics and EV Platforms

The transition to 800 V electric vehicle architectures and the widespread adoption of silicon carbide (SiC) and gallium nitride (GaN) devices are creating a distinct growth avenue for direct plated copper (DPC) technologies on ceramic substrates. Power electronics manufacturers are increasingly abandoning traditional wire-bonded assemblies in favor of thick, high-purity copper layers directly plated onto aluminum nitride (AlN) and silicon nitride (Si₃N₄) ceramics. By 2025, more than half of global power module producers had begun transitioning to ceramic substrates to address rising power densities and thermal loads. DPC offers lower parasitic inductance, improved current distribution, and superior thermal spreading—capabilities that are essential for high-switching-frequency SiC devices used in traction inverters and fast chargers. This shift is also reshaping upstream supply chains. Demand for ultra-high-purity copper foils and electrolytes suitable for defect-free thick plating has driven significant investment in copper plating chemistry, with new facilities coming online in Southeast Asia to support advanced packaging and power module production. At the regional level, domestic manufacturing initiatives are gaining momentum. In 2025, large-scale investments announced in India targeted the production of EV-grade copper foils to support local inverter, battery management system, and power electronics manufacturing. As governments push for supply-chain localization and electrification simultaneously, direct plated copper is emerging as a strategic intersection point between advanced materials, power efficiency, and industrial policy.

Market Share Analysis: High-End Copper Foil Market

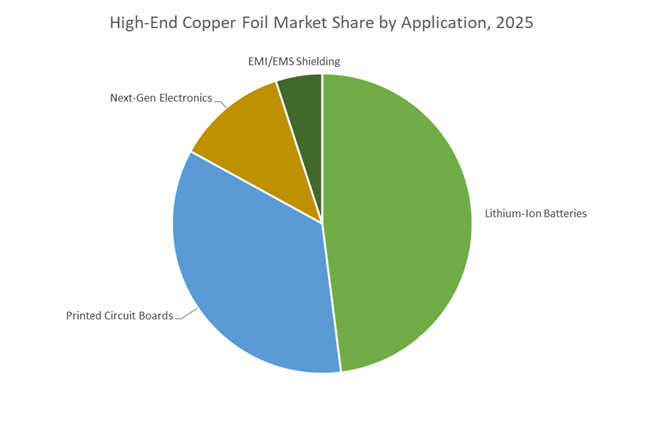

Market Share by Application: Lithium-Ion Batteries as the Structural Demand Anchor

Lithium-ion batteries account for approximately 45% of high-end copper foil demand in 2025, driven by a fundamental shift in battery design economics where incremental material improvements directly translate into vehicle-level performance gains. The transition from conventional 8–10 μm copper foil to ultra-thin 4.5–6 μm grades delivers a 5–11% boost in battery energy density, making copper foil thickness reduction one of the most cost-efficient levers for extending EV driving range without increasing pack size or weight. This performance impact explains why copper foil has moved into the strategic procurement tier for battery manufacturers, now representing 8–10% of total EV battery cell cost—a remarkably high share for a single current collector material. Demand momentum is reinforced by scale: EV-sector copper foil consumption rose by roughly 50% year over year in 2025, supported by global EV sales exceeding the 10-million-unit threshold. At the same time, next-generation anode chemistries—particularly silicon-rich and semi-solid-state designs—are imposing stricter mechanical requirements, pushing suppliers to deliver foils with tensile strength above 50 kgf/mm² to withstand repeated expansion and contraction during fast-charge cycles. These combined drivers—energy density gains, cost leverage, volume growth, and mechanical performance—lock lithium-ion batteries into the dominant application position in the high-end copper foil market.

Market Share by Product Type: ULP/VLP Copper Foil as the High-Margin Performance Standard

Ultra-Low Profile (ULP) and Very-Low Profile (VLP) copper foils command around 35% of total market share because they are no longer niche materials but essential enablers of high-frequency signal integrity in advanced electronics and AI infrastructure. As data rates escalate across 5G, emerging 6G, and AI server architectures, surface roughness has become a first-order performance variable rather than a secondary specification. Benchmarks show that HVLP foils can reduce signal insertion loss by up to 40% versus standard copper foil, directly improving power efficiency and thermal stability in densely packed circuit boards. This effect is magnified in AI hardware, where per-unit HVLP foil consumption is now roughly eight times higher than in conventional servers, creating an “AI demand multiplier” that structurally favors low-profile foil producers. Supply dynamics further reinforce this dominance: the ultra-thin foil segment below 5 μm is effectively capacity-constrained, with leading suppliers controlling over 95% of global output and expanding production to industrial scale in 2025. The latest HVLP generations achieving surface roughness (Rz) below 0.5 μm are now critical for ultra-fine circuit patterning aligned with 2 nm and 3 nm semiconductor substrates, cementing ULP/VLP copper foil as the highest-value, fastest-scaling product category within the high-end copper foil market.

Competitive Landscape: Specialty Producers, Vertical Expansion and Technology Leaders in High-End Copper Foil

The competitive field is led by firms that combine process mastery (electrodeposition and continuous rolling), regional capacity expansion, and product specialization (ultra-thin anode foils, HVLP/VLP foils, RA rolled foils). Market leaders differentiate on yield performance, surface engineering (reverse treatment, low-Dk barrier coatings), and the ability to deliver HTE-qualified products for demanding thermal cycles. Strategic moves in 2024-2025 - plant builds in Malaysia and Quebec, acquisitions in Europe, and raw-material innovation pilots - underscore a race to secure premium battery and telecom OEM contracts.

SK Nexilis - Ultra-Thin Battery Foil Leader Scaling For Global Gigafactories

SK Nexilis is a global frontrunner in ultra-thin copper foil for lithium-ion battery current collectors, mass-producing 4 µm foils with robust tensile strength and elongation metrics. The company has committed substantial capital (over 1 trillion KRW in 2024-2025) to build capacity in Malaysia and Poland to serve EU and U.S. gigafactories. Proprietary continuous rolling and advanced electrodeposition techniques deliver exceptionally low surface roughness (Ra <0.2 µm), making SK Nexilis a preferred supplier to major battery OEMs and securing long-term offtake relationships.

Lotte Energy Materials - Aggressive EV Supply Strategy and Thin-Foil R&D

Lotte Energy Materials (formerly Iljin Materials) is positioning to capture a material share of the non-Chinese battery foil market via rapid plant builds in Southeast Asia and technological R&D targeting foils as thin as 3.5 µm for next-gen and solid-state batteries. The company emphasizes process efficiency-claiming one of the industry’s lowest waste rates-through proprietary additives and drum surface treatments, supporting its strategic aim of 25% market share outside China by 2030.

Mitsui Kinzoku - HVLP Specialist For High-Frequency and Automotive Electronics

Mitsui Kinzoku focuses on HVLP and reverse-treated foils engineered for high-speed digital, RF, and ADAS applications. Its product portfolio includes ultra-smooth foils (typical Rz <1.0 µm) and tailored surface treatments (low-Dk barrier layers) to ensure adhesion to low-loss dielectrics. The company’s July 2025 HVLP launch addresses telecom infrastructure and autonomous driving demands where signal integrity is mission-critical.

Furukawa Electric - Rolled Copper Expertise and HTE Performance For Flexible and Multilayer Pcbs

Furukawa Electric is a leader in rolled (RA) copper foil used in flexible PCBs, wearables and display interconnects. The firm has advanced alloying approaches that enhance high-temperature elongation (HTE), minimizing dimensional and cracking issues during multi-step lamination at elevated temps. Recent investments in rolling mill capacity (wider formats up to 1,500 mm) target automotive BMS and large-panel display markets.

Jingbao Electronic Materials - Scale Player Moving Up The Technology Stack in China

Jingbao is a major Chinese electrodeposited foil manufacturer leveraging scale, cost competitiveness, and strong domestic demand from EV gigafactories. Having expanded ultra-thin capacity by ~40% in 2024, the company is now developing double-sided treated HVLP foils (sub-1.0 µm roughness) aimed at server and 5G base-station applications-a strategic move to capture higher-value, high-frequency segments while supporting massive domestic battery production.

Japan continues to function as the global technology benchmark for high-end copper foil, particularly in applications where signal integrity and ultra-low transmission loss are non-negotiable. In 2025, Japanese manufacturers have decisively moved beyond conventional HVLP toward sub-1-micron surface roughness foils, aligning copper foil development directly with Beyond 5G (B5G), early 6G research, and hyperscale AI server backplanes. Mitsui Mining & Smelting’s November 2025 decision to expand its proprietary VSP™ copper foil capacity by 45%—reaching 1,200 tons per month across Taiwan and Malaysia—underscores the structural demand shift toward ultra-smooth, high-frequency materials rather than commodity battery foils.

Technologically, Japan remains the only country to commercially stabilize HVLP5 (SI3-VSP) category foils at scale, achieving surface profiles below 1 micron. This is critical for mitigating skin-effect losses at extremely high data rates used in AI accelerators and next-generation photonic-copper hybrid interconnects. Government-backed programs such as the NICT Innovative ICT Fund further reinforce Japan’s role as the materials backbone for 6G-era infrastructure, ensuring continued dominance in the premium segment of the global copper foil value chain.

South Korea: High-End R&D Retention Amid Energy-Driven Manufacturing Migration

South Korea’s high-end copper foil strategy in 2025 reflects a two-speed industrial model: retaining advanced R&D and materials engineering domestically while relocating energy-intensive mass production overseas. Rising industrial electricity costs—now exceeding residential tariffs—have structurally altered cost economics, pushing producers such as SK Nexilis and Lotte Energy Materials to expand battery foil capacity in Malaysia and Uzbekistan, where power costs are roughly 40% lower. This geographic rebalancing is not a retreat but a margin-protection strategy in an increasingly competitive battery materials landscape.

At the technology frontier, South Korea has strengthened its position in next-generation EV battery foils. Lotte Energy Materials’ launch of HiSTEP hybrid copper foil in August 2025 marked a key milestone, combining ultra-thinness with high tensile strength and elongation—attributes essential for dry-process electrode manufacturing and high-energy-density 800V EV platforms. Simultaneously, Korean suppliers are entering glass substrate copper foil for advanced AI chip packaging, a niche but high-margin application that links copper foil demand directly to semiconductor roadmap evolution rather than cyclical EV volumes.

Taiwan: HVLP4 Supply Bottleneck and AI Hardware Pricing Power

Taiwan has emerged as the most immediate pressure point in the global high-end copper foil market, driven by surging AI server demand and tightening supply of HVLP4-grade materials. In 2025, Taiwanese manufacturers such as Co-tech Development benefited directly from the acceleration of AI infrastructure spending, with November revenues reaching NT$716 million, the highest level in four years. The material mix is shifting rapidly toward high-frequency, low-profile foils optimized for AI accelerators and high-speed switch ASICs.

Structurally, analysts project a global HVLP4 supply gap of 500,000–600,000 kg per month from mid-2026, positioning Taiwanese suppliers with rare near-term pricing leverage. This imbalance has already enabled 5–10% price increases in Q4 2025 for premium foil grades. Technically, Taiwan’s strength lies in its integration of HVLP foils with Modified Semi-Additive Process (MSAP) technologies, enabling ultra-fine line widths for compact 5G and AI hardware. As a result, Taiwan is becoming the price-setter for AI-grade copper foil, despite lacking the upstream scale of China or Japan.

China: Export Stabilization and Domestic Ultra-Thin Localization

China remains the world’s largest producer of copper foil by volume, but its 2025 strategy reflects a deliberate pause and recalibration rather than aggressive expansion. The temporary suspension of restrictive export controls under MOFCOM Announcement No. 70 (November 2025) has stabilized global lithium battery copper foil supply through November 2026, reducing near-term volatility for international battery manufacturers. This move signals China’s intent to maintain export relevance while avoiding further geopolitical escalation.

Concurrently, Beijing is channeling subsidies toward below-5-micron electronic-grade copper foil, targeting import substitution in semiconductor and EV power electronics. New national quality standards introduced in 2025 aim to align domestic HVLP production with requirements for 14nm and below logic nodes, narrowing the performance gap with Japanese suppliers. Strategically, China is balancing its role as a global export hub with a long-term objective of self-sufficiency in ultra-high-end copper foil, especially for internal AI and EV ecosystems.

India: Subsidy-Led Capacity Build and 5G-Driven Demand Surge

India’s high-end copper foil market in 2025 is being shaped less by current capacity and more by policy-driven future demand visibility. Under the Modified Special Incentive Package Scheme (M-SIPS), the government is offering 20–25% capital subsidies for greenfield copper foil plants, catalyzing interest from large industrial conglomerates seeking entry into VLP and HVLP production. While India remains a net importer of high-end foils today, the policy framework is designed to compress the technology gap over the next investment cycle.

Demand fundamentals are strengthening rapidly. Following over USD 19 billion in 5G spectrum investments, copper foil consumption in base stations and transmission equipment is projected to quadruple between 2024 and 2027. Hindalco’s 2025 R&D progress in surface-treated copper foils—enhancing adhesion for high-capacity EV battery anodes—signals early movement toward higher-value applications. India’s trajectory positions it as a future volume growth market, with gradual migration toward performance-driven segments.

European Union: Battery Resilience and ESG-Driven Copper Foil Localization

The European Union’s high-end copper foil strategy in 2025 is anchored in supply chain resilience and regulatory leverage rather than cost leadership. The European Commission’s “Battery Booster” strategy explicitly targets copper foil as a critical bottleneck material for the region’s 251 GWh annual battery cell capacity, prioritizing domestic finishing and recycling over reliance on Asian imports. This policy reflects growing concern over geopolitical exposure amid global overcapacity.

Sustainability is a decisive differentiator. In 2025, 100% recycled copper foil certification—such as UL-validated products from Fukuda Metal Foil & Powder—has become increasingly mandatory for European OEMs under the EU Battery Regulation. Spain and Hungary have emerged as preferred investment hubs for copper foil finishing plants, supported by IPCEI funding and proximity to battery gigafactories. As a result, Europe is carving out a premium ESG-compliant copper foil segment, even as absolute production volumes remain lower than in Asia.

2025 Strategic Matrix: High End Copper Foil National Comparison

High End Copper Foil Matrix

|

Country

|

Primary Market Driver

|

2025 Strategic Milestone

|

Key Material Focus

|

|

Japan

|

6G & AI servers

|

VSP™ capacity expanded to 1,200 t/month

|

HVLP5, ultra-smooth profiles

|

|

South Korea

|

High-energy EV batteries

|

HiSTEP hybrid foil commercial launch

|

4.5-micron, dry-process compatible

|

|

Taiwan

|

AI hardware & PCBs

|

HVLP4 revenue peak, pricing power

|

High-frequency, low-loss foils

|

|

China

|

Global export stability

|

12-month export control pause

|

Electronic-grade & Li-ion foil

|

|

India

|

5G rollout & M-SIPS

|

20–25% capital subsidy approvals

|

VLP/HVLP for telecom & EVs

|

|

European Union

|

Battery resilience & ESG

|

“Battery Booster” policy adoption

|

100% recycled, ESG-certified foil

|

High End Copper Foil Market Report Scope

High End Copper Foil Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.5 Billion

|

|

Market Size (2035)

|

$4.7 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Product Type (Electrolytic Copper Foil, Rolled Annealed Copper Foil, Ultra-Low Profile & Very-Low Profile Foil, MicroThin / Carrier-Attached Foil, Double-Side Treated Foil), By Thickness (Ultra-Thin Foil, Thin Foil, Standard Thickness, Heavy/Thick Foil), By Application (Printed Circuit Boards, Lithium-Ion Batteries, EMI/EMS Shielding, Next-Generation Electronics), By End-User Industry (Automotive, Telecommunications, Consumer Electronics, Aerospace & Defense, Renewable Energy)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mitsui Mining & Smelting Co. Ltd., SK Nexilis (SKC Ltd.), JX Nippon Mining & Metals Corporation, Furukawa Electric Co. Ltd., Chang Chun Group, Doosan Corporation (Electro-Materials), Circuit Foil Luxembourg S.à r.l., Nippon Denkai Ltd., LS Mtron Ltd., Fukuda Metal Foil & Powder Co. Ltd., Nan Ya Plastics Corporation, UACJ Corporation, Jinbao Electronics Co. Ltd., Iljin Materials Co. Ltd. (Lotte Energy Materials), Targray Technology International

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High-End Copper Foil Market Segmentation

By Product Type

- Electrolytic Copper Foil

- Rolled Annealed Copper Foil

- Ultra-Low Profile and Very-Low Profile Foil

- MicroThin / Carrier-Attached Foil

- Double-Side Treated Foil

By Thickness

- Ultra-Thin Foil

- Thin Foil

- Standard Thickness

- Heavy/Thick Foil

By Application

- Printed Circuit Boards

- Lithium-Ion Batteries

- EMI/EMS Shielding

- Next-Gen Electronics

By End-User Industry

- Automotive

- Telecommunications

- Consumer Electronics

- Aerospace & Defense

- Renewable Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in High-End Copper Foil Market

- Mitsui Mining & Smelting Co., Ltd.

- SK Nexilis (SKC Ltd.)

- JX Nippon Mining & Metals Corporation

- Furukawa Electric Co., Ltd.

- Chang Chun Group

- Doosan Corporation (Electro-Materials)

- Circuit Foil Luxembourg S.à r.l.

- Nippon Denkai, Ltd.

- LS Mtron Ltd.

- Fukuda Metal Foil & Powder Co., Ltd.

- Nan Ya Plastics Corporation

- UACJ Corporation

- Jinbao Electronics Co., Ltd.

- Iljin Materials Co., Ltd. (Lotte Energy Materials)

- Targray Technology International

*- List not Exhaustive