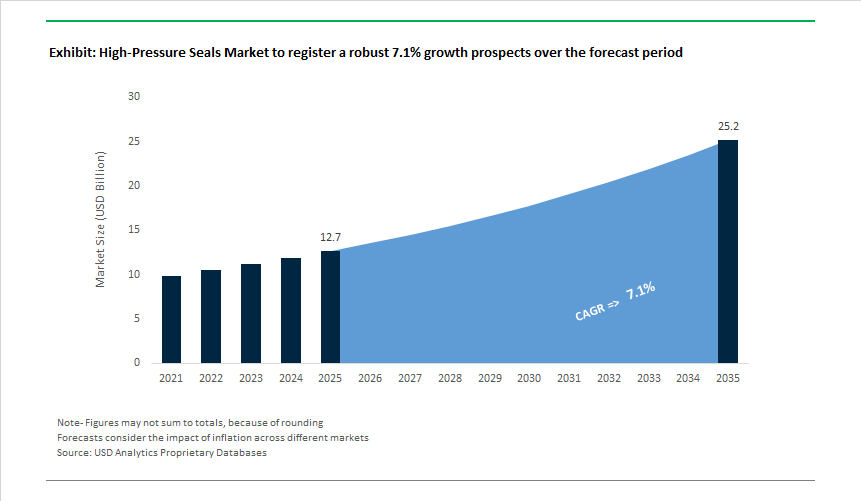

Market Overview: FKM/FFKM Material Leadership and Pump-Seal Criticality Fuel the USD 12.7B Market With 7.1% CAGR To 2035

The High-Pressure Seals Market is valued at USD 12.7 billion in 2025 and is projected to reach USD 25.2 billion by 2035, advancing at a 7.1% CAGR as sealing performance shifts from a maintenance consideration to a core determinant of asset uptime, safety, and regulatory compliance. Across oil & gas, petrochemicals, chemicals, power generation, and aerospace, high-pressure seals are specified not for cost efficiency but for their ability to survive extreme combinations of pressure, temperature, chemical exposure, and dynamic loading where failure consequences are economically and operationally severe.

Material leadership defines value concentration in this market. Fluoroelastomers (FKM) and perfluoroelastomers (FFKM) account for a disproportionate share of revenue because they remain functionally stable under continuous operating temperatures above 200°C while resisting aggressive hydrocarbons, acids, amines, and specialty chemicals. These properties make FKM/FFKM compounds the default sealing materials for high-pressure, high-temperature (HPHT) environments in upstream oil & gas, refining, and chemical processing. In parallel, metal seals and advanced polymer formulations are specified in aerospace and specialty industrial systems where performance must be maintained across extreme thermal envelopes (approximately −54°C to +649°C), in line with standards such as AS1895 and equivalent high-temperature sealing specifications.

From an application standpoint, mechanical pump seals represent the largest value pool, accounting for roughly 64% of mechanical-seal revenue. This dominance reflects the direct linkage between seal reliability and plant economics: seal failures in critical pumping systems can result in production losses approaching USD 100,000 per hour, in addition to safety incidents, environmental exposure, and downstream equipment damage. As a result, operators increasingly prioritize sealing systems with validated lifetime performance, predictive monitoring compatibility, and proven resistance to wear, extrusion, and chemical attack-shifting procurement toward higher-spec, higher-margin solutions.

Future growth is reinforced by operational severity rather than volume expansion. Deep-water and unconventional drilling environments are accelerating demand for Rapid Gas Decompression (RGD)-resistant elastomer compounds, designed to withstand repeated pressure cycling without blistering or crack initiation. Similarly, higher process pressures, hotter operating regimes, and tighter emissions and safety regulations are narrowing acceptable material choices across refineries and chemical plants.

Market Analysis: Capacity Moves, Major Contracts and Product Launches

The market saw a sequence of strategic expansions, product introductions and service contract awards that underscore both product innovation and a shift toward service-led revenue. In December 2023, Precision Polymer Engineering (IDEX) introduced a new FFKM compound tailored for ammonia and sour-gas service, reflecting upstream needs for elastomers that can endure harsh chemistries. Manufacturing and geographic capacity expansion continued with March 2024 Sealmatic India bringing a new 25,000 sq ft plant online to increase production capacity by roughly 65%, supporting exports to over 50 countries and addressing global demand for engineered mechanical seals.

Service and large project wins marked 2025: January 2025 Flowserve secured a major dry-gas-seal order for ADNOC’s large CCS project in the UAE, highlighting the role of seals in energy-transition infrastructure, while August 2025 John Crane won a five-year gas-seal management contract in South Korea, signaling growing demand for integrated seal lifecycle services and predictive maintenance. Product innovation continued with November 2025 Trelleborg launching high-performance polyurethane hydraulic seals designed for heavy industrial extrusion resistance, and December 2025 Chinese firm LEPU SEAL announcing global manufacturing strengthening to pursue chemical, oil & gas and power markets. Earlier moves include a February 2024 acquisition by a global sealing technology firm of a specialized PTFE/polymer sealing business to broaden offerings for semiconductor and aggressive chemical applications, and January 2024 EagleBurgmann deepening pipeline OEM partnerships for large-scale modernization projects. Taken together, these events point to: (1) continued demand from oil & gas, CCS and power; (2) product innovation in high-temperature elastomers, PTFE systems and polyurethanes; and (3) a growing services orientation (seal management and IIoT) that reduces end-user downtime risk.

High-Pressure Seals Market: Trends and Opportunities

Material Architectures Optimized for Hydrogen and Supercritical CO₂ Environments

The rapid scale-up of hydrogen infrastructure and supercritical CO₂ (sCO₂) systems has exposed the structural limits of conventional elastomers. Hydrogen’s ultra-small molecular size and sCO₂’s solvent-like behavior induce swelling, permeation, and Rapid Gas Decompression (RGD)—now recognized as the dominant catastrophic failure mechanism in high-pressure gas service.

By late 2025, industry validation protocols have converged around ISO 23936-2 and NORSOK M-710, with elastomers such as FKM, EPDM, and HNBR qualified for 100% hydrogen exposure at pressures approaching 1,000 bar without micro-cavity initiation. These standards are becoming non-negotiable for compressors, valves, and injection equipment deployed in hydrogen hubs and CCUS networks.

In parallel, supercritical CO₂ injection has moved from pilot scale to commercial deployment. In January 2025, Flowserve Corporation secured a landmark contract to supply dry gas seals for the ADNOC Habshan CCUS project, designed to capture 1.5 million tons of CO₂ per year. Continuous sCO₂ service imposes unique challenges—pressure cycling, phase transitions, and chemical aggressiveness—driving demand for seals engineered specifically for CO₂ solubility resistance rather than legacy hydrocarbon performance.

To counter hydrogen permeation, suppliers such as Angst+Pfister are commercializing UHMW-PE and PTFE-based seal systems validated for ultra-low gas diffusion across −40 °C to +150 °C. These thermoplastics are increasingly specified in hydrogen compressors and valves where elastomer-based solutions exhibit unacceptable leakage or embrittlement risk.

Smart Seals and Embedded Telemetry Enabling Predictive Maintenance

High-pressure sealing is undergoing a structural shift from scheduled replacement to predictive, condition-based maintenance. “Smart seals” embed sensing functionality directly into the sealing interface, converting wear and degradation into actionable data streams.

In 2024–2025, Freudenberg Sealing Technologies validated a rod seal architecture that functions as a capacitive wear sensor. By layering conductive and insulating elastomers, the seal continuously monitors its own thickness; as wear progresses, capacitance changes are transmitted to digital dashboards, enabling precise prediction of remaining service life. This capability is particularly valuable in hydraulic presses, high-pressure compressors, and turbomachinery where seal failure cascades rapidly into system shutdowns.

The analytics layer is advancing rapidly. By October 2025, refinery and pipeline operators were integrating seal-derived vibration, temperature, and leakage-rate signatures into AI-driven Asset Intelligence platforms, enabling maintenance scheduling based on real operating conditions. Early adopters report up to 30% reductions in unplanned downtime, a material economic advantage in continuous-process industries.

Edge-enabled seal support systems—now aligned with API digitalization frameworks—are also gaining traction in emerging applications such as 800V EV battery cooling circuits and high-speed industrial compressors. Detecting micro-leakage before thermal runaway or pressure loss occurs has become a core safety requirement rather than a value-added feature.

High-Pressure Sealing Systems for Hydrogen Refueling and Distribution Infrastructure

The global rollout of hydrogen fueling stations is creating a structurally new demand profile for high-pressure seals, driven by extreme cycling frequency and uptime requirements. Modern stations rely on diaphragm compressors capable of 700 bar dispensing for light-duty vehicles and 350 bar for heavy freight, placing extraordinary fatigue and permeation stress on dynamic seals.

Equipment suppliers such as PDC Machines and Maximator Hydrogen are deploying automatic seal exchange systems that reduce seal replacement time from multiple days to under 10 minutes, enabling near-continuous station operation. This shift redefines seals as modular, service-optimized components rather than consumables requiring prolonged shutdowns.

Policy support is reinforcing this opportunity. The EU’s Clean Hydrogen Joint Undertaking (2025 Work Programme) explicitly prioritizes R&I funding for static and dynamic seals capable of withstanding cryogenic temperatures down to −253 °C for liquid hydrogen (LH₂) transport and storage. As hydrogen logistics diversify beyond gaseous systems, seal performance at cryogenic extremes is becoming a new competitive differentiator.

On the mobility side, hydrogen trucking programs— including pilots by Ashok Leyland—are generating volume demand for rotary shaft seals and metallic gaskets that tolerate high rotational speeds, vibration, and rapid pressure cycling in mobile fuel-cell powertrains.

Metal-to-Metal and HP/HT Seals for Deep-Sea and Subsea Energy Systems

Offshore exploration and carbon storage are pushing sealing requirements into regimes exceeding 15,000 psi (≈1,034 bar) and depths beyond 10,000 feet, where elastomeric solutions reach their physical limits. This is accelerating the adoption of metal-to-metal sealing architectures in HP/HT subsea equipment.

By 2025, Baker Hughes had commercialized subsea tree systems rated for 15,000 psi and 177 °C, relying extensively on precision-machined metal seals to ensure absolute containment in corrosive, high-salinity environments. These seals are now standard in deepwater developments where intervention costs dwarf initial equipment CAPEX.

Subsea CO₂ storage hubs represent a parallel growth vector. High-pressure injection packages for offshore carbon sequestration depend on dry gas seals and BB5 pump systems to move captured CO₂ through dedicated pipelines into geological formations. As CCUS transitions from demonstration to infrastructure-scale deployment, sealing reliability directly influences project bankability.

Emerging subsea energy storage concepts further amplify demand. Studies published during 2024–2025 show that CO₂-based subsea energy storage systems can deliver ~2.17× higher energy density than air-based alternatives. However, these systems impose repeated gas–liquid phase transitions at ambient seabed pressures, making advanced high-pressure seals a gating technology for commercialization.

Market Share Analysis: High-Pressure Seals Market

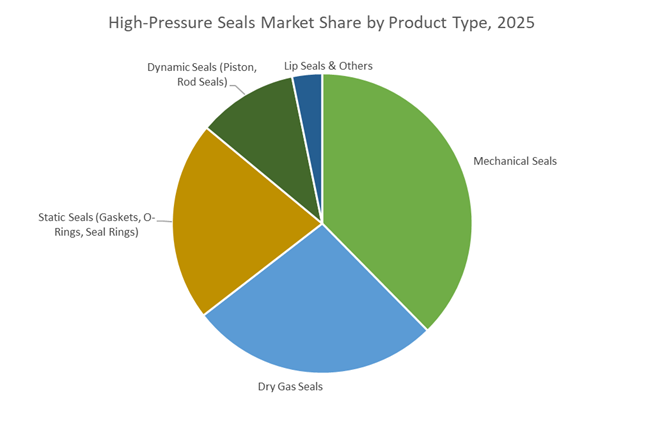

Market Share by Product Type: Mechanical Seals Dominate High-Pressure Fluid Integrity Requirements

Mechanical seals command the largest share of the High-Pressure Seals Market because they directly address the two most expensive failure modes in pressurized systems: unplanned leakage and energy loss. As industrial processes move toward higher operating pressures, temperatures, and regulatory scrutiny, traditional packing-based sealing has become economically and operationally obsolete. Mechanical seals are now engineered as system-level efficiency components, not consumables. Their near-zero fugitive emission performance—cutting leakage by up to 99%—has become a non-negotiable requirement for operators complying with EPA LDAR programs, EU Industrial Emissions Directive (IED), and refinery decarbonization mandates. Beyond compliance, the shift is financially rational: reducing seal-face friction directly lowers shaft power draw, translating into measurable energy savings at scale in pump-intensive facilities. The ability of modern metal bellows and cartridge mechanical seals to operate continuously at pressures approaching 138 bar and temperatures above 400°C enables their deployment in services where seal failure historically triggered catastrophic shutdowns, including hydrocrackers, deep-well injection pumps, and high-head compressors. This combination of regulatory alignment, lifecycle cost reduction, and extreme-condition reliability structurally anchors mechanical seals as the dominant product category.

Market Share by End-User Industry: Oil & Gas Anchors Demand Through Reliability-Critical Operations

Oil & Gas remains the largest end-user segment because high-pressure sealing performance is directly linked to asset uptime, safety risk, and environmental exposure, all of which carry outsized financial consequences in this sector. Unlike other industries where seals are maintenance items, in offshore platforms, refineries, and long-distance pipelines, seal failure translates into millions of dollars in lost production per day. As a result, procurement decisions increasingly prioritize Mean Time Between Failure (MTBF) and multi-year maintenance intervals rather than upfront seal cost. The push into deep-water exploration and extended-reach wells has elevated operating pressures beyond legacy design envelopes, making advanced mechanical and dry gas seals mission-critical. At the same time, the energy transition is reshaping demand: CO₂ re-injection for CCUS projects, hydrogen blending in gas pipelines, and sour-gas processing all introduce aggressive media that rapidly degrade conventional sealing solutions. High-pressure seals engineered for these applications now function as enablers of energy transition infrastructure. The sector’s willingness to pay for reliability—driven by safety regulations, emissions liability, and extreme downtime costs—explains why Oil & Gas continues to capture the largest share of global high-pressure seal demand despite broader diversification into other industries.

Competitive Landscape: Established Global Seal Suppliers Expanding Materials, Services and Digital Monitoring

The high-pressure seals competitive field is concentrated among engineering groups that combine advanced elastomer and metal-seal chemistry, precision machining, certifications (AS1895/AMS) and emerging digital service offerings. Companies are pursuing material R&D (FFKM, HNBR, PTFE laminates), project-scale contracts (CCS, LNG, pipelines), and life-cycle services that monetize uptime and predictive maintenance.

John Crane, Flowserve, Freudenberg Sealing Technologies, Trelleborg Sealing Solutions and Parker Hannifin lead markets through integrated product portfolios, project wins, and investments in smart sealing technologies - each with distinct strategic angles described below.

John Crane - Global Leader in Dry-Gas Seals and Smart Seal Services

John Crane is a dominant supplier of mechanical and dry-gas seals (Type 28/32 series) used in high-speed centrifugal compressors for LNG and pipeline service. The company is shifting toward outcome-based contracts - evidenced by a five-year gas-seal management contract (Aug 2025) in South Korea - and heavy R&D in non-contacting seals and integrated sensors for real-time temperature and vibration monitoring, positioning it at the nexus of mechanical reliability and Industry 4.0 service models. Its large installed base and seal-support systems expertise make it a preferred partner for critical rotating equipment.

Flowserve Corporation - System Integrator Winning CCS and Nuclear Sealing Megaprojects

Flowserve’s breadth across pumps, valves and seals allows it to supply integrated sealing system packages for energy transition infrastructure; the company’s largest dry-gas-seal order (Jan 2025) for ADNOC’s CCS project underscores credibility in megaproject sealing. With recurring nuclear orders and an IIoT platform (RedRaven) for remote condition monitoring, Flowserve leverages system integration to provide predictive maintenance, reducing unplanned downtime in high-value assets.

Freudenberg Sealing Technologies - Elastomer Science and FFKM Expertise For Harsh Chemistries

Freudenberg (FST) leads in elastomeric sealing, developing PTFE and FKM solutions for EV battery cooling and high-pressure chemical services. Its proprietary FFKM (Simriz®) materials resist hundreds of aggressive chemicals and tolerate temperatures up to ~327°C, while R&D into HNBR and alternative elastomers targets hydrogen and new-energy applications. FST’s focus on material science and automotive/industrial sealing gives it a cross-sector edge.

Trelleborg Sealing Solutions - PTFE and PEEK Specialist With New Polyurethane Hydraulic Seals For Heavy Industry

Trelleborg is a premier polymer sealing supplier offering Turcon® PTFE seals and HiMod® PEEK bearings for minimal friction and extreme-pressure applications. The company launched a new range of polyurethane hydraulic seals (Nov 2025) engineered for improved extrusion resistance under cyclic loads, targeting construction and heavy machinery markets. Trelleborg’s AS1895/AMS certifications and wide product catalogue make it a trusted supplier for aerospace and high-reliability OEMs.

Parker Hannifin - Metal and FFKM Seal Provider With Digital and Filtration Synergies

Parker’s Engineered Materials Group delivers elastomeric, hydraulic and metal seals, including Parofluor FFKM compounds tailored for semiconductor and ultra-pure chemical processes to extend MTBF. With historic acquisitions expanding filtration and sealing capabilities, Parker is also investing in smart seals for condition monitoring, enabling customers to adopt predictive maintenance and Industry 4.0 strategies in heavy-duty installations.

The United States high-pressure seals market in 2025 is being reshaped by a convergence of methane abatement regulation, supercritical operating regimes, and aerospace modernization. Following EPA methane rules, operators have accelerated adoption of dry gas seals and low-emission mechanical seals across pipelines and midstream assets. In September 2025, John Crane completed the first U.S. field installation of Type 8628VL multiphase seals on Gulf Coast ethane lines operating near ~1,100 psi, setting a benchmark for leak-zero performance under volatile pressure profiles.

Innovation in flow control further elevated standards. In March 2025, Flowserve launched the INNOMAG® TB-MAG™ Dual Drive™, the first magnetic-drive pump with true secondary containment for high-pressure chemical service—recognized with the 2025 Vaaler Award for leak elimination. Concurrently, FAA procurement momentum under the 2024 Reauthorization Act is sustaining demand for dynamic aircraft seals in landing gear and hydraulic actuators, supporting a ~USD 3.68 billion aircraft seals sub-sector and reinforcing U.S. leadership in extreme-duty sealing.

China: Whole-Chain Governance, Refining Scale & EV Sealing Localization

China’s high-pressure seals market is anchored in petrochemical scale and whole-chain governance of materials. By late 2025, rapid refining capacity expansion made China the world’s most influential market for spiral-wound gaskets, metal-jacketed gaskets, and high-pressure packings. Policy alignment under Made in China 2025 incentivized 70% self-sufficiency in critical components, accelerating domestic production of FKM and HNBR compounds for high-voltage EV battery sealing and heavy machinery.

Regulatory leverage tightened further in November 2025 when MOFCOM implemented export monitoring on high-performance polymer precursors, ensuring priority access for domestic manufacturers supplying semiconductor processing system seals. This blend of scale, standards, and export oversight positions China as a price-setting and specification-setting force in global high-pressure sealing.

United Arab Emirates: CCS Testbed and Supercritical CO₂ Injection Seals

The UAE has transitioned into a global testbed for carbon capture and storage (CCS) sealing, moving beyond traditional oilfield consumption. In January 2025, ADNOC awarded Flowserve a landmark contract for Dry Gas Seals at the Habshan gas plant, enabling continuous supercritical CO₂ (sCO₂) injection targeting 1.5 million tons/year of captured CO₂.

With a national ambition to reach 5 million tons/year by 2030, the UAE is catalyzing a localized ecosystem for high-pressure injection package seals capable of resisting corrosion, phase change, and sustained sCO₂ pressures. This environment is accelerating qualification cycles for next-generation non-contacting gas seals under desert and offshore conditions.

India: PLI Extension, Standards Harmonization & Power-Sector Demand

India’s high-pressure seals market is scaling on the back of localization policy, standards harmonization, and expanding energy infrastructure. The 2025 Union Budget signaled an extension of the PLI scheme into Light Engineering, directly benefitting domestic producers of mechanical seals, high-pressure O-rings, and gland packings. Quality alignment advanced as the Bureau of Indian Standards (BIS) finalized national specifications for expanded graphite foils, virgin PTFE, and wire-reinforced asbestos jointing materials, narrowing gaps with ISO benchmarks.

Demand fundamentals are strong. With installed power capacity reaching 476 GW by June 2025, India’s grid, refining, and process industries are driving ~7% annual growth in reliable high-pressure sealing—particularly for turbines, compressors, and high-duty pumps—cementing India’s role as a cost-competitive manufacturing hub.

Germany: PFAS-Free Transition, Digital Twins & Renewable Duty Cycles

Germany leads Europe’s technical pivot toward PFAS-compliant, sustainable high-pressure seals. In November 2025, Freudenberg Sealing Technologies announced a breakthrough BPAF-free FKM, responding to the EU’s immediate ban on bisphenol AF in food-contact materials and forcing redesigns across pharma and beverage sealing systems.

Renewables add complexity and volume. In August 2025, German manufacturers introduced specialized shaft seals for high-output hydropower plants engineered for extreme mechanical stress. At Hannover Messe 2025, seal majors showcased AI-driven digital twins that cut development time by up to 40%, embedding predictive sensors directly into seal geometries—raising reliability while compressing time-to-qualification.

Saudi Arabia: Vision 2030, Asset Management & High-Temperature sCO₂

Saudi Arabia’s high-pressure seals market is localizing rapidly under Vision 2030, emphasizing lifecycle asset management and advanced energy pilots. In March 2025, John Crane secured multiple asset management contracts with major petrochemical operators, bundling on-site refurbishment with digital diagnostics for rotating equipment uptime.

Forward-looking energy projects deepen requirements. Partnerships with European firms on supercritical CO₂ pilot plants are specifying dry gas seals that operate beyond 500 °C, a prerequisite for next-generation concentrated solar power (CSP) and high-efficiency cycles—positioning the Kingdom at the frontier of high-temperature, high-pressure sealing.

2025 Strategic Matrix: High-Pressure Seals by Country

High-Pressure Seals Matrix

|

Country

|

Primary Market Driver

|

2025 Strategic Milestone

|

Material / Technology Focus

|

|

United States

|

Methane abatement & aerospace

|

Type 8628VL field installs; TB-MAG™ launch

|

Multiphase dry gas & magnetic drive seals

|

|

China

|

Refining scale & localization

|

MOFCOM export monitoring (Nov 2025)

|

FKM, HNBR, spiral-wound gaskets

|

|

UAE

|

Carbon capture (CCS)

|

ADNOC Habshan sCO₂ injection

|

Supercritical CO₂ dry gas seals

|

|

India

|

PLI & power expansion

|

BIS standards for graphite/PTFE

|

Mechanical seals for grid & refining

|

|

Germany

|

PFAS compliance & renewables

|

BPAF-free FKM; AI digital twins

|

Sustainable FKM, smart seals

|

|

Saudi Arabia

|

Vision 2030 asset mgmt

|

Localization & sCO₂ pilots

|

High-temp (>500 °C) gas seals

|

High-Pressure Seals Market Report Scope

High-Pressure Seals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.7 Billion

|

|

Market Size (2035)

|

$25.2 Billion

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Material Type (Metal Seals, Fluoroelastomers, TPU, EPDM, HNBR, Specialty Polymers), By Product Type (Mechanical Seals, Dry Gas Seals, Dynamic Seals, Static Seals, Lip Seals), By Pressure Rating (High Pressure, Ultra-High Pressure, Supercritical Pressure), By End-User Industry (Oil & Gas, Energy & Power, Automotive, Aerospace & Defense, Chemicals & Petrochemicals, Pharmaceutical & Food)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

John Crane, Flowserve Corporation, Parker Hannifin Corporation, Trelleborg AB, EagleBurgmann, SKF Group, Saint-Gobain (Omniseal Solutions), Technetics Group, A.W. Chesterton Company, AESSEAL plc, Hallite Seals International, Garlock, James Walker, Flexitallic, Meccanotecnica Umbra S.p.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High-Pressure Seals Market Segmentation

By Material Type

- Metal Seals

- Fluoroelastomers

- Thermoplastic Polyurethane (TPU)

- Ethylene Propylene Diene Monomer (EPDM)

- Hydrogenated Nitrile Butadiene Rubber (HNBR)

- Specialty Polymers

By Product Type

- Mechanical Seals

- Dry Gas Seals

- Dynamic Seals

- Static Seals

- Lip Seals

By Pressure Rating

- High Pressure

- Ultra-High Pressure

- Supercritical Pressure

By End-User Industry

- Oil & Gas

- Energy & Power

- Automotive

- Aerospace & Defense

- Chemicals & Petrochemicals

- Pharmaceutical & Food

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in High-Pressure Seals Market

- John Crane (Smiths Group plc)

- Flowserve Corporation

- Parker Hannifin Corporation

- Trelleborg AB

- EagleBurgmann

- SKF Group

- Saint-Gobain (Omniseal Solutions)

- Technetics Group (EnPro Industries)

- Chesterton (A.W. Chesterton Company)

- AESSEAL plc

- Hallite Seals International

- Garlock (EnPro Industries)

- James Walker

- Flexitallic

- Meccanotecnica Umbra S.p.A.

*- List not Exhaustive