Market Overview: High Purity Pig Iron as the Cornerstone of Ductile Iron, Precision Casting & Green Steelmaking

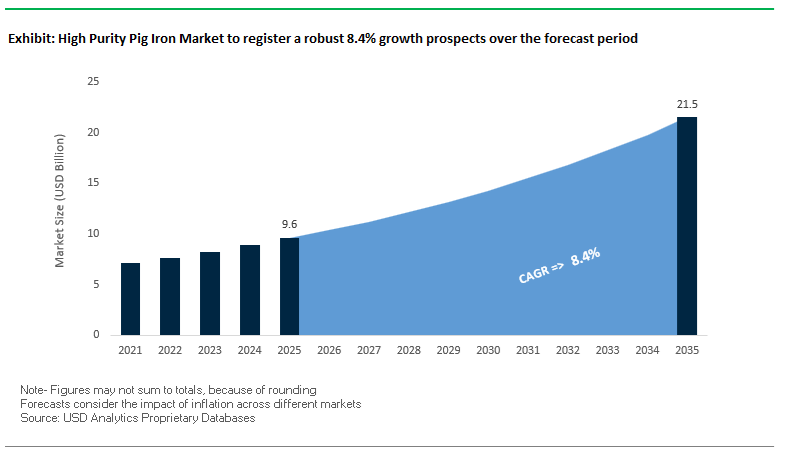

The High Purity Pig Iron (HPPI) Market is expected to expand from USD 9.6 billion in 2025 to USD 21.5 billion by 2035, reflecting a strong CAGR of 8.4%. This growth is fueled by the structural shift toward high-quality ductile iron castings, cleaner steelmaking processes, and precision-grade industrial components requiring ultra-low impurity feedstock. HPPI is increasingly becoming a mission-critical input for manufacturers seeking superior metallurgical control, improved castability, and compliance with evolving low-carbon production standards.

The market is deeply influenced by stringent purity thresholds. Automotive and machinery manufacturers require HPPI with sulfur <0.015%, ensuring proper graphite nodularization and enabling high-ductility ductile iron components. Precision casting markets—including engine blocks, heavy machinery housings, and wind turbine hubs—mandate phosphorus <0.030% to prevent embrittlement and ensure reliable impact resistance. Meanwhile, the global shift toward Electric Arc Furnace (EAF) and Hydrogen-based Direct Reduction (H-DRI) steelmaking is accelerating demand for ultra-clean HPPI due to its exceptionally low residual metals (Cu, Cr, Mo), which cannot be easily removed during scrap melting. Regulatory drivers such as Europe’s Carbon Border Adjustment Mechanism (CBAM), effective from October 2023, are further amplifying demand for low-carbon pig iron, compelling producers to modernize smelting technology and reduce embedded emissions.

Key Insights for Manufacturers & Foundries

- <0.015% sulfur content is critical for achieving reliable graphite nodularity in ductile iron castings.

- HPPI is becoming the preferred feedstock for EAF and H-DRI green steel plants due to its low residual impurity levels.

- <0.030% phosphorus is mandatory for precision castings used in engines and wind turbine hubs to prevent brittle failure.

- CBAM regulations are reshaping import patterns, boosting demand for verifiably low-carbon HPPI across Europe.

- Ultra-clean HPPI stabilizes metallurgical processes, giving foundries greater control over mechanical properties and defect reduction.

Market Analysis: Production Growth, Low-Carbon Ironmaking & Supply Realignments Shaping HPPI Demand

The High Purity Pig Iron market is experiencing accelerated momentum driven by rising global pig iron production, clean steel transitions, and increased precision casting activity. In March 2025, the World Steel Association reported that global pig iron output reached 120.8 million tonnes, reflecting 6.7% month-on-month growth and 2.4% year-on-year expansion, signaling strengthening foundational demand across foundries, pipe manufacturers and steelmakers. Parallelly, Q1 2025 data from India showed a 6.2% YoY increase in pig iron production, highlighting robust domestic growth in ductile iron pipes, automotive castings and infrastructure-related foundries.

Sustainability-focused shifts are reshaping regional HPPI consumption patterns. During Q3 2025, India’s Ministry of Steel announced multiple pilot projects deploying low-carbon pig iron in EAFs, contributing to a 10% increase in green feedstock usage in 2023. This reflects a broader global trend where HPPI is used to dilute impurities and reduce carbon intensity in flexible steelmaking routes. In August 2024, leading producers emphasized capital investments to improve blast furnace energy efficiency, reduce emissions and stabilize long-term HPPI production costs, supporting the transition toward greener metallurgical practices.

Supply realignments are also influencing the market. September 2025 reports confirmed that major Russian steel producers are optimizing blast furnace operations to expand exports of foundry-grade pig iron, ensuring adequate supply for European and Asian foundries experiencing rising casting demand. Meanwhile, the shift toward high-precision automotive and machinery castings became evident when the USGS reported in October 2024 a 7% increase in precision component production, strengthening demand for low-S and low-P HPPI grade inputs. Additionally, April 2025 fluctuations in iron ore pricing created margin pressures for blast furnace operators, emphasizing the value proposition of HPPI as a premium, high-control input that compensates for volatile raw material costs.

Long-term demand signals remain strong. In December 2025, global assessments projected sustained growth in the ductile iron profile market, underpinned by water and sewage infrastructure upgrades worldwide. This ensures a stable multi-year demand trajectory for nodular pig iron, which remains the primary feedstock for ductile iron pipes and high-strength industrial castings.

Technological Trends and Emerging Commercial Opportunities Driving Ultra-Low-Residual HPPI Adoption

Market Trend 1: Shift Toward Ultra-Low-Titanium HPPI to Improve Fatigue Performance in High-Strength Ductile Iron Crankshafts

The High Purity Pig Iron market is undergoing a structural transition as engine manufacturers tighten microstructural control requirements for ductile iron crankshafts in high-performance and heavy-duty engines. Titanium content is now being mandated at <0.015% (150 ppm) to prevent the formation of hard TiN inclusions, which act as severe stress risers in high-cycle fatigue environments. When Ti exceeds 0.020%, TiN clusters begin to nucleate along fillet regions—an area responsible for the majority of fatigue crack initiation—causing a 10–15% drop in fatigue endurance limit for high-strength ductile iron grades such as EN-GJS-700-2.

Even more critically, excessive Ti levels (>0.03%) interfere with magnesium spheroidization, producing degenerated graphite morphologies that reduce fatigue strength by an additional 20–30%. Since approximately 90% of metallic failures in crankshafts arise from fatigue, OEMs are increasingly specifying HPPI as the only feedstock capable of meeting these impurity constraints. By removing scrap-related contaminants and providing controlled chemistry at ppm levels, HPPI ensures consistent nodule count, uniform matrix structure, and predictable endurance performance—key to next-generation lightweight engine architectures.

Market Trend 2: Growing Dependence on Low-Residual HPPI to Achieve Toughness Requirements for Thick-Section Offshore Wind Castings

Offshore wind turbine hubs, nacelle frames, and large pitch control housings require thick-section ductile iron castings exceeding 200 mm wall thickness, creating challenging cooling conditions that encourage segregation of tramp elements. Standards such as EN-GJS-400-18U-LT require minimum 12 J Charpy impact energy at −20°C, a performance level impossible to achieve when residuals like Sn, Sb, and As exceed 0.005–0.010%.

During slow solidification, these impurities segregate to eutectic boundaries and promote the formation of steadite (Fe₃P) and other brittle phases, drastically elevating the ductile-to-brittle transition temperature. This microstructural embrittlement is further aggravated by phosphorus and chromium carbides, which reduce fracture toughness and promote crack propagation under low-temperature loading.

HPPI, with inherently low levels of these tramp elements, is increasingly recognized as the only reliable meltstock capable of delivering the micro-cleanliness needed to meet certification requirements for offshore structures. Its use minimizes segregation risks, improves impact toughness, and stabilizes graphite morphology—ensuring structural integrity in demanding marine environments.

Opportunities Transforming HPPI Adoption Across Automotive, Renewable Infrastructure, and Green Steel Pathways

Market Opportunity 1: Commercialization of Ultra-Low-Phosphorus HPPI for Thin-Wall Automotive Ductile Iron Structures

Automotive lightweighting is creating strong demand for ultra-low phosphorus HPPI, with new specifications targeting <0.020% P (200 ppm)—half the historical limit of 0.040–0.050%. Phosphorus promotes the formation of phosphide eutectic (steadite), which solidifies last at approximately 1,050°C and forms brittle networks at grain boundaries. In thin-wall castings with rapid thermal gradients, this eutectic severely increases the risk of cracking during solidification and cool-down.

Mechanical performance also degrades sharply as phosphorus increases: elongation drops, impact toughness declines, and internal microporosity rises due to segregated steadite films. For automotive structural safety components requiring ≥12% elongation, ultra-low-P HPPI provides major advantages by minimizing eutectic networks, reducing porosity, and improving fatigue tolerance. This positions HPPI as a high-value precursor material for next-generation, lightweight ductile iron components in EV chassis systems, steering knuckles, control arms, and crash-relevant components.

Market Opportunity 2: HPPI as a Preferred Precursor for Sponge Iron (HPSI) in Hydrogen-Based Green Steelmaking

Green steelmaking pathways—particularly Hydrogen Direct Reduction (H-DRI) combined with Electric Arc Furnace (EAF) melting—are transforming the metallurgical landscape. HPPI offers major metallurgical advantages due to its minimal gangue content and low levels of SiO₂ and Al₂O₃. In hydrogen-based routes, using HPPI as a feedstock enables:

- Up to 85% CO₂ reduction compared to blast furnace steelmaking

- 15–25% lower slag generation due to its exceptionally low gangue load

- Improved EAF thermal and electrical efficiency

- Faster tap-to-tap times due to reduced slag-cleaning reactions

H-DRI processes using HPPI-derived materials achieve 94–96% metallization, a key benchmark for sponge iron suitability in high-quality steel production. Moreover, HPPI’s chemistry simplifies refining, reduces alloy corrections, and enhances energy efficiency across the EAF process.

As steelmakers accelerate decarbonization compliance and move toward 2030–2050 emission targets, HPPI is increasingly viewed as a strategically important, high-purity precursor for sustainable ironmaking.

High Purity Pig Iron Market Share Analysis

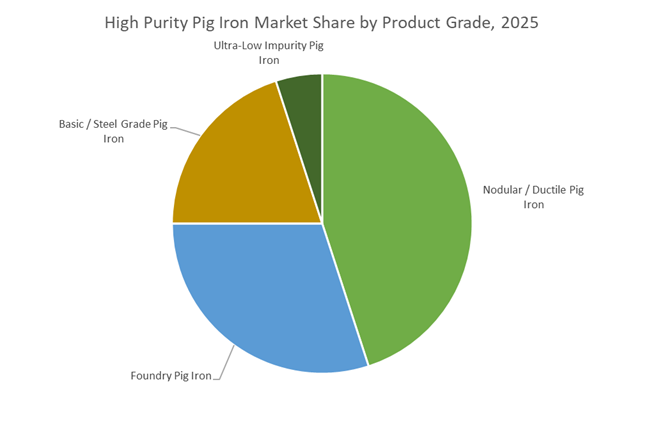

Market Share by Product Grade: Nodular / Ductile Pig Iron Leads Due to Its Critical Role in High-Strength, High-Reliability Casting Applications

Nodular / Ductile Pig Iron (DPI) holds the largest share of the global High Purity Pig Iron (HPPI) market—approximately 45% in 2025—because it is the indispensable feedstock for producing ductile iron castings, which dominate high-performance industrial and automotive applications. DPI relies on exceptionally low impurity levels (notably S ≤ 0.015%, P ≤ 0.030%, Ti ≤ 0.030%) to ensure the formation of spheroidal graphite during magnesium treatment, a microstructure that transforms cast iron from brittle to highly ductile and fatigue-resistant. This superior mechanical profile—combining high tensile strength, excellent elongation, and resistance to impact and thermal cycling—positions ductile iron as the most cost-efficient substitute for steel in high-load, precision-cast components. Because impurity control directly influences nodule count, shape, matrix distribution, and casting soundness, HPPI is the only viable raw material for achieving consistent metallurgical behavior across large-scale production runs. This explains why nodular pig iron remains the preferred input for foundries manufacturing critical components such as crankshafts, gears, hubs, heavy-duty housings, and high-pressure hydraulic parts. The segment’s leadership is also reinforced by the rapid global shift toward higher-quality castings, driven by stricter OEM specifications, the rise of lightweighting strategies, and the expansion of EV component manufacturing, all of which require ultra-clean, high-performance iron feedstock.

Market Share By End-Use Industry: Automotive & Transportation Dominates Owing to High-Volume Demand for Structural and Powertrain Castings

The Automotive & Transportation sector accounts for the largest end-use share of the HPPI market—approximately 55% in 2025—because modern vehicles depend heavily on ductile iron castings for structural integrity, fatigue resistance, and cost-effective mass production. Ductile iron derived from HPPI is extensively used in engine blocks, crankshafts, differential housings, gears, brake components, suspension knuckles, steering systems, and heavy-duty axle parts, where material performance is directly linked to vehicle safety and long-term durability. HPPI’s controlled impurity levels ensure reliable nodularity and uniform mechanical properties—requirements that are non-negotiable for automotive OEMs operating under strict global quality and traceability standards. The electrification of transportation further accelerates HPPI demand: EVs require advanced ductile iron components for thermal management structures, high-strength housings, motor brackets, and powertrain casings, while ultra-low-impurity pig iron is increasingly used to produce specialty electrical steels for traction motors and high-efficiency generators. With global automotive production expanding and EV adoption surging, the need for defect-free, dimensionally stable, fatigue-resistant cast parts continues to rise. This keeps the Automotive & Transportation sector firmly positioned as the highest-value, highest-volume consumer of high purity pig iron worldwide.

Country Analysis: Strategic High Purity Pig Iron Capabilities Reshaping Global Casting and Specialty Steel Markets

China: High-Purity Pig Iron Backbone for EV Casting, Ultra-Low Carbon Iron, and Foundry Expansion

China remains the central engine of growth in the High Purity Pig Iron Market, driven by its massive EV manufacturing ecosystem and government-backed quality mandates. Demand for ultra-clean HPPI is accelerating as Chinese automakers scale production of high-precision components such as electric motor stators, rotors, and structural chassis elements, all of which require iron with extremely low sulfur and phosphorus levels to ensure machinability, fatigue strength, and fault-free electromagnetic performance. This surge aligns with the country’s parallel R&D push into DT4E pure iron precursors, featuring an ultra-low carbon content of ≤0.025%, making them indispensable for EV relay stampings due to their outstanding magnetic permeability and reduced coercivity.

China’s foundry sector is simultaneously undergoing an aggressive modernization phase. Large manufacturers are installing next-generation blast furnace systems capable of producing Nodular (Ductile) Pig Iron with highly stable chemistry tailored for complex automotive, industrial, and rail castings. The government's strengthened Quality Control Order (QCO) framework is reshaping downstream steel and casting markets by enforcing stricter impurity thresholds—thereby boosting HPPI consumption as a compliance enabler. Combined with rapid scaling across automotive, machinery, and infrastructure industries, China maintains unmatched leadership in both volume and technological advancement of high-purity pig iron.

India: Specialty Steel PLI Acceleration, Green Hydrogen Pilots, and HPPI for Ductile Iron Infrastructure

India is strategically building a self-reliant High Purity Pig Iron supply chain, propelled by government incentives and rapid industrial growth. The Production-Linked Incentive (PLI) Scheme for Specialty Steel, backed by ₹27,106 crore in committed investments, is a major structural driver increasing HPPI demand, as downstream mills require ultra-clean feedstock to produce alloy steels, automotive steels, and precision-cast components. Indian producers such as Jai Balaji Group and Sree Metaliks are scaling Foundry Grade Pig Iron production with exceptionally low sulfur and phosphorus levels (0.035–0.045% S), reducing downstream refining costs and supporting metallurgical consistency for high-performance castings.

India is simultaneously exploring transformative pathways in low-carbon metallurgy. Under the National Green Hydrogen Mission, the government awarded pilot projects in late 2024 to integrate Green Hydrogen injection into blast furnaces, potentially lowering coke consumption and dramatically reducing the carbon intensity of HPPI production. At the same time, booming industrialization and water infrastructure expansion across Odisha, Maharashtra, and Jharkhand are driving extensive demand for Nodular (Ductile) Pig Iron used in ductile iron pipes, municipal water systems, and heavy engineering components. These demand patterns, reinforced by domestic manufacturing incentives and resource security initiatives, position India as one of the fastest-rising HPPI markets globally.

United States: Ultra-Low Impurity HPPI for Aerospace, High-Precision Machinery, and Scrap Dilution R&D

The United States demonstrates a robust technological focus within the High Purity Pig Iron Market, emphasizing ultra-low impurity inputs for mission-critical manufacturing sectors. U.S. precision foundries increasingly specify HPPI grades with tight tolerances for carbon, sulfur, phosphorus, and tramp elements, enabling the production of high-strength aerospace castings, high-tolerance industrial machinery components, and specialty engineered alloys. This requirement is especially important for high-load, high-temperature environments where material consistency is non-negotiable.

U.S. steelmakers are simultaneously investing in innovative refining approaches to manage the rising proportion of scrap metal in Electric Arc Furnaces (EAFs). HPPI is being tested as a dilution feedstock to neutralize impurity spikes from lower-grade scrap and stabilize final steel chemistry. This aligns with broader decarbonization trends, as domestic mills attempt to increase scrap circularity without compromising metallurgical quality. In addition, HPPI remains vital in specialty alloy production where tramp elements such as Ni, Mo, and Cr must be tightly controlled—ensuring consistent microstructure formation and predictable performance across high-end castings and advanced component applications.

South Africa: Titanium-Rich Magnetite Processing Hub and Premium HPPI Export Supply

South Africa plays a strategic role in the high-purity pig iron global supply chain, leveraging its vast titaniferous magnetite reserves. Producers such as Richards Bay Minerals (RBM) operate integrated mineral separation and smelting assets that co-produce high-quality Titanium Dioxide slag and High Purity Pig Iron, making the country a reliable source of HPPI with low residual contamination. This dual-product capability places South Africa at the center of value chains serving aerospace, automotive, and specialty foundry markets that require low-impurity iron for superior casting integrity.

HPPI from South Africa is primarily export-oriented, fulfilling demand from advanced European and Asian foundries. These downstream users rely on South African HPPI to manufacture components requiring strict chemical uniformity—such as hydraulic system castings, precision gear housings, and structural automotive parts. Its chemical purity, combined with consistent availability, positions South Africa as a crucial global stabilizer for HPPI supply amid rising capacity constraints in other regions.

Japan: HPPI for High-Grade Electrical Steel and High-Efficiency Motor Applications

Japan applies HPPI in one of the world’s most technologically sophisticated metallurgical segments: electrical steel production. Japanese steelmakers require High Purity Pig Iron with extremely low levels of harmful elements to ensure the production of high-grade grain-oriented and non-grain-oriented electrical steel, which is essential for high-efficiency transformers, traction motors, robotics systems, and EV drive units. HPPI is particularly critical because its purity allows manufacturers to minimize eddy current losses and achieve superior magnetic flux density.

Government sustainability mandates and corporate decarbonization efforts continue to push Japanese manufacturers toward ultra-high-efficiency motor designs, increasing reliance on pure iron components with low core losses. As EV penetration surges, Japan’s strategic metallurgical R&D programs are reinforcing the role of HPPI as an indispensable feedstock for next-generation electromagnetic materials, ensuring global competitiveness in high-performance electrical systems.

Brazil: Bio-Charcoal Based Low-Carbon Pig Iron for Global Green Steel Supply Chains

Brazil has emerged as a pivotal supplier in the low-carbon pig iron market, leveraging abundant biomass resources to produce pig iron using bio-charcoal instead of metallurgical coke. This innovation dramatically reduces the carbon footprint of pig iron production and positions Brazil as a preferred supplier for global green steelmakers seeking low-emission inputs. Brazilian HPPI producers are securing long-term contracts with European and North American mills as sustainability mandates intensify across global supply chains.

Competitive Landscape: Leading HPPI Producers Advancing Purity Control, Green Ironmaking & Integrated Supply

The competitive landscape of the High Purity Pig Iron market is dominated by vertically integrated miners, specialty smelters, and advanced metallurgical producers focused on ultra-low impurity control, consistent chemistry and sustainability-driven production. Companies differentiate through residual management, sulfur/phosphorus control, smelting technology, and regional supply network strength.

Rio Tinto Fer et Titane (RTFT) – Global Benchmark in Ultra-High Purity Nodular Pig Iron

Rio Tinto Fer et Titane produces Sorelmetal®, widely regarded as the highest-purity Nodular Pig Iron available globally, with extremely low levels of sulfur, phosphorus and tramp elements. Its vertical integration—from ilmenite mining to electric furnace smelting—enables unmatched chemical consistency and metallurgical reliability. RTFT is the preferred supplier for premium ductile iron applications, including safety-critical automotive castings, heavy machinery and energy infrastructure components.

Tronox Holdings (RBM) – Cost-Efficient HPPI Production via Integrated TiO₂ Operations

Tronox, through Richards Bay Minerals, produces HPPI as a co-product of titanium dioxide slag production, offering a cost-competitive source of ultra-clean feedstock. Its HPPI is valued for tight chemical consistency and predictable casting performance. With a strong foothold across Africa, RBM enhances supply availability for European and Asian foundries requiring high-specification pig iron for ductile iron pipe, automotive castings and precision industrial components.

Eramet SA – Specialty Metallurgy Leader Supporting Foundry & Alloy Markets

Eramet leverages its strength in manganese alloys, nickel and specialty metallurgy to deliver high-purity pig iron tailored for demanding foundry applications. Its ability to supply both HPPI and critical alloying materials (such as manganese) allows integrated solutions for cast iron chemistry optimization. Eramet’s emphasis on responsible mining and sustainable production enhances its strategic appeal amid growing ESG-focused procurement.

Vedanta Limited – Dominant Supplier to India’s Rapidly Growing Casting & Pipe Sector

Vedanta is among India’s key producers of foundry-grade pig iron, serving the nation’s booming ductile iron pipe and automotive casting industries. The company continuously invests in blast furnace optimization, thermal efficiency enhancement and impurity reduction to ensure stable, high-quality HPPI output. Its strong domestic supply capacity supports India’s infrastructure build-out and rapidly expanding casting ecosystem.

Kobe Steel (KOBELCO) – Advanced Ironmaking Technologies Supporting High-Performance Castings

Kobe Steel utilizes cutting-edge ironmaking systems including the MIDREX DRI process and optimized blast furnaces to produce low-impurity iron units suitable for advanced alloys and high-performance steel applications. Its metallurgical expertise ensures HPPI tailored for specialized castings, automotive components and high-strength industrial materials, reinforced by its deep materials science capabilities.

China Hanking Holdings – Large-Scale HPPI Supply for Asia-Pacific Foundries

China Hanking supplies high-quality pig iron at scale, supporting the massive demand from China’s ductile iron pipe, construction casting and industrial manufacturing sectors. With extensive iron ore reserves and processing facilities, the company ensures high-volume, consistent HPPI output, maintaining strong impurity control to meet East Asia’s stringent ductile iron casting requirements.

High Purity Pig Iron Market Report Scope

High Purity Pig Iron Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.6 Billion

|

|

Market Size (2035)

|

$21.5 Billion

|

|

Market Growth Rate

|

8.4%

|

|

Segments

|

By Product Grade (Foundry Pig Iron, Nodular/Ductile Pig Iron, Basic/Steel Grade Pig Iron, Ultra-Low Impurity Pig Iron), By Casting/Form (Piglets/Ingots, Granulated Pig Iron, Powdered Pig Iron), By End-Use Application (Automotive & Transportation, Specialty Steel Production, Machinery & Equipment Castings, Energy & Infrastructure Components)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Rio Tinto (QIT-Fer et Titane), Eramet, Tronox, Richards Bay Minerals, Kobe Steel, Severstal, Vedanta, Jindal Steel & Power, JFE Steel, POSCO, ArcelorMittal, Mineral-Loy, Ironveld, High Purity Iron Inc., China Baowu Steel Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High Purity Pig Iron Market Segmentation

By Product Grade

- Foundry Pig Iron

- Nodular / Ductile Pig Iron

- Basic / Steel Grade Pig Iron

- Ultra-Low Impurity Pig Iron

By Casting / Form

- Piglets / Ingots

- Granulated Pig Iron

- Powdered Pig Iron

By End-Use Industry

- Automotive & Transportation

- Specialty Steel Production

- Machinery & Equipment Castings

- Energy & Infrastructure Components

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in High Purity Pig Iron Market

- Rio Tinto (QIT-Fer et Titane)

- Eramet

- Tronox

- Richards Bay Minerals

- Kobe Steel

- Severstal

- Vedanta

- Jindal Steel & Power

- JFE Steel

- POSCO

- ArcelorMittal

- Mineral-Loy

- Ironveld

- High Purity Iron Inc.

- China Baowu Steel Group.

*- List not Exhaustive

Research Coverage: High Purity Pig Iron (HPPI) Market

In this comprehensive High Purity Pig Iron Market study, USDAnalytics delivers an authoritative assessment of the forces reshaping global demand, supply chains, and metallurgical innovations within ultra-clean iron feedstocks. This report investigates the scaling requirements of ductile iron, precision casting, and next-generation green steelmaking, examining how impurity thresholds, decarbonization mandates, and advanced manufacturing are redefining HPPI adoption across critical industries. It further highlights breakthrough advancements in low-residual chemistry control, the strategic role of HPPI in EAF/H-DRI green steel routes, and the rising influence of OEM-grade specifications that require ppm-level sulfur, phosphorus, and titanium management. Through structured analysis reviews, technology mapping, regional policy evaluation, and supply realignment insights, this report equips decision-makers with deep visibility into evolving product mixes, competitive strategies, and end-use dynamics. By examining cross-industry metallurgical requirements, foundry modernization, and the fast-growing use of HPPI in EV, aerospace, and renewable energy applications, this report is an essential resource for producers, investors, policymakers, and downstream manufacturers seeking reliable intelligence on purity-driven differentiation and long-range growth opportunities within this strategically critical materials market.

Scope Highlights

- By Product Grade: Foundry Pig Iron, Nodular/Ductile Pig Iron, Basic/Steel Grade Pig Iron, Ultra-Low Impurity Pig Iron

- By Casting/Form: Piglets/Ingots, Granulated Pig Iron, Powdered Pig Iron

- By End-Use Industry: Automotive & Transportation, Specialty Steel Production, Machinery & Equipment Castings, Energy & Infrastructure Components

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Timeframe: Historic data 2021–2025 and forecast outlook 2026–2034.

- Company Coverage: Detailed analysis and profiles of 15+ leading HPPI producers.