High Temperature Coatings Market Size, Thermal Protection Demand, and Industrial Heat Resistance Trends (2025–2032)

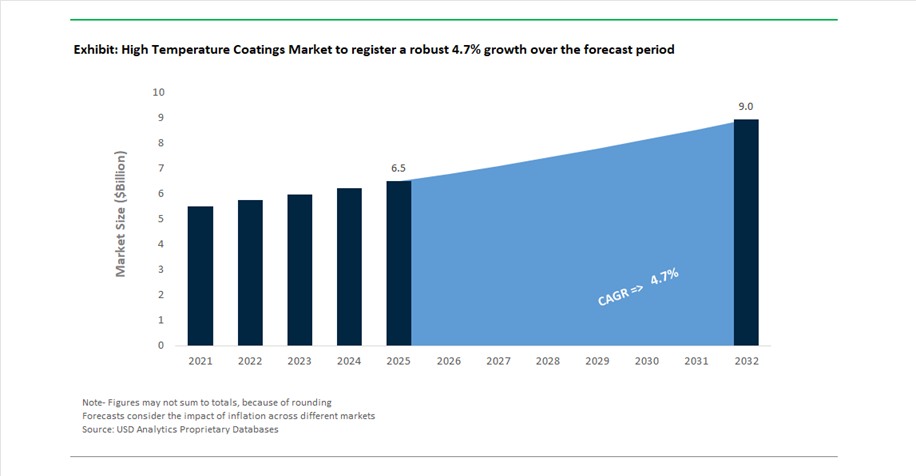

The global high temperature coatings market was valued at $6.5 billion in 2025 and is projected to reach $9 billion by 2032, expanding at a CAGR of 4.7%. Growth is being driven by increasing demand for heat-resistant coatings, thermal barrier coatings, corrosion-resistant coatings, and high-temperature industrial coatings across energy, marine, automotive, and heavy industrial sectors. These coatings are essential in environments where substrates are exposed to extreme heat, oxidation, and thermal cycling, particularly in oil & gas refineries, power plants, offshore platforms, and industrial processing units.

A major market driver is the rising focus on corrosion under insulation (CUI) prevention, which remains a critical operational challenge in high-temperature environments. This has accelerated the adoption of silicone-based coatings, inorganic zinc coatings, epoxy-based high-temperature coatings, and hybrid coating systems designed for long-term durability. Additionally, the expansion of renewable energy infrastructure, hydrogen production systems, and advanced power generation technologies is creating new demand for coatings capable of withstanding elevated temperatures and aggressive chemical exposure.

The market is also benefiting from increased investment in global infrastructure and maritime transport, where marine coatings and passive fire protection coatings are used to enhance asset lifespan and reduce maintenance costs. Regulatory frameworks such as ISO 12944 standards are further influencing product innovation, pushing manufacturers toward low-VOC, high-efficiency coating formulations.

Advanced Coating Technologies, and Energy Sector Expansion Shaping Market Dynamics

The high temperature coatings industry is undergoing a phase of consolidation and technological advancement, with major players focusing on high-performance formulations, energy sector applications, and regional manufacturing expansion. A significant development occurred in February 2026, when AkzoNobel and Axalta announced an all-stock merger of equals, creating a dominant entity in high-performance and high-temperature industrial coatings. This merger combines Axalta’s expertise in high-heat energy resins with AkzoNobel’s International® protective coatings portfolio, strengthening their position in global energy, infrastructure, and industrial markets.

Product innovation remains central to competitive differentiation. In January 2026, Jotun introduced its upgraded Jotatemp coating range, featuring hybrid epoxy technologies designed to withstand extreme thermal cycling and saline offshore conditions, addressing durability challenges in marine and offshore oil platforms. Similarly, PPG Industries’ April 2025 launch of PPG PITT-THERM 909, a silicone-based spray-on insulation coating, represents a significant advancement in CUI mitigation, particularly in complex industrial geometries where traditional insulation systems fail due to moisture entrapment.

Manufacturing expansion and operational efficiency improvements are also shaping the market. In March 2025, Sherwin-Williams expanded its Global Core product line to include high-temperature inorganic zinc and epoxy primers compliant with ISO 12944:2018, ensuring standardized performance across global energy projects. In parallel, PPG’s March 2025 operational milestone involving electrostatic coating application on COSCO Shipping tankers demonstrates the industry's move toward reduced overspray, lower VOC emissions, and higher coating efficiency, with implications for high-temperature coating applications.

Investment in production capacity is aligned with the global energy transition. Hempel A/S reported strong financial growth in February 2025 and announced investments in new manufacturing lines for high-heat coatings, particularly to support renewable energy infrastructure in Europe. Likewise, PPG’s March 2024 facility expansion in the Netherlands is aimed at boosting high-temperature coating production capacity across the EMEA region.

Emerging applications in electric vehicles and advanced materials are also influencing innovation. Zircotec’s ElectroHold® coating, introduced in September 2024, provides thermal barriers up to 1,400°C along with dielectric insulation, addressing thermal runaway risks in EV battery enclosures. Additionally, Kansai Helios’ February 2024 acquisition of WEILBURGER Coatings, including the senotherm® brand, strengthens its position in high-temperature coatings for household appliances and industrial heating systems.

Regional expansion strategies further reinforce market growth. Jotun’s May 2024 production facility in Algeria highlights increasing localization to serve North Africa’s oil, gas, and power sectors, where demand for heat-resistant protective coatings is rising.

Multi-Layer Thermal Barrier Coatings Enabling Hydrogen-Fueled Gas Turbine Performance

The transition toward hydrogen-fueled power generation is fundamentally reshaping the high-temperature coatings landscape, particularly in gas turbine systems exposed to extreme steam-rich combustion environments. Conventional thermal barrier coatings are increasingly inadequate under these conditions, leading to the adoption of advanced multi-layer architectures designed for enhanced phase stability and resistance to water vapor-induced degradation. These next-generation coatings incorporate thicker ceramic topcoats, often reaching up to 1.1 mm, enabling operation at temperatures approaching 2,000°C while maintaining a critical thermal gradient that protects underlying superalloy components. Rare-earth-doped zirconate materials are playing a key role in this evolution, offering approximately 30% lower thermal conductivity compared to traditional yttria-stabilized zirconia, which is essential for managing the elevated flame temperatures associated with hydrogen combustion. Additionally, the integration of densified thermally grown oxide layers significantly reduces oxygen diffusion rates by nearly 40%, extending coating lifespan under continuous exposure to high moisture conditions. These systems are engineered to achieve service intervals of up to 30,000 operating hours, even under rapid thermal cycling conditions typical of modern peaking power plants. These advancements are positioning multi-layer thermal barrier coatings as a critical enabler of hydrogen-based energy infrastructure.

Aluminide Diffusion Coatings Extending Lifecycle of Ethylene Cracking Furnaces

The petrochemical industry is increasingly adopting aluminide diffusion coatings for radiant coil protection in ethylene cracking furnaces, replacing conventional liquid-applied coatings that lack durability under extreme thermal conditions. These coatings form a stable aluminum oxide barrier that significantly reduces catalytic coke formation, achieving reductions of 70% to 90% compared to untreated alloys. This improvement allows facilities to extend furnace run lengths from approximately 60 days to over 100 days, directly enhancing throughput and operational efficiency. In addition to coke suppression, aluminide coatings provide strong resistance to carburization by inhibiting carbon diffusion into alloy grain boundaries, resulting in a 40% to 50% increase in component lifespan. Unlike traditional coatings that may degrade during decoking operations, diffusion aluminide systems form an intermetallic bond with the substrate, ensuring durability through repeated high-temperature cleaning cycles. These performance advantages are driving widespread adoption in high-capacity petrochemical plants where minimizing downtime and maximizing operational efficiency are critical.

India’s Green Hydrogen Mission Driving Demand for High-Durability Electrolyzer Coatings

India’s National Green Hydrogen Mission is creating a substantial growth opportunity for high-temperature and corrosion-resistant coatings used in alkaline electrolyzer systems. These systems operate in highly caustic environments, requiring coatings that can withstand prolonged exposure to potassium hydroxide electrolytes while maintaining structural and electrochemical stability. Separator plates and electrodes are being engineered with nickel-based and ceramic coatings capable of achieving operational lifespans exceeding 80,000 hours, a critical requirement for continuous industrial hydrogen production. Performance optimization is also a key focus, with advanced coatings targeting electrolyzer efficiencies above 75% by reducing voltage losses and improving reaction kinetics. Government incentives under large-scale funding programs are accelerating the development of domestic coating supply chains, aligning with national objectives to reduce hydrogen production costs and enhance energy security. As utilization rates increase to meet economic targets, the durability and performance of coating materials are becoming central to the scalability of hydrogen infrastructure.

US VA Mandates Driving Adoption of High-Temperature Silicone Coatings in Boiler Systems

The modernization of healthcare energy infrastructure in the United States is creating a strong demand for high-temperature silicone coatings used in boiler systems and associated piping networks. The Department of Veterans Affairs is implementing updated standards that require coatings capable of withstanding continuous temperatures between 150°C and 370°C, with intermittent spikes up to 650°C. These coatings are essential for mitigating corrosion under insulation, a major contributor to maintenance costs in aging steam systems. Silicone-based coatings provide durable protection against moisture ingress and thermal degradation, significantly extending the service life of carbon steel components. Adhesion performance is a critical requirement, with coatings required to maintain full adhesion under repeated thermal cycling conditions to ensure safety in sensitive healthcare environments. Additionally, compliance with strict VOC limits below 100 grams per liter is driving the adoption of high-solids and waterborne silicone formulations. These regulatory and operational drivers are positioning high-temperature silicone coatings as a key solution in the modernization of institutional energy systems.

High Temperature Coatings Market Share and Segmentation Insights

Market Share by Technology: Solvent-Borne Coatings Lead with 52% Share Due to Extreme Heat Resistance and Industrial Reliability

Solvent-borne coatings dominate the high temperature coatings market with a 52% share in 2025, driven by their proven performance in extreme thermal environments and unmatched substrate adhesion characteristics. Formulations based on silicone, epoxy, and alkyd chemistries are engineered to withstand continuous and cyclic temperatures ranging from 200°C to over 1000°C, making them indispensable for critical industrial applications. These coatings exhibit superior thermal stability, oxidation resistance, and mechanical integrity under prolonged heat exposure, which water-borne and powder coating technologies often fail to sustain. As a result, solvent-borne high temperature coatings are extensively deployed across exhaust systems, industrial furnaces, boilers, pipelines, and engine components where performance failure is not an option. Additionally, their versatility across multiple substrates and compatibility with complex geometries further reinforce their market leadership. Despite increasing regulatory pressure on VOC emissions, the high-performance requirements of end-use industries continue to anchor solvent-borne systems as the dominant technology in the global high temperature coatings market.

Market Share by End-Use Industry: Oil and Gas Sector Captures 28% Share Driven by High-Temperature Corrosion and Fire Protection Needs

The oil and gas industry leads the high temperature coatings market with a 28% share in 2025, reflecting the sector’s exposure to some of the most aggressive thermal and corrosive operating conditions. Assets such as refineries, petrochemical processing units, offshore platforms, pipelines, and storage tanks routinely operate at elevated temperatures while being subjected to corrosive chemicals, pressure fluctuations, and environmental stressors. This necessitates the use of advanced high temperature coatings that provide thermal insulation, corrosion resistance, and critical fire protection capabilities. Intumescent coatings and passive fire protection (PFP) systems are particularly vital in safeguarding structural steel and process vessels, ensuring operational safety and asset integrity. Furthermore, stringent regulatory frameworks such as NORSOK, API, and ISO fire safety standards mandate the adoption of certified coating systems capable of withstanding hydrocarbon fires and extreme heat flux. Coupled with ongoing investments in upstream and downstream infrastructure, especially in the Middle East and North America, the oil and gas sector remains the primary demand engine for high temperature coatings globally.

High Temperature Coatings Market Competitive Landscape: Extreme Heat Protection, Energy Infrastructure Expansion, and Advanced Thermal Coatings Driving Competition

The high temperature coatings market is highly competitive, driven by demand from energy, petrochemical, EV battery, and data center sectors. Leading players are focusing on CUI mitigation, ultra-high-temperature resistance, low-VOC formulations, and rapid-curing technologies to enhance durability, operational efficiency, and compliance with global performance standards.

Sherwin-Williams enhances global industrial coatings with rapid-curing zinc systems and CUI mitigation leadership

The Sherwin-Williams Company is a dominant player in the high temperature coatings market, driven by its expanded Global Core portfolio that standardizes high-performance coatings such as Zinc Clad® 2500 and Macropoxy® 4600 across global operations. Its Heat-Flex® ACE coating remains a critical solution for corrosion under insulation (CUI), preventing failure in aggressive ISO 12944 CX environments. The company has achieved significant operational efficiency with new inorganic zinc primers offering a 45-minute dry-to-handle time and a 2-hour recoat window, accelerating industrial throughput. Its network of over 5,000 stores ensures just-in-time delivery and strong technical support for large-scale projects. Additionally, its Industrial Energy applicator program provides turnkey coating services that reduce downtime by up to 20%. This integration of performance, speed, and service strengthens its leadership in high-temperature coatings.

PPG drives integrated thermal coating systems for data centers and sustainable industrial applications

PPG Industries is strengthening its position in the high temperature coatings market through integrated protective systems and sustainability-driven innovation. In April 2026, the company introduced an end-to-end coating solution for data centers, combining dielectric, insulative, and heat-reflective properties to reduce cooling demand. With $15.9 billion in 2025 revenue and Q1 2026 EPS of $1.83, PPG is capitalizing on growth in industrial and transportation sectors. It remains the only player offering both coating systems and in-house application expertise, enabling faster project execution and improved reliability. 44% of its sales are derived from sustainably advantaged products, including low-VOC coatings compliant with IEEE and UL standards. This combination of performance, sustainability, and integration reinforces its competitive advantage.

AkzoNobel strengthens high-temperature coatings leadership through cold-spray innovation and strategic consolidation

AkzoNobel N.V. is advancing its position in the high temperature coatings market through innovation and strategic consolidation. Its Intertherm 751CSA cold-spray coating provides thermal protection across a wide range from -196°C to 650°C without requiring heat curing, simplifying application for large-scale piping projects. The company is progressing toward a $25 billion merger with Axalta, aimed at creating a global leader in performance coatings. It continues to optimize its portfolio by divesting non-core assets, including its Pakistan unit, to focus on high-margin industrial segments. AkzoNobel achieved a 14.2% adjusted EBITDA margin in 2026, supported by value-driven strategies. This combination of advanced technology and strategic focus enhances its leadership in high-performance coatings.

Axalta accelerates EV battery safety coatings with AI-driven manufacturing and fire-resistant technologies

Axalta Coating Systems is strengthening its competitive position in the high temperature coatings market through innovation in EV battery safety and digital manufacturing. Its Alesta® e-PRO FG Black coating, which won a Gold Edison Award, is engineered to contain thermal runaway at temperatures exceeding 1200°C. The company has introduced TintMaster AI, improving manufacturing efficiency by reducing batch errors and enhancing Right-First-Time performance by up to 29%. Axalta is prioritizing coatings that resist ignition and smoke generation, addressing critical safety requirements in electric vehicles. Strong analyst confidence, reflected in a $33.5 median price target, underscores its growth potential. This focus on safety, efficiency, and innovation positions Axalta as a key player in high-temperature coatings.

Hempel drives sustainable growth in energy and infrastructure coatings with record financial performance

Hempel A/S is enhancing its presence in the high temperature coatings market through strong financial performance and sustainability initiatives. The company achieved a record 18.2% adjusted EBITDA margin and generated €259 million in free cash flow in 2026. Its “Accelerate to Win” strategy focuses on the Energy & Infrastructure segment, which contributes €775 million in revenue. Hempel has reduced Scope 1 and 2 emissions by 70% compared to 2019 and is targeting a 90% reduction by the end of 2026. Its Hempaguard and Avantguard coatings remain industry leaders in corrosion protection, contributing to significant CO2 reductions for customers. This combination of financial strength and sustainability positions Hempel as a leader in advanced coatings.

Jotun strengthens global high-temperature coatings with advanced glass flake systems and regional expansion

Jotun A/S is a major player in the high temperature coatings market, supported by its extensive global footprint with 40 production facilities across 25 countries. The company has commercialized advanced glass flake technologies that improve barrier efficiency by 15%, enhancing performance in subsea and energy infrastructure applications. Its Jotapipe™ and Marathon coatings offer superior adhesion and rapid curing for extreme industrial environments. Jotun is expanding in high-growth regions such as the Middle East and Southeast Asia, where industrialization and infrastructure development are accelerating demand. With strong technical capabilities and regional expansion strategies, Jotun continues to strengthen its position in high-performance thermal coatings.

United States High Temperature Coatings Market: Aerospace Expansion and Infrastructure Modernization Driving Demand

The United States high temperature coatings market is experiencing robust growth, driven by advancements in aerospace engineering, infrastructure rehabilitation, and semiconductor manufacturing. Federal initiatives such as the Infrastructure Investment and Jobs Act have allocated significant funding toward updated energy codes, increasing the adoption of thermal barrier coatings (TBCs) in federal building retrofits. These coatings are critical for enhancing energy efficiency and ensuring long-term durability in high-temperature environments, particularly in industrial and commercial infrastructure.

The aerospace sector remains a key demand driver, with increased aircraft production fueling the need for ceramic-metallic (cermet) coatings capable of withstanding temperatures exceeding 1,000°C in turbine blades. Simultaneously, the expansion of semiconductor fabrication facilities—supported by large-scale investments—has heightened the demand for ultra-low-outgassing heat resistant coatings in cleanroom systems. Technological advancements, including predictive maintenance-enabled coatings for pipelines, are improving operational reliability by monitoring corrosion under insulation (CUI) in real time. Additionally, the widespread adoption of fusion bonded epoxy (FBE) and silicone-hybrid coatings in hydrogen-natural gas pipeline networks highlights the growing role of high temperature coatings in supporting energy transition infrastructure.

China High Temperature Coatings Market: Green Manufacturing Scale-Up and Energy Storage Expansion

China continues to dominate the global high temperature coatings market, leveraging its vast manufacturing ecosystem and strategic focus on sustainable industrial practices. The country is actively transitioning toward water-based and UV-curable coating systems under its long-term Green Manufacturing strategy, significantly reducing reliance on high-VOC formulations. This shift is further supported by government subsidies encouraging energy-efficient coating technologies, particularly UV-cured powder coatings.

The rapid expansion of battery energy storage systems is a major growth catalyst, with large-scale installations driving demand for fire-retardant ceramic coatings that enhance safety by preventing thermal runaway. China’s industrial sector, which accounts for a significant share of global manufacturing output, is increasingly utilizing high-solids epoxy and silicone coatings for heavy machinery and exhaust systems. Technological innovations such as graphene-enhanced coatings are improving heat dissipation in advanced applications like 5G infrastructure. Additionally, the adoption of intumescent coatings in smart city projects and ceramic-metallic coatings in ultra-supercritical power plants underscores China’s leadership in high-temperature industrial coatings for both infrastructure and energy applications.

Germany High Temperature Coatings Market: Hydrogen Infrastructure and Sustainable Coating Innovation

Germany stands as a central hub for high temperature coatings innovation in Europe, driven by its leadership in hydrogen infrastructure and commitment to sustainability. The development of polymer-ceramic hybrid coatings for the European Hydrogen Backbone is a significant milestone, enabling safe and efficient transportation of hydrogen through repurposed natural gas pipelines. These coatings are designed to withstand extreme thermal and chemical stress, making them essential for the evolving energy landscape.

Sustainability initiatives are also shaping the market, with the introduction of bio-based silicone resin binders derived from renewable sources such as linseed and soy. These formulations offer high thermal resistance while remaining solvent-free, aligning with stringent REACH compliance standards. Technological advancements such as UV-LED curing systems are improving manufacturing efficiency by reducing energy consumption in automotive supply chains. Additionally, the development of de-coatable coatings is enabling full material recyclability, supporting circular economy goals. The growing use of photocatalytic coatings to reduce NOx emissions in urban environments further highlights Germany’s role in advancing environmentally responsible high temperature coating solutions.

India High Temperature Coatings Market: Smart City Expansion and Industrial Growth Accelerating Adoption

India is emerging as a high-growth market for high temperature coatings, driven by rapid urbanization, industrial expansion, and government-led initiatives such as the Production Linked Incentive (PLI) schemes. The increasing valuation of the industrial coatings sector reflects strong demand for epoxy and silicone-based coatings used in protecting oil and gas infrastructure from extreme temperatures and corrosion. These coatings are essential for ensuring operational efficiency and longevity in critical industrial applications.

Infrastructure development is a major catalyst, with large-scale projects under the National Infrastructure Pipeline specifying high-reflectivity solar-control coatings for airport construction and other public assets. The rapid expansion of smart cities is further boosting demand for waterborne, low-VOC fire-protection coatings in high-rise commercial buildings. Localized product innovations, including anti-fungal heat-resistant coatings designed for high-humidity coastal regions, are addressing region-specific challenges. Additionally, the expansion of metro rail networks is driving significant adoption of high-performance primers and protective coatings, reinforcing India’s position as a key growth engine in the global high temperature coatings market.

Japan High Temperature Coatings Market: Radiative Cooling Technologies and Precision Engineering Leadership

Japan continues to lead the high temperature coatings market through its focus on precision engineering and advanced material innovations. The commercialization of radiative cooling coatings, showcased at Expo 2025 Osaka, represents a breakthrough in energy-efficient thermal management by enabling passive heat dissipation without external energy input. This innovation is setting new benchmarks for sustainable building technologies and industrial applications.

Advanced nano-coatings are also driving growth, with the development of anti-fogging heat-resistant coatings that maintain near-perfect optical clarity at elevated temperatures. These coatings are widely used in automotive LiDAR systems and medical sensors, where performance reliability is critical. Product innovations such as self-healing polyurethane coatings are enhancing durability in consumer electronics by automatically repairing micro-cracks under thermal stress. Government support for recycled fluoropolymer coatings is promoting circular economy practices, while regulatory mandates for energy-efficient construction are standardizing the use of infrared-reflective coatings in residential buildings. Japan’s dominance in optical fiber coatings further underscores its expertise in high-performance materials for extreme environments.

South Korea High Temperature Coatings Market: Semiconductor Purity and EV Battery Safety Driving Innovation

South Korea is rapidly advancing in the high temperature coatings market, leveraging its strengths in semiconductor manufacturing, aerospace, and energy storage technologies. The expansion of high-purity coating facilities in semiconductor hubs such as Pyeongtaek is driving demand for ultra-high-purity oxide coatings used in wafer processing and cleanroom environments. These coatings are essential for maintaining operational precision and minimizing contamination in advanced chip manufacturing.

The electric vehicle sector is another major growth driver, with leading manufacturers integrating ceramic-infused heat-resistant coatings into battery modules to achieve stringent fire safety standards. Technological advancements such as carbon/silicon carbide (C/SiC) composites capable of withstanding extreme temperatures are supporting aerospace and defense applications. Increased investments in localized production of high-purity precursors are further strengthening the domestic supply chain for advanced coatings. Regulatory updates under K-REACH are ensuring compliance with safety and environmental standards, while the widespread use of fluoropolymer coatings in consumer electronics is enhancing thermal management in high-performance devices such as foldable smartphones powered by advanced processors.

High Temperature Coatings Market Report Scope

High Temperature Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.5 Billion

|

|

Market Size (2032)

|

$9 Billion

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Resin Type (Silicone, Epoxy, Acrylic, Polyester, Alkyd, Ethyl Silicate, High-Performance Thermoplastics, Ceramic), By Technology (Solvent-borne, Water-borne, Powder Coatings, Sol-Gel Technology, Specialty), By Temperature Range (Low-High, Medium-High, Ultra-High, Extreme Heat), By Substrate (Metals, Concrete and Masonry, Advanced Composites, Technical Glass), By End-Use Industry (Energy and Power Generation, Oil and Gas, Automotive and Transportation, Aerospace and Defense, Consumer Goods, Metal Processing and Foundries, Building and Construction), By Use Case (OEM, MRO)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Jotun A/S, Hempel A/S, Axalta Coating Systems Ltd., RPM International Inc., Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., Tnemec Company, Inc., Aremco Products, Inc., Belzona International Ltd., Dampney Company, Inc., KCC Corporation, Teknos Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High Temperature Coatings Market Segmentation

By Resin Type

- Silicone

- Epoxy

- Acrylic

- Polyester

- Alkyd

- Ethyl Silicate

- High-Performance Thermoplastics

- Ceramic

By Technology

- Solvent-borne

- Water-borne

- Powder Coatings

- Sol-Gel Technology

- Specialty

By Temperature Range

- Low-High

- Medium-High

- Ultra-High

- Extreme Heat

By Substrate

- Metals

- Concrete and Masonry

- Advanced Composites

- Technical Glass

By End-Use Industry

- Energy and Power Generation

- Oil and Gas

- Automotive and Transportation

- Aerospace and Defense

- Consumer Goods

- Metal Processing and Foundries

- Building and Construction

By Use Case

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in High Temperature Coatings Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Jotun A/S

- Hempel A/S

- Axalta Coating Systems Ltd.

- RPM International Inc.

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- Tnemec Company, Inc.

- Aremco Products, Inc.

- Belzona International Ltd.

- Dampney Company, Inc.

- KCC Corporation

- Teknos Group

*- List not Exhaustive