Hydrocarbon Fire Intumescent Coating Services Market Size, Offshore Fire Protection Demand, and PFP Solutions Outlook

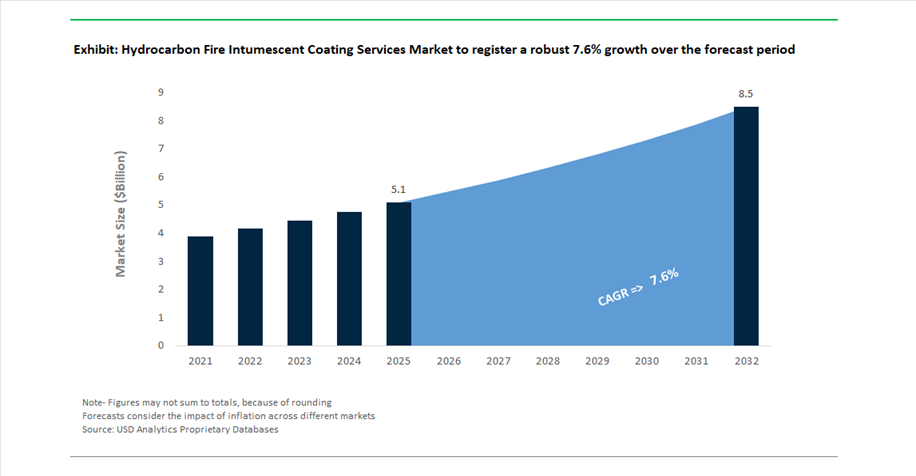

The global hydrocarbon fire intumescent coating services market was valued at $5.1 billion in 2025 and is projected to reach $8.5 billion by 2032, growing at a CAGR of 7.6%. This above-average growth rate reflects the increasing criticality of passive fire protection (PFP) services, particularly in oil & gas, LNG terminals, petrochemical facilities, and offshore platforms, where exposure to hydrocarbon fires, jet fires, and explosion scenarios requires advanced coating solutions and specialized service execution.

A key driver of market expansion is the rising complexity of hydrocarbon processing infrastructure, including deepwater exploration assets, floating production storage units (FPSOs), and green hydrogen and biofuel facilities. These environments demand epoxy intumescent coatings, thermal insulation coatings, and fireproofing services that can withstand rapid temperature escalation, thermal shock, and cryogenic spill conditions. Increasing regulatory scrutiny and updated safety certifications for jet fire protection and CUI-fire synergy performance are further pushing asset owners toward certified, high-performance intumescent coating systems.

The services component of the market is gaining importance as operators prioritize precision application, lifecycle maintenance, digital inspection, and compliance management. The adoption of off-site modular coating application, digital fire protection modeling, and dry film thickness (DFT) optimization tools is enhancing project efficiency and reducing operational risks.

PFP Mega-Merger, Digital Fire Protection Services, and Energy Transition Driving Market Transformation

The hydrocarbon fire intumescent coating services industry is undergoing rapid transformation driven by consolidation, advanced coating technologies, and service-led innovation. A major inflection point occurred in February 2026, when AkzoNobel and Axalta announced a mega-merger, creating a dominant player in the passive fire protection (PFP) services sector. The integration of Axalta’s high-heat resin technologies with AkzoNobel’s Chartek product portfolio—widely regarded as a benchmark in offshore hydrocarbon fire protection coatings—is expected to significantly strengthen capabilities in high-risk energy infrastructure projects.

Product innovation continues to elevate performance standards in hydrocarbon fire scenarios. In November 2025, Jotun launched Jotachar 1709XT at ADIPEC, a next-generation epoxy intumescent coating engineered for hydrocarbon fire and explosion conditions. The formulation enables faster film build and improved application efficiency, particularly in high ambient temperature environments typical of Middle Eastern operations. Supporting this expansion, Jotun also commissioned a new production line in Oman with a capacity of 2.4 million liters annually, strategically positioned to serve Saudi Arabia and UAE giga-projects, reducing lead times for regional operators.

Service innovation is becoming a critical differentiator. In August 2025, PPG Industries introduced an advanced PFP Digital Support Suite, enabling engineers to calculate precise dry film thickness (DFT) requirements for complex hydrocarbon fire scenarios in real time. This reflects a broader industry shift toward digitized fire protection engineering, predictive modeling, and compliance optimization. Similarly, Sherwin-Williams enhanced its FIRETEX M90/02 system in June 2025, enabling off-site coating application for modular steel structures, significantly reducing on-site labor, improving coating quality, and accelerating project timelines.

Strategic pivots toward emerging energy segments are also reshaping the market. Hempel A/S, following strong financial performance in March 2025, announced a focus on “renewable hydrocarbons”, including fire protection services for green hydrogen and biofuel processing plants, which present unique fire risk profiles compared to conventional hydrocarbons. In parallel, AkzoNobel’s January 2025 certification milestone for Chartek 1709—becoming the first system approved for jet fire protection in cryogenic spill scenarios—addresses critical safety requirements for LNG terminal infrastructure.

Earlier product developments continue to influence market positioning. PPG’s STEELGUARD 951, introduced globally in September 2024, offers up to three hours of hydrocarbon fire protection while resisting thermal shock, making it suitable for industrial steel structures. Sherwin-Williams’ FIRETEX FX7002, launched in March 2024, extends application into fringe hydrocarbon environments such as fuel storage facilities and transport hubs, broadening the scope of intumescent coating services.

Jet Fire-Rated Intumescent Coatings Becoming Mandatory in LNG Infrastructure

The hydrocarbon fire intumescent coatings services market is undergoing a critical shift as LNG infrastructure projects adopt mandatory jet fire-rated specifications to address high-intensity fire scenarios. Unlike conventional hydrocarbon pool fires, jet fires generate extreme heat flux levels of 250–300 kW/m² combined with high-velocity erosive forces, requiring specialized epoxy intumescent coatings engineered for structural resilience. Modern systems are designed to withstand pressurized gas releases equivalent to 14 MW flames for durations up to 120 minutes, ensuring structural steel integrity under catastrophic failure scenarios. A key advancement is the integration of dual-purpose protection capabilities, where coatings provide both jet fire resistance and cryogenic spill protection down to −196°C, preventing brittle fracture during LNG leaks. Performance specifications now mandate limiting steel substrate temperatures to approximately 400°C, significantly below thresholds associated with structural weakening. Additionally, the adoption of updated ISO 22899-3 testing protocols has intensified qualification requirements, with over 75% of LNG projects specifying coatings that pass extended jet fire erosion tests to prevent coating sloughing under pressure. These stringent performance benchmarks are positioning advanced intumescent coatings as a critical safety component in global LNG expansion projects.

Shift Toward Off-Site Modular Application of Intumescent Coatings for Refinery Turnarounds

The industry is increasingly adopting off-site, shop-applied intumescent coating strategies to improve efficiency and safety during refinery turnarounds and large-scale energy projects. Modularization enables coating application in controlled environments, eliminating the variability associated with on-site conditions such as weather and limited access in congested facilities. This approach delivers significant operational benefits, including a 30% to 40% reduction in application timelines and the completion of up to 90% of fireproofing work before installation. From a performance perspective, shop-applied coatings achieve 15% to 20% higher bond strength due to optimized curing conditions, reducing the risk of delamination during transport and installation. Safety improvements are equally important, with reduced on-site labor exposure lowering the likelihood of incidents in high-risk refinery environments. Economically, modular fireproofing strategies have demonstrated total project cost reductions of up to 12%, driven by the elimination of scaffolding, containment systems, and extended shutdown periods. These advantages are accelerating the adoption of modular coating services as a standard practice in modern refinery and petrochemical infrastructure projects.

Saudi Aramco IKTVA Program Driving Localization of Fireproofing Coating Services

Saudi Arabia’s In-Kingdom Total Value Add program is creating a substantial opportunity for localized hydrocarbon fire protection coating services. With a target of achieving 70% to 75% local content by 2026, the program is reshaping procurement strategies in favor of companies that establish in-country application and testing capabilities. Approximately 70% of procurement spending is now linked to local content performance, making localization a critical factor for securing major contracts in large-scale projects such as industrial complexes and maritime infrastructure developments. The initiative is also fostering collaboration between global coating manufacturers and local service providers, particularly for compliance with stringent application standards. Additionally, there is a growing demand for certified inspection personnel, with requirements for over 1,000 locally accredited inspectors to ensure quality assurance and regulatory compliance. Training programs and certification initiatives are expanding rapidly to support workforce development, aligning with broader national objectives for job creation and industrial diversification. These dynamics are positioning localized fireproofing services as a strategic growth segment in the Middle East energy sector.

US EPA RMP Revisions Expanding Demand for Intumescent Coatings Across Chemical Facilities

Recent updates to the United States Environmental Protection Agency’s Risk Management Program are significantly expanding the addressable market for hydrocarbon fire intumescent coatings beyond large-scale facilities to include smaller chemical operations. The revised framework now applies to approximately 12,000 facilities, many of which are required to conduct Safer Technology and Alternatives Analyses that frequently identify passive fire protection systems as a key risk mitigation measure. Facilities with repeated incident histories are subject to mandatory third-party audits, often resulting in requirements to retrofit existing infrastructure with UL 1709-rated hydrocarbon fire coatings. This is driving increased adoption of intumescent coatings for pipe racks, storage vessels, and structural supports to prevent fire escalation and protect surrounding communities. Additionally, enhanced data transparency through public reporting tools is increasing pressure from regulators, insurers, and local stakeholders for demonstrable safety improvements. These regulatory developments are creating a sustained demand pipeline for fireproofing coating services, particularly in retrofit and compliance-driven applications across the chemical processing industry.

Hydrocarbon Fire Intumescent Coating Services Market Share 2025: New Build Applications and 120-Minute Ratings Lead Demand

Service Type Insights: New Build Application Dominates in Large-Scale Energy Infrastructure Projects

The new build application segment leads the hydrocarbon fire intumescent coating services market with a 42% market share in 2025, driven by the surge in capital-intensive oil & gas, LNG, and petrochemical infrastructure projects. Major developments such as offshore platforms, LNG terminals, refineries, and storage tank farms require high-performance hydrocarbon fire intumescent coatings on structural steel as a core safety specification during initial construction. A key growth factor is the preference for project bundling by EPC (Engineering, Procurement, and Construction) contractors, who integrate coating application with steel fabrication processes. This ensures consistent dry film thickness (typically 2–8mm), certified fire protection performance, and streamlined installation timelines before components are transported on-site. As global investments in energy infrastructure and industrial expansion continue, new build applications will remain the primary revenue driver in the hydrocarbon fire protection coatings services market.

Fire Protection Rating Insights: 120-Minute Protection Standard Drives Market Adoption

The 120 minutes (2 hours) fire protection rating segment dominates the market with a 45% share in 2025, reflecting its status as the industry standard for hydrocarbon fire scenarios. Leading specifications such as NORSOK, API standards, and Shell DEP guidelines mandate 120-minute jet fire or pool fire resistance for critical assets including structural supports, vessels, and pipe racks in oil & gas facilities. This rating provides an optimal balance between safety performance and cost efficiency, ensuring sufficient time for emergency response and structural integrity under extreme fire exposure. While higher ratings beyond 120 minutes are available, they typically require significantly thicker coatings (often exceeding 10mm) or complex multi-layer systems with ceramic insulation, resulting in sharply increased material and labor costs. Consequently, most operators standardize on 120-minute protection as the most practical solution, reinforcing its dominance in the hydrocarbon fire intumescent coating services market.

Hydrocarbon Fire Intumescent Coating Services Market Competitive Landscape: Jet Fire Protection, LNG Safety, and High-Performance Epoxy Systems Driving Competition

The hydrocarbon fire intumescent coating services market is highly competitive, driven by demand from LNG terminals, petrochemical facilities, and energy infrastructure. Leading players are focusing on lightweight epoxy PFP systems, mesh-free technologies, and rapid-application solutions to enhance fire resistance, reduce installation time, and meet stringent UL and ISO standards.

AkzoNobel leads global hydrocarbon fire protection with Chartek® innovation and mesh-free technology

AkzoNobel N.V. is a dominant leader in hydrocarbon fire intumescent coatings, leveraging its Chartek® portfolio as the global benchmark for passive fire protection. With over 6 million square meters of steel protected worldwide, the company holds an estimated 18% market share. The launch of Chartek 1620CSP delivers dual protection against hydrocarbon fires and cryogenic LNG spills, addressing critical safety requirements in energy infrastructure. Its Chartek 7E system provides up to 2 hours of jet fire resistance while reducing installed weight by 30% compared to legacy systems. The Chartek 8E mesh-free technology eliminates reinforcing mesh for up to 60-minute protection, reducing labor costs by 25%. The ongoing $25 billion merger with Axalta further strengthens its leadership in global PFP solutions.

PPG advances lightweight epoxy intumescent systems with superior jet fire and blast resistance

PPG Industries is strengthening its competitive position in hydrocarbon fire coatings through advanced epoxy intumescent systems and rapid application technologies. Its PITT-CHAR® NX system is at least 15% lighter than conventional epoxy PFP coatings while achieving a 2-hour UL 1709 rating at just 7.98 mm thickness. The coating is engineered for jet fire and explosion resistance, flexing with steel structures to prevent delamination during blast events. PPG’s “Safer, Tougher, Faster” strategy enables full PFP system application within a single day, improving project efficiency. The company operates a UL-certified Global Protection Technology Center for real-time fire scenario testing and formulation customization. This integration of performance, testing, and efficiency positions PPG as a leader in high-performance fire protection coatings.

Sherwin-Williams expands FIRETEX® portfolio with high-duration protection and low-VOC epoxy innovation

The Sherwin-Williams Company is enhancing its presence in hydrocarbon fire intumescent coatings through innovation and global service capabilities. Its FIRETEX® M90 series provides up to 4 hours of hydrocarbon pool fire protection for critical onshore and offshore infrastructure. The company introduced FIRETEX FX6010, a single-spray application system designed to simplify installation in large infrastructure projects such as transport hubs. Sherwin-Williams is developing low-VOC epoxy intumescents at its new global R&D center in Cleveland, targeting compliance with C5 high-corrosion standards. Its extensive network of over 5,000 stores enables on-site technical support, thickness verification, and compliance auditing for EPC contractors. This combination of innovation, service, and scale strengthens its competitive position.

Jotun accelerates project efficiency with mesh-free intumescent systems and large-scale energy contracts

Jotun A/S is a key player in hydrocarbon fire protection coatings, driven by innovation in mesh-free epoxy intumescent systems. Its Jotachar JF750 coating provides protection against both jet fires and pool fires within a single system, reducing application time by up to 60%. The company reported record revenue of NOK 34.33 billion in 2026, supported by strong demand in energy infrastructure projects. Jotun is capturing significant market share in the Middle East and Asia-Pacific, particularly in projects such as the Saudi Aramco Master Gas System. Its sustainability initiatives include a 70% reduction in Scope 1 and 2 emissions and a transition toward solvent-free PFP solutions for hydrogen projects. This focus on efficiency, scale, and sustainability reinforces its leadership in intumescent coatings.

Hempel strengthens energy infrastructure coatings with high-efficiency intumescent systems and sustainability focus

Hempel A/S is expanding its role in the hydrocarbon fire intumescent coatings market through performance-driven solutions and sustainability initiatives. Its Hempafire Extreme 550 system delivers high-build protection with predictable drying cycles, minimizing handling damage during transport. The rollout of Hempafire Pro 400 improves application efficiency through reduced material consumption and faster drying times. Hempel achieved a record 18.2% EBITDA margin in 2026, supported by strong growth in its Energy & Infrastructure segment. The company is integrating emissions-based supplier screening into procurement processes, aligning with global climate targets. This combination of operational efficiency and sustainability strengthens its position in advanced fire protection coatings.

Kansai Paint expands Asia-Pacific dominance with localized hydrocarbon fire protection solutions

Kansai Paint Co., Ltd. is a leading regional player in hydrocarbon fire intumescent coatings, particularly in Asia-Pacific where it accounts for 30% of the global PFP market. The company has expanded its footprint through the amalgamation with Nerofix, strengthening its presence in industrial fireproofing and construction chemicals. Its Thermoset Hydrocarbon Shield coating is designed for refinery furnaces and high-temperature processing environments, addressing critical safety needs. Kansai Paint’s backward integration into epoxy resins enables stable pricing despite raw material volatility in 2026. The company is targeting India’s growing LNG and chemical infrastructure sectors with localized coating services. This regional strength and integration position Kansai Paint as a key player in emerging markets.

Saudi Arabia Hydrocarbon Fire Intumescent Coating Services Market: Vision 2030 Megaprojects Driving Industrial Fireproofing Demand

Saudi Arabia stands as the most active global hub for hydrocarbon fire intumescent coating services, fueled by massive investments in oil & gas infrastructure under Vision 2030. The expansion of the Master Gas System and large-scale developments such as the Jafurah Gas Development Phase 2 are significantly increasing demand for thick-film epoxy intumescent coatings across processing facilities and NGL plants. These coatings are essential for ensuring structural integrity under extreme hydrocarbon fire scenarios, particularly in high-risk petrochemical environments.

Regulatory standardization is a key growth driver, with Saudi Aramco mandating advanced intumescent systems with UL/JET certification to achieve extended fire resistance ratings for offshore assets. Technological advancements such as robotic spray applications are enhancing coating uniformity and efficiency across long pipeline networks, especially in extreme desert conditions. Additionally, stricter inspection requirements under the updated Saudi Building Code are increasing demand for certified coating inspection services. The expansion of localized training centers and innovation hubs is further strengthening domestic capabilities, positioning Saudi Arabia as a leader in industrial fireproofing services for hydrocarbon facilities.

India Hydrocarbon Fire Intumescent Coating Services Market: Gas Grid Expansion and Ethanol Infrastructure Boosting Demand

India is witnessing rapid growth in the hydrocarbon fire intumescent coating services market, driven by large-scale energy infrastructure expansion and clean fuel initiatives. The “One Nation, One Gas Grid” program has significantly increased the length of the natural gas pipeline network, resulting in a surge in service tenders for fireproofing valves, actuators, and pipeline components. This growth is further supported by the country’s ethanol blending targets, which are accelerating the construction of integrated energy storage and distribution facilities requiring specialized fire protection coatings.

Regulatory enforcement is playing a crucial role, with updated petroleum and natural gas rules mandating fire safety audits across thousands of CNG stations. This has triggered widespread retrofitting of existing infrastructure with intumescent coatings to enhance fire resistance. The presence of global coating companies establishing regional support teams is improving compliance and technical expertise across diverse state regulations. Additionally, localized product innovations designed for high-humidity coastal environments are addressing region-specific challenges. The growing adoption of thin-film intumescent coatings in decentralized LNG stations and industrial plants further underscores India’s emergence as a key growth market for fireproof coating services.

United States Hydrocarbon Fire Intumescent Coating Services Market: Shale Gas Expansion and Advanced Fire Protection Standards

The United States hydrocarbon fire intumescent coating services market is evolving rapidly, driven by the resurgence of shale gas exploration and stricter fire safety standards in industrial facilities. The implementation of API Recommended Practice 752 has transformed fire risk assessment in refineries, necessitating the use of advanced hybrid intumescent-ablative coating systems for enhanced thermal protection of critical infrastructure.

Product innovation is accelerating market growth, with leading manufacturers introducing high-performance coatings designed to withstand aggressive operating conditions in regions such as the Permian Basin. The expansion of shale gas drilling and associated repair services is increasing demand for coatings capable of maintaining adhesion under extreme thermal and cryogenic stress. Additionally, federal investments in hydrogen recovery units are creating new opportunities for coatings that can endure high-temperature jet fires. Technological advancements such as mobile spray-on insulation systems are improving on-site application efficiency, while the adoption of lightweight thin-film coatings in aerospace and EV battery applications highlights the expanding scope of hydrocarbon fire protection technologies in the U.S.

Norway Hydrocarbon Fire Intumescent Coating Services Market: Arctic-Grade Innovation and CCS Infrastructure Leadership

Norway continues to lead the global hydrocarbon fire intumescent coating services market through its focus on offshore innovation and carbon capture and storage (CCS) infrastructure. The deployment of specialized coatings for supercritical CO₂ transport vessels is a key development, requiring materials that can maintain flexibility and performance under extreme temperature fluctuations during liquefied CO₂ handling.

Technological advancements in harsh-environment coatings are driving market growth, with new product launches offering enhanced resistance to jet fires, cryogenic conditions, and salt-spray exposure. The tightening of regulatory inspection cycles for offshore assets is also boosting demand for maintenance and repair coating services. Innovations such as intelligent coatings embedded with fiber-optic sensors are enabling real-time monitoring of structural integrity under thermal stress, enhancing safety and operational efficiency. Additionally, the shift toward halogen-free and low-VOC formulations aligns with European sustainability directives, reinforcing Norway’s leadership in environmentally compliant fire protection solutions.

China Hydrocarbon Fire Intumescent Coating Services Market: Industrial Safety Mandates and Energy Storage Growth

China remains the volume leader in the hydrocarbon fire intumescent coating services market, driven by its vast industrial base and stringent safety regulations. The implementation of national standards for energy storage systems is mandating the use of advanced coatings that prevent thermal propagation in high-density battery installations, significantly increasing demand for silicone-rich and ceramic-intumescent hybrid coatings.

Government directives aimed at improving industrial safety are requiring the widespread use of thick-film intumescent coatings in hazardous chemical zones, particularly in large-scale industrial parks. The rapid expansion of electric vehicle manufacturing is further driving innovation in coating technologies designed for high-voltage battery systems. Strategic partnerships between global and domestic players are facilitating the deployment of advanced intumescent coatings across marine and industrial applications. Additionally, the integration of fire safety systems with building management technologies is enhancing monitoring and compliance in petrochemical facilities, supporting sustained market growth in China.

United Kingdom Hydrocarbon Fire Intumescent Coating Services Market: Post-Grenfell Compliance and Industrial Decarbonization

The United Kingdom hydrocarbon fire intumescent coating services market is undergoing a major transformation, driven by stricter building safety regulations and increased focus on fire protection in high-risk environments. Regulatory updates following recent safety reforms have introduced mandatory third-party testing for fire protection coatings used in residential and commercial buildings, significantly raising industry standards.

Industrial decarbonization initiatives are also fueling demand, particularly in regions such as Teesside and Humber, where investments in hydrogen production facilities require advanced fire protection solutions. Technological advancements in waterborne intumescent coatings are enabling compliance with stringent VOC limits while maintaining high fire resistance performance. Market consolidation through acquisitions is streamlining service delivery, offering integrated solutions from specification to certification. Additionally, the use of advanced hybrid coating systems for subsea equipment and critical infrastructure is expanding application areas, reinforcing the UK’s position as a key market for high-performance fire protection coatings.

Hydrocarbon Fire Intumescent Coating Services Market Report Scope

Hydrocarbon Fire Intumescent Coating Services Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.1 Billion

|

|

Market Size (2032)

|

$8.5 Billion

|

|

Market Growth Rate

|

7.6%

|

|

Segments

|

By Service Type (New Build Application, Maintenance and Repair, Turnkey Fire Protection Services, Inspection and Certification Services), By Coating (Thick-Film Epoxy Intumescent, Thin-Film Intumescent, Solvent-borne Services, Water-borne Services, Solvent-free), By End-Use Industry (Upstream Oil and Gas, Downstream Oil and Gas, Chemicals and Pharmaceuticals, Metals and Mining, Power Generation, Marine and Shipbuilding), By Application Environment (Onshore Facilities, Offshore and Marine Environments, High-Humidity, Extreme Temperature Environments), By Fire Protection Rating (Up to 60 Minutes, 90 Minutes, 120 Minutes, Beyond 120 Minutes)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Jotun A/S, Hempel A/S, RPM International Inc., Sika AG, Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., KCC Corporation, 3M Company, Isolatek International, Promat International, Mattr, Arabian Vermiculite Industries

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hydrocarbon Fire Intumescent Coating Services Market Segmentation

By Service Type

- New Build Application

- Maintenance and Repair

- Turnkey Fire Protection Services

- Inspection and Certification Services

By Coating

- Thick-Film Epoxy Intumescent

- Thin-Film Intumescent

- Solvent-borne Services

- Water-borne Services

- Solvent-free

By End-Use Industry

- Upstream Oil and Gas

- Downstream Oil and Gas

- Chemicals and Pharmaceuticals

- Metals and Mining

- Power Generation

- Marine and Shipbuilding

By Application Environment

- Onshore Facilities

- Offshore and Marine Environments

- High-Humidity

- Extreme Temperature Environments

By Fire Protection Rating

- Up to 60 Minutes

- 90 Minutes

- 120 Minutes

- Beyond 120 Minutes

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Hydrocarbon Fire Intumescent Coating Services Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Jotun A/S

- Hempel A/S

- RPM International Inc.

- Sika AG

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- KCC Corporation

- 3M Company

- Isolatek International

- Promat International

- Mattr

- Arabian Vermiculite Industries

*- List not Exhaustive