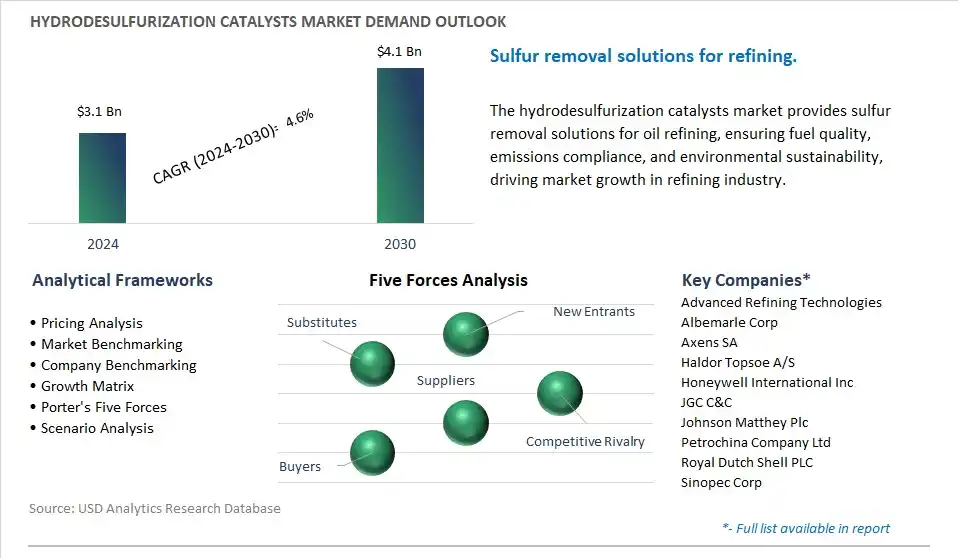

The global Hydrodesulfurization Catalysts Market is poised to register a 4.6% CAGR from $3.1 Billion in 2024 to $4.1 Billion in 2030.

The global Hydrodesulfurization Catalysts Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Load Type, Non-Load Type), By Application (Diesel, Naphtha, Others).

An Introduction to Global Hydrodesulfurization Catalysts Market in 2024

Hydrodesulfurization (HDS) catalysts are essential components in the petroleum refining industry for removing sulfur compounds from crude oil and intermediate products, ensuring compliance with environmental regulations and improving the quality of fuels such as gasoline, diesel, and jet fuel. One key trend shaping the future of hydrodesulfurization catalysts is the development of catalyst formulations and process technologies to meet increasingly stringent sulfur content specifications while maximizing conversion efficiency and minimizing energy consumption and environmental impact. Catalyst manufacturers are innovating new catalytic materials, active phases, and support structures to enhance HDS activity, selectivity, and stability under challenging operating conditions, including high temperatures, pressures, and sulfur levels. Additionally, advancements in catalyst synthesis methods, surface modification techniques, and reactor design are optimizing catalyst performance, particle size distribution, and attrition resistance, ensuring reliable and cost-effective sulfur removal in refinery units. Moreover, the integration of advanced analytics, modeling software, and pilot-scale testing facilities is enabling predictive modeling and optimization of HDS processes, facilitating catalyst selection, regeneration, and lifecycle management strategies for refinery operators. As refineries seek to produce cleaner and higher-quality fuels while minimizing environmental impact and operating costs, the hydrodesulfurization catalysts industry is poised for innovation and growth, with opportunities for collaboration, technology transfer, and market expansion to meet the evolving needs of the refining sector and regulatory requirements.

Hydrodesulfurization Catalysts Market Competitive Landscape

The market report analyses the leading companies in the industry including Advanced Refining Technologies, Albemarle Corp, Axens SA, Haldor Topsoe A/S, Honeywell International Inc, JGC C&C, Johnson Matthey Plc, Petrochina Company Ltd, Royal Dutch Shell PLC, Sinopec Corp.

Hydrodesulfurization Catalysts Market Dynamics

Hydrodesulfurization Catalysts Market Trend: Increasing Stringency of Environmental Regulations for Sulfur Emissions

A prominent trend in the market for Hydrodesulfurization Catalysts is the increasing stringency of environmental regulations aimed at reducing sulfur emissions from fuels and industrial processes. With growing concerns about air pollution, acid rain, and health impacts associated with sulfur dioxide emissions, governments worldwide are implementing stricter emissions standards for sulfur-containing fuels such as diesel and gasoline. Hydrodesulfurization catalysts play a critical role in removing sulfur compounds from hydrocarbon streams by catalyzing the conversion of sulfur-containing molecules into hydrogen sulfide, which can then be captured and processed. This is driven by regulatory mandates to lower sulfur content in fuels, advancements in catalyst technology to improve sulfur removal efficiency, and the need for cleaner and more sustainable energy sources, leading to increased demand for hydrodesulfurization catalysts in refining and petrochemical industries.

Hydrodesulfurization Catalysts Market Driver: Growing Demand for Clean Fuels and Compliance with Fuel Quality Standards

The market for Hydrodesulfurization Catalysts is being driven by the growing demand for clean fuels and compliance with fuel quality standards worldwide. As economies develop and urban populations increase, there is a rising need for transportation fuels with reduced sulfur content to mitigate air pollution and improve public health. Hydrodesulfurization catalysts enable refiners to produce ultra-low sulfur diesel (ULSD) and gasoline that meet regulatory specifications for sulfur content, emissions limits, and engine performance. Factors such as urbanization, vehicle electrification trends, and the transition to cleaner energy sources drive investments in hydrodesulfurization capacity and technology upgrades, fueling market growth and adoption in the oil refining and fuel production sectors.

Hydrodesulfurization Catalysts Market Opportunity: Development of Next-Generation Catalyst Formulations and Technologies

An exciting opportunity within the market for Hydrodesulfurization Catalysts lies in the development of next-generation catalyst formulations and technologies that offer improved sulfur removal efficiency, catalyst activity, and selectivity while minimizing energy consumption and environmental footprint. Companies can explore opportunities to innovate in catalyst design, composition, and manufacturing processes to enhance catalyst performance and durability under harsh operating conditions in refineries and petrochemical plants. Additionally, there is potential to develop catalysts tailored for specific feedstocks, sulfur species, and process conditions to optimize sulfur removal efficiency and minimize catalyst deactivation. By leveraging their expertise in catalyst research, materials science, and chemical engineering, companies can capitalize on the growing demand for advanced hydrodesulfurization catalysts and position themselves as leaders in providing innovative solutions for cleaner and more sustainable energy production, driving growth and differentiation in the hydrodesulfurization catalysts market.

Hydrodesulfurization Catalysts Market Ecosystem

The hydrodesulfurization (HDS) catalyst market operates through diverse interconnected stages, each with specific companies contributing to the production and distribution of these essential catalysts. Research and development efforts led by institutions including BASF SE and Haldor Topsoe focus on advancing catalyst formulations for improved efficiency and performance. Catalyst manufacturing companies including BASF SE and Albemarle Corporation produce a range of HDS catalysts, including specialty formulations tailored for specific feedstocks.

Specialty catalyst producers including Clariant and Sud Chemie offer high-performance HDS catalysts designed to meet unique refining requirements. Distribution channels are facilitated through oilfield services companies including Schlumberger and Halliburton, which distribute HDS catalysts alongside broader oil and gas processing equipment and services. Further, oil refineries serve as the primary end users, employing HDS catalysts in hydrodesulfurization units to produce cleaner fuels with reduced sulfur content, highlighting the critical role of these catalysts in refining processes and environmental stewardship.

Hydrodesulfurization Catalysts Market Share Analysis: Non-Load held the dominant revenue share in 2024

The largest segment in the Hydrodesulfurization Catalysts Market is the Non-Load Type segment. This dominance is primarily due to diverse key factors. Non-load type hydrodesulfurization catalysts consist of active metal oxides supported on an inert substrate, such as alumina or silica-alumina. These catalysts are widely used in the petroleum refining industry for the removal of sulfur compounds from crude oil and petroleum products. Additionally, non-load type catalysts offer diverse advantages over load type catalysts, including higher catalytic activity, selectivity, and stability under harsh operating conditions. In addition, non-load type catalysts exhibit excellent resistance to poisoning by contaminants such as metals, nitrogen compounds, and aromatics, ensuring long-term catalyst performance and operational efficiency in hydrodesulfurization processes. Further, advancements in catalyst formulation, manufacturing processes, and support materials further enhance the performance and reliability of non-load type catalysts, making them a preferred choice for hydrodesulfurization applications in the refining industry. Overall, the Non-Load Type segment holds the largest share in the Hydrodesulfurization Catalysts Market due to its superior performance, versatility, and widespread use in petroleum refining operations for sulfur removal.

Hydrodesulfurization Catalysts Market Share Analysis: Diesel is the fastest growing market segment over the forecast period to 2030

The fastest-growing segment in the Hydrodesulfurization Catalysts Market is the Diesel application segment. This growth is primarily due to diverse key factors. Firstly, diesel fuels play a critical role in various sectors such as transportation, industrial, and agricultural machinery, making them one of the most widely consumed petroleum products globally. As environmental regulations become increasingly stringent, there is a growing emphasis on reducing sulfur emissions from diesel fuels to comply with regulatory standards and mitigate environmental pollution. Hydrodesulfurization catalysts are essential for removing sulfur compounds, such as sulfur oxides (SOx) and hydrogen sulfide (H2S), from diesel fuels, thereby reducing sulfur content to meet regulatory limits. Additionally, the demand for ultra-low sulfur diesel (ULSD) is increasing globally, driven by regulatory mandates aimed at improving air quality and reducing emissions of sulfur dioxide (SO2), particulate matter, and nitrogen oxides (NOx). In addition, the shift toward cleaner and more efficient diesel engines, including diesel-electric hybrids and diesel particulate filters (DPF), further amplifies the need for high-performance hydrodesulfurization catalysts to ensure optimal engine performance and emissions control. Further, technological advancements in catalyst design, composition, and manufacturing processes enhance the efficiency, activity, and stability of hydrodesulfurization catalysts, enabling them to meet the stringent performance requirements of modern diesel refining operations. Overall, the Diesel application segment is experiencing rapid growth in the Hydrodesulfurization Catalysts Market due to increasing demand for clean diesel fuels, regulatory compliance, and advancements in catalyst technology to address environmental challenges and ensure sustainable energy solutions.

Hydrodesulfurization Catalysts Market Report Scope-

By Type

Load Type

Non-Load Type

By Application

Diesel

Naphtha

Others

Hydrodesulfurization Catalysts Market Companies Profiled

Advanced Refining Technologies

Albemarle Corp

Axens SA

Haldor Topsoe A/S

Honeywell International Inc

JGC C&C

Johnson Matthey Plc

Petrochina Company Ltd

Royal Dutch Shell PLC

Sinopec Corp

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Hydrodesulfurization Catalysts Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Hydrodesulfurization Catalysts Market Size Outlook, $ Million, 2021 to 2030

3.2 Hydrodesulfurization Catalysts Market Outlook by Type, $ Million, 2021 to 2030

3.3 Hydrodesulfurization Catalysts Market Outlook by Product, $ Million, 2021 to 2030

3.4 Hydrodesulfurization Catalysts Market Outlook by Application, $ Million, 2021 to 2030

3.5 Hydrodesulfurization Catalysts Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Hydrodesulfurization Catalysts Industry

4.2 Key Market Trends in Hydrodesulfurization Catalysts Industry

4.3 Potential Opportunities in Hydrodesulfurization Catalysts Industry

4.4 Key Challenges in Hydrodesulfurization Catalysts Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Hydrodesulfurization Catalysts Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Hydrodesulfurization Catalysts Market Outlook by Segments

7.1 Hydrodesulfurization Catalysts Market Outlook by Segments, $ Million, 2021- 2030

By Type

Load Type

Non-Load Type

By Application

Diesel

Naphtha

Others

8 North America Hydrodesulfurization Catalysts Market Analysis and Outlook To 2030

8.1 Introduction to North America Hydrodesulfurization Catalysts Markets in 2024

8.2 North America Hydrodesulfurization Catalysts Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Hydrodesulfurization Catalysts Market size Outlook by Segments, 2021-2030

By Type

Load Type

Non-Load Type

By Application

Diesel

Naphtha

Others

9 Europe Hydrodesulfurization Catalysts Market Analysis and Outlook To 2030

9.1 Introduction to Europe Hydrodesulfurization Catalysts Markets in 2024

9.2 Europe Hydrodesulfurization Catalysts Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Hydrodesulfurization Catalysts Market Size Outlook by Segments, 2021-2030

By Type

Load Type

Non-Load Type

By Application

Diesel

Naphtha

Others

10 Asia Pacific Hydrodesulfurization Catalysts Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Hydrodesulfurization Catalysts Markets in 2024

10.2 Asia Pacific Hydrodesulfurization Catalysts Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Hydrodesulfurization Catalysts Market size Outlook by Segments, 2021-2030

By Type

Load Type

Non-Load Type

By Application

Diesel

Naphtha

Others

11 South America Hydrodesulfurization Catalysts Market Analysis and Outlook To 2030

11.1 Introduction to South America Hydrodesulfurization Catalysts Markets in 2024

11.2 South America Hydrodesulfurization Catalysts Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Hydrodesulfurization Catalysts Market size Outlook by Segments, 2021-2030

By Type

Load Type

Non-Load Type

By Application

Diesel

Naphtha

Others

12 Middle East and Africa Hydrodesulfurization Catalysts Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Hydrodesulfurization Catalysts Markets in 2024

12.2 Middle East and Africa Hydrodesulfurization Catalysts Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Hydrodesulfurization Catalysts Market size Outlook by Segments, 2021-2030

By Type

Load Type

Non-Load Type

By Application

Diesel

Naphtha

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Advanced Refining Technologies

Albemarle Corp

Axens SA

Haldor Topsoe A/S

Honeywell International Inc

JGC C&C

Johnson Matthey Plc

Petrochina Company Ltd

Royal Dutch Shell PLC

Sinopec Corp

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Load Type

Non-Load Type

By Application

Diesel

Naphtha

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)