Imaging Chemicals Market to Reach $119.7 Billion by 2034 at 7% CAGR Driven by EUV Photoresists, Sustainable Inks, and Semiconductor AI Demand

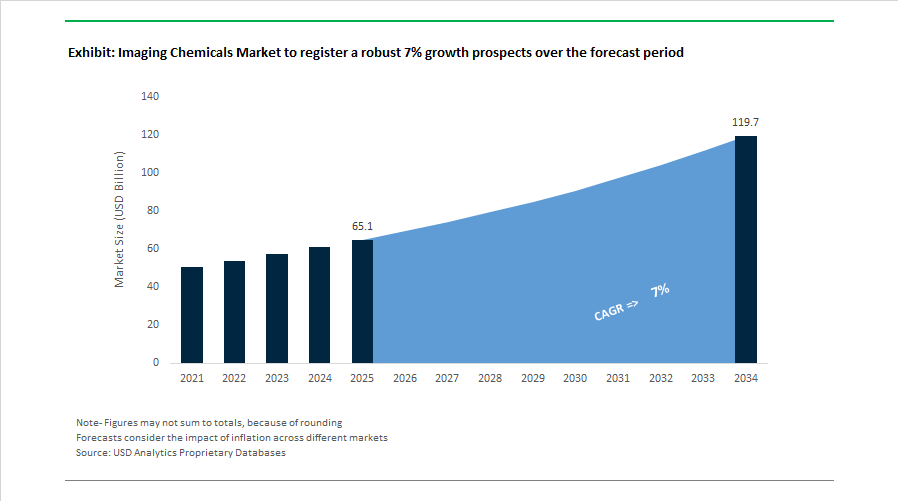

The Imaging Chemicals Market is projected to expand from $65.1 billion in 2025 to $119.7 billion by 2034, registering a CAGR of 7%. Growth is being fueled by escalating demand for advanced photoresists for EUV lithography, high-performance pigments for automotive and electronics coatings, sustainable imaging inks, and recycled-content specialty polymers. The convergence of semiconductor scaling, AI-enabled chip fabrication, digital archiving standards, and sustainability mandates is accelerating capital deployment across imaging resins, dispersants, colorants, and specialty coating chemistries.

In April 2024, Toyo Ink India, part of the Artience Group, announced a 3.5-fold capacity expansion for solvent-based adhesives and imaging-related coatings at its Gujarat facility, with completion targeted for April 2026. This investment positions India as a strategic export base for imaging chemicals serving the Middle East and Africa. In 2025, Kodak Alaris refreshed its scanner and imaging portfolio to meet FADGI standards, aligning imaging chemistry performance with stringent U.S. federal digital archiving guidelines. During July 2025, Sakata Inx released its Integrated Report 2025 outlining a strategic pivot toward water-based and UV-curable imaging inks, accelerating the phase-out of high-VOC formulations in textile and packaging segments. In October 2025, BASF Coatings unveiled its 2025–2026 Automotive Color Trends collection, utilizing advanced interference pigments and liquid metal-like finishes to enhance multidimensional imaging effects in automotive applications.

Semiconductor imaging chemicals witnessed intensified investment through late 2025. In November 2025, BASF commissioned a new CFRP-based high-performance dispersant line in Nanjing, enabling broader color gamut stability and improved dispersion control for advanced inks and imaging coatings used in electronics. In the same month, Sun Chemical, a DIC Group company, expanded perylene pigment capacity in Ludwigshafen to support high-transparency imaging applications in automotive coatings and digital printing. Fujifilm Electronic Materials completed a 13 billion yen development facility in Shizuoka in November 2025, deploying AI image recognition to enhance particle inspection accuracy for next-generation photoresists and image sensor color filters. Fujifilm further announced a capital commitment exceeding 100 billion yen between fiscal 2025 and 2026 to accelerate EUV photoresist and semiconductor imaging chemical development, reinforcing its position in AI-capable chip manufacturing. In 2025, Fujifilm also received Samsung Electronics’ "Most Valuable Partner Award" for delivering integrated imaging material solutions spanning advanced photoresists and color filter technologies.

Sustainability and structural realignment continued into 2026. In February 2026, Eastman Chemical reported that its Kingsport methanolysis facility increased output by 2.5 times year-on-year, supplying Renew-branded recycled polymers for high-performance imaging films. On January 5, 2026, DIC Corporation transitioned to a Global Operating Model to strengthen accountability across its color and imaging divisions, prioritizing high-growth digital imaging and advanced resin platforms. In January 2026, Toyo Printing Inks introduced BPA-free imaging coatings and enamels for metal packaging at the World Can Experience event, aligning with tightening global food-contact regulations. These developments highlight a market characterized by EUV lithography scaling, pigment innovation, advanced dispersant technologies, circular polymer integration, and regulatory-compliant imaging solutions across semiconductor, automotive, packaging, and digital archiving sectors.

Imaging Chemicals Market Trends and Opportunities

Strategic Consolidation in High-NA EUV Lithography Ancillary Chemicals

The global imaging chemicals market is undergoing a structural realignment driven by the semiconductor industry’s transition toward High Numerical Aperture Extreme Ultraviolet lithography at sub 2 nm technology nodes. At these dimensions, imaging performance is no longer defined by photoresists alone. Developers, edge bead removers, underlayers, and cleaning chemistries now directly influence yield, line edge roughness, and defectivity. Because EUV radiation is absorbed by almost all materials, even trace metallic contamination can cause catastrophic pattern collapse, pushing acceptable impurity thresholds into sub parts per billion territory.

This shift has accelerated consolidation among suppliers capable of meeting ultra purity specifications at scale. The joint High NA EUV Lithography Lab opened by ASML and imec in Veldhoven in mid 2024 has become a global validation hub where chemical suppliers qualify next generation imaging stacks under real process conditions. Participation in these ecosystems is increasingly limited to tier one formulators with deep capital reserves and advanced analytical capabilities.

Capital intensity in this segment continues to rise. FUJIFILM Corporation disclosed cumulative investments exceeding 100 billion yen between FY2021 and FY2024, with an additional 100 billion yen committed through FY2026 to expand semiconductor chemical evaluation capacity. AI enabled particle detection and inline defect analysis are now being deployed to control contamination risks at atomic scales. At the same time, exclusive R&D alliances are reshaping the value chain. JSR Corporation, in collaboration with IBM and Lam Research, is advancing dry resist platforms that significantly reduce the need for liquid developers. If commercialized at scale, these technologies could structurally reduce volumes in traditional wet imaging chemicals while increasing the strategic value of highly specialized ancillary formulations.

Structural Decline of Silver Halide Imaging in Medical Diagnostics

While advanced semiconductor applications are driving premium growth, legacy segments of the imaging chemicals market are experiencing irreversible contraction. The medical diagnostics sector has reached an inflection point as direct digital radiography becomes the default imaging modality across developed healthcare systems. This transition is being reinforced by sustainability mandates aimed at eliminating hazardous waste streams associated with silver halide films, developers, and fixers.

Industry assessments presented at global radiology forums in 2025 estimate that medical imaging contributes close to 1% of total healthcare related greenhouse gas emissions. Digital imaging systems integrated with cloud based picture archiving platforms are now viewed as essential tools for reducing chemical waste, water consumption, and energy intensity. Peer reviewed studies published during 2024 and 2025 demonstrate that digital X ray systems reduce patient throughput time by roughly 50% compared to analog workflows, improving asset utilization and clinical economics.

As a result, demand for traditional imaging chemicals is now largely confined to residual niches such as veterinary practices, remote clinics, and select emerging markets. In G7 economies, analog imaging volumes have fallen below 10% of total diagnostic imaging activity. For chemical suppliers, this has shifted strategy away from volume preservation toward margin optimization, inventory rationalization, and selective exit from non core silver halide product lines.

Conductive and Dielectric Inks for Flexible Hybrid Electronics

One of the most dynamic growth opportunities for imaging chemicals lies in functional inks used for flexible hybrid electronics. The convergence of smart packaging, automotive human machine interfaces, and wearable healthcare devices is driving demand for conductive and dielectric formulations that can be printed on flexible substrates with high precision and reliability. These applications require inks that combine electrical performance with controlled rheology, adhesion, and long term mechanical durability.

In August 2025, Electroninks entered a strategic partnership with Insulectro to scale metal organic decomposition inks for advanced packaging and automotive touch controls. These systems rely on imaging grade rheology modifiers to maintain print stability at high speeds, underscoring the convergence between traditional imaging chemistry expertise and electronics materials science. In parallel, healthcare focused collaborations involving Henkel, Covestro, and Quad Industries are accelerating the adoption of stretchable conductive inks for continuous health monitoring patches.

Although silver nanoparticle inks still account for roughly 80% of conductive ink usage due to superior conductivity, copper based alternatives are posting the fastest growth rates. Recent advances in anti oxidation coatings have improved shelf life and reliability, positioning copper inks as cost effective solutions for RFID tags and intelligent packaging where price sensitivity is high.

Sustainable Functional Inks for Industrial Digital Textile Printing

Another structurally attractive opportunity is emerging in digital textile printing as the global apparel industry pivots from mass production to on demand manufacturing. Digital pigment, reactive, and acid inks are replacing traditional screen printing chemistries due to their dramatic reductions in water and energy consumption. Systems commercialized by Kornit Digital and DuPont have demonstrated water savings of up to 95% compared with rotary screen printing, directly supporting compliance with circular economy and wastewater discharge regulations.

Water based pigment inks are gaining particular traction because they eliminate post printing washing and steaming steps while delivering wash fastness that meets or exceeds conventional standards. Environmental performance assessments indicate up to 40% improvement in lifecycle impact metrics, making these inks central to sustainability driven sourcing decisions by global apparel brands. In major textile manufacturing hubs across Vietnam and India, adoption of high speed digital print heads is enabling producers to cut operational costs by as much as 50% by removing screen preparation, chemical handling, and energy intensive curing stages. This structural shift is creating sustained demand for high stability, imaging grade ink dispersions optimized for continuous, on demand production models.

Imaging Chemicals Market Share and Segmentation Insights

Photoresist Chemistry Dominates Imaging Chemicals Demand in Advanced Semiconductor Photolithography

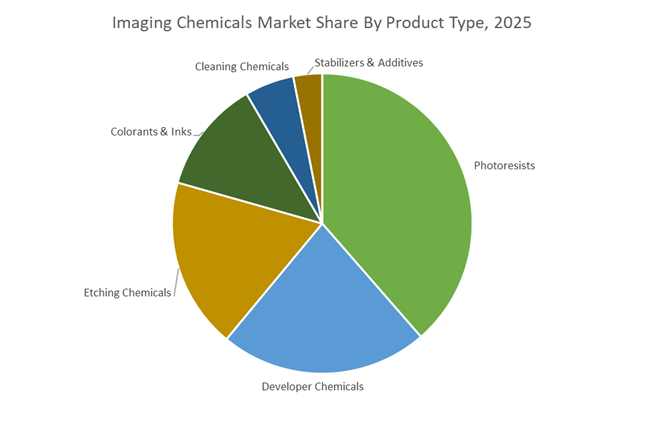

Photoresists accounted for 38.60% of the Imaging Chemicals Market share in 2025, making them the most critical product type in semiconductor manufacturing and microelectronics fabrication. Photoresists are specialized light-sensitive imaging chemicals used in photolithography processes to transfer circuit patterns onto silicon wafers, enabling the production of integrated circuits, memory chips, and advanced semiconductor devices. Their dominance is directly tied to the scaling of semiconductor technology, where each generation of smaller nodes increases the complexity and consumption of photolithography materials. As the semiconductor industry moves toward 3nm and emerging 2nm process nodes, manufacturers require more advanced photoresist formulations capable of delivering high-resolution pattern fidelity and defect control. In 2025, the most significant innovation trend is the evolution of extreme ultraviolet (EUV) photoresists, designed specifically for 13.5 nm wavelength lithography systems used in advanced chip manufacturing. These next-generation photoresists incorporate new polymer architectures, photoacid generators, and underlayer materials, enabling precise nanoscale patterning while commanding premium pricing in semiconductor process chemistry markets.

Semiconductor and Electronics Sector Drives Imaging Chemicals Consumption

Semiconductor and Electronics represented 58.60% of the Imaging Chemicals Market share in 2025, establishing it as the dominant end-use industry across the global imaging materials supply chain. Imaging chemicals such as photoresists, developer chemicals, etching solutions, and wafer cleaning agents are essential for the fabrication of integrated circuits, microprocessors, memory devices, flat panel displays, and LED components. Semiconductor manufacturing relies on multiple photolithography and chemical processing steps, with each wafer undergoing repeated cycles of coating, exposure, development, etching, and cleaning. This multi-stage fabrication process significantly increases the consumption of high-purity imaging chemicals. In 2025, global semiconductor supply chain restructuring is further strengthening demand. Governments and industry stakeholders are investing heavily in domestic semiconductor manufacturing through initiatives such as the U.S. CHIPS and Science Act, the European Chips Act, and continued capacity expansion across Asia-Pacific. These programs have triggered the construction of multiple new semiconductor fabrication plants worldwide, each requiring qualification of imaging chemical suppliers and consistent high-purity material supply as production ramps toward full-scale chip manufacturing.

Competitive Landscape in Imaging Chemicals Market

Fujifilm Expands Semiconductor Imaging Materials Leadership

Fujifilm Holdings has completed its transition into a diversified deep-technology leader, with imaging chemicals now central to semiconductor and healthcare growth. Between 2025 and 2026, the company committed over ¥100 billion to expand electronic materials, including an $86 million advanced photoresist facility in Shizuoka completed in November 2025. In February 2026, Fujifilm invested ¥5 billion in Rapidus, reinforcing its position as a strategic supplier of EUV-compatible photoresists and CMP slurries for advanced logic manufacturing. Its WAVE CONTROL MOSAIC line supports high-resolution image sensors used in smartphones and autonomous systems. The company targets ¥500 billion in semiconductor materials sales by 2030, emphasizing PFAS-free resists and AI-assisted quality control.

Kodak Repositions Imaging Chemistry Toward Advanced Materials

Eastman Kodak has shifted from consumer imaging to industrial materials and contract chemical manufacturing. Under its Material Science as a Service framework, Kodak leverages Rochester-based infrastructure to supply advanced materials for EV batteries and transparent conductive films. The KODAK PROSPER portfolio focuses on nanoparticulate inks for high-speed digital presses, replacing offset printing in packaging applications. In late 2025, Kodak expanded pharmaceutical partnerships to manufacture specialty chemicals for medical imaging contrast agents. Its Advanced Materials and Chemicals division now contributes a substantial portion of EBITDA, reducing dependence on legacy film operations and strengthening its role in specialty imaging chemistries.

Agfa-Gevaert Aligns Imaging Chemistry with Energy Transition

Agfa-Gevaert has streamlined operations to focus on digital print chemicals and green energy materials. Full integration of Inca Digital Printers enhanced its Digital Print and Chemicals division, targeting décor and packaging inkjet growth. The company markets ZIRFON separator membranes that employ specialized chemical coatings for green hydrogen production, signaling a pivot beyond conventional imaging science. Agfa is advancing UV-curable and water-based inks to reduce volatile organic compound emissions in industrial printing. It also retains leadership in Non-Destructive Testing chemicals and films for aerospace and oil and gas, where regulatory certification slows digital substitution.

DIC Accelerates Electronic Materials and Display Pigments

DIC Corporation is advancing its Vision 2030 strategy, designating semiconductors, batteries, and physical AI as primary growth pillars. In 2026, the company initiated Phase 2 of this plan and adopted a Global Operating Model to synchronize production across major regions. DIC is implementing internal carbon pricing to stimulate bio-derived resin and pigment innovation. It holds nearly 40% of the high-end global market for green and blue pigments used in LCD and OLED color filters, a critical segment within imaging chemicals for advanced displays. This shift positions DIC at the intersection of electronic materials and sustainable imaging technology.

Artience Expands Bio-Based and Food-Safe Imaging Solutions

Artience Group, formerly Toyo Ink, is strengthening its presence in packaging and sustainable imaging chemistry. In November 2025, it announced expansion of liquid ink production in Gujarat, India, with output projected to increase 1.5 times by 2028. In February 2026, the company launched German Printing Ink Ordinance compliant UV-curable inks in Europe, designed for ultra-low migration food packaging. Achieving INGEDE deinkability certification for mineral-oil-free inks enhances recyclability of paper-based packaging. The inauguration of a new research center in Bengaluru supports development of localized imaging chemicals and adhesive technologies for South Asian markets.

TDK Integrates Imaging Chemistry with Sensor and Data Infrastructure Growth

TDK Corporation applies advanced chemical coatings and magnetic materials to imaging and data storage technologies. In February 2026, the company revised its full-year projection upward to ¥2.47 trillion in net sales, supported by demand for high-performance sensors and imaging-related magnetic heads. TDK manufactures thermal transfer ribbons and chemical coatings for HDD suspension assemblies critical to high-density data center storage. Its Digital Transformation and Green Transformation initiatives include establishing a new regional headquarters in India in April 2026 to accelerate AI-integrated imaging sensor development. Recognition as a Sustainability Yearbook Member 2026 underscores progress toward renewable energy adoption in chemical-intensive manufacturing.

Japan Imaging Chemicals Market: Semiconductor-Grade Precision and Functional Materials Acceleration

Japan’s imaging chemicals industry is undergoing a structurally significant upgrade, anchored in semiconductor-grade precision, aerospace imaging reliability, and functional material innovation. In November 2025, Fujifilm Corporation completed a ¥13 billion advanced facility at its Shizuoka Factory under its Electronic Materials strategy. The site is dedicated to next-generation photoresists, EUV-compatible imaging chemicals, and PFAS-free formulations, directly aligned with sub-5nm semiconductor manufacturing and tightening global environmental compliance. This expansion is reinforced by Fujifilm’s planned investment exceeding ¥100 billion during FY2025–FY2026 into semiconductor and electronic imaging materials, largely driven by AI data center build-outs and advanced logic chip demand.

Beyond semiconductors, Japan is extending imaging chemistry into extreme-use environments. In March 2025, Mitsubishi Chemical Group achieved a space-grade validation milestone when proprietary high-rigidity materials and imaging coatings enabled successful lunar surface image capture by the private rover YAOKI. Parallelly, Artience Group under its Grow UP 2026 roadmap is shifting toward value transformation, prioritizing bio-based liquid inks, high-purity colorants, and imaging chemicals for flexible electronics and advanced packaging. At the manufacturing layer, Japanese producers are integrating AI-driven image recognition systems capable of detecting angstrom-scale particulates, supporting 99.999% purity thresholds required for advanced node fabrication and reinforcing Japan’s positioning in ultra-high-reliability imaging chemicals.

Germany Imaging Chemicals Market: Regulatory-Driven Purity and Sustainable Reformulation

Germany’s imaging chemicals landscape is being reshaped by electronic-grade capacity expansion and regulatory-led material reformulation. In October 2025, BASF announced the construction of a state-of-the-art Electronic Grade ammonium hydroxide facility at Ludwigshafen, designed to supply ultra-pure chemicals for wafer cleaning and etching in advanced node chip manufacturing. Scheduled to commence operations in 2027, the project directly supports European semiconductor supply chain resilience under the European Chips Act, strengthening localized access to critical imaging and processing chemistries.

Sustainability and compliance are equally central. German chemical clusters are piloting enzyme-integrated imaging stabilizers that lower the carbon footprint of photo-processing by approximately 15% compared with conventional solvent-based synthesis routes. Concurrently, in anticipation of REACH 2026 mandates, formulators are transitioning away from restricted fluorinated compounds toward siloxane-acrylic hybrid resins in industrial imaging applications. This dual emphasis on electronic-grade purity and regulatory-compliant reformulation positions Germany as a benchmark market for high-performance, environmentally aligned imaging chemicals across Europe.

China Imaging Chemicals Market: Policy-Led Localization and Digitalized Manufacturing

China’s imaging chemicals industry is advancing through coordinated industrial policy, localization targets, and mandatory digital transformation. Under the Ministry of Industry and Information Technology Petrochemical Work Plan for 2025–2026, electronic chemicals and high-end imaging polyolefins are prioritized as strategic materials, with the broader chemical sector targeted for sustained annual expansion above 5%. Central to this framework is the objective to raise domestic self-sufficiency in critical semiconductor imaging intermediates beyond 90% by 2026, supported by direct R&D subsidies and capacity incentives.

Operationally, China is enforcing “AI plus petrochemicals” mandates that require imaging chemical facilities to adopt blockchain-enabled traceability and automated hazard detection systems by late 2026, fundamentally changing compliance and quality assurance models. In early 2025, Sinopec operationalized a new ultra-pure chemical production line in Shanghai dedicated to photoresist monomers for 12-inch wafer manufacturing. These developments underscore China’s push toward vertically integrated, digitally monitored imaging chemical supply chains capable of serving domestic semiconductor fabrication at advanced process nodes.

India Imaging Chemicals Market: Capacity Expansion and Bio-Based Policy Alignment

India’s imaging chemicals market is transitioning from import reliance toward capacity creation and bio-based specialization. In November 2025, Toyo Ink India announced a 1.5x capacity expansion at its Gujarat facility, focusing on high-performance liquid packaging inks and digital imaging colorants tailored to rising domestic consumption and organized retail printing. This expansion aligns with India’s broader specialty chemicals manufacturing push.

Policy support is reinforcing this trajectory. The government’s BioE3 Policy introduced in 2025 formally recognizes bio-based chemicals as a priority vertical, offering production-linked incentives for enzymatic imaging stabilizers and sustainable formulation platforms. Complementing this, dedicated Petroleum, Chemical, and Petrochemical Investment Regions in Gujarat are being developed to attract global imaging chemical producers and integrate upstream feedstocks with downstream specialty outputs. At the domestic supplier level, Gujarat Alkalies and Chemicals Ltd. optimized high-purity lines in 2025 to enable localized synthesis of pharmaceutical-grade imaging agents and diagnostic dyes, strengthening India’s positioning in regulated imaging applications.

South Korea Imaging Chemicals Market: Sub-2nm Readiness and Cross-Sector Convergence

South Korea’s imaging chemicals sector is tightly coupled with its semiconductor leadership and emerging energy storage applications. In April 2025, BASF inaugurated a new Electronic Materials R&D Center in Ansan, dedicated to advanced cleaning and photo-imaging chemicals for AI processors and memory chips. This facility supports rapid material iteration cycles demanded by leading-edge fabs.

Simultaneously, domestic chemical players are diversifying imaging chemistry into adjacent high-value sectors. In late 2025, Lotte Fine Chemical reported a strategic pivot toward high-value HEMC and HPMC imaging binders for EV battery foils, leveraging film-forming properties to improve energy storage system stability. Industry collaboration with domestic foundries has further resulted in the deployment of extreme-purity metallization chemicals designed for sub-2nm process nodes by 2026, positioning South Korea at the forefront of angstrom-level imaging and deposition chemistry.

United States Imaging Chemicals Market: Capital Reallocation and Regulatory-Led Reformulation

The United States imaging chemicals market is being shaped by corporate balance sheet restructuring, AI-enabled imaging platforms, and tightening environmental regulation. In December 2025, Eastman Kodak completed a pension reversion that released over one billion dollars to its balance sheet, with a significant allocation directed toward its Advanced Materials and Chemicals division. These funds are being used to accelerate development of industrial imaging chemistries and diagnostic material specialties.

Product innovation remains closely linked to digital imaging ecosystems. In July 2025, Kodak Alaris launched the S5000 series production scanners alongside Capture Pro 7.0 software, integrating AI-powered document processing that relies on specialized thermal and chemical imaging substrates. On the regulatory front, stricter EPA VOC standards scheduled for 2026 are accelerating adoption of waterborne imaging stabilizers across the U.S. Midwest, materially reducing solvent emissions in printing and lithography while reshaping formulation strategies for compliant imaging chemicals.

Summary Table: Country-Level Strategic Positioning in the Imaging Chemicals Industry

Imaging Chemicals Market County Level Snapshot

|

Country

|

Strategic Focus Areas

|

Key Industrial Shifts

|

Policy and Compliance Drivers

|

|

Japan

|

EUV photoresists, aerospace imaging, functional inks

|

AI-driven purity control, bio-based colorants

|

Semiconductor self-reliance, PFAS-free mandates

|

|

Germany

|

Electronic-grade purity, sustainable stabilizers

|

Enzyme-based synthesis, hybrid resin adoption

|

European Chips Act, REACH 2026

|

|

China

|

Localization of imaging intermediates

|

Blockchain traceability, AI-enabled plants

|

MIIT petrochemical plan, self-sufficiency targets

|

|

India

|

Capacity expansion, bio-based imaging chemicals

|

PCPIR-led clustering, high-purity diagnostics

|

BioE3 policy, production-linked incentives

|

|

South Korea

|

Sub-2nm semiconductor chemicals, EV convergence

|

Advanced R&D centers, extreme-purity materials

|

Semiconductor competitiveness agenda

|

|

United States

|

Advanced materials reinvestment, low-VOC reformulation

|

AI-integrated imaging substrates

|

EPA VOC enforcement 2026

|

Imaging Chemicals Market Report Scope

Imaging Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$65.1 Billion

|

|

Market Size (2034)

|

$119.7 Billion

|

|

Market Growth Rate

|

7%

|

|

Segments

|

By Product Type (Photoresists, Developer Chemicals, Etching Chemicals, Cleaning Chemicals, Colorants & Inks, Stabilizers & Additives), By Technology (Semiconductor Photolithography, Digital Printing, Medical Imaging, Silver Halide Photography, Printed Electronics), By End-Use Industry (Semiconductor & Electronics, Packaging & Printing, Healthcare, Aerospace & Defense)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

FUJIFILM Corporation, BASF SE, Eastman Kodak Company, Mitsubishi Chemical Group, Artience Co., Ltd., Shin-Etsu Chemical Co., Ltd., Merck KGaA, Dow Inc., Lotte Fine Chemical Co., Ltd., Kodak Alaris, Sinopec, Tokyo Ohka Kogyo Co., Ltd., Sumitomo Chemical Co., Ltd., DuPont de Nemours, Inc., SCREEN Holdings Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Imaging Chemicals Market Segmentation

By Product Type

- Photoresists

- Positive

- Negative

- EUV

- ArF

- KrF

- Developer Chemicals

- Etching Chemicals

- Wet Etchants

- Dry Etching Chemicals

- Cleaning Chemicals

- Colorants & Inks

- Stabilizers & Additives

By Technology

- Semiconductor Photolithography

- Digital Printing

- Medical Imaging

- Silver Halide Photography

- Printed Electronics

By End-Use Industry

- Semiconductor & Electronics

- Packaging & Printing

- Healthcare

- Aerospace & Defense

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Imaging Chemicals Industry

- FUJIFILM Corporation

- BASF SE

- Eastman Kodak Company

- Mitsubishi Chemical Group

- Artience Co., Ltd.

- Shin-Etsu Chemical Co., Ltd.

- Merck KGaA

- Dow Inc.

- Lotte Fine Chemical Co., Ltd.

- Kodak Alaris

- Sinopec

- Tokyo Ohka Kogyo Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- DuPont de Nemours, Inc.

- SCREEN Holdings Co., Ltd.

*- List not Exhaustive