Industrial Anti-Scaling Chemicals Market to Reach $7.7 Billion by 2034 at 5.2% CAGR Driven by Integrated Cooling, Digital Water Optimization, and Bio-Based Antiscalants

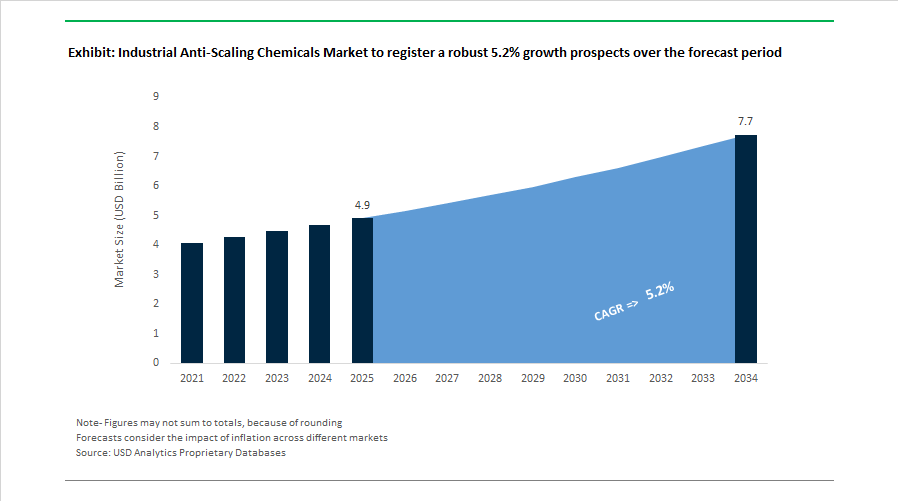

The Industrial Anti-Scaling Chemicals Market is projected to expand from $4.9 billion in 2025 to $7.7 billion by 2034, registering a CAGR of 5.2%. Growth is being propelled by rising water stress, stricter discharge regulations, expansion of high-tech manufacturing, and the increasing complexity of industrial cooling and boiler systems. Anti-scaling chemicals, including phosphonates, polymer-based dispersants, organophosphates, and biodegradable antiscalants, are now central to industrial water treatment programs in power generation, data centers, steel production, pulp and paper, desalination, and semiconductor fabrication. Market participants are transitioning from commodity threshold inhibitors toward integrated chemical-digital platforms that combine scale control, corrosion inhibition, and real-time monitoring to maximize heat-transfer efficiency and minimize downtime.

Strategic portfolio realignment began in February 2024 when Kemira completed the divestment of its Oil & Gas portfolio, sharpening its focus on core Water Solutions and specialty scale inhibitors for municipal and industrial applications. In August 2024, Nalco Water, an Ecolab company, signed a strategic cooperation agreement with Danieli to optimize water treatment in the metals industry, combining metallurgical process technology with advanced anti-scaling chemistries to reduce fouling, maintenance frequency, and carbon intensity in steel mills. During late 2023 and early 2024, BASF introduced a new generation of biodegradable antiscalants formulated with advanced biopolymers designed to meet ready biodegradability standards, addressing tightening environmental compliance requirements for discharge into sensitive aquatic systems.

Industry consolidation and digital integration accelerated in 2025. In April 2025, Kurita America appointed Todd Emslander as CEO, reinforcing its “Master Every Drop” initiative that integrates smart dosing systems with predictive chemical control for real-time scale prevention. In June 2025, Solenis announced its merger with NCH Corporation, expanding its reach into middle-market industrial customers and strengthening localized anti-scaling service capabilities worldwide. In November 2025, Ecolab expanded its Integrated Cooling Program for data centers, leveraging digital monitoring and advanced scale inhibitors to maintain optimal cooling tower performance amid AI-driven thermal loads. In December 2025, Ecolab finalized the acquisition of Ovivo’s Electronics Ultrapure Water business, enhancing its ability to deliver specialized anti-scaling chemistries for semiconductor fabrication environments where ultra-low mineral contamination is critical.

Strategic positioning intensified entering 2026. In January 2026, Kemira unveiled its Sustainability-driven Growth Strategy, targeting a doubling of water treatment revenue and €500 million in bio-based product sales by 2030, including renewable scale-control agents. During the same month, Ecolab partnered with CDP to create a water performance benchmarking framework that enables industrial operators to quantify the effectiveness of anti-scaling programs within broader ESG reporting structures. In December 2025, Kurita and ispace initiated collaboration on lunar water resource development, advancing research into extreme-condition scale control technologies with potential terrestrial applications. In February 2026, Ecolab reported record fourth-quarter 2025 results and projected 12% to 15% Adjusted Diluted EPS growth for 2026, attributing performance to high-margin integrated cooling and scale inhibition solutions across industrial and high-tech sectors.

Industrial Anti-Scaling Chemicals Market Trends and Opportunities

Mandatory Transition Toward Phosphonate-Free and Biodegradable Anti-Scaling Chemistries

The industrial anti-scaling chemicals market is undergoing a decisive regulatory-driven transformation as phosphorus discharge limits tighten across major industrial economies. By late 2025, amendments to EU REACH Annex XVII and region-specific nutrient loading controls in the United States have accelerated the decline of conventional phosphonates such as ATMP and HEDP, particularly in open-loop cooling and non-contained water systems. These measures are designed to curb eutrophication risks in sensitive water bodies, forcing industrial operators to reassess long-established scale control programs.

In response, biodegradable polymeric anti-scalants are gaining rapid commercial traction. Phosphorus-free alternatives such as polyaspartic acid and carboxymethyl inulin are now demonstrating calcium carbonate inhibition efficiencies exceeding 95% in industrial cooling and membrane applications, while offering substantially improved aquatic toxicity profiles. Regulatory data from U.S. Midwest municipal authorities show that industrial phosphorus loading declined by approximately 20 to 25% between 2023 and 2025 following mandates that required phosphonate-free water treatment packages for high-discharge facilities.

At the supplier level, ESG integration is no longer optional. Tier-1 providers such as Ecolab and Dow have redirected R&D pipelines toward sustainable anti-scalants engineered for high-recovery reverse osmosis systems. These next-generation products not only prevent scale deposition but also enable higher cycles of concentration, reducing blowdown volumes and overall wastewater discharge. This dual benefit is positioning green anti-scalants as both a compliance solution and a cost optimization lever for industrial water users.

Digitalization of Anti-Scaling Programs Through Smart Dosing and AI Analytics

Digital transformation is rapidly redefining how anti-scaling chemicals are applied and managed. The market is moving away from static, manual dosing regimes toward connected, sensor-driven systems that dynamically adjust inhibitor feed rates based on real-time water chemistry parameters such as Langelier and Ryznar indices. This shift is being driven by rising water costs, stricter discharge permits, and the growing adoption of Industry 4.0 standards across manufacturing and infrastructure assets.

In 2025, the commercial rollout of smart dosing platforms significantly accelerated. Grundfos introduced digitally integrated dosing pumps capable of autonomous adjustment using live sensor inputs, enabling facilities to cut anti-scalant consumption by an estimated 15 to 20% without compromising scale control. Beyond hardware, AI-powered predictive models are increasingly used by hyperscale data centers and industrial campuses to anticipate scaling events before they occur. These systems analyze historical trends, feedwater variability, and operational load to trigger preemptive dosing corrections, extending membrane life by up to 30% and reducing unplanned downtime.

Chemical suppliers are monetizing this shift through service-based models. Companies such as Solenis and Italmatch Chemicals are expanding “Water-as-a-Service” contracts that bundle chemicals, sensors, analytics, and compliance reporting into a single performance-guaranteed offering. This evolution is raising switching costs for end users and reshaping competition around digital capability rather than product price alone.

High-Temperature, High-Pressure Anti-Scalants for Advanced Geothermal Energy

The expansion of enhanced geothermal systems is creating a specialized, high-margin opportunity for thermally robust anti-scalants. Unlike conventional geothermal wells, next-generation systems operate at temperatures above 150°C and under extreme pressures, conditions that rapidly degrade standard scale inhibitors and lead to silica and calcite deposition in wellbores and surface equipment.

Strategic collaborations are accelerating commercialization. In October 2025, SLB partnered with Ormat Technologies to address scale-related productivity losses in deep geothermal reservoirs. According to U.S. Department of Energy projections, advanced geothermal could contribute up to 90 gigawatts of baseload power by 2050, provided chemical challenges such as high-enthalpy scaling are effectively managed. Silica inhibitors now account for nearly 40% of geothermal anti-scalant demand, with new sulfonated polymer chemistries demonstrating improved thermal stability and the ability to prevent efficiency losses of up to 15% in the first year of operation. Government policy support, including India’s National Policy on Geothermal Energy 2025, is expected to further stimulate demand for these high-performance formulations.

Anti-Scaling Solutions for High-Salinity Produced Water Reuse in Shale Operations

Produced water recycling has emerged as a critical ESG priority in shale oil and gas operations, driving strong demand for anti-scalants that function reliably in ultra-high salinity environments. Recycled produced water often contains extreme total dissolved solids and elevated sulfate levels, creating severe scaling risks when reused in hydraulic fracturing without advanced chemical control.

Operational milestones underscore the scale of this opportunity. In 2025, Select Water Solutions reported supplying more than 500,000 barrels of recycled produced water per day in the Permian Basin, a volume made feasible only through advanced, compatibility-tested anti-scalant packages. Industry data indicate that water reuse rates in the Permian now exceed 50%, creating sustained, high-volume demand for inhibitors that remain stable alongside friction reducers and biocides. New research published in late 2025 demonstrates that coupling specialized anti-scalants with membrane-based treatment can improve water recovery by approximately 12% while meeting tightening discharge standards. As shale operators continue to prioritize freshwater avoidance, anti-scalants engineered for high-TDS, chemically complex systems are becoming mission-critical inputs rather than discretionary additives.

Industrial Anti-Scaling Chemicals Market Share and Segmentation Insights

Phosphonate-Based Scale Inhibitors Dominate Industrial Water Treatment in High-Temperature Process Systems

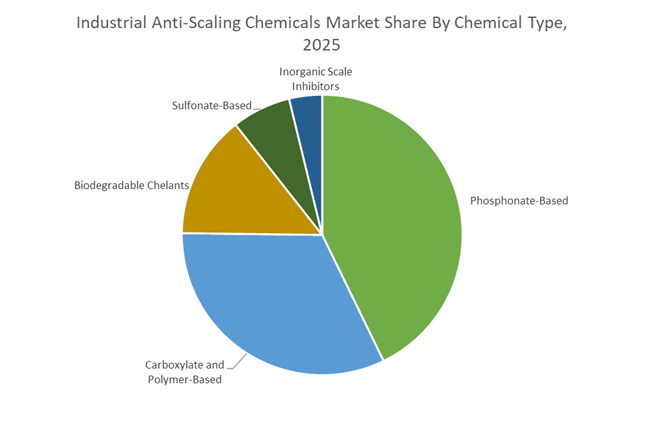

Phosphonate-based chemicals accounted for 42.80% of the Industrial Anti-Scaling Chemicals Market share in 2025, making them the leading chemical type in industrial scale inhibition technologies. Phosphonate scale inhibitors are widely used because they provide high-performance control of mineral scaling such as calcium carbonate, calcium sulfate, and barium sulfate, which commonly accumulate in industrial water systems and process equipment. Their chemical stability across wide pH ranges, elevated temperatures, and high salinity environments makes them highly effective in complex industrial operations including cooling towers, industrial boilers, desalination plants, and oilfield water treatment systems. In 2025, technological advancements have focused on improving thermal stability and calcium tolerance of phosphonate chemistries, enabling reliable performance in high-stress environments such as deep-well injection systems, geothermal operations, and high-pressure steam generation facilities. These improved formulations maintain scale inhibition efficiency even under extreme process conditions where conventional scale inhibitors may degrade, reinforcing phosphonates as a preferred chemistry for industrial water treatment programs.

Power Generation Sector Drives the Largest Demand for Industrial Anti-Scaling Chemicals

Power Generation represented 32.80% of the Industrial Anti-Scaling Chemicals Market share in 2025, establishing it as the largest end-use industry for scale inhibitor technologies. Thermal power plants including coal-fired, natural gas combined-cycle, nuclear, and concentrated solar power facilities operate extensive water circulation systems that require strict scale control to maintain operational efficiency and equipment longevity. Scaling in boilers, heat exchangers, cooling towers, and condensers can significantly reduce heat transfer efficiency, increase energy consumption, and accelerate equipment wear. As a result, scale inhibitors play a critical role in maintaining boiler reliability, turbine efficiency, and long-term plant performance. In 2025, the integration of renewable energy into national power grids is creating new operational challenges for conventional power plants. Facilities that previously operated under stable baseload conditions are increasingly required to cycle frequently between startup, shutdown, and partial load operation, causing fluctuations in water temperature, pressure, and flow conditions. These variable operating conditions increase the risk of mineral precipitation, driving demand for next-generation anti-scaling chemicals specifically formulated for flexible power plant operation.

Competitive Landscape in Industrial Anti-Scaling Chemicals Market

Ecolab (Nalco Water) Advances Predictive Antiscalant Control

Ecolab Inc., through Nalco Water, remains the dominant global force in industrial scale control. In 2026, its strategy centers on AI integration within the 3D TRASAR™ digital platform, enabling predictive identification of scaling events before deposition occurs. The “One Ecolab” initiative continues to streamline operations while embedding machine-learning algorithms into dosing systems. In December 2025, the acquisition of Ovivo’s Electronics Ultrapure Water business significantly expanded Ecolab’s presence in semiconductor-grade water treatment, a segment requiring ultra-low silica and calcium scaling thresholds. The company projects adjusted diluted EPS of $8.43–$8.63 in 2026, reflecting 12%–15% growth. Hosting the 2026 Nalco Water Steel Conference further reinforced its positioning in high-load industrial RO and metallurgical process environments where membrane scaling and iron fouling remain operational bottlenecks.

Solenis Expands Ultrasonic Monitoring and Sustainability Transparency

Solenis strengthened its global industrial footprint following the merger with Diversey and the November 2025 integration of NCH Corporation. Its OnGuard™ scale analyzer platform uses patented ultrasonic detection capable of identifying scale deposition at approximately 1 micron, enabling precise inhibitor dosing and reduced chemical overfeed. In February 2026, Solenis was recognized in the S&P Global Sustainability Yearbook, underscoring its governance and environmental metrics. The company has committed to reporting revenue exposure to Substances of Very High Concern (SVHC) beginning FY2026, with a 2030 phase-out objective. This compliance-driven transparency is increasingly relevant as phosphonate-based inhibitors face regulatory scrutiny in Europe.

Veolia Integrates Antiscaling with Long-Term Water Concessions

Veolia continues expanding its integrated water-treatment model under the “GreenUp” framework. In February 2026, the company secured two 15-year contracts in Mumbai totaling 2.91 billion liters per day in treatment capacity. These large-scale plants require advanced antiscalant management for high-recovery RO systems and brine concentration units. Veolia also operates India’s first carbon capture plant for Tata Steel, reflecting its combined decarbonization and water stewardship positioning. Its roadmap for 2026 emphasizes governance improvements and environmental compliance as water costs rise globally. Scale control in high-TDS municipal and industrial wastewater reuse projects represents a primary growth driver.

Kemira Concentrates on Water-Only Portfolio Strategy

Kemira Oyj has completed its divestment of Oil & Gas operations and is now fully focused on water treatment and renewable solutions. The company aims to double water-related revenues long term, supported by a strong 2025 balance sheet (Net debt/Operative EBITDA of 1.0). In early 2026, Kemira introduced enhanced DNA Tools capable of identifying microbiologically induced scaling risks in cooling towers and pulp-processing circuits. Bio-based antiscalant pilots are expanding as part of its €500 million renewable-solution revenue target by 2030. Kemira remains dominant in pulp & paper water systems, where calcium carbonate and barium sulfate scaling significantly impact evaporator efficiency.

BASF Leverages Verbund Integration for Cost and Feedstock Advantage

BASF SE is executing its “Winning Ways” strategy to enhance competitiveness in performance chemicals, including antiscalants. The Zhanjiang Verbund site in China, operational since late 2025, serves as a central growth platform for Asian water treatment additives. BASF forecasts 2026 EBITDA before special items between €6.2 billion and €7.0 billion, supported by improved earnings in Chemicals and Nutrition & Care. Achieving a €1.7 billion cost-reduction run rate by end-2025, with a €2.3 billion target by end-2026, enhances margin resilience amid volatile raw material costs. The Verbund model provides backward integration into phosphonates and dispersants, strengthening supply security in high-growth desalination and industrial reuse markets.

SUEZ Expands PFAS and Phosphonate Reduction Technologies

SUEZ continues aggressive expansion in emerging water markets. In February 2026, it secured a 25-year concession in Salem, India, serving over one million residents—its largest contract in the country. The company is focusing on PFAS treatment, soil remediation, and integrated pyrocarbonization solutions for sludge management. In 2026, SUEZ introduced digital dosing systems capable of reducing phosphonate consumption in antiscalant formulations by up to 15%, directly addressing regulatory pressure on phosphorus discharge. Ongoing expansion in Jiangsu and Shandong provinces reinforces its role in industrial wastewater and utility-scale scaling mitigation across China.

India: Import Liberalization, Desalination Demand, and Green Chemistry Substitution

India’s industrial anti-scaling chemicals market is being reshaped by policy-driven cost realignment, infrastructure-led demand, and a decisive transition toward biodegradable formulations. In December 2025, the Government of India withdrew Quality Control Orders on several petrochemical intermediates, lowering raw material costs for domestic formulators and improving input flexibility for downstream water treatment additives. This regulatory reset is particularly relevant for anti-scaling formulations used in power generation, textiles, and process industries where cost sensitivity remains high.

Capacity formation is accelerating in parallel. Large-scale investments nearing completion across Petroleum, Chemical, and Petrochemical Investment Regions are anchoring integrated anti-scaling production lines within multi-product specialty chemical clusters. These hubs are designed to support consistent supply of phosphonate alternatives, polymeric antiscalants, and chelant-based inhibitors for industrial water systems. Demand momentum strengthened further in 2025 with the launch of the National Desalination Mission, which materially increased requirements for reverse osmosis antiscalants along the Gujarat and Tamil Nadu coastlines, where seawater desalination plants operate under high scaling indices.

Domestic substitution is also advancing in agrochemicals. Clean Science and Technology Limited expanded catalytic capacity in late 2025, enabling local availability of scale inhibitors used in pesticide formulation and reducing reliance on imports. Looking ahead, industrial output recovery expected in 2026 under the Production-Linked Incentive scheme is set to lift consumption of high-performance water treatment chemicals. Concurrently, firms such as Aquapharm are scaling biodegradable GLDA and MGDA production, positioning green chelants as replacements for traditional phosphonates in textile and paper processing by 2026.

Germany: Compliance Cost Pressure and Energy-Efficient Chemistry Innovation

Germany’s industrial anti-scaling chemicals market is increasingly defined by regulatory intensity, portfolio rationalization, and innovation focused on energy efficiency. In September 2025, Solvay announced a €25 million restructuring to reposition its Bad Wimpfen facility as a global specialty chemicals hub, while phasing out selected toxic organofluorine compounds by early 2026. This move reflects a broader industry pivot away from substances facing heightened scrutiny under EU chemical policy.

Decarbonization strategy is also influencing asset decisions. BASF conducted a strategic review of its Ludwigshafen operations in late 2025, resulting in the closure of legacy hydrosulfite units and a sharper focus on sustainable water treatment chemistry and green hydrogen precursors. Industry surveys from the same period indicate that a majority of German producers are experiencing rising compliance costs linked to new ECHA mandates targeting PFAS and other persistent chemicals commonly used in conventional anti-scaling coatings.

Against this backdrop, formulation innovation is emerging as a competitive lever. German research laboratories successfully commercialized low-temperature antiscalants in 2025, allowing cooling towers to operate at higher cycles of concentration without mineral precipitation. These products support reduced water consumption and energy use, aligning anti-scaling performance with national efficiency and emissions objectives.

United States: Digital Water Management, PFAS Exit, and Infrastructure-Led Uptake

The United States industrial anti-scaling chemicals market is being shaped by digital water management, regulatory-driven formulation changes, and renewed infrastructure investment. In 2025, a landmark study by Ecolab through its Nalco Water division highlighted the growing water footprint of artificial intelligence infrastructure. The findings underscored the reliance of data center cooling systems on advanced anti-scaling chemistry, elevating the strategic importance of high-efficiency inhibitors in mitigating water stress.

Technology integration is accelerating adoption. At its October 2025 Naperville Technology Conference, Ecolab demonstrated AI-driven process optimization platforms capable of predictive scale modeling, reducing industrial water system downtime by up to 50%. Regulatory pressure is also reshaping portfolios. U.S. manufacturers such as Dow and Solenis accelerated the phase-out of PFOA-related stabilizers in late 2025, launching Green Seal-certified anti-scaling agents for boilers and municipal systems.

Public spending is reinforcing demand. Funds allocated under the Bipartisan Infrastructure Law in 2025 were increasingly directed toward industrial wastewater reuse upgrades, supporting adoption of high-performance flocculant and antiscalant hybrid chemistries designed for closed-loop and high-recovery operations.

Sweden: Filtration Protection and PFAS-Oriented Water Treatment

Sweden’s industrial anti-scaling chemicals market is developing around advanced water purification infrastructure and leadership in PFAS mitigation. In September 2025, Kemira received final investment approval for an activated carbon reactivation facility in Helsingborg. The plant is engineered to remove micropollutants while preventing scaling in Nordic water treatment circuits that operate under cold-climate conditions.

The Helsingborg facility, scheduled for operation by 2027, integrates antiscalants specifically formulated to protect high-performance filtration membranes from fouling caused by persistent organic pollutants. This approach positions anti-scaling chemicals as enablers of advanced PFAS removal technologies rather than standalone treatment additives, reinforcing Sweden’s role as a testbed for next-generation water treatment solutions.

Comparative Snapshot: Industrial Anti-Scaling Chemicals Market by Country

Industrial Anti-Scaling Chemicals Market County Level Snapshot

|

Country

|

Primary Driver

|

Core Application Focus

|

Structural Direction

|

|

India

|

Import liberalization and desalination rollout

|

RO systems, textiles, agrochemicals

|

Cost reduction and green chelant substitution

|

|

Germany

|

PFAS regulation and decarbonization

|

Cooling towers, industrial water loops

|

Energy-efficient, low-temperature formulations

|

|

United States

|

Digital water management and infrastructure spend

|

Data centers, boilers, reuse systems

|

AI-enabled optimization and PFAS-free chemistry

|

|

Sweden

|

PFAS removal and advanced filtration

|

Municipal and industrial water treatment

|

Membrane protection and integrated purification

|

Industrial Anti-Scaling Chemicals Market Report Scope

Industrial Anti-Scaling Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.9 Billion

|

|

Market Size (2034)

|

$7.7 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Chemical Type (Phosphonate-Based, Carboxylate and Polymer-Based, Sulfonate-Based, Biodegradable Chelants, Inorganic Scale Inhibitors), By Application (Cooling Towers, Boilers, Desalination Systems, Oil and Gas Operations, Membrane Systems), By End-Use Industry (Power Generation, Oil and Gas and Mining, Wastewater Treatment, Food and Beverage, Pulp and Paper, Chemical Manufacturing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc., Solenis, Kemira Oyj, BASF SE, Veolia Water Technologies, Kurita Water Industries Ltd., Suez S.A., Dow Inc., Clariant AG, Italmatch Chemicals S.p.A., Thermax Limited, Baker Hughes Inc., BWA Water Additives, Avista Technologies, Inc., Aquapharm Chemical Pvt. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Industrial Anti-Scaling Chemicals Market Segmentation

By Chemical Type

- Phosphonate-Based

- Carboxylate and Polymer-Based

- Sulfonate-Based

- Biodegradable Chelants

- Inorganic Scale Inhibitors

By Application

- Cooling Towers

- Boilers

- Desalination Systems

- Oil and Gas Operations

- Membrane Systems

By End-Use Industry

- Power Generation

- Oil and Gas and Mining

- Wastewater Treatment

- Food and Beverage

- Pulp and Paper

- Chemical Manufacturing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Industrial Anti-Scaling Chemicals Market

- Ecolab Inc.

- Solenis

- Kemira Oyj

- BASF SE

- Veolia Water Technologies

- Kurita Water Industries Ltd.

- Suez S.A.

- Dow Inc.

- Clariant AG

- Italmatch Chemicals S.p.A.

- Thermax Limited

- Baker Hughes Inc.

- BWA Water Additives

- Avista Technologies, Inc.

- Aquapharm Chemical Pvt. Ltd.

*- List not Exhaustive