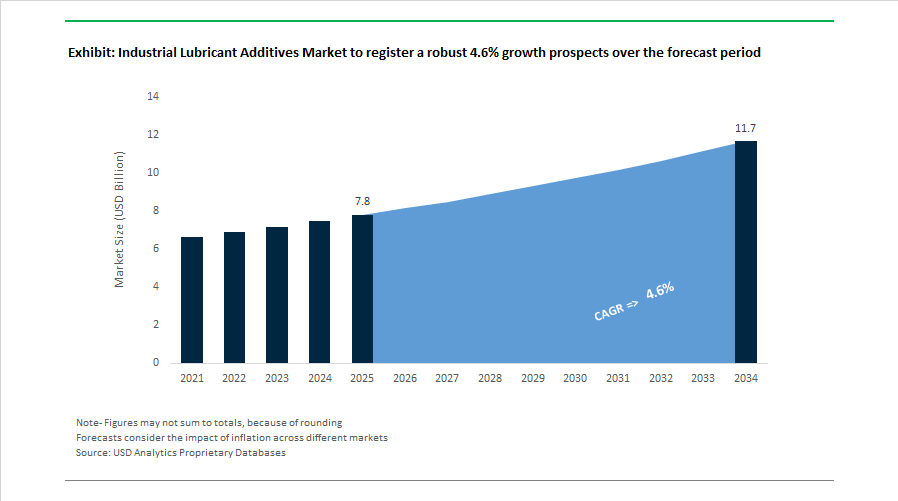

Industrial Lubricant Additives Market to Reach $11.7 Billion by 2034 at 4.6% CAGR Fueled by Hydrogen Engines, Low-SAPS Formulations, and Sustainable EP Additives

The Industrial Lubricant Additives Market is projected to expand from $7.8 billion in 2025 to $11.7 billion by 2034, registering a CAGR of 4.6%. Growth is being driven by the evolution of high-efficiency engines, electrified drivetrains, hydrogen internal combustion engines, and increasingly stringent emissions and durability standards. Industrial lubricant additives including aminic antioxidants, extreme-pressure (EP) agents, dispersants, viscosity modifiers, corrosion inhibitors, and anti-wear chemistries are central to extending equipment life, improving fuel economy, and supporting higher operating temperatures in heavy-duty machinery, power generation, and manufacturing systems. As regulatory frameworks tighten globally, additive producers are accelerating innovation in low-SAPS, renewable-content, and ultra-low viscosity formulations tailored for next-generation industrial mobility and energy systems.

Capacity expansion and specification upgrades defined the 2024 to 2025 period. In May 2024, Lubrizol launched Lubrizol® CV9660, a low-SAPS heavy-duty lubricant solution engineered to meet modern aftertreatment system requirements while covering multiple viscosity grades. In July 2024, Lubrizol introduced PV1710 to enable lubricant marketers to transition to the ILSAC GF-7 specification effective March 31, 2025, ensuring compliance with stricter fuel economy and engine durability benchmarks. Meanwhile, Chevron Oronite made a final investment decision in May 2024 to expand its Ningbo, China facility, with construction beginning in July 2024 and commercial production targeted for late 2026, reinforcing supply reliability in the Asia-Pacific industrial market.

Innovation accelerated significantly in 2025. In February 2025, Univar Solutions acquired Brad-Chem Holdings, strengthening its distribution capabilities for specialty lubricant additives including tackifiers and corrosion inhibitors. In March 2025, BASF announced an expansion of aminic antioxidant production at its Puebla, Mexico site, with completion scheduled for 2026 to meet rising demand for extended drain interval lubricants. In August 2025, Afton Chemical introduced the HiTEC® 65522 series, the first additive chemistry approved for the revised TOP TIER+™ standard, addressing injector deposit control and stochastic pre-ignition challenges in downsized engines. In September 2025, Afton Chemical launched HiTEC® 12582, the world’s first additive specifically engineered for hydrogen internal combustion engines, optimized for water management and corrosion resistance unique to hydrogen combustion environments. During the same month, BASF announced Keropur® AP 225-20, certified under the new U.S. TOP TIER+™ standard and scheduled for commercial availability in the first half of 2026.

Sustainability and strategic partnerships intensified entering 2026. In October 2025, LANXESS launched an ISCC PLUS-certified sustainable version of Additin® RC 2515, containing over 80% renewable raw materials and delivering a 34% lower carbon footprint for industrial gear oils and metalworking fluids. Between November 2025 and January 2026, Infineum globally rolled out P6188 technology approved against Volkswagen’s latest SAE 0W-20 standards, supporting ultra-low viscosity lubricants with enhanced wear protection. In 2025, Infineum signed a strategic partnership with Rianlon Corporation to strengthen additive supply chains across Asia. In early 2026, Lubrizol unveiled its refreshed brand identity, “Formulating Tomorrow,” emphasizing system-level solutions for electrified drivetrains and sustainable mobility. These developments highlight a structural shift toward high-performance, low-carbon industrial lubricant additives designed to support hydrogen fuel systems, advanced combustion engines, and long-life industrial equipment.

Industrial Lubricant Additives Market Trends and Opportunities

Specialized Additive Packages for Offshore Wind and Tidal Reliability

The rapid scale-up of offshore wind capacity is fundamentally reshaping demand patterns in the industrial lubricant additives market. Next-generation offshore turbines exceeding 15 MW are being designed for extended service intervals of up to six years, placing unprecedented mechanical and chemical stress on gearbox and bearing systems. This shift is driving demand for advanced extreme pressure agents, ashless antioxidants, and anti-wear chemistries that can operate reliably under high torque, fluctuating loads, and constant exposure to salt-laden air.

A notable inflection point emerged in May 2024, when Oak Ridge National Laboratory, supported by the U.S. Department of Energy, demonstrated short-chain ammonium phosphate ionic liquid additives that delivered 50% lower friction and a tenfold reduction in wear relative to conventional gear oils. These results are commercially significant because they align performance gains with zero aquatic toxicity requirements, a non-negotiable criterion for offshore deployment. In parallel, additive suppliers such as Afton Chemical have expanded production of WEC-mitigating formulations as gearbox failures linked to white etching cracks remain one of the highest-cost failure modes in offshore assets. As tidal and wave energy projects move from pilot to early commercial scale in 2025, additive design is further evolving toward molecular structures that retain film strength under seawater contamination while meeting marine ecotoxicity thresholds.

Reformulation for Low-GWP Refrigerant and HFO Compatibility

Regulatory mandates targeting refrigerant emissions are triggering a second major reformulation cycle across industrial lubricant additives. The prohibition of new HVAC systems using R-410A under the U.S. Environmental Protection Agency 2025 ruleset has accelerated the adoption of hydrofluoroolefin refrigerants and natural alternatives such as CO₂. These systems impose far stricter chemical compatibility requirements on lubricant additives, particularly with respect to hydrolytic stability and acid control.

In response, additive developers are prioritizing ashless dispersants and high-performance antioxidants that can withstand prolonged exposure to reactive refrigerant chemistries. Market introductions in early 2025, including hydraulic and compressor packages with turbine oil stability test durations exceeding 5,000 hours, underscore the shift toward lifetime-fill and ultra-extended drain strategies. From a business perspective, this trend is closely tied to Scope 3 waste reduction goals. Industrial operators are increasingly quantifying lubricant-related waste streams, and oils that last twice as long can reduce hazardous waste volumes by more than 40% over a system’s operating life, reinforcing demand for premium additive technologies.

Electro-Compatible Additives for Electrified Industrial Machinery

The electrification of heavy industrial equipment is creating a structurally new opportunity for lubricant additive suppliers. Electrified mining trucks, automated forklifts, and airport ground support vehicles introduce stray electrical currents that can cause electrocorrosion, bearing fluting, and premature lubricant breakdown. Conventional sulfur-based extreme pressure additives are poorly suited to these environments due to their copper aggressiveness and unstable dielectric behavior.

By late 2025, research published in the journal Lubricants highlighted nitrogen-modified polymethacrylate architectures as a critical enabler for new energy vehicle transmission fluids. These formulations balance oxidation resistance with the thermal profiles of high-speed electric motors while maintaining controlled dielectric constants. For additive suppliers, this represents a high-margin niche where electro-compatibility, copper passivation, and wear protection must be engineered as an integrated system. As electrification expands beyond automotive into core industrial fleets, demand for purpose-built “E-fluid” additive packages is expected to scale rapidly.

High-Water-Based Fluids for Sustainable Metal Forming

Sustainability and fire safety pressures in steel and aluminum rolling are opening a second major growth avenue through high-water-based fluids containing more than 80% water. These fluids drastically reduce VOC emissions and fire risk but require sophisticated additive packages to replicate the lubricity, corrosion protection, and microbial control of mineral oil systems.

Regulatory momentum is reinforcing this transition. In April 2025, the Federation of Indian Chambers of Commerce and Industry outlined an Extended Producer Responsibility roadmap mandating progressive increases in used-oil recycling, reaching 50% by FY2031. High-water-based fluids align naturally with these objectives because they are easier to treat, recycle, and dispose of than neat oils. The commercial opportunity lies in multifunctional aqueous additive systems that deliver lubricity, tramp oil rejection, and bioresistance without relying on formaldehyde-releasing biocides. Government-backed investments in high-purity industrial chemical infrastructure during 2024 and 2025 further signal a long-term shift toward localized production of advanced aqueous process fluids, positioning high-performance HWBF additive packages as a strategic growth pillar within the industrial lubricant additives market.

Industrial Lubricant Additives Market Share and Segmentation Insights

Dispersant Additives Lead Industrial Lubricant Formulations Through Sludge and Deposit Control

Dispersants accounted for 24.80% of the Industrial Lubricant Additives Market share in 2025, making them the most widely used additive type in industrial lubricant formulations. Dispersant additives are critical for maintaining lubricant cleanliness by suspending insoluble particles such as soot, oxidation byproducts, and degradation residues, preventing the formation of sludge and varnish deposits that can obstruct oil flow and damage equipment. These additives are widely incorporated into industrial engine oils, hydraulic fluids, compressor oils, and gear lubricants, where contamination control is essential for maintaining equipment reliability and operational efficiency. As industrial machinery operates under increasingly demanding conditions, lubricant formulations require higher dispersant loading to maintain stability over longer operating cycles. In 2025, technological development has focused on advanced polymeric dispersant chemistries capable of handling higher contaminant loads and maintaining suspension stability at elevated temperatures, supporting the industry shift toward extended oil drain intervals and reduced maintenance downtime across industrial operations.

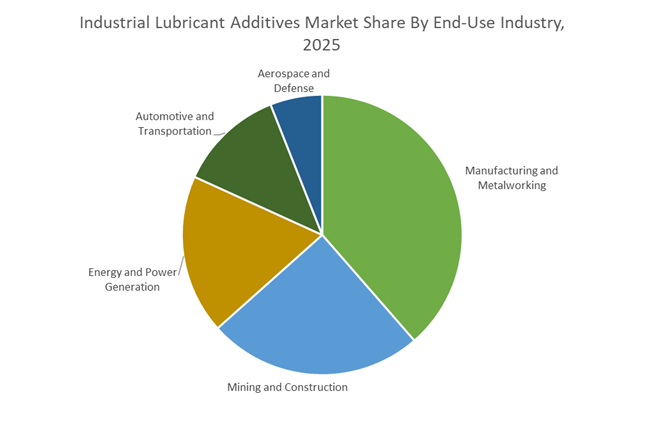

Manufacturing and Metalworking Sector Drives the Largest Demand for Industrial Lubricant Additives

Manufacturing and Metalworking represented 38.60% of the Industrial Lubricant Additives Market share in 2025, establishing it as the largest end-use industry for lubricant additive technologies. Industrial manufacturing facilities rely heavily on lubricants across numerous applications including hydraulic systems, gearboxes, compressors, turbine systems, machine tool operations, and metalworking processes, creating substantial demand for high-performance lubricant formulations. Additives such as dispersants, anti-wear agents, antioxidants, and corrosion inhibitors are essential for improving lubricant durability, reducing equipment wear, and maintaining operational efficiency in continuous production environments. The sector’s lubricant consumption is closely linked to global industrial production levels and factory output, making manufacturing activity a key driver of additive demand. In 2025, the rise of Industry 4.0 and predictive maintenance technologies is reshaping lubricant management practices. Industrial facilities increasingly use sensor-based monitoring systems and lubricant condition analysis to track additive depletion, contamination levels, and oil degradation in real time. This transition is driving demand for advanced additive packages designed to maintain performance for longer service intervals while supporting predictive maintenance strategies in smart manufacturing environments.

Competitive Landscape in Industrial Lubricant Additives Market

Lubrizol Expands Regionalization and Lithium Alternatives

The Lubrizol Corporation remains the global volume leader and is executing a “Local-for-Local” manufacturing strategy to reduce geopolitical supply exposure. In late 2025, it unveiled its China Automotive & Industrial Roadmap, focusing on localized R&D and tier-based market penetration for Asian lubricant blenders. In October 2025, Lubrizol expanded collaboration with Oil Store to strengthen finished fluid and additive package distribution across the UK and MENA region. A core strategic pivot involves scaling non-lithium grease thickener technologies to mitigate lithium price volatility. February 2026 technical releases highlight advanced dispersant and antioxidant systems capable of extending industrial oil drain intervals by up to 30%, reinforcing asset protection and energy-efficiency positioning.

Infineum Builds Asia-Centric Supply Chain

Infineum International Ltd., the Shell–ExxonMobil joint venture, is restructuring toward regional self-sufficiency in Asia-Pacific. In January 2026, it signed a framework agreement with Rianlon Corporation to integrate Chinese component manufacturing into its global additive supply network. Its new India blending facility is scheduled to reach full commercial production by Q3 2026, focusing on sulfonate and salicylate detergent packages. Infineum’s salicylate technology is increasingly critical for engines operating on alternative fuels such as LNG and hydrogen, where acid neutralization and deposit control profiles differ significantly from diesel systems. CEO Aldo Govi emphasized in early 2026 that supply resilience and regional integration are central to navigating trade and tariff complexity.

Afton Targets Hydrogen and Electrified Hardware

Afton Chemical Corporation is positioning itself at the forefront of hydrogen-compatible lubricant chemistry. In September 2025, it introduced HiTEC® 12582, the first commercially available additive package designed specifically for hydrogen heavy-duty engines, addressing unique oxidation and water-handling challenges. The company’s 2026 strategy centers on hardware-specific formulation guidance, moving away from fuel-agnostic lubricants. Afton is also expanding its Electrified Transmission Fluid (ETF) technology platform, emphasizing copper corrosion protection and enhanced thermal management for EV and industrial automation drivetrains. Through its “eVolving” framework, it supports additive development for off-highway electrified machinery and industrial robotics.

Chevron Oronite Strengthens RRBO and APAC Capacity

Chevron Oronite Company LLC is leveraging its parent’s integrated refining network to deliver high-stability additive chemistries. In January 2026, the company announced expanded distribution through Azelis South Africa, strengthening its African technical support network. Its Ningbo, China facility reached full capacity utilization in late 2025, becoming the primary APAC hub for CK-4 heavy-duty and industrial gear additive production. Newly introduced OLOA® 55620 packages target high-stress engine environments. A major 2026 research priority involves additive compatibility with re-refined base oils (RRBO), ensuring oxidation stability and deposit control in circular economy lubricant systems.

LANXESS Accelerates Sustainable EP Additives

LANXESS AG has completed its transition into a pure-play Specialty Additives company after divesting its urethane systems business in April 2025. In October 2025, it launched a lower-carbon Additin® RC 2515 sulfur carrier for extreme pressure applications, featuring ISCC PLUS certification and a 34% reduced carbon footprint. Its Scopeblue label identifies products containing at least 50% recycled or bio-based raw materials. Under its “Forward!” action plan, EBITDA rose 32% in 2025 through improved capacity utilization and cost optimization. In 2026, LANXESS is prioritizing high-margin industrial gear oils, metalworking additives, and climate-friendly EP systems aligned with European decarbonization standards.

BASF Scales Ashless and Sustainability-Certified Chemistries

BASF SE is expanding lubricant additive capacity at its Zhanjiang Verbund site in China, now a central growth engine for Asian markets. The company has restructured its Jurong Island operations in Singapore to focus on high-purity antioxidants and metal deactivators. For 2026, BASF targets group EBITDA between €6.2 billion and €7.0 billion, with increased revenue from sustainability-certified additive systems. Strategic R&D emphasis is on zero-ash anti-wear and EP chemistries designed for food-grade, environmentally sensitive, and low-ash industrial lubrication systems. The integrated Verbund model provides feedstock advantages in amines, phenols, and dispersant intermediates.

United States Industrial Lubricant Additives Market: Standards Reset, Electrification Readiness, and Oxidation Control Capacity

The United States industrial lubricant additives market is being redefined by tighter fuel quality standards, accelerated electrification, and durability requirements for high-stability machinery. In September 2025, BASF announced the launch of the Keropur AP 225-20 series to meet the revised TOP TIER™+ detergent gasoline standard, directly addressing injector deposit control challenges in gasoline direct injection engines. Commercial deliveries are scheduled for the first half of 2026, positioning detergent additive packages as a compliance enabler for refiners and blenders navigating higher cleanliness thresholds. In parallel, U.S. formulators are advancing beyond EPA Lowest Additive Concentration benchmarks, with 2025 portfolio updates optimized for California Air Resources Board approval ahead of mandatory 2027 timelines.

Electrification is reshaping additive architectures. In late 2025, Afton Chemical launched HiTEC 35701, the first complete eAxle additive engineered for direct-cooled electric motors with multi-speed systems, delivering copper protection in both liquid and vapor phases. The same year, Afton introduced a dedicated additive for hydrogen-fueled heavy-duty engines, signaling a pivot toward alternative powertrains in long-haul transport. Underpinning these innovations, BASF completed a multi-million-dollar expansion of aminic antioxidant capacity in March 2025, addressing demand for long-life lubricants required by high-temperature, high-oxidation industrial environments.

India Industrial Lubricant Additives Market: Manufacturing Scale-Up and Low-Carbon Innovation

India is rapidly strengthening its position as a manufacturing and innovation hub for industrial lubricant additives through greenfield investments, localized blending, and digital engineering. Lubrizol is developing a $200 million state-of-the-art facility in Aurangabad on a 120-acre site to expand domestic and export capabilities for high-performance additive packages. Complementing this, Infineum announced a new local blending facility for sulfonate and salicylate packages, with trial production targeted for mid-2025 and full commercial operations by the third quarter of 2025, reducing lead times for regional customers.

Innovation capacity is being reinforced through ecosystem investments. Chevron established the $1 billion Chevron Engineering and Innovation Excellence Center in Bengaluru in 2025 to advance lower-carbon solutions for global energy and lubricants through engineering and digital services. Earlier, Indian Oil and Gujarat Gas signed a non-binding memorandum in April 2024 to boost energy solutions for growing industries, catalyzing localized R&D for industrial-grade additives. On the product front, Savsol Corp launched Ester 5 in early 2024, a biodegradable ester additive designed to reduce friction and extend mileage in high-speed railway coaches and electric vehicle battery systems.

Germany Industrial Lubricant Additives Market: Certified Sustainability and Portfolio Refocus

Germany’s industrial lubricant additives sector is advancing through certified sustainability frameworks and strategic portfolio optimization. In November 2025, Infineum achieved ISCC PLUS certification across manufacturing sites under the Mass Balance approach, enabling lower-carbon lubricant production aligned with European sustainability reporting requirements effective in 2026. This certification facilitates the integration of renewable and circular feedstocks without disrupting performance-critical formulations.

Product and asset strategies are converging on higher value segments. In 2025, BASF commercially deployed Trilon G, a biodegradable GLDA-based chelating agent with 56% renewable carbon content, applicable in industrial cleaning and specialized lubricant formulations to meet Green Deal mandates. BASF also confirmed the divestment of its optical brightening agent business effective the first quarter of 2026, signaling a deliberate shift toward specialized, high-margin performance chemicals serving industrial lubricants and institutional applications.

Mexico Industrial Lubricant Additives Market: Antioxidant Supply for North America

Mexico is strengthening its role in the North American lubricant additives supply chain through targeted capacity expansion. In March 2025, BASF announced a significant expansion of aminic antioxidant capacity at its Puebla site, scheduled for completion in 2026. The investment is designed to supply automotive and industrial sectors across North America with additives that meet stringent oxidation stability and durability requirements, supporting long-drain intervals and high-temperature operations.

China Industrial Lubricant Additives Market: EV-Centric Innovation and Collaborative Decarbonization

China’s industrial lubricant additives market is aligning with electric mobility growth and collaborative decarbonization across the value chain. In late 2025, Lubrizol opened a Film Center of Excellence and commissioned a paint protection film production line in Shanghai, supporting development of specialized coatings and additive systems for electric vehicles and industrial machinery. This infrastructure enhances local formulation capabilities and accelerates application-specific testing.

Strategic collaboration is deepening. In November 2025, Infineum launched its refreshed Formulating Tomorrow initiative, centered on the China Business and Technology Centre, with a focus on joint decarbonization efforts across base oils, additives, and finished lubricants. The approach underscores China’s role as a co-development market for next-generation additive technologies rather than a downstream-only consumer.

Industrial Lubricant Additives: Country-Level Strategic Summary

Industrial Lubricant Additives Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Core Technology or Investment

|

Industry Direction

|

|

United States

|

Standards tightening and electrification

|

TOP TIER™+ detergents, eAxle and hydrogen additives, antioxidants

|

High-performance, future powertrain readiness

|

|

India

|

Manufacturing scale and digital innovation

|

Greenfield plants, local blending, biodegradable esters

|

Export-oriented growth with low-carbon focus

|

|

Germany

|

Certified sustainability and portfolio optimization

|

ISCC PLUS, GLDA chelation

|

Lower-carbon, high-margin formulations

|

|

Mexico

|

Regional supply security

|

Antioxidant capacity expansion

|

North America-focused stability additives

|

|

China

|

EV growth and co-development

|

Centers of excellence, collaborative decarbonization

|

Application-led innovation for electric mobility

|

Industrial Lubricant Additives Market Report Scope

Industrial Lubricant Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.8 Billion

|

|

Market Size (2034)

|

$11.7 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Additive Type (Dispersants, Detergents, Viscosity Index Improvers, Antioxidants, Anti-Wear and Extreme Pressure Agents, Friction Modifiers, Corrosion and Rust Inhibitors, Pour Point Depressants, Defoamers, Emulsifiers), By Base Oil Compatibility (Group I, II, and III Base Oils, Group IV Base Oils, Group V Base Oils), By Application (Industrial Engine Oils, Metalworking Fluids, Hydraulic Fluids, Industrial Gear Oils, Grease Additives, eMobility Fluids), By End-Use Industry (Manufacturing and Metalworking, Energy and Power Generation, Automotive and Transportation, Aerospace and Defense, Mining and Construction)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Lubrizol Corporation, Infineum International Ltd., Afton Chemical Corporation, Chevron Oronite Company LLC, BASF SE, Evonik Industries AG, LANXESS AG, Dover Chemical Corporation, Vanderbilt Chemicals, LLC, Sanyo Chemical Industries, Ltd., ADEKA Corporation, Songwon Industrial Co., Ltd., Clariant AG, King Industries, Inc., Italmatch Chemicals S.p.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Industrial Lubricant Additives Market Segmentation

By Additive Type

- Dispersants

- Detergents

- Viscosity Index Improvers

- Antioxidants

- Anti-Wear and Extreme Pressure Agents

- Friction Modifiers

- Corrosion and Rust Inhibitors

- Pour Point Depressants

- Defoamers

- Emulsifiers

By Base Oil Compatibility

- Group I, II, and III Base Oils

- Group IV Base Oils

- Group V Base Oils

By Application

- Industrial Engine Oils

- Metalworking Fluids

- Hydraulic Fluids

- Industrial Gear Oils

- Grease Additives

- eMobility Fluids

By End-Use Industry

- Manufacturing and Metalworking

- Energy and Power Generation

- Automotive and Transportation

- Aerospace and Defense

- Mining and Construction

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Industrial Lubricant Additives Industry

- Lubrizol Corporation

- Infineum International Ltd.

- Afton Chemical Corporation

- Chevron Oronite Company LLC

- BASF SE

- Evonik Industries AG

- LANXESS AG

- Dover Chemical Corporation

- Vanderbilt Chemicals, LLC

- Sanyo Chemical Industries, Ltd.

- ADEKA Corporation

- Songwon Industrial Co., Ltd.

- Clariant AG

- King Industries, Inc.

- Italmatch Chemicals S.p.A.

*- List not Exhaustive