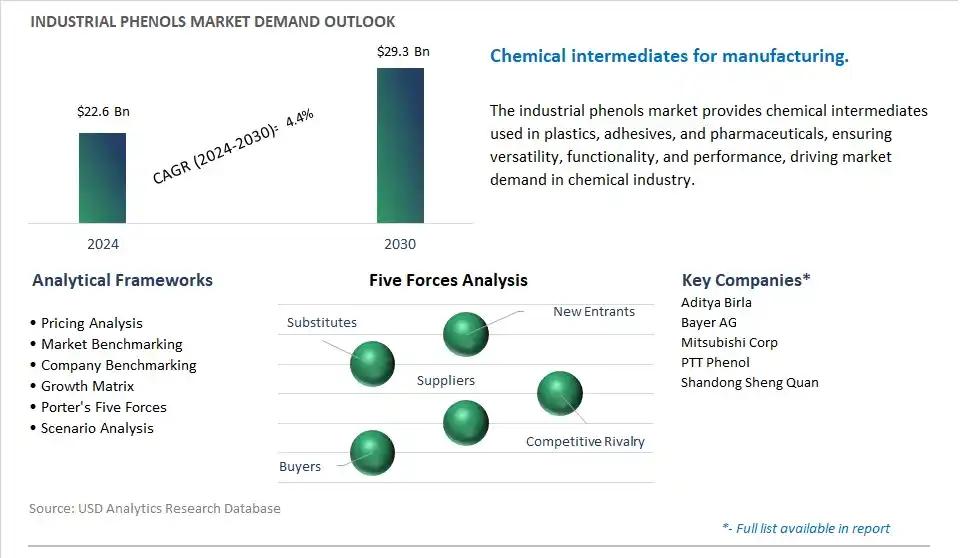

The global Industrial Phenols Market is poised to register a 4.4% CAGR from $22.6 Billion in 2024 to $29.3 Billion in 2030.

The global Industrial Phenols Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Epoxy Resins, Henol-Methanal Resins), By Application (Residential, Commercial).

An Introduction to Global Industrial Phenols Market in 2024

Industrial phenols are a group of organic compounds derived from benzene and used as key raw materials in various industrial processes such as plastics manufacturing, pharmaceutical synthesis, and chemical production. One key trend shaping the future of industrial phenols is the development of sustainable production methods and feedstocks to reduce environmental impact, improve resource efficiency, and meet regulatory requirements for hazardous chemical management and emissions reduction. Phenol producers are investing in alternative feedstock sources, such as biomass, lignin, and waste plastics, as well as green chemistry processes such as enzymatic catalysis, biotransformation, and solvent-free synthesis, to reduce dependency on fossil fuels and minimize carbon footprint in phenol production. Additionally, advancements in phenol purification, separation, and recovery technologies are improving process efficiency, product quality, and waste minimization, enabling closed-loop systems and resource recovery strategies to maximize resource utilization and minimize environmental impact. Moreover, the integration of phenol derivatives into sustainable product formulations, such as bio-based plastics, resins, and adhesives, is driving market expansion and innovation in the bioeconomy, supporting circular economy principles and sustainable development goals. As industries seek to transition to greener and more sustainable chemical processes, the industrial phenols industry is poised for innovation and growth, with opportunities for collaboration, technology transfer, and market expansion to meet the evolving needs of manufacturers, chemical producers, and regulatory stakeholders.

Industrial Phenols Market Competitive Landscape

The market report analyses the leading companies in the industry including Aditya Birla, Bayer AG, Mitsubishi Corp, PTT Phenol, Shandong Sheng Quan.

Industrial Phenols Market Dynamics

Industrial Phenols Market Trend: Increasing Demand for Phenolic Resins in Automotive and Construction Industries

A prominent trend in the industrial phenols market is the rising demand for phenolic resins, particularly in the automotive and construction industries. Phenolic resins, derived from industrial phenols, are widely used as adhesives, coatings, and molding compounds due to their exceptional heat resistance, mechanical strength, and flame retardant properties. In the automotive sector, phenolic resins are utilized in brake pads, clutch facings, and interior components, contributing to improved safety and performance standards. Similarly, in the construction industry, phenolic resins are employed in laminates, insulation panels, and structural components, providing durability and fire resistance. This is driven by the growing emphasis on lightweight materials, energy efficiency, and safety regulations in both sectors, driving the demand for industrial phenols as key raw materials for phenolic resin production.

Industrial Phenols Market Driver: Growth in End-Use Industries such as Electronics and Consumer Goods

A key driver propelling the industrial phenols market is the expanding demand from end-use industries such as electronics and consumer goods. Phenolic compounds find widespread applications in the manufacturing of electrical insulators, printed circuit boards, and electronic components due to their excellent dielectric properties and thermal stability. Moreover, phenolic resins are utilized in consumer goods such as kitchenware, laminates, and coatings, offering heat resistance, chemical resistance, and durability. The proliferation of electronic devices, household appliances, and consumer products worldwide is driving the demand for industrial phenols, as manufacturers seek reliable and cost-effective materials to meet stringent performance and safety requirements in their products.

Industrial Phenols Market Opportunity: Development of Bio-based Phenol Production Technologies

An opportunity for growth in the industrial phenols market lies in the development of bio-based phenol production technologies. With increasing environmental concerns and regulatory pressures to reduce carbon emissions and reliance on fossil fuels, there is a growing interest in sustainable alternatives to conventional phenol production methods, which typically involve petrochemical feedstocks. Bio-based phenol production technologies utilize renewable feedstocks such as biomass, lignin, or bio-based chemicals derived from agricultural or forestry residues, offering potential environmental benefits and reducing dependence on finite fossil resources. By investing in research and innovation, companies can capitalize on the growing demand for eco-friendly and sustainable solutions in the industrial phenols market, while also positioning themselves as leaders in green chemistry and sustainability initiatives.

Industrial Phenols Market Ecosystem

The industrial phenols market encompasses various stages, from feedstock acquisition to end-user applications, involving diverse key companies. Feedstock acquisition primarily relies on petrochemical companies including Exxon Mobil and Royal Dutch Shell, which provide benzene and other aromatic hydrocarbons, the primary feedstock for modern phenol production. Phenol production predominantly employs the cumene process, with major producers including LyondellBasell Industries, SABIC, BASF, Covestro, and Dow Chemical. These companies convert benzene and propylene into phenol and acetone. Following production, companies specialize in purifying crude phenol or producing specific phenol derivatives with varying functionalities.

Distribution channels involve chemical distributors including Brenntag AG and Univar Solutions Inc., which distribute a wide range of industrial chemicals, including phenols, to end-users. Additionally, large phenol producers engage in direct sales, offering customized solutions through dedicated sales teams for specific industries. End-users of industrial phenols span various sectors, including the resins and plastics industry, where phenol serves as a key raw material for phenol-formaldehyde resins used in plywood adhesives, molding compounds, and laminates. Phenol is also crucial for bisphenol A (BPA) production, although its use is facing restrictions due to health concerns. Furthermore, phenol derivatives find applications in the pharmaceutical industry, agrochemicals sector, and various other industrial applications including dyes, explosives, and disinfectants.

Industrial Phenols Market Share Analysis: Phenol-Methanal Resins held the dominant revenue share in 2024

The phenol-methanal resins segment is the largest sector in the Industrial Phenols Market, driven by diverse pivotal factors contributing to its dominance. Phenol-methanal resins, commonly known as phenolic resins, are widely used in various industrial applications due to their exceptional properties, versatility, and cost-effectiveness. These resins are extensively employed in the production of adhesives, coatings, laminates, molded products, and insulation materials across industries such as automotive, construction, electronics, and consumer goods. The dominance of phenol-methanal resins can be attributed to their excellent adhesive properties, high heat resistance, chemical stability, and mechanical strength. In addition, phenolic resins offer superior fire resistance, making them suitable for applications where fire safety is a priority. Additionally, the ease of processing and curing of phenolic resins enhances manufacturing efficiency and productivity. Further, the availability of raw materials such as phenol and formaldehyde, along with established manufacturing processes, contributes to the widespread adoption of phenol-methanal resins in industrial applications. As industries continue to prioritize performance, durability, and cost-effectiveness in their products and processes, the phenol-methanal resins segment of the industrial phenols market is expected to maintain its leading position and witness sustained growth in the coming years.

Industrial Phenols Market Share Analysis: Commercial is the fastest growing market segment over the forecast period to 2030

The commercial segment is the fastest-growing sector in the Industrial Phenols Market, driven by diverse critical factors propelling its rapid expansion. Industrial phenols find extensive applications in various commercial sectors, including construction, manufacturing, automotive, electronics, and healthcare. In the commercial sector, phenolic compounds are used in the production of adhesives, sealants, coatings, laminates, insulation materials, and disinfectants, among others. With the increasing demand for durable and high-performance materials in commercial applications, there's a rising need for phenolic products that offer superior mechanical strength, chemical resistance, thermal stability, and fire retardancy. In addition, the commercial sector encompasses a wide range of industries and applications, providing diverse opportunities for the utilization of phenolic compounds in different products and processes. Additionally, the growing focus on sustainability and environmental regulations in commercial sectors drives the demand for eco-friendly phenolic materials and formulations. Further, the commercial sector's rapid urbanization, infrastructure development, and industrialization contribute to the increasing consumption of phenolic products in construction, manufacturing, and other commercial activities. As commercial industries continue to evolve and innovate to meet market demands and regulatory requirements, the commercial segment of the industrial phenols market is poised for significant growth, presenting lucrative opportunities for industry stakeholders.

Industrial Phenols Market Report Scope-

By Type

Epoxy Resins

Henol-Methanal Resins

By Application

Residential

Commercial

Industrial Phenols Market Companies Profiled

Aditya Birla

Bayer AG

Mitsubishi Corp

PTT Phenol

Shandong Sheng Quan

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Industrial Phenols Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Industrial Phenols Market Size Outlook, $ Million, 2021 to 2030

3.2 Industrial Phenols Market Outlook by Type, $ Million, 2021 to 2030

3.3 Industrial Phenols Market Outlook by Product, $ Million, 2021 to 2030

3.4 Industrial Phenols Market Outlook by Application, $ Million, 2021 to 2030

3.5 Industrial Phenols Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Industrial Phenols Industry

4.2 Key Market Trends in Industrial Phenols Industry

4.3 Potential Opportunities in Industrial Phenols Industry

4.4 Key Challenges in Industrial Phenols Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Industrial Phenols Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Industrial Phenols Market Outlook by Segments

7.1 Industrial Phenols Market Outlook by Segments, $ Million, 2021- 2030

By Type

Epoxy Resins

Henol-Methanal Resins

By Application

Residential

Commercial

8 North America Industrial Phenols Market Analysis and Outlook To 2030

8.1 Introduction to North America Industrial Phenols Markets in 2024

8.2 North America Industrial Phenols Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Industrial Phenols Market size Outlook by Segments, 2021-2030

By Type

Epoxy Resins

Henol-Methanal Resins

By Application

Residential

Commercial

9 Europe Industrial Phenols Market Analysis and Outlook To 2030

9.1 Introduction to Europe Industrial Phenols Markets in 2024

9.2 Europe Industrial Phenols Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Industrial Phenols Market Size Outlook by Segments, 2021-2030

By Type

Epoxy Resins

Henol-Methanal Resins

By Application

Residential

Commercial

10 Asia Pacific Industrial Phenols Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Industrial Phenols Markets in 2024

10.2 Asia Pacific Industrial Phenols Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Industrial Phenols Market size Outlook by Segments, 2021-2030

By Type

Epoxy Resins

Henol-Methanal Resins

By Application

Residential

Commercial

11 South America Industrial Phenols Market Analysis and Outlook To 2030

11.1 Introduction to South America Industrial Phenols Markets in 2024

11.2 South America Industrial Phenols Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Industrial Phenols Market size Outlook by Segments, 2021-2030

By Type

Epoxy Resins

Henol-Methanal Resins

By Application

Residential

Commercial

12 Middle East and Africa Industrial Phenols Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Industrial Phenols Markets in 2024

12.2 Middle East and Africa Industrial Phenols Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Industrial Phenols Market size Outlook by Segments, 2021-2030

By Type

Epoxy Resins

Henol-Methanal Resins

By Application

Residential

Commercial

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Aditya Birla

Bayer AG

Mitsubishi Corp

PTT Phenol

Shandong Sheng Quan

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Epoxy Resins

Henol-Methanal Resins

By Application

Residential

Commercial

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)