Industrial Wastewater Operation & Maintenance Services Market Overview

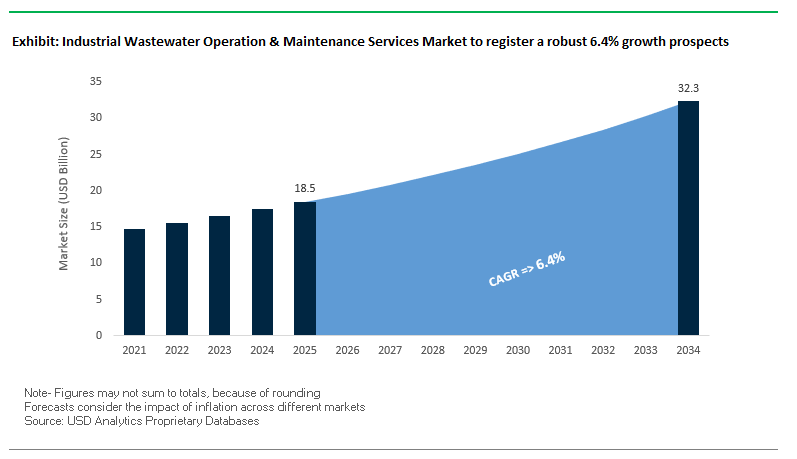

The global industrial wastewater operation & maintenance (O&M) services market is projected to grow from $18.5 billion in 2025 to $32.3 billion by 2034, achieving a CAGR of 6.4%. The market is propelled by stringent environmental regulations, increasing industrial water reuse, and the rising adoption of digital and energy-efficient wastewater management solutions. Industrial O&M services are evolving beyond routine maintenance, incorporating AI-driven monitoring, predictive analytics, and resource recovery to optimize operations and reduce environmental footprints.

Industry Stakeholders are increasingly viewing wastewater as a valuable resource rather than a liability, emphasizing energy recovery, chemical reuse, and digital plant management. The sector is witnessing a strong shift toward sustainable, automated, and cost-efficient O&M solutions, driven by both regulatory compliance and operational efficiency goals.

Key Insights for Industry Stakeholders:

- Regulatory Compliance: New regulations, such as India’s Liquid Waste Management Rules effective October 2025, mandate minimum reuse of industrial wastewater, driving demand for advanced O&M services.

- Resource Recovery: Technologies like anaerobic digestion are enabling energy-neutral operations and biogas production from industrial wastewater.

- Water Reuse and Circular Economy: Industrial water reuse is growing under initiatives like the EU Circular Economy Action Plan, reducing freshwater withdrawals and supporting sustainability goals.

- Digitalization: IIoT, smart sensors, and AI-driven predictive maintenance are optimizing chemical dosing, equipment reliability, and operational efficiency.

- Emerging Contaminants Management: Industries increasingly require O&M services capable of addressing PFAS and other contaminants, ensuring compliance and environmental protection.

Market Analysis: Recent Developments in Industrial Wastewater O&M Services

The industrial wastewater O&M services market has seen significant expansion through strategic acquisitions, new technology deployments, and sustainable projects. In August 2025, Abu Dhabi National Energy Company (TAQA) acquired GS Inima, a Spanish water treatment and desalination company, for $1.2 billion, significantly expanding its industrial wastewater portfolio globally. During the same month, VA Tech Wabag secured a five-year, $13.6 million O&M contract in Bahrain for the Madinat Salman Sewage Treatment Plant, underscoring the value of repeat orders and long-term operational expertise.

In July 2025, SUEZ inaugurated a biogas production unit at the Seine Aval wastewater plant in France, highlighting energy recovery and circular economy initiatives. Concurrently, Veolia launched one of the largest PFAS treatment plants in Delaware, U.S., employing proprietary technologies to serve over 100,000 residents, reflecting growing industry responsiveness to emerging contaminants. In April 2025, SUEZ commissioned China’s largest industrial membrane-based desalination plant for Wanhua Chemical’s Penglai Industrial Park, promoting water conservation in the chemical sector.

Notable prior developments include Jacobs’ O&M contract expansions across western U.S. (November 2024) using its Intelligent O&M digital solutions, SUEZ’s Hillerød plant upgrade in Denmark (October 2024) addressing pharmaceutical micropollutants, and Veolia’s mobile water services deployment in Malaysia (March 2024), demonstrating strategic flexibility to serve industrial clients in temporary or emergency scenarios.

Key Trends Shaping Industrial Wastewater O&M Services

Transition from CapEx to OpEx Models

The industrial wastewater O&M services market is witnessing a fundamental shift from large capital expenditures to flexible, operational expenditure models. Leading providers like Veolia Water Technologies are promoting Water-as-a-Service (WaaS), enabling customers to pay based on water volume treated rather than upfront infrastructure costs. A global case in Alice, Texas, demonstrates that this model allowed the city to avoid a $12 million capital investment, while ensuring lower water rates for residents. This trend highlights the growing preference for predictable operational costs, financial flexibility, and outsourced management of complex treatment infrastructure.

Integration of Digital Solutions and Predictive Analytics

Digitalization is revolutionizing industrial wastewater O&M. AI and IoT-driven systems optimize chemical dosing, blower setpoints, and treatment parameters, achieving up to 20% reduction in chemical usage while reducing energy consumption. Companies are leveraging these technologies to minimize unplanned disruptions. For example, utilities employing Xylem’s smart sewer solutions reported an 80% reduction in Combined Sewer Overflow (CSO) volumes, translating into significant cost avoidance. These developments illustrate that predictive analytics and real-time monitoring are becoming essential for maximizing operational efficiency and compliance.

Corporate Sustainability Goals and the Circular Economy

Sustainability and circular economy principles are becoming central to industrial wastewater management. Treated effluent is increasingly reused for industrial processes, irrigation, or energy generation. A California food processing company converted anaerobic digestion by-products into biogas, saving approximately US$700,000 annually in energy costs. This trend underscores how O&M services are evolving from mere compliance-focused operations to strategic enablers of resource recovery, cost reduction, and environmental sustainability.

Strategic Opportunities in Industrial Wastewater O&M

The market presents compelling opportunities for integrated O&M providers offering operations, maintenance, spare parts management, emergency response, and consulting services. Digital transformation enables predictive maintenance and energy optimization, while circular economy initiatives unlock revenue from wastewater reuse. Flexible payment models (WaaS/OpEx) are expanding adoption among industrial and municipal clients. High-value opportunities exist in regulated, high-complexity industries like pharmaceuticals, chemicals, and food & beverage, where expert O&M services directly impact compliance, efficiency, and profitability.

Market Share Insights of Industrial Wastewater Operation & Maintenance Services

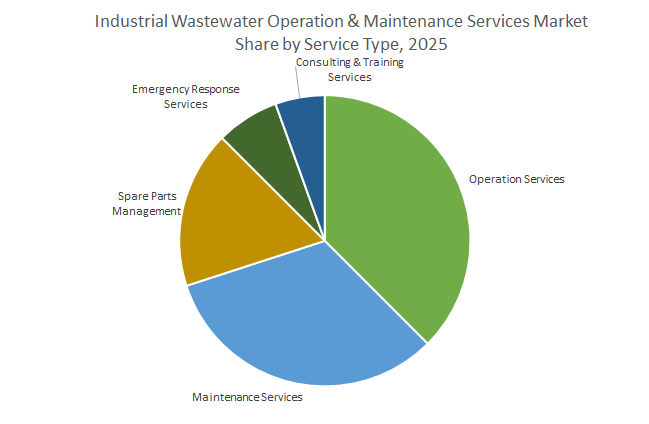

Market Share by Service Type: Operation Services Lead with Maintenance and Spare Parts

Operation Services (38%) dominate, encompassing 24/7 process control, monitoring, and compliance reporting. Maintenance Services (32.8%) prevent unplanned shutdowns and ensure plant reliability, including calibration and equipment overhauls. Spare Parts Management (16.9%) ensures critical components like pumps, membranes, and aerators are available to minimize downtime. Emergency Response Services act as insurance during system upsets or spills, while Consulting & Training supports process optimization, feasibility studies, and staff skill development. This distribution highlights the critical importance of operations and maintenance in managing complex industrial wastewater streams.

Market Share by Treatment Technology: Biological and Physical-Chemical Lead

Biological Treatment (32.8%), including activated sludge, MBBR, MBR, and anaerobic digestion, dominates due to cost-effective organic removal. Physical-Chemical Treatment (26.9%) handles solids, metals, and FOG, protecting downstream processes. Membrane Filtration (16.9%) and Advanced Treatment cater to high-value effluent reuse and strict regulatory compliance. Sludge Handling & Dewatering (14.2%) remains a universal challenge due to cost, regulation, and disposal logistics. These segments emphasize high-skill, high-value O&M services critical to industrial compliance and operational excellence.

Market Share by End-User Industry: Food & Beverage and Chemicals Lead

The Food & Beverage (22.5%) segment leads due to high wastewater volumes and strong incentives for reuse and energy recovery. Chemicals & Petrochemicals (16.9%) and Pharmaceuticals (12.6%) represent high-value segments with complex effluent requiring specialized treatment. Power Generation (13.5%), Metals & Mining, and Pulp & Paper are also significant due to cooling blowdown, sludge management, and recalcitrant compounds. Oil & Gas, Textiles, and Semiconductors & Electronics reflect niche, high-complexity O&M opportunities. Each industry’s unique effluent profile underscores the need for tailored, expert O&M services and explains the diverse market segmentation.

United States: Infrastructure Funding and Regulatory Pressure Accelerating O&M Adoption

The United States industrial wastewater O&M services market is undergoing a major transformation fueled by the Environmental Protection Agency’s (EPA) initiatives under the Bipartisan Infrastructure Law (BIL), which allocates over $50 billion to modernize the nation’s water infrastructure. This unprecedented funding is accelerating the adoption of digital technologies, such as remote monitoring and AI-driven optimization, to modernize aging industrial wastewater treatment facilities. The result is a surge in demand for outsourced O&M contracts, as industries increasingly rely on service providers to ensure operational reliability and cost-efficiency.

At the same time, the EPA’s National Pollutant Discharge Elimination System (NPDES) permits are becoming stricter, particularly with respect to emerging contaminants like per- and polyfluoroalkyl substances (PFAS). This compliance pressure is reshaping corporate strategies, pushing industries toward O&M partnerships for consistent regulatory adherence. On the corporate side, the 2023 merger between Xylem and Evoqua has created a powerhouse in industrial wastewater O&M, offering integrated solutions that span monitoring, treatment, and maintenance. Recent projects, such as Corix DE Systems’ innovative energy system in Bellingham’s Waterfront District (October 2024), highlight how energy recovery is being embedded into industrial wastewater management, requiring highly specialized O&M expertise. The U.S. market is strongly supported by applications in food and beverage, chemicals, and pharmaceuticals, where on-site treatment is critical to meeting regulatory obligations and lowering discharge costs.

China: Policy-Driven Circular Economy Boosting Industrial Wastewater O&M Services

China is one of the fastest-growing markets for industrial wastewater O&M services, driven by strong government mandates under the 14th Five-Year Plan (2021–2025), which targets recycling 25% of urban wastewater by 2025. Complementing this, the “Beautiful China” initiative mandates industrial resource recovery and reuse, creating significant demand for advanced O&M services to maintain compliance and operational efficiency. In August 2024, a Chinese wastewater project earned the International Water Association (IWA) innovation prize for its sustainable resource recovery model, underscoring the country’s leadership in pioneering industrial wastewater solutions.

China enforces some of the world’s most stringent wastewater discharge standards, requiring companies to secure permits and meet strict effluent benchmarks. The O&M market is further strengthened by rapid deployment of technologies aligned with circular economy principles. For instance, a dairy facility in Inner Mongolia has successfully achieved 80% wastewater recycling for cleaning and cooling purposes, which is only sustainable through specialized O&M services. Key industrial applications fueling demand include high-organic-load effluents from food and beverage, pulp and paper, and pharmaceutical sectors. Additionally, renewable energy recovery from biogas has become a major operational priority, reinforcing the importance of advanced O&M systems across the industrial landscape.

India: Government Missions and Private Investments Driving O&M Expansion

India’s industrial wastewater O&M market is being reshaped by government-led initiatives such as the Jal Jeevan Mission, the Namami Gange Mission, and Swachh Bharat Mission-Urban (SBM-U) 2.0, which emphasize wastewater management and ensure that untreated effluents are not discharged into rivers and ecosystems. These initiatives have triggered demand for professional O&M services, particularly for common effluent treatment plants (CETPs) serving industrial clusters. In May 2025, Enviro Infra Engineers Limited secured an EPC order worth over ₹127 crore, including five years of O&M, pushing its order book to ₹738 crore and demonstrating the market’s preference for long-term service-based contracts.

Corporate initiatives are also shaping the competitive landscape. VA Tech Wabag, a leading Indian water technology firm, is pursuing an FY26 strategy that prioritizes high-margin O&M contracts both domestically and in the Middle East and Africa, building on its expertise in desalination and climate-resilient wastewater solutions. Industrial wastewater O&M demand is primarily fueled by efforts to clean rivers and secure reliable water supply for urban and rural populations. With industrial clusters expanding rapidly and stricter enforcement of pollution norms, India presents one of the most lucrative long-term markets for outsourced O&M services.

Germany: Advanced Regulations Driving Demand for Specialized Wastewater O&M

Germany is at the forefront of regulatory-driven demand for industrial wastewater O&M services. The revised EU Urban Wastewater Treatment Directive, implemented in January 2025, requires the addition of a 4th purification stage to eliminate micropollutants, adding significant complexity to wastewater treatment systems. Industrial operators increasingly depend on specialized O&M partners to manage advanced purification technologies while ensuring regulatory compliance under stringent EU standards.

Technological advancements are a key feature of Germany’s market, with the Federal Environment Agency (UBA) encouraging digital monitoring, AI-driven optimization, and digital twins to improve treatment efficiency in the face of climate change. Companies like H2O GmbH and GEA Group AG are leading in the Zero Liquid Discharge (ZLD) systems segment, offering innovative wastewater management technologies bundled with long-term O&M services. The result is a strong shift towards technology-enabled operation and maintenance contracts that align with sustainability objectives and EU climate goals.

Singapore: Innovation Hub for Low-Maintenance Wastewater O&M Technologies

Singapore has positioned itself as a hub for cutting-edge wastewater treatment technologies that transform O&M service models. In January 2024, Hydroleap introduced its Advanced Electrochemical Treatment (AET) technology, which eliminates the need for chemicals and reduces operational man-hours by up to 95%, thereby creating demand for specialized O&M to manage low-maintenance, technology-driven systems. This reflects the country’s long-term focus on sustainable, resource-efficient industrial wastewater management.

Corporate collaboration further strengthens Singapore’s position. CleanEdge Water Pte Ltd. plays a leading role in integrated industrial wastewater solutions, and in July 2024, it partnered with IDE Technologies to deliver a state-of-the-art wastewater treatment facility for the mining industry in India. Singapore’s O&M market is primarily driven by water recycling and reuse initiatives that ensure water security in a resource-scarce environment, making it one of the most innovation-led wastewater O&M ecosystems in Asia.

Saudi Arabia: PPP Projects and Infrastructure Investments Driving O&M Growth

Saudi Arabia is scaling up its industrial wastewater O&M services market through large-scale infrastructure investments backed by the Public-Private Partnership (PPP) model. The Saudi Water Partnership Company (SWPC) continues to award new projects with embedded long-term O&M contracts, while the National Water Company (NWC) announced plans in May 2025 to award 15 sewage infrastructure projects worth over $613.3 million. These projects are designed to strengthen wastewater management capacity in rapidly growing urban centers like Jeddah.

The Kingdom’s O&M market is driven by the urgent need to provide reliable wastewater services for a booming population and expanding industrial base. The government’s emphasis on operational efficiency and sustainable urban growth ensures strong demand for specialized O&M providers who can deliver performance-driven solutions across the wastewater lifecycle.

Competitive Landscape of Industrial Wastewater O&M Services Market

The industrial wastewater O&M services market is highly competitive, dominated by global players providing integrated, technology-driven solutions. Companies differentiate through digital platforms, energy recovery capabilities, sustainable operations, and expertise in emerging contaminants management.

Veolia Environnement S.A. leads with sustainable and digitally optimized O&M solutions

Veolia offers end-to-end industrial wastewater services, combining advanced technologies such as AnoxKaldnes™ MBBR and Biothane® anaerobic digestion. Its Hubgrade digital platform leverages AI and analytics to optimize operations and reduce environmental impact. In June 2025, Veolia introduced Drop® technology in Europe, achieving up to 99.9999% destruction of targeted PFAS, highlighting rapid innovation in addressing critical environmental challenges.

SUEZ S.A. excels in automated industrial wastewater management

SUEZ provides comprehensive engineering, construction, and O&M services, with a strong footprint in chemical and petrochemical industries. Its fully automated desalination plant for Wanhua Chemical in China (April 2025) demonstrates expertise in large-scale industrial projects. Strategic partnerships, such as with Renault Group (September 2024), emphasize circular economy initiatives and resource recovery. The company also leverages digital tools and automated facilities to enhance operational efficiency and sustainability.

Jacobs Engineering Group Inc. drives digital-first wastewater O&M in North America

Jacobs combines engineering expertise with innovative digital solutions, including the Digital OneWater suite, Intelligent O&M, Aqua DNA, and Dragonfly, to optimize industrial wastewater operations. In July 2025, Jacobs secured multiple O&M contracts across western U.S., reinforcing its regional presence. The company focuses on resilient infrastructure delivery and complex project management, including modernization of utilities and integration of digital solutions.

VA Tech Wabag Ltd. emphasizes long-term contracts and lifecycle management

VA Tech Wabag, a leading Indian multinational, specializes in industrial wastewater O&M, particularly in municipal and industrial sectors. Its August 2025 repeat O&M contract in Bahrain illustrates the company’s ability to secure long-term agreements. Wabag offers full lifecycle management, from design to operation, incorporating tertiary treatment, aerobic sludge digestion, and thermal drying technologies.

Evoqua Water Technologies (A Xylem Brand) focuses on resource recovery and emerging contaminants

Evoqua Water Technologies provides a wide range of industrial O&M services, including filtration, disinfection, and anaerobic digestion. The company has a strong focus on PFAS removal and energy recovery. In March 2023, Evoqua expanded its U.S. footprint by acquiring a Texas-based industrial water service business. Its technologies enable clients to convert wastewater into renewable energy, reflecting a commitment to sustainable and circular industrial operations.

Industrial Wastewater Operation & Maintenance Services Market Report Scope

Industrial Wastewater Operation & Maintenance Services Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$18.5 Billion

|

|

Market Size (2034)

|

$32.3 Billion

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Service Type (Operation Services, Maintenance Services, Spare Parts Management, Emergency Response Services, Consulting & Training Services), By Treatment Technology (Biological Treatment, Physical-Chemical Treatment, Membrane Filtration, Advanced Treatment, Sludge Handling & Dewatering), By End-User Industry (Food & Beverage, Chemicals & Petrochemicals, Pharmaceuticals, Oil & Gas, Power Generation, Metals & Mining, Pulp & Paper, Textiles, Semiconductors & Electronics), By Contract Model (Full-Outsourcing, Performance-based Contracts, Time & Material Contracts, Fixed-price Contracts), By Service Provider Type (Technology Providers & OEMs, Engineering, Procurement, and Construction (EPC) Firms, Specialized O&M Service Companies, Water & Wastewater Utility Companies)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., Evoqua Water Technologies, VA Tech Wabag Ltd., Aquatech International, DuPont de Nemours, Inc., Alfa Laval, Kubota Corporation, Kurita Water Industries Ltd., H2O GmbH, Thermax Limited, Ecolab, Enviro Infra Engineers Limited, Siemens

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Industrial Wastewater Operation & Maintenance Services Market Segmentation

By Service Type

- Operation Services

- Maintenance Services

- Spare Parts Management

- Emergency Response Services

- Consulting & Training Services

By Treatment Technology

- Biological Treatment

- Physical-Chemical Treatment

- Membrane Filtration

- Advanced Treatment

- Sludge Handling & Dewatering

By End-User Industry

- Food & Beverage

- Chemicals & Petrochemicals

- Pharmaceuticals

- Oil & Gas

- Power Generation

- Metals & Mining

- Pulp & Paper

- Textiles

- Semiconductors & Electronics

By Contract Model

- Full-Outsourcing

- Performance-based Contracts

- Time & Material Contracts

- Fixed-price Contracts

By Service Provider Type

- Technology Providers & OEMs

- Engineering, Procurement, and Construction (EPC) Firms

- Specialized O&M Service Companies

- Water & Wastewater Utility Companies

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Industrial Wastewater Operation & Maintenance Services Industry include-

- Veolia

- SUEZ

- Xylem Inc.

- Evoqua Water Technologies

- VA Tech Wabag Ltd.

- Aquatech International

- DuPont de Nemours, Inc.

- Alfa Laval

- Kubota Corporation

- Kurita Water Industries Ltd.

- H2O GmbH

- Thermax Limited

- Ecolab

- Enviro Infra Engineers Limited

- Siemens

*- List not Exhaustive

Research Coverage

The Industrial Wastewater O&M Services Market Report by USDAnalytics investigates the evolution of outsourced operations from routine upkeep to digital, performance-driven service models that maximize compliance, reuse, and resource recovery. It highlights breakthroughs in AI-enabled optimization, predictive analytics, and circular economy integrations; delivers analysis reviews on OpEx/WaaS contracting, PFAS readiness, and energy-neutral treatment; and highlights how emerging regulations are reshaping service scopes, SLAs, and risk allocation. By synthesizing cross-industry case learnings and technology benchmarks, this report is an essential resource for CXOs, plant heads, and ESG leaders seeking to lower total cost of ownership, harden compliance, and unlock value from wastewater through resilient, automated O&M programs. Scope Includes-

- By Service Type: Operation Services; Maintenance Services; Spare Parts Management; Emergency Response Services; Consulting & Training Services

- By Treatment Technology: Biological Treatment; Physical-Chemical Treatment; Membrane Filtration; Advanced Treatment; Sludge Handling & Dewatering

- By End-User Industry: Food & Beverage; Chemicals & Petrochemicals; Pharmaceuticals; Oil & Gas; Power Generation; Metals & Mining; Pulp & Paper; Textiles; Semiconductors & Electronics

- By Contract Model: Full-Outsourcing; Performance-based Contracts; Time & Material Contracts; Fixed-price Contracts

- By Service Provider Type: Technology Providers & OEMs; EPC Firms; Specialized O&M Service Companies; Water & Wastewater Utility Companies

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Profiles of 15+ companies): Veolia; SUEZ; Xylem Inc.; Evoqua Water Technologies; VA Tech Wabag Ltd.; Aquatech International; DuPont de Nemours, Inc.; Alfa Laval; Kubota Corporation; Kurita Water Industries Ltd.; H2O GmbH; Thermax Limited; Ecolab; Enviro Infra Engineers Limited; Siemens

Methodology

USDAnalytics applies a mixed-method approach combining executive interviews, plant walk-throughs, and expert panels with secondary validation from regulatory filings, permits, EHS disclosures, and technical literature. We calibrate segment baselines using bottom-up capacity/O&M spend models at site level, align them with top-down industry output, and triangulate with announced contracts and service backlogs. Forecasts (2025–2034) incorporate regulatory timelines, capex-to-opex migration rates, digital adoption curves, tariff/energy sensitivities, and reuse mandates. Competitive positioning leverages technology benchmarking (biological vs. phys-chem vs. membrane/advanced), PFAS readiness scoring, SLA structures, and OpEx contract archetypes to ensure decision-grade accuracy.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Industrial Wastewater Operation & Maintenance Services Market

1. Executive Summary

1.1. Market Highlights & Key Projections

1.2. Global Market Snapshot

1.3. Key Findings

2. Industrial Wastewater O&M Services Market Overview (2025–2034)

2.1. Introduction

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $18.5 Billion

2.2.2. Forecasted Market Size (2034): $32.3 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 6.4%

2.3. Market Drivers and Challenges

2.3.1. Drivers: Stricter Regulations, Water Reuse, and Digitalization

2.3.2. Challenges: Capital Intensity and Complexity of Emerging Contaminants

2.4. Key Insights for Industry Stakeholders

3. Key Market Trends and Recent Developments

3.1. Transition from CapEx to OpEx Models (e.g., Water-as-a-Service)

3.2. Integration of Digital Solutions and Predictive Analytics

3.3. Corporate Sustainability Goals and the Circular Economy

3.4. Recent Developments & Strategic Moves (2024–2025)

3.4.1. Strategic Acquisitions and Partnerships

3.4.2. New Technology Deployments and Project Awards

4. Industrial Wastewater O&M Services Market – Segmentation Insights

4.1. By Service Type

4.1.1. Operation Services (38% Market Share)

4.1.2. Maintenance Services (32.8% Market Share)

4.1.3. Spare Parts Management (16.9% Market Share)

4.1.4. Emergency Response Services

4.1.5. Consulting & Training Services

4.2. By Treatment Technology

4.2.1. Biological Treatment (32.8% Market Share)

4.2.2. Physical-Chemical Treatment (26.9% Market Share)

4.2.3. Membrane Filtration (16.9% Market Share)

4.2.4. Advanced Treatment

4.2.5. Sludge Handling & Dewatering (14.2% Market Share)

4.3. By End-User Industry

4.3.1. Food & Beverage (22.5% Market Share)

4.3.2. Chemicals & Petrochemicals (16.9% Market Share)

4.3.3. Power Generation (13.5% Market Share)

4.3.4. Pharmaceuticals (12.6% Market Share)

4.3.5. Oil & Gas

4.3.6. Metals & Mining

4.3.7. Pulp & Paper

4.3.8. Textiles

4.3.9. Semiconductors & Electronics

4.4. By Contract Model

4.4.1. Full-Outsourcing

4.4.2. Performance-based Contracts

4.4.3. Time & Material Contracts

4.4.4. Fixed-price Contracts

4.5. By Service Provider Type

4.5.1. Technology Providers & OEMs

4.5.2. Engineering, Procurement, and Construction (EPC) Firms

4.5.3. Specialized O&M Service Companies

4.5.4. Water & Wastewater Utility Companies

5. Country Analysis and Outlook: Industrial Wastewater O&M Services Market

5.1. United States: Infrastructure Funding and Regulatory Pressure

5.2. China: Policy-Driven Circular Economy

5.3. India: Government Missions and Private Investments

5.4. Germany: Advanced Regulations and Technology Adoption

5.5. Singapore: Innovation Hub for Low-Maintenance Technologies

5.6. Saudi Arabia: PPP Projects and Infrastructure Investments

6. Market Size Outlook by Region (2025-2034)

6.1. North America Industrial Wastewater O&M Services Market Size Outlook to 2034

6.1.1. By Service Type

6.1.2. By Treatment Technology

6.1.3. By Country (US, Canada, Mexico)

6.2. Europe Industrial Wastewater O&M Services Market Size Outlook to 2034

6.2.1. By Service Type

6.2.2. By Treatment Technology

6.2.3. By Country (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

6.3. Asia Pacific Industrial Wastewater O&M Services Market Size Outlook to 2034

6.3.1. By Service Type

6.3.2. By Treatment Technology

6.3.3. By Country (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

6.4. South America Industrial Wastewater O&M Services Market Size Outlook to 2034

6.4.1. By Service Type

6.4.2. By Treatment Technology

6.4.3. By Country (Brazil, Argentina, Rest of South America)

6.5. Middle East and Africa Industrial Wastewater O&M Services Market Size Outlook to 2034

6.5.1. By Service Type

6.5.2. By Treatment Technology

6.5.3. By Country (Saudi Arabia, UAE, South Africa, Egypt, Rest of MEA)

7. Company Profiles: Leading Players

7.1. Veolia Environnement S.A.

7.1.1. Company Overview

7.1.2. Sustainable and Digitally Optimized Solutions

7.2. SUEZ S.A.

7.2.1. Company Overview

7.2.2. Automated Industrial Wastewater Management

7.3. Jacobs Engineering Group Inc.

7.4. VA Tech Wabag Ltd.

7.5. Evoqua Water Technologies (A Xylem Brand)

7.6. Other Key Players

7.6.1. Xylem Inc.

7.6.2. Aquatech International

7.6.3. DuPont de Nemours, Inc.

7.6.4. Alfa Laval

7.6.5. Kubota Corporation

7.6.6. Kurita Water Industries Ltd.

8. Methodology

8.1. Research Scope

8.2. Market Research Approach

8.3. Data Sources and Validation

8.4. Assumptions and Limitations

9. Appendix

9.1. Acronyms and Abbreviations

9.2. List of Tables

9.3. List of Figures