Industrial Wipes Market to Reach $9.5 Billion by 2034 at 4.8% CAGR Driven by Sustainable Nonwovens, IoT-Enabled Hygiene Systems, and High-Performance Substrates

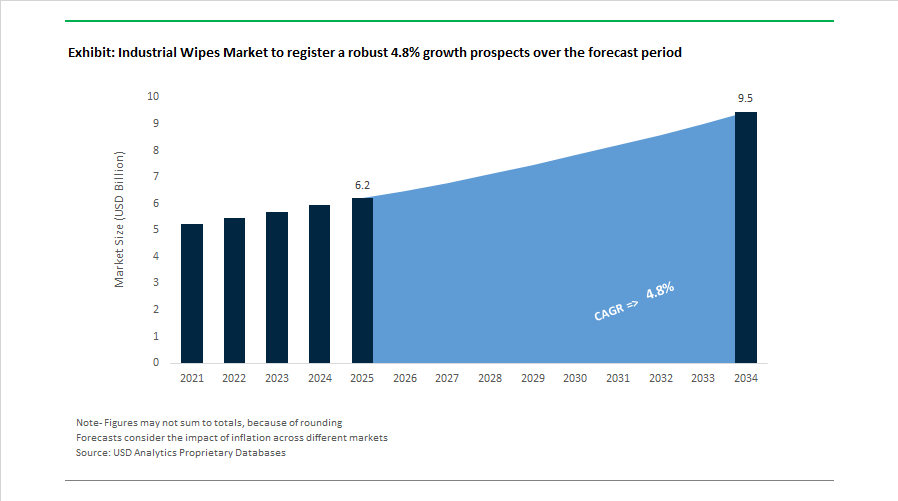

The Industrial Wipes Market is projected to expand from $6.2 billion in 2025 to $9.5 billion by 2034, registering a CAGR of 4.8%. Growth is being shaped by structural shifts toward sustainable nonwoven materials, performance-engineered substrates for heavy manufacturing, and the integration of digital hygiene management systems across industrial and institutional environments. Between 2024 and 2026, major manufacturers accelerated investments in recyclable fibers, reduced-carbon wipe production, hydroentangled fabric innovation, and data-driven facility cleaning solutions. Regulatory pressure in Europe and the United Kingdom regarding plastic-free mandates and deforestation compliance is also influencing manufacturing strategies and capital allocation.

In early 2024, Sontara introduced TriFlo™ Multipurpose Wipes, utilizing a proprietary hydroentangling process to deliver high thickness and extremely low lint performance for cleanroom and pharmaceutical maintenance. During the same year, ITW Pro Brands expanded its SCRUBS® Hand & Tool Wipes portfolio with dual-textured industrial solutions capable of degreasing machinery and cleaning skin simultaneously, reducing product complexity on factory floors. In 2024, Essity reported that more than 1.2 billion people passed through facilities using Tork® Vision Cleaning technology, an IoT-based system that reduced unnecessary dispenser checks by 91% and optimized wipe consumption through real-time monitoring. In August 2024, Kimberly-Clark announced the closure of its Flint, UK manufacturing sites, citing challenges in retrofitting legacy operations to comply with plastic-free wet wipe regulations, underscoring the capital intensity of sustainability transitions. By early 2025, Berry Global completed a $70 million expansion of its Benson, North Carolina nonwoven facility, installing high-speed proprietary technology to boost output of disinfectant and industrial cleaning substrates serving automotive and healthcare sectors.

Sustainability and portfolio consolidation intensified through 2025. In April 2025, Milliken launched the N/XT Life™ circular textile initiative, introducing closed-loop concepts for industrial wipes and protective fabrics that convert end-of-life garments and wipers into reusable raw materials for automotive and construction applications. In April 2025, Berry Global announced a strategic merger with Amcor plc, creating a large-scale sustainable materials platform that strengthens Berry’s access to recycled polymer supply chains for industrial wipe substrates. In September 2025, Kimberly-Clark Professional upgraded its WypAll® X70 and X80 cloths with performance-engineered construction that improved oil and water absorbency by up to 20%, alongside a nearly 10% larger sheet format for high-intensity industrial environments. In October 2025, Chicopee® and Sontara® unified operations under the Magnera identity, consolidating hydroentangled nonwoven expertise with foodservice and industrial cleaning capabilities into a single technical platform. On November 17, 2025, Sontara launched a reduced-carbon wipe portfolio manufactured in Spain using recycled PET, wood pulp, and lyocell fibers, achieving up to 42% lower CO2 emissions while aligning with the EU Deforestation Regulation.

Strategic reorganization and material innovation continued into 2026. Effective January 1, 2026, Essity reorganized its operations to establish Professional Hygiene as a standalone core business area, centering growth around sustainable wiping systems and data-driven cleaning analytics under the Tork® brand. Following the November 2025 introduction of Tyvek® APX™, DuPont extended this high-durability, breathable substrate into specialized industrial wiping formats by early 2026, targeting cleanroom and controlled environments where lint-free and chemically stable materials are mandatory. These developments demonstrate that the industrial wipes sector is transitioning from commodity wiping cloths toward engineered, sustainable, and digitally integrated cleaning systems designed for high-compliance manufacturing, healthcare, automotive, and semiconductor facilities.

Industrial Wipes Market Trends and Opportunities

Mandatory Transition to ISO 14644–Aligned Cleanroom Wipes

The Industrial Wipes Market is undergoing a non-discretionary upgrade cycle driven by the 2025 revisions to ISO 14644, which have materially tightened cleanroom contamination control and documentation requirements across semiconductor and pharmaceutical manufacturing. Cleanroom wipes are no longer treated as low-risk consumables; instead, they are being elevated to “process-critical inputs” with traceability, batch validation, and extractables control becoming mandatory for ISO Class 1–5 environments.

The 2025 ISO updates introduce stronger emphasis on continuous environmental trend monitoring rather than periodic compliance snapshots. As a result, wipes used in controlled environments must now demonstrate certified ultra-low extractables, with sodium and potassium ion levels below 0.5 ppm, to avoid triggering audit flags during frequent requalification cycles. Legacy non-woven wipes, which were historically acceptable, are increasingly failing these validation checks, accelerating replacement demand for laser-sealed edge polyester and microfiber wipes with documented low NVR profiles.

This shift is particularly acute in advanced semiconductor manufacturing. In sub-2 nm fabrication, even trace ionic or organic residues introduced during cleaning can cause pattern collapse and yield loss. By mid-2025, leading fabs began mandating a Certificate of Analysis for every wipe batch, aligning wipe procurement protocols with those used for photoresists and process chemicals. This represents a structural change in procurement behavior, increasing switching costs and favoring suppliers with strong QA systems and contamination analytics capabilities.

In pharmaceutical aseptic processing, the regulatory impact is equally pronounced. Under updated FDA cGMP expectations and EU GMP Annex 1, cleaning validation must now explicitly demonstrate that wipes do not introduce secondary contamination. This has driven accelerated adoption of sterile, gamma-irradiated wipes for Grade A and Grade B cleanrooms, where airborne particle concentrations are capped at 3,520 particles ≥0.5 µm per cubic meter. For decision makers, this trend directly translates into higher per-unit wipe costs but materially lower compliance risk and audit exposure.

Corporate ESG Mandates Driving Launderable-as-a-Service Adoption

A second structural trend in the Industrial Wipes Market is the rapid migration away from disposable shop towels toward launderable industrial wipe systems delivered under service contracts. This transition is being driven less by cost minimization and more by ESG compliance, waste reduction targets, and hazardous waste liability management.

Updated lifecycle assessments released in 2025 show that reusable industrial towels require 62% less primary energy demand and 81% less crude oil than single-use non-wovens over their usable life. More importantly for sustainability reporting, reusable systems generate 69% less total solid waste, making them a high-impact lever for manufacturers reporting against Scope 3 emissions and landfill diversion KPIs.

Safety and contamination concerns, which historically limited adoption, are being addressed through standardized laundering protocols. A late-2025 independent study published by the Textile Rental Services Association confirmed that EPA-regulated industrial laundering removes 99.9% of metal particulates, oils, and residues, allowing reusable wipes to meet or exceed the safety benchmarks of disposable alternatives. This validation has removed a major barrier for automotive, aerospace, and heavy manufacturing sites.

Commercially, the market is shifting toward a rental and service-based model. In 2025, leading providers reported that “Wipe-as-a-Service” contracts grew by more than 15% year-on-year. These contracts allow manufacturers to outsource hazardous saturated-waste handling, regulatory documentation, and disposal liabilities to certified providers, converting a compliance burden into a predictable operating expense. For procurement and sustainability leaders, this model improves audit readiness while stabilizing total cost of ownership.

Pre-Saturated Wipes with USDA BioPreferred® Chemistries

Pre-saturated industrial wipes are evolving from simple solvent carriers into precision cleaning tools aligned with green chemistry and worker safety mandates. The June 2025 USDA BioPreferred® Program Streamlining Rule has accelerated certification timelines, significantly improving market access for bio-based cleaning formulations embedded in wipe substrates.

In March 2025, Renewable Lubricants introduced GreenStrip Bio, a USDA-certified bio-based degreaser designed for heavy equipment maintenance. This launch reflects a broader market shift toward soy- and corn-derived feedstocks formulated to meet Design for the Environment standards without sacrificing cleaning efficacy. These formulations are increasingly being embedded directly into wipes to ensure consistent dosing and reduce operator exposure to bulk chemicals.

Market validation is strong. Diversey reported that its SURE range, a 100% bio-based professional cleaning portfolio, recorded a 36% demand increase in 2025, making it the company’s fastest-growing cleaning brand. This performance demonstrates that buyers are willing to pay a premium for wipes that deliver regulatory alignment, Ecolabel compliance, and reduced chemical handling risks.

Operationally, facilities using pre-saturated wipes have documented a 20% reduction in chemical waste by eliminating variability associated with manual pour-and-wipe practices. For decision makers, this translates into lower chemical spend leakage, improved safety metrics, and simplified chemical inventory management.

Specialized Sorbent Wipes for Battery and Hydrogen Infrastructure

The global expansion of lithium-ion battery gigafactories and green hydrogen infrastructure is creating a new, high-margin application segment within the Industrial Wipes Market. These environments involve novel hazard profiles that conventional wipes are not engineered to manage.

Battery electrolyte spills require not only absorption but chemical neutralization. In 2025, suppliers such as BHS Industrial Equipment and GECI expanded their battery spill kit offerings to include specialized polypropylene sorbent wipes capable of immobilizing and neutralizing acidic lithium-ion electrolytes. These solutions prevent toxic off-gassing and reduce secondary fire and exposure risks, addressing a critical safety gap in battery manufacturing and maintenance facilities.

Material compatibility is a key differentiator. Standard wipes often degrade or react when exposed to battery manufacturing chemicals such as NMP or HF-derived compounds. This has opened a premium niche for chemically inert, non-conductive wipe substrates that can be safely used around energized battery modules without increasing short-circuit risk.

Hydrogen infrastructure introduces a different challenge. Maintenance wipes used around liquefaction and storage systems must retain flexibility and absorbency at cryogenic temperatures. As green hydrogen projects scale, demand is emerging for advanced synthetic non-woven blends that do not embrittle or lose performance in extreme cold. This represents a strategic innovation frontier with limited qualified suppliers and strong long-term demand visibility.

Industrial Wipes Market Share and Segmentation Insights

Spunlace Technology Leads Industrial Wipes Production Through Binder-Free Hydroentanglement Performance

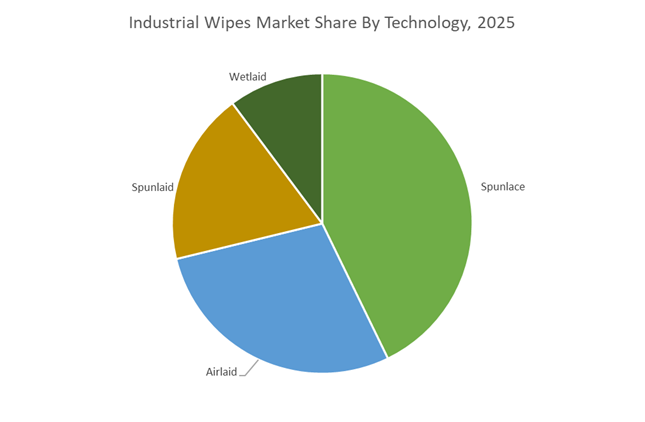

Spunlace technology accounted for 42.80% of the Industrial Wipes Market share in 2025, making it the most widely used manufacturing process for high-performance industrial wipes. Spunlace wipes are produced through hydroentanglement technology, where high-pressure water jets mechanically bond fibers to create a strong, absorbent, and lint-free nonwoven material without the use of chemical binders. This manufacturing approach delivers wipes with excellent tensile strength, superior absorbency, and low lint generation, making them suitable for demanding industrial cleaning applications such as precision equipment maintenance, food processing sanitation, and cleanroom surface preparation. Because spunlace materials rely on mechanical bonding rather than chemical additives, they offer significant advantages in environments where contamination control and chemical extractables must be minimized. In 2025, the binder-free production process has gained additional importance as sustainability and regulatory pressures encourage the use of recyclable, compostable, and low-residue industrial cleaning materials, positioning spunlace technology as the preferred platform for next-generation industrial wipes manufacturing.

Manufacturing and Metalworking Sector Drives the Largest Demand for Industrial Wipes

Manufacturing and Metalworking represented 42.80% of the Industrial Wipes Market share in 2025, establishing the sector as the largest consumer of industrial wiping products. Industrial production environments generate continuous cleaning requirements as machinery, tools, and components accumulate machining oils, metalworking fluids, lubricants, adhesives, and production residues that must be removed to maintain equipment reliability and product quality. Industrial wipes are therefore widely used in machine maintenance, surface preparation, assembly line cleaning, and operator workstation sanitation, creating steady demand across manufacturing facilities and metal fabrication operations. The sector’s diverse applications span machining shops, automotive component manufacturing, heavy equipment fabrication, and electronics assembly, all of which require reliable wiping materials for operational cleanliness and workplace safety. In 2025, industrial distributors increasingly provide managed wiping programs often referred to as wipes-as-a-service, where companies receive color-coded wipes designed for specific cleaning tasks along with dispensing systems, usage monitoring, and automated replenishment services. These programs improve inventory management, reduce overall wipe consumption, and ensure consistent cleaning performance across industrial operations.

Competitive Landscape in Industrial Wipes Market

Kimberly-Clark Professional Leads with Advanced Absorbency and Lifecycle Programs

Kimberly-Clark Professional sets the global benchmark in heavy-duty industrial wipes and precision cleaning cloths through its proprietary HYDROKNIT technology, which enhances strength, durability, and liquid absorption. In September 2025, the company upgraded its WypAll X70 and X80 wipes with a 10% larger sheet size and 20% higher oil and water absorbency, reinforcing its leadership in industrial degreasing and maintenance cleaning applications. The WypAll portfolio is structured into PowerClean, CriticalClean, and GeneralClean categories to streamline procurement across automotive, manufacturing, and cleanroom environments. Its 2026 Thrive Sustainability Services program enables industrial facilities to track wipe lifecycle performance and divert used nonwoven materials from landfills via circular recycling partnerships. The ICON Dispenser Collection, offering high-resolution designer faceplates, has gained traction in modern industrial facilities that integrate hygiene, compliance, and aesthetic workplace standards.

Essity Accelerates Professional Hygiene Growth Through Tork Innovation

Essity has strengthened its position in the industrial wipes and professional hygiene market by reorganizing its global business structure in January 2026, establishing Professional Hygiene as one of four dedicated strategic pillars. Under the Tork brand, Essity markets the Tork Performance industrial cloth range, including solvent-resistant wipes certified for food contact and engineered to withstand aggressive chemical cleaning agents without fiber breakdown. In February 2026, the company received three Product of the Year awards for circular hygiene solutions, including carbon-neutral dispensers and recycled fiber wiping products, reinforcing its sustainability leadership in industrial cleaning consumables. Essity is advancing Digital Hygiene Management through its Tork Vision Cleaning platform, which uses real-time usage analytics to maintain optimal stock levels in high-traffic manufacturing and logistics zones. This data-driven approach enhances operational efficiency and reduces downtime in industrial wiping stations.

Berry Global and Magnera Advance Recycled and Plastic-Free Wipe Solutions

Berry Global has consolidated its professional wiping brands under the Magnera identity, strengthening its competitive footprint in industrial nonwoven wipes. At the Manchester Cleaning Show 2026, the company introduced a unified strategy presenting Chicopee and Sontara under a single global platform in the United Kingdom. The 2026 launch of the rMicrofibre wipe marks a significant sustainability milestone as the first disposable wipe manufactured from 100% recycled material, delivering a 50% reduction in carbon footprint compared to conventional alternatives. Berry Global has integrated its U.S. and European manufacturing operations to ensure local-for-local supply reliability, particularly for healthcare and aerospace clients that demand validated contamination control and traceability. Its Plastic-Free Transition initiative is shifting Sontara industrial wipes toward natural wood pulp, lyocell, and cotton fibers to eliminate microplastic shedding during industrial degreasing and solvent wiping operations.

ITW Pro Brands Specializes in High-Potency Pre-Moistened Industrial Wipes

ITW Pro Brands differentiates itself through pre-moistened industrial wipes under the SCRUBS brand, combining mechanical abrasion and high-performance chemical formulations to eliminate the need for secondary spray systems. In late 2025 and early 2026, the company transitioned its entire SCRUBS IN-A-BUCKET product line to 100% recycled plastic packaging, reinforcing its sustainability credentials in the MRO consumables segment. The flagship SCRUBS blue wipes feature a dual-texture design with an abrasive side for removing embedded grease, oil, and tar, and a smooth side for safe hand cleaning without water. A new high-capacity refill pack for its 72-count bucket reduces plastic waste by 90% compared to purchasing new canisters, targeting cost-efficient maintenance operations. In 2026, ITW Pro Brands expanded its flood clean-up solutions portfolio, positioning its industrial-strength wipes as rapid-response tools for equipment restoration following severe weather events.

Contec Strengthens Cleanroom Compliance and Custom Contamination Control

Contec is a specialist in contamination control wipes for cleanrooms, biotechnology, aerospace, and pharmaceutical manufacturing environments. In 2026, the company intensified its focus on Annex 1 compliance, assisting pharmaceutical manufacturers in meeting updated EU regulatory standards for sterile medicinal production through structured Contamination Control Strategies. Contec recently introduced recycled plastic knitted polyester wipes that maintain ISO Class 3 to 8 cleanroom validation standards while diverting plastic waste from landfills. Its Ignite Innovation platform enables industrial clients to submit contamination challenges for the development of custom-engineered wiping solutions tailored to specific chemical, particulate, or microbial risks. Holding a Bronze Sustainability Rating from EcoVadis as of early 2026, Contec demonstrates transparency in CSR reporting while reinforcing its leadership in high-purity, low-particulate industrial wiping systems.

United States Industrial Wipes Market: Reshoring, Digital Operations, and Green Chemistry Adoption

The United States industrial wipes industry is entering a structurally defensive growth phase characterized by reshoring, digital supply chain control, and sustainability-led formulation shifts. In January 2026, Berry Global finalized a $70 million expansion at its Benson, North Carolina facility, reinforcing domestic production of disinfecting wipes and high-performance nonwoven substrates. The project directly supports demand from critical environments such as healthcare, laboratories, and industrial manufacturing while adding specialized technical roles to strengthen U.S.-based nonwoven expertise. This reshoring trend reflects heightened risk sensitivity following pandemic-era disruptions and rising scrutiny of imported hygiene products in regulated environments.

Operational digitalization is advancing in parallel. In November 2025, The Clorox Company disclosed a strategic inventory build ahead of a major ERP transition within its U.S. professional division, designed to safeguard continuity of CloroxPro disinfecting wipes through 2026. At the same time, circularity and performance upgrades are redefining value propositions. Kimberly-Clark Professional launched its ReNew Programme to integrate smart restroom systems with end-to-end recovery of used wipes and towels, targeting full customer transition by January 2026. Product innovation is reinforcing these shifts. CloroxPro introduced EcoClean Disinfecting Wipes in late 2025 using a plant-based, EPA-approved formulation aligned with green chemistry principles, while Kimberly-Clark upgraded its WypAll X70 and X80 ranges with enhanced hydro-knit absorbency for metalworking and heavy manufacturing. Public-sector demand remains a stabilizing force, with renewed back-to-school disinfection guidance in August 2025 explicitly endorsing EPA-registered industrial wipes to reduce absenteeism across educational facilities.

United Kingdom and European Union Industrial Wipes Market: Plastic Elimination and Circular Processing Mandates

The UK and EU industrial wipes market is undergoing a regulatory reset anchored in plastic elimination, biodegradable substrates, and circular processing infrastructure. From April 2026, statutory bans confirmed by the UK and Welsh governments will prohibit the sale of wet wipes containing plastic, compelling a full transition to biodegradable fibers such as viscose and lyocell across industrial and professional applications. This policy is reshaping raw material sourcing, substrate engineering, and supplier qualification for wipes used in manufacturing, hospitality, and institutional hygiene.

Compliance carries both cost and opportunity. A UK impact assessment released in September 2025 estimated net profit impacts of approximately £209 million for producers due to higher input costs, while simultaneously projecting £61 million in greenhouse gas savings by 2026 from lower-emission production pathways. Infrastructure investment is responding accordingly. Kimberly-Clark designated its Koblenz mill in Germany as the primary European processing hub for the ReNew Programme, with a roadmap to reach 100% renewable energy by 2029, supporting carbon-neutral industrial wipes for Europe’s manufacturing belt. Innovation at the formulation level is also accelerating. UK-based Guardpack announced the development of multifunctional antiviral and hypoallergenic industrial wipes in late 2025, targeting hospitality and travel sectors adapting to post-pandemic hygiene expectations.

India Industrial Wipes Market: Regulatory Alignment, High-Purity Applications, and Export-Oriented Manufacturing

India’s industrial wipes industry is transitioning from cost-driven manufacturing toward regulatory alignment and application-specific specialization. During 2025–2026, updates from the Bureau of Indian Standards are accelerating the shift toward plastic-free and chemical-minimized wipes, favoring bamboo fiber and organic cotton substrates. These changes are elevating baseline quality requirements while opening export pathways to regions enforcing similar sustainability standards.

Technology upgrades are expanding application scope. In 2025, Ginni Filaments Ltd. advanced its industrial wipes portfolio by introducing ultra-pure water wipes produced using wetlaid technology, targeting sensitive electronics assembly and laboratory environments. Manufacturing scale is also increasing. Kimberly-Clark Hygiene Products Private Limited and Hindustan Unilever expanded domestic output under Make in India initiatives, with a clear export pivot toward Southeast Asian and Middle Eastern markets by 2026. This combination of standards harmonization and capacity expansion is positioning India as a regional supply base for compliant industrial wipes.

Brazil Industrial Wipes Market: Cellulosic Feedstock Advantage and Cost-Stable Sustainability

Brazil’s industrial wipes industry benefits from structural access to sustainable cellulose feedstocks, underpinning competitive biodegradable wipe production. With national pulp and paper capacity reaching approximately 23.85 million tons in recent cycles, domestic wipe manufacturers are leveraging abundant, low-cost cellulose fibers to secure supply stability for industrial and institutional wiping products. This feedstock advantage supports consistent quality while insulating producers from volatility in imported nonwoven raw materials.

The integration of pulp infrastructure with wipe converting operations is strengthening Brazil’s position in biodegradable industrial wipes for manufacturing, food processing, and maintenance applications. As global buyers increasingly prioritize plastic-free and renewable substrates, Brazil’s vertically aligned pulp-to-wipe ecosystem is emerging as a strategic sourcing option for sustainability-focused procurement programs.

Industrial Wipes Industry: Country-Level Strategic Snapshot

Industrial Wipes Market County Level Snapshot

|

Region

|

Primary Strategic Driver

|

Key Industry Shift

|

Structural Outcome

|

|

United States

|

Reshoring and green chemistry

|

Domestic capacity expansion, plant-based disinfecting wipes

|

Supply security with sustainability premium

|

|

United Kingdom & EU

|

Statutory plastic bans

|

Biodegradable substrates, circular processing hubs

|

Compliance-led reformulation and cost realignment

|

|

India

|

Standards harmonization and specialization

|

Plastic-free substrates, ultra-pure water wipes

|

Export-ready, application-specific growth

|

|

Brazil

|

Cellulose feedstock strength

|

Biodegradable industrial wipes

|

Cost-stable, renewable material advantage

|

Industrial Wipes Market Report Scope

Industrial Wipes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.2 Billion

|

|

Market Size (2034)

|

$9.5 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Technology (Spunlace, Airlaid, Wetlaid, Spunlaid), By Material Type (Synthetic Fibers, Natural Fibers, Semi-Synthetic Fibers, Blended Fabrics), By Product Type (Dry Wipes, Wet Wipes), By Application Category (Equipment Maintenance, Controlled Environments, Surface Preparation, Food Service and Hygiene, Healthcare and Medical), By End-Use Industry (Manufacturing and Metalworking, Automotive and Transportation, Aerospace and Defense, Electronics and Semiconductors, Food and Beverage Processing, Healthcare and Life Sciences)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kimberly-Clark Corporation, Berry Global Group, Inc., Essity AB, The Clorox Company, Rockline Industries, Nice-Pak Products, Inc., S.C. Johnson & Son, Inc., DuPont de Nemours, Inc., Freudenberg Group, Ahlstrom-Munksjö, Ginni Filaments Ltd., Contec, Inc., Tork, Kruger Inc., Hengan Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Industrial Wipes Market Segmentation

By Technology

- Spunlace

- Airlaid

- Wetlaid

- Spunlaid

By Material Type

- Synthetic Fibers

- Natural Fibers

- Semi-Synthetic Fibers

- Blended Fabrics

By Product Type

By Application Category

- Equipment Maintenance

- Controlled Environments

- Surface Preparation

- Food Service and Hygiene

- Healthcare and Medical

By End-Use Industry

- Manufacturing and Metalworking

- Automotive and Transportation

- Aerospace and Defense

- Electronics and Semiconductors

- Food and Beverage Processing

- Healthcare and Life Sciences

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Industrial Wipes Industry

- Kimberly-Clark Corporation

- Berry Global Group, Inc.

- Essity AB

- The Clorox Company

- Rockline Industries

- Nice-Pak Products, Inc.

- S.C. Johnson & Son, Inc.

- DuPont de Nemours, Inc.

- Freudenberg Group

- Ahlstrom-Munksjö

- Ginni Filaments Ltd.

- Contec, Inc.

- Tork

- Kruger Inc.

- Hengan Group

*- List not Exhaustive