Integrated Kitchen Appliances Market Overview: Growth Outlook and Strategic Insights

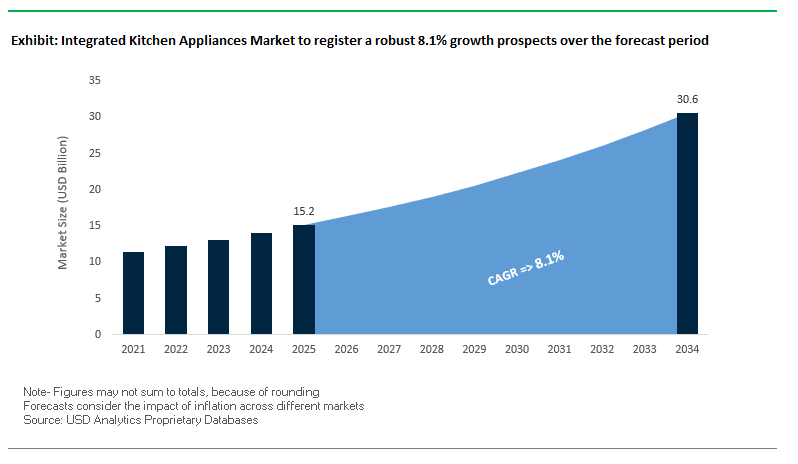

The global integrated kitchen appliances market is forecasted to grow from USD 15.2 billion in 2025 to USD 30.6 billion in 2034, at a CAGR of 8.1%. The industry is at the forefront of the evolution of modern kitchens, with customers demanding seamless design, high-end connectivity, and environmentally friendly performance. Integrated appliances concealed behind cabinetry are increasingly becoming the go-to choice among homeowners, developers, and corporate kitchen designers for their ability to deliver functionality without compromising design. The industry increases with the trend for smart home integration, green technology, and urban city living.

Key Insights for Industry Professionals

- Minimalist Design Demand – Integrated appliances are central to sleek, modern kitchen aesthetics.

- Smart Home Convergence – AI-powered, app-connected appliances are reshaping user experience.

- Sustainability Priority – Government regulations and consumer expectations are driving A+++ rated solutions.

- Urbanization Influence – Space-efficient solutions are increasingly critical in high-density cities.

- Premiumization Trend – Brands are targeting affluent consumers with luxury finishes and customization.

Integrated Kitchen Appliances Market Analysis: Technological Convergence and Regional Expansion Driving Competitive Shifts

The integrated kitchen appliances market saw solid momentum between August 2024 and August 2025, with leading players investing in intelligent technology, domestic manufacturing, and green design. Bosch Home Appliances' June 2025 statement of a huge investment in India, including a locally produced refrigerator factory, underscores the importance of developing markets in global strategy. Liebherr's August 2025 launch of the first integrated refrigerators outside Europe produced in India is a strategic diversification of its manufacturing base.

IFA events have served as a launching pad for innovation: Miele introduced high-performance extractor hoods and AI-enabled refrigerators in July 2025, and LG Electronics introduced Europe's launch of its premium built-in package in August 2024. Samsung introduced its global launch of its Bespoke kitchen package in November 2024, introducing its move to own the premium modular design space. In addition to launches, brands are taking advantage of design-led marketing, such as in May 2025 when Smeg marketed its Italy-designed appliances during New York Design Week, emphasizing the convergence of luxury and lifestyle.

Sustainability continues to be a determining market driver. Miele's dominance in energy-efficient dishwashers, Liebherr's Gold EcoVadis certification for sustainability, and Bosch/Siemens' constant R&D in efficiency technology are testimonials that energy performance is now no longer a differentiator but a sector norm. Urban living trends also come into play, with integrated compact solutions becoming a necessity in Asian-Pacific and European metropolitan complexes.

Emerging Trends and High-Value Opportunities in the Integrated Kitchen Appliances Market

Unified Smart Kitchen Operating Systems Driving Next-Level Automation

The integrated kitchen appliance market is moving from discrete smart appliances to centralized, AI-driven operating systems powering the entire kitchen system. These systems allow appliances to communicate with and collaborate with one another, facilitating seamless cooking sessions, smart energy management, and improved food stock management. For example, a smart refrigerator can recommend recipes based on ingredients and command the oven to preheat automatically. The shift to these systems aligns with consumers' desire for personalized, efficient, and sustainable living, and also presents manufacturers with the potential for building interoperable appliances that trap consumers in their brand ecosystem. In premium segments, the smart refrigerator is emerging as the command center of the connected home, with voice assistants, large touch screens, and IoT connectivity to control kitchen as well as household functions.

Retractable Induction + Steam Hybrid Cooktops Redefining Space Optimization

As urban areas expand and kitchen areas shrink, retractable hybrid cooktops are one of the leading innovations in space-saving home design. By combining energy-efficient induction technology with health-oriented steam cooking, the appliances offer flexibility with less countertop space. The retractable element allows the cooktop to fold in when not in use, offering a clean, smooth surface that maximizes function and design. Induction offers precise temperature control and faster cooking, while steam facilitates nutrition retention and healthier cooking methods. With minimalist and modular kitchen designs gaining popularity, these hybrid solutions are poised to capture a larger portion of the premium appliance market, particularly in luxury condos and high-end residential communities.

Prosumer Sous Vide Integration for Professional-Grade Cooking at Home

The growth of the prosumer cooking category serious home cooks seeking professional outcomes is creating opportunities for integrated sous vide technology on high-end ovens, cooktops, and multifunction appliances. Integrating sous vide capability into built-in units enables manufacturers to discontinue the use of add-on immersion circulators, recouping lost counter space and streamlining the cooking process. Integration is attractive to health-conscious culinary trends, as sous vide preserves nutrients and optimizes flavor without excessive oil. Smart connectivity enables remote monitoring and automated precision, making the process convenient for mainstream consumers. Since the global market for sous vide is growing at a fast pace, appliance brands that leverage this integration can enhance their position in the high-end residential market.

Appliance-as-a-Service Leasing Models for Commercial Kitchens

In the commercial foodservice industry, the Appliance-as-a-Service (AaaS) business model is revolutionizing the way restaurants, cloud kitchens, and catering companies obtain integrated kitchen technology. Instead of committing large amounts of money upfront, companies can rent appliances on a pay-per-use or subscription plan, obtaining the most up-to-date energy-efficient and smart-enabled equipment. This lowers capital barriers for small players, facilitates quick scalability for cloud kitchens, and offers frequent upgrades to technology without the related costs and inconvenience of ownership. Maintenance and service are often part of the leasing agreement, lowering downtime and operational risk. As the foodservice industry becomes more agile and technology-driven, AaaS models will play an important role in the deployment of sophisticated integrated kitchen solutions.

Integrated Kitchen Appliances Market Share and Segmentation Insights

Market Share by Product Type: Cooking Appliances Lead with Smart Feature Integration

Built-in kitchen appliances are led by cooking appliances at 35%, driven by consumers' need for built-in ovens, induction, and multi-function units with smart capabilities. These appliances are increasingly equipped with Wi-Fi connectivity, cooking cycles, and precision sensors, allowing users to create professional-level results with ease. The 30% of the market for the refrigerator and freezers is evolving with modular interior design, convertible space, and AI-based inventory management, contributing to them becoming a standard in today's kitchens. Dishwashers are becoming popular with quiet-operation technology and adaptability of drawer configurations, while small built-in appliances like built-in coffee systems and steam ovens are turning into luxury upgrades for upscale kitchen remodels.

.png)

Market Share by Structure: Built-In Appliances Dominate Premium Kitchen Remodeling

Built-ins capture 60% market share, indicating strong demand for clean lines and space savings in upscale urban and residential kitchen design. Their compatibility with cabinetry aligns with open-plan and minimalist design, and they are the go-to choice among architects and interior designers. Freestanding appliances remain relevant in retrofit and budget-based projects, but hybrid designs such as slide-in ranges and flush-fit dishwashers are bridging the gap, offering the high-end look of built-ins with installation ease. With home remodeling expenses on the increase and consumers looking for design harmony as well as functionality, built-in appliances will keep their market-leading share, particularly in luxury and mid-to-high-end projects.

Competitive Landscape – Leading Players in Integrated Kitchen Appliances Market

The integrated kitchen appliances market is characterized by global conglomerates and luxury niche brands that compete through technological leadership, premium design, and localized strategies. Key players included are Whirlpool Corporation, LG Electronics Inc., BSH Hausgeräte GmbH, Electrolux AB, Haier Group Corporation, Samsung Electronics Co., Ltd., Midea Group Co., Ltd., Miele & Cie. KG, Panasonic Holdings Corporation, Smeg S.p.A., Gorenje Group, GE Appliances, Sub-Zero Group, Inc., Arcelik A.S., Viking Range, LLC, Others.

BSH Hausgeräte GmbH (Bosch/Siemens) – German Engineering Meets Smart Connectivity

BSH provides Bosch and Siemens ovens, dish washers, refrigerators, and hobs, supported by its Home Connect smart ecosystem. Praise for German engineering technology, BSH emphasizes ruggedness, energy efficiency, and artificial intelligence integration. In June 2025, Bosch's investment in India reflected its focus on emerging markets. The company is also driving experiential retail to increase customer interaction.

Miele & Cie. KG – High-Performance with an Environmental Perspective

Miele is a world standard in high-spec integrated appliances, with durable pyrolytic ovens, induction hobs, and dishwashers. Renowned for 20-year-tested appliances, Miele is the sustainability leader, with its dishwashers leading EU efficiency charts in 2024. At IFA 2025, it launched refrigerators with built-in cameras for remote stock checks, finding the right balance between technology and waste reduction.

Samsung Home Appliances – AI-Powered Bespoke Models that Tailor To Your Taste

Samsung's Bespoke line has modular, customizable integrated appliances tied to its SmartThings platform. Drawing on its consumer electronics heritage, Samsung drives AI-enabled functionality for a personalized kitchen experience. Its worldwide November 2024 Bespoke package launch carried its premium presence to several continents once more, demonstrating its market reach.

Liebherr Appliances – Refrigeration Specialist with Global Manufacturing Growth

Liebherr dominates the refrigeration industry through technologies like BioFresh and DuoCooling. Its expertise in energy-efficient preservation is now complemented with global expansion August 2025 announced its first integrated refrigerators manufactured outside of Europe. Its Variable Capacity Compressors offer low energy consumption and exceptional performance, complementing domestic and commercial use.

Smeg S.p.A. – Italian Design Heritage in Contemporary Integration

Smeg blends retro-chic with state-of-the-art appliance design, and fashion-forward consumers adore it. With a reputation for high-end finishes and collaborations with designers, it showcased craftsmanship at New York Design Week 2025, making the brand a lifestyle statement. Smeg's focus on trend-setting color and luxury personalization positions it squarely in the luxury kitchen space.

Germany: Engineering Excellence and Sustainable Innovation

Germany stands out in the integrated kitchen appliances market as a leader in precision engineering and cutting-edge technology integration. Brands such as Bosch and Siemens, under BSH Hausgeräte GmbH, have pioneered IoT-enabled built-in appliances that connect seamlessly to smart home ecosystems, allowing users to control cooking, refrigeration, and cleaning devices remotely through smartphone applications. This technological leadership is reinforced by an emphasis on design aesthetics German appliances are globally recognized for their minimalist, high-quality finishes that complement modern kitchen layouts. Export strength is another defining factor, with Germany serving as a major hub for both kitchen furniture and high-end appliance exports, influencing design trends worldwide.

Sustainability is deeply embedded in the German market’s DNA, aligning with the government’s push for green technologies. The country’s stringent EU Energy Label requirements drive manufacturers to innovate with energy-efficient ovens, dishwashers, and refrigerators. Notable advancements include ovens with integrated sensors for precision cooking and dishwashers with advanced water-saving features, appealing to both eco-conscious consumers and cost-sensitive buyers. This combination of engineering expertise, sustainability, and global market influence positions Germany as a powerhouse in shaping future kitchen appliance trends.

United States: Smart Kitchen Adoption and Premiumization

The United States is a major growth engine for the integrated kitchen appliances sector, propelled by rising demand for smart, IoT-enabled devices. Consumers are embracing appliances with features such as voice-activated ovens, inventory-tracking refrigerators, and AI-driven cooking assistants. Government-backed incentives, including appliance rebates and energy-efficiency tax credits, are further encouraging adoption, while DOE programs targeting electrification in tribal and low-income communities expand the addressable market.

The premiumization trend is particularly strong, driven by home renovation booms and the growing popularity of luxury cooking experiences. Market leaders such as Whirlpool and GE Appliances are integrating advanced technologies like SlimTech vacuum insulation for refrigerators to save space while improving energy performance. Personalized user interfaces powered by AI and machine learning add further value. With incentives for sustainable upgrades and an appetite for high-end features, the U.S. market continues to push the boundaries of smart, energy-efficient kitchen living.

China: Manufacturing Powerhouse and Smart Technology Leadership

China plays a pivotal role as one of the largest manufacturing hubs for integrated kitchen appliances, supported by favorable government policies and a robust supply chain that attracts global brands. Rapid urbanization, coupled with rising disposable incomes, is accelerating the shift from traditional kitchens to modular, space-optimized designs. Middle-class consumers are increasingly drawn to high-tech solutions, driving demand for Wi-Fi and Bluetooth-enabled appliances.

Domestic giants like Haier Group and Midea Group are leading innovation, integrating AI-powered diagnostics, smart cooking algorithms, and energy-optimized operation modes. The government’s “green consumption” initiatives are encouraging consumers to replace outdated models with energy-efficient alternatives, supported by attractive subsidies. E-commerce platforms such as JD.com and Tmall further shape buying behavior, offering extensive product comparisons, live-stream demonstrations, and direct-to-door delivery, making digital channels a dominant force in market expansion.

Japan: Energy Policy-Driven Efficiency and Health-Oriented Design

Japan’s Top Runner program has been instrumental in shaping the energy-efficiency standards for integrated kitchen appliances, prompting continuous product innovation. Manufacturers are competing to deliver high-performance models with reduced environmental impact, from induction cooktops to ultra-efficient refrigeration systems. IoT integration and sensor-based automation are becoming standard, enabling users to control appliances remotely and optimize performance.

A notable consumer trend in Japan is the growing health and wellness focus, fueling demand for steam ovens, air fryers, and other appliances that support healthy cooking methods. Government investment in residential infrastructure modernization is boosting appliance replacement rates, while high disposable incomes encourage the purchase of premium, design-led products. Japanese consumers value both technological sophistication and aesthetic harmony, ensuring that innovation and style remain intertwined in market offerings.

France: Sustainability-Led Demand and Design Sophistication

France’s integrated kitchen appliances market is evolving around sustainability, with EU Energy Label regulations compelling manufacturers to develop eco-friendly models like inverter refrigerators and low-energy dishwashers. Consumers are increasingly choosing appliances that align with environmental values without compromising on performance. This trend is supported by a cultural shift toward home cooking, driving demand for multifunctional appliances such as steam ovens and high-speed blenders.

Technological advancement is a clear growth driver, with smart home connectivity and voice-assisted control becoming popular in urban households. The French market also shows strong demand for premium, design-forward appliances that blend seamlessly with modern interiors, appealing to the country’s refined culinary and aesthetic sensibilities. This intersection of eco-consciousness, innovation, and design makes France a key market for luxury and sustainable integrated kitchen solutions.

United Kingdom: Renovation-Driven Growth and Smart Home Integration

The UK’s integrated kitchen appliances industry is benefiting from a surge in home renovation projects and new housing developments, particularly in the premium segment. The increasing popularity of smart home ecosystems is reshaping consumer expectations, with appliances that connect to centralized home control systems gaining market traction. The UK government’s new smart appliance standards aim to reduce energy bills and increase grid flexibility, creating regulatory momentum for adoption.

Sustainability remains a major purchasing factor, with energy-efficient appliances now a priority for most homeowners. Brands like Whirlpool are launching advanced, low-energy refrigerators and dishwashers to meet these expectations. Additionally, the expansion of online retail channels has widened access to a diverse range of integrated kitchen appliance brands, enabling consumers to make informed choices through product reviews, comparisons, and direct shipping. This combination of renovation trends, sustainability focus, and digital retail presence positions the UK as one of Europe’s fastest-evolving markets for integrated kitchen solutions.

Integrated Kitchen Appliances Market Report Scope

Integrated Kitchen Appliances Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$15.2 Billion

|

|

Market Size (2034)

|

$30.6 Billion

|

|

Market Growth Rate

|

8.1%

|

|

Segments

|

By Product Type (Cooking Appliances (Cooktops, Ovens, Microwaves, Range Hoods, Hobs), Refrigerators & Freezers, Dishwashers, Small Kitchen Appliances (Coffee Makers, Blenders, Food Processors, Air Fryers)), By Application (Residential, Commercial (Restaurants, Hotels, Cafes, Institutional)), By Structure (Built-in Appliances, Freestanding Appliances), By Distribution Channel (Offline (Specialty Stores, Supermarkets & Hypermarkets), Online (E-commerce Platforms, Company-Owned Websites)), By Technology (Smart Appliances, Conventional Appliances), By Power Source (Electric, Gas)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Whirlpool Corporation, LG Electronics Inc., BSH Hausgeräte GmbH, Electrolux AB, Haier Group Corporation, Samsung Electronics Co., Ltd., Midea Group Co., Ltd., Miele & Cie. KG, Panasonic Holdings Corporation, Smeg S.p.A., Gorenje Group, GE Appliances, Sub-Zero Group, Inc., Arcelik A.S., Viking Range, LLC, Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Integrated Kitchen Appliances Market Segmentation

By Product

- Cooking Appliances

- Cooktops

- Ovens

- Microwaves

- Range Hoods

- Hobs

- Refrigerators & Freezers

- Dishwashers

- Small Kitchen Appliances

- Coffee Makers

- Blenders

- Food Processors

- Air Fryers

By Application

- Residential

- Commercial

- Restaurants

- Hotels

- Cafes

- Institutional

By Structure

- Built-in Appliances

- Freestanding Appliances

By Distribution Channel

- Offline

- Specialty Stores

- Supermarkets & Hypermarkets

- Online

- E-commerce Platforms

- Company-Owned Websites

By Technology

- Smart Appliances

- Conventional Appliances

By Power Source

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Integrated Kitchen Appliances Market

- Whirlpool Corporation

- LG Electronics Inc.

- BSH Hausgeräte GmbH

- Electrolux AB

- Haier Group Corporation

- Samsung Electronics Co. Ltd.

- Midea Group Co. Ltd.

- Miele & Cie. KG

- Panasonic Holdings Corporation

- Smeg S.p.A.

- Gorenje Group

- GE Appliances

- Sub-Zero Group Inc.

- Arcelik A.S.

- Viking Range LLC

* List Not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the global Integrated Kitchen Appliances Market through 2034, delivering analysis reviews of demand inflection points, channel shifts, and premium design adoption across residential and commercial kitchens. It highlights breakthroughs shaping the next wave of kitchen innovation—including unified smart-kitchen operating systems, retractable induction-steam hybrids, prosumer sous-vide integration, and appliance-as-a-service models—while benchmarking energy-efficiency momentum, urban space optimization, and brand strategies in key countries. With competitive intelligence on product roadmaps, pricing ladders, and ecosystem plays, this report is an essential resource for appliance OEMs, component suppliers, retailers, developers, and investors seeking data-driven decisions in a fast-evolving, design-led category. Scope includes-

- Segmentation

- By Product: Cooking Appliances; Refrigerators & Freezers; Dishwashers; Small Kitchen Appliances

- By Application: Residential; Commercial

- By Structure: Built-in Appliances; Freestanding Appliances

- By Distribution Channel: Offline; Online

- By Technology: Smart Appliances; Conventional Appliances

- By Power Source: Electric; Gas

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Time Frame: Historic data 2021–2024 and forecast data 2025–2034.

- Companies: Analysis/profiles of 15+ companies (e.g., Whirlpool, LG, BSH, Electrolux, Haier, Samsung, Midea, Miele, Panasonic, Smeg, Gorenje, GE Appliances, Sub-Zero, Arçelik, Viking Range, etc.).

Methodology

USDAnalytics applies a mixed-methods approach combining primary interviews (global OEMs, channel partners, builders, designers, and service providers) with secondary sources (regulatory databases, company filings, customs data, and trade publications). Market sizing blends bottom-up shipment models with top-down triangulation using install-base, renovation spend, housing starts, and online/offline sell-through. Forecasts leverage scenario analysis for price/mix, energy-label transitions, urban density, and smart-home penetration; technology diffusion curves capture adoption of unified OS, induction-steam hybrids, and AaaS leasing. All numbers are validated via cross-region consistency checks, sensitivity testing, and expert review to ensure decision-grade accuracy.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.