Interactive Teaching Software Market: AI Integration, Gamification, and Global EdTech Expansion

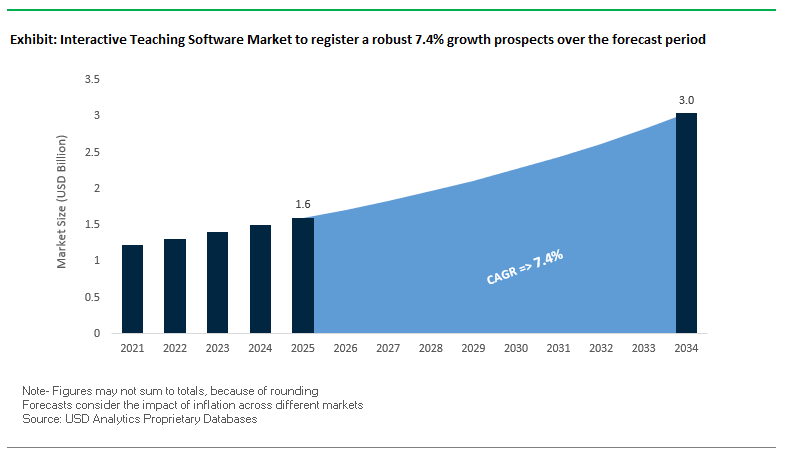

The global interactive tutoring software market is transforming from being an adjunct electronic device to being the focal point of contemporary education. The market is projected to expand from $1.6 billion in 2025 to $3.4 billion by 2034, achieving a CAGR of 7.4%. The driving force for this change is the need for more interactive, collaborative, and adaptive learning environments that are responsive to emergent pedagogies and 21st-century skill sets. The market is being influenced by developments in artificial intelligence, gamification tactics, and the accelerated rollout of digital infrastructure across the globe.

Interactive learning software is no longer an adjunct to the classroom but a catalyst of active learning designs, allowing teachers to create lessons that support engagement, creativity, and critical thinking. AI integration means personalized learning routes, instant feedback, and the capacity to free teachers from routine tasks to concentrate on higher-order pedagogy. Governments and private institutions are spending serious money on smart classrooms, providing equitable access to technology that can potentially equalize the playing field for learning across geographies.

Key Insights for Market Stakeholders:

- Pedagogical Shift: Over 80% of educators globally are using interactive tools, moving from passive delivery to active, student-centered learning.

- Infrastructure Support: UNESCO reports 65% of upper secondary schools now have internet access, with strong policy momentum to close the digital divide.

- AI Personalization: Adaptive AI systems are transforming how students learn, delivering tailored lessons that improve retention and outcomes.

- Gamification Impact: Leaderboards, points, and interactive quizzes are increasing student motivation and engagement across learning environments.

Market Analysis: Recent Developments Driving Interactive Teaching Software Adoption

The market for interactive teaching software saw a wave of technological advancements, global partnerships, and expansions that positioned it for explosive growth. In April 2025, Oak National Academy's AI lesson planner software "Aila" picked up momentum, being adopted by over 20,000 teachers, showing the demand for the creation of AI-based content for learning. In February 2025, Huawei released its Smart Classroom Service based on edge-cloud technology, enabling live streaming, smart attendance, and real-time speech-to-text capabilities that mark a new era of classrooms completely empowered by cloud analytics.

June 2025 was a milestone when Coursera saw a 1,060% growth for enrollments in Generative AI courses, an indicator that interactive learning websites are highly sought after as they help transfer knowledge in cutting-edge technology. SMART Technologies intensified its partnerships with education ministries in October 2024, a move that cemented its presence in emerging markets as governments invest heavily in online learning.

In contrast, November 2024 witnessed Microsoft expanding its contribution to educational partnerships to embed AI throughout its education offerings to drive 30% enterprise adoption growth. September 2024 witnessed Adobe's new cloud-based integrations to enhance scalability at Asia-Pacific schools, while July 2025 UNESCO reports witnessed the observation that although policy has progressed, digital divide is still a challenge highlighting the need for cost-effective, scalable software solutions.

Trends and Opportunities Transforming the Interactive Teaching Software Market

AI-Driven Real-Time Student Engagement Analytics Enhancing Personalized Learning

AI interactive learning platforms are revolutionizing the interactive learning software space with interactive real-time analysis of student understanding, performance, and engagement. AI-powered platforms like Curipod and SchoolAI are leveraging sophisticated algorithms to analyze learner feedback in real-time, detect skill gaps, and offer instant, adaptive feedback that addresses the unique needs of each learner. Such AI-driven personalization not only boosts learners' confidence but also facilitates skill mastery at a quicker rate through rapid iteration and targeted learning activity. For educators, AI dashboards combine class-level and individual performance data, enabling them to detect interventions for struggling learners. Automated quiz and lesson creation also helps decrease teachers' workload, freeing up time for one-to-one mentorship. Detection of early disengagement and skill gaps with proactive intervention has been shown to bring dropout rates down to a great degree, making AI analytics the backbone of the modern digital classroom space.

VR/AR Integration Creating Immersive and Experiential Learning Environments

The integration of augmented reality (AR) and virtual reality (VR) technologies with interactive learning software is revolutionizing STEM and applied education. By enabling visualization of abstract concepts such as molecular structures, historical reconstructions, or engineering blueprints in three dimensions, VR/AR bridges the theoretical-experiential knowledge gap. Virtual environments offer low-cost, risk-free virtual experiments mirroring real-world conditions without logistical or safety constraints. Multi-user VR/AR platforms also support collaborative problem-solving, communication, and critical thinking competencies required for 21st-century professional success. A growing wealth of evidence confirms that VR/AR-enhanced learning richly increases student engagement, retention, and knowledge depth, making immersive technologies a strategic growth engine for the interactive learning software market.

Corporate Upskilling Partnerships Expanding Revenue Streams

Outside the classroom, the business learning market is a lucrative growth opportunity for interactive teaching software firms. Global businesses are facing ever-accelerating skill obsolescence in technologies such as AI, cloud computing, and cybersecurity. Microsoft and Pluralsight have already demonstrated the potential of ongoing employee upskilling through platform-based learning. With adaptive AI-based learning paths, interactive teaching products can tailor training modules to unique career goals and skill levels. Role-playing simulation and AI-based scenario training simulate real-world hands-on training in key business skills such as negotiation, leadership, and customer engagement. Advanced analytics allow employers to measure skill acquisition and connect training programs to quantifiable productivity gains, with a clearly defined return on investment (ROI) for corporate clients.

Localized Language Learning Platforms Targeting Underserved Markets

There is growing demand for AI-driven language learning software for non-English-speaking markets. Duolingo and Babbel dominate the English-learning market, but there is vast potential for localized platforms that incorporate culture and native-language instruction. AI chat-based interfaces can provide personalized grammar correction, pronunciation guidance, and vocabulary training to enable immersion without social anxiety of speaking to a human coach. Integration of cultural modules that encompass idioms, manners, and regional communication practices makes such solutions differentiated and promotes fluency. With language proficiency becoming increasingly directly tied to employability, travel, and cross-border collaborations, vendors that answer local market opportunities have the potential to capture high-growth, underserved markets in the interactive teaching software market.

Market Share Insights in the Interactive Teaching Software Industry

Market Share by Product Type: LMS Leading with AI-Enhanced Personalization

Learning Management Systems (LMS) hold the largest market share of 35% as the pillars of interactive learning environments. The market is shifting toward highly integrated platforms with seamless third-party solution integration, sophisticated analytics, and AI-powered personalization. Interactive whiteboards and screens trail with 25%, riding the wave of hybrid classroom adoption where real-time collaboration capability is a must. Assessment and analytics software is developing strongly, as institutions increasingly adopt data-driven teaching to spot learning gaps and adjust teaching strategies. Authoring tools are shifting toward AI-facilitated design, enabling educators to create multimedia-rich, interactive materials with little technical knowledge. Classroom management software, on the other hand, is being supplemented with real-time monitoring of engagement and behavior tracking, as schools focus on efficiency and accountability.

.png)

Market Share by Application: K-12 Dominating Due to Government EdTech Investments

K-12 leads with a market-high 50% share, fueled by government-sponsored 1:1 device initiatives, digital curriculum initiatives across the country, and focus on hybrid/blended learning models. The segment is targeted to engagement-driven software for various learning styles and accessibility needs. Higher education is leveraging interactive teaching software to scale massive online courses (MOOCs) and enhance experiential learning through AR/VR-based virtual labs particularly in technical and medical domains. Corporate training, accounting for 20% of the market, is also growing fast as companies adopt microlearning modules, gamification-driven training, and VR-based simulations for employee upskilling. Demand for on-demand, mobile-friendly platforms in the segment indicates the confluence of edtech innovation and professional development needs.

Competitive Landscape: Leading Companies in Interactive Teaching Software

The competitive field is characterized by technology leaders, specialized EdTech firms, and hardware-software integrators that are collectively shaping the future of interactive learning environments. Key players included are Microsoft Corporation (Microsoft Education), SMART Technologies ULC, Alphabet Inc. (Google for Education), Promethean World Limited, Discovery Education, Adobe Inc., Chegg, Inc., Renaissance Learning, Inc., Pearson plc, McGraw-Hill Education, Instructure, Inc., BrainPOP, Kahoot!, Nearpod, ClassDojo, Others.

Microsoft Corporation – Cloud-Driven AI Education Ecosystem

Microsoft's key strength lies in its end-to-end learning platform Microsoft Teams, OneNote, and Azure Cloud offering collaboration, lesson delivery, and data analysis all within a single system. Microsoft's approach is based on the unification of AI to automate functions, including the addition of accessibility features, and the offering of data-driven insights. In November 2024, Microsoft extended AI-driven partnerships with schools, accelerating adoption in schools and corporate learning environments.

Google LLC – Seamless, Accessible, and Integrated Learning Tools

Google takes the lead with its simple and free platforms such as Google Classroom and Google Workspace for Education. With simple-to-use platforms such as Google Jamboard to facilitate brainstorming sessions and AI-suggested content ideas, it emphasizes simplicity and accessibility. It has even added new security and privacy controls in order to establish trust with parents and teachers.

SMART Technologies – Hardware-Software Classroom Innovator

A market leader in interactive whiteboards, SMART Technologies pairs its SMART Board with SMART Learning Suite software, offering lesson planning, assessment, and collaboration features. Its integrated system makes hardware and software collaborate as a single teaching system. In October 2024, it formed new global partnerships to drive adoption in nations where governments are investing heavily in digital classrooms.

Promethean (NetDragon Websoft Holdings Limited) – All-in-One Interactive Display Solutions

Promethean offers the ActivPanel and software products like ActivInspire and ClassFlow, which facilitate easy lesson planning and engaging students in real-time. The company focuses on multilingual support and localized software releases for international growth. This has made Promethean a top provider for multicultural and emerging education markets.

Kahoot! – Gamification Leader in EdTech

Kahoot!'s learning platform through games engages students in quizzes, challenges, and leaderboards accessible on any device. Its strategic expansion targets not only classrooms but also business and home learning. In late 2024, Kahoot! also teamed up with a worldwide publisher in a bid to develop quizzes based on curricula, further expanding its content and user base to new segments of users.

China: Government-Led Educational Informatization and AI-Powered Classroom Tools

China’s interactive teaching software market is deeply shaped by the government’s “Educational Informatization 2.0” strategy, which has transformed the country’s digital education infrastructure. By 2021, more than 99.5% of primary and secondary schools were equipped with multimedia classrooms, and over 87% of all classrooms featured advanced multimedia teaching tools. This robust foundation allows for seamless deployment of cloud-based interactive learning platforms, real-time collaboration tools, and multimedia-rich lesson plans. The government’s strategic emphasis on in-school technology adoption particularly in public schools has positioned China as a leading hub for scalable digital education solutions.

Artificial intelligence (AI) integration is a central driver of growth. The push for AI-powered education platforms has resulted in tools capable of automated grading, real-time student performance tracking, and speech recognition for language learning. While the “double reduction” policy initially constrained after-school tutoring providers, it redirected innovation toward curriculum-aligned classroom software that supports teachers directly during instruction. With one of the largest student populations in the world, China provides unparalleled opportunities for testing and refining interactive education solutions at scale, enabling rapid feedback loops and product optimization.

United States: AR/VR Integration and Data-Driven Personalization

The United States remains a global leader in interactive education technology, driven by a competitive and innovation-rich EdTech ecosystem. Companies are incorporating augmented reality (AR), virtual reality (VR), and gamification to transform traditional lessons into immersive learning experiences. Platforms like SMART Learning Suite and Classcraft are integrating real-time feedback tools, collaborative workspaces, and interactive assessments that allow teachers to personalize instruction. Federal and state-level funding programs such as the Elementary and Secondary School Emergency Relief (ESSER) Fund are fueling investments in digital learning infrastructure, ensuring adoption even in underserved districts.

A key differentiator in the U.S. market is the emphasis on data-driven personalized learning. Advanced analytics within interactive teaching software allow educators to monitor individual student progress, identify learning gaps, and deliver tailored lesson plans. The integration of cloud-based Learning Management Systems (LMS) has enabled schools to blend in-person and remote learning without compromising interactivity. With the rise of competency-based education and STEM-focused curricula, the U.S. is fostering an environment where adaptive digital tools are integral to student success.

Germany: GDPR-Compliant Digital Transformation and AI-Enhanced Learning

Germany’s interactive teaching software market is thriving within one of Europe’s most advanced software ecosystems, where data privacy and cybersecurity are paramount. Compliance with strict GDPR regulations has driven the development of secure, privacy-first platforms that build trust among schools and parents. Government initiatives such as the “High-Tech Strategy 2025” and DigitalPakt Schule are accelerating the digital transformation of classrooms through funding for hardware, software, and teacher training. This ensures that cloud-based interactive platforms are implemented in a way that meets rigorous national and EU standards.

German software companies are also investing heavily in AI-powered classroom solutions, enhancing automation in grading, predictive analytics for student performance, and adaptive learning pathways. Interactive whiteboards, digital collaboration tools, and simulation-based learning are becoming increasingly prevalent in secondary schools and vocational education. The integration of STEM-focused digital resources aligns with Germany’s industrial and technological strengths, preparing students with practical skills for the evolving workforce.

Japan: GIGA School Acceleration and Digital Skills Development

Japan’s interactive education software market has experienced significant acceleration under the GIGA School Program, which has provided every student with a computing device and nationwide high-speed internet access. This initiative has laid the groundwork for universal adoption of ICT-enabled interactive learning tools, empowering educators to implement cloud-based lesson plans, collaborative virtual classrooms, and multimedia-enhanced teaching strategies. The country’s advanced 5G network coverage ensures low-latency, high-quality interaction in both urban and rural schools, removing connectivity barriers that could hinder adoption.

The Japanese government’s Educational Digital Transformation Roadmap is further standardizing educational data and integrating AI to support personalized and competency-based learning models. Schools are incorporating software that develops creativity, collaboration, and problem-solving such as digital animation projects and group-based online research tasks. With cultural emphasis on precision and continuous improvement, Japan is leveraging interactive teaching platforms not just to enhance academic outcomes but also to equip students with future-ready digital skills.

Interactive Teaching Software Market Report Scope

Interactive Teaching Software Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.6 Billion

|

|

Market Size (2034)

|

$3 Billion

|

|

Market Growth Rate

|

7.4%

|

|

Segments

|

By Product Type (Learning Management Systems (LMS), Classroom Management Software, Authoring Tools, Interactive Whiteboards/Displays, Assessment and Analytics Software), By Application (K-12 Education, Higher Education, Corporate Training), By Deployment Model (Cloud-Based, On-Premise), By Technology (AI & Machine Learning, Virtual Reality (VR), Augmented Reality (AR), Gamification), By End-User (Teachers, Students, Educational Institutions), By Device Compatibility (Desktop/PC, Mobile Devices, Tablets)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Microsoft Corporation (Microsoft Education), SMART Technologies ULC, Alphabet Inc. (Google for Education), Promethean World Limited, Discovery Education, Adobe Inc., Chegg, Inc., Renaissance Learning, Inc., Pearson plc, McGraw-Hill Education, Instructure, Inc., BrainPOP, Kahoot!, Nearpod, ClassDojo, Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Interactive Teaching Software Market Segmentation

By Product

- Learning Management Systems (LMS)

- Classroom Management Software

- Authoring Tools

- Interactive Whiteboards/Displays

- Assessment and Analytics Software

By Application

- K-12 Education

- Higher Education

- Corporate Training

By Deployment Model

By Technology

- AI & Machine Learning

- Virtual Reality (VR)

- Augmented Reality (AR)

- Gamification

By End-User

- Teachers

- Students

- Educational Institutions

By Device Compatibility

- Desktop/PC

- Mobile Devices

- Tablets

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Interactive Teaching Software Market

- Microsoft Corporation

- SMART Technologies ULC

- Alphabet Inc.

- Promethean World Limited

- Discovery Education

- Adobe Inc.

- Chegg Inc.

- Renaissance Learning Inc.

- Pearson plc

- McGraw-Hill Education

- Instructure Inc.

- BrainPOP

- Kahoot!

- Nearpod

- ClassDojo

* List Not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global Interactive Teaching Software Market, delivering comprehensive analysis reviews, highlighting recent technological breakthroughs, and examining strategic developments that are shaping the industry. It explores the market’s transition from supplemental digital tools to core enablers of active, student-centered learning across K-12, higher education, and corporate training. The study covers advancements in AI-driven personalization, immersive VR/AR experiences, and gamification strategies, along with global EdTech infrastructure expansion. It also assesses competitive landscapes, government-led education initiatives, and the integration of cloud-based analytics for data-driven instruction. By combining in-depth technology analysis with regional adoption patterns and growth forecasts, this report is an essential resource for EdTech companies, policymakers, and institutional decision-makers seeking to navigate and capitalize on the rapidly evolving interactive learning environment. Scope includes-

- Segmentation:

- By Product: Learning Management Systems (LMS), Classroom Management Software, Authoring Tools, Interactive Whiteboards/Displays, Assessment and Analytics Software

- By Application: K-12 Education, Higher Education, Corporate Training

- By Deployment Model: Cloud-Based, On-Premise

- By Technology: AI & Machine Learning, Virtual Reality (VR), Augmented Reality (AR), Gamification

- By End-User: Teachers, Students, Educational Institutions

- By Device Compatibility: Desktop/PC, Mobile Devices, Tablets

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Historic Data & Forecasts: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Analysis/profiles of 15+ companies.

Methodology

The research methodology integrates primary and secondary data sources to provide an accurate, data-driven view of the interactive teaching software market. Primary research involved direct interviews and surveys with EdTech executives, school administrators, corporate training managers, and policymakers across multiple regions. Secondary research encompassed analysis of government education policy documents, industry white papers, patent filings, corporate reports, and reputable academic studies. Quantitative modeling was applied to forecast adoption rates across product segments and geographies, while qualitative insights were derived from case studies of technology deployment in diverse educational contexts. This approach ensures the findings reflect real-world market conditions, emerging opportunities, and competitive positioning strategies.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.