Market Overview: Sterile, Circular, and High-Barrier IBC Liners Safeguard Bulk Flows

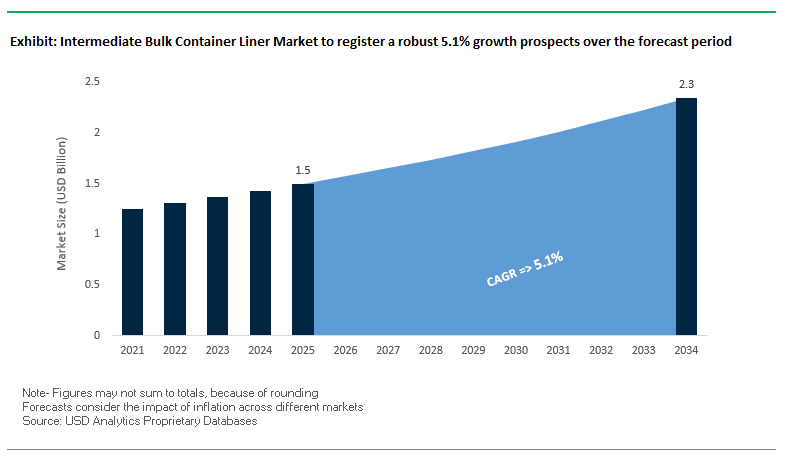

The Intermediate Bulk Container (IBC) Liner Market is valued at USD 1.5 billion in 2025 and is projected to reach USD 2.3 billion by 2034, expanding at a CAGR of 5.1%. For buyers and operations leaders, the key question is how to ensure aseptic integrity, faster changeovers, and lower total cost-to-serve while meeting ESG and circular-economy targets. IBC liners flexible, single-use films that line rigid IBCs deliver sterility, contamination control, and logistics efficiency for bulk liquids, semi-viscous products, and powders across food & beverage, pharmaceuticals, chemicals, and personal care. By eliminating wash cycles, liners cut water/chemical use, speed sanitization, and support closed-loop reconditioning of the rigid outer container. Advanced barrier films (EVOH, metallized layers) now protect oxygen- and light-sensitive products, broadening use from industrial chemicals to high-purity food ingredients.

Key Insights for Industry Professionals:

- Growth vector: USD 1.5B (2025) → 2.3B (2034) at 5.1% CAGR backed by aseptic handling in pharma/food and efficiency gains in chemicals.

- Sustainability lever: Liners eliminate intensive IBC cleaning, lowering water/chemicals and enabling circular reconditioning of rigid IBCs.

- Operational agility: Lightweight, disposable/recyclable liners reduce return logistics, shrink changeover time, and minimize cross-contamination risk.

- Barrier innovation: EVOH/metallized structures extend protection for oxygen/light-sensitive bulks.

- Application breadth: From sterile syrups and nutraceuticals to solvents, resins, and powders, versatility expands addressable demand.

Market Analysis: Recent Developments Signal Smart, Sustainable, and Consolidated Supply

The IBC liner ecosystem is being reshaped by sustainability mandates, digital traceability, and strategic M&A. In August 2025, DNP previewed mono-material, recyclable healthcare packaging in Thailand evidence that medical-grade sustainability requirements are spreading into adjacent bulk formats. Structural consolidation continued in July 2025 with the Amcor–Berry Global combination, strengthening scale in flexibles/rigids and accelerating innovation spillovers into industrial liners.

Materials and digitalization trends remain decisive. June 2025 saw Mondi launch a mono-material recyclable paper-based pouch for pet nutrition, underscoring the market’s pivot to recyclability and simplified structures that can influence liner film design. A report in April 2025 highlighted growing adoption of QR, NFC, RFID capabilities increasingly embedded in bulk logistics to enhance lot traceability, chain-of-custody, and recall readiness. In February 2025, Amcor introduced AmFiber Performance Paper with a 73% lower carbon footprint than standard pouches, aligning with buyer preferences for low-impact packaging systems within broader portfolios. Earlier signals also point to higher circularity: December 2024 research emphasized mono-material adoption for recycling efficiency, while October 2024 showcased Pelican BioThermal’s Crēdo Vault™ for bulk pharma indicative of rising expectations for validated thermal control in high-value bulk movements.

Capacity and regional reach are expanding. Mauser Packaging Solutions advanced its footprint with acquisitions in September 2024 (South Africa) and January 2024 (Consolidated Container Company), strengthening end-to-end industrial container services that complement liner programs.

Key Trends and Opportunities Shaping the Intermediate Bulk Container (IBC) Liner Market

Adoption of High-Barrier Coextruded Films for Oxygen-Sensitive Liquids

The IBC liner market is witnessing a strategic shift towards high-barrier coextruded films designed to protect oxygen-sensitive and moisture-sensitive liquids. This trend is driven by the need to preserve product integrity for food-grade liquids, pharmaceuticals, and high-purity chemicals, extending shelf life while reducing spoilage and operational costs.

Case studies such as CDF Corporation’s Defender™ Liner highlight the impact of high-barrier liners in minimizing cleaning requirements and supporting corporate sustainability initiatives. Advanced film technologies like Toppan Group’s GL BARRIER series, including the transparent GL-SP film, exemplify innovation in both performance and eco-friendly packaging.

In the food and beverage sector, companies like General Films develop coextruded liners for modified atmosphere packaging (MAP) of meats, cheeses, and spices, effectively controlling gas, flavor, and aroma transmission rates to significantly extend shelf life. Meanwhile, ALC Liquid Packaging offers AIRMAX liners with bladder-like systems that facilitate complete discharge of viscous liquids, reducing residual waste and maximizing product yield. This trend demonstrates how high-performance liners are increasingly critical for sensitive, high-value liquids.

Strategic Shift Towards Polymer-Lite and Lightweighting Designs

The lightweighting trend is gaining momentum as IBC liner manufacturers engineer products using less plastic resin without compromising performance. This strategy aligns with corporate sustainability mandates to reduce plastic consumption and Scope 3 transportation emissions.

For example, Mondi’s TankerBox solution, developed in partnership with Aromsa, replaces stainless-steel containers with corrugated cardboard IBCs, offering lighter, sustainable alternatives that simplify transportation and eliminate the need for cleaning and return logistics. Blue Whale’s foldable Paper IBC and liner system demonstrates that lightweight designs can increase loading capacity by up to 20%, optimizing fuel consumption and carbon footprint.

The adoption of single-use liners can also minimize water and energy consumption compared to traditional reusable containers, while innovations such as quad liners from ALC reduce excess material and improve decanting efficiency. These developments underscore the market’s shift toward performance-driven, environmentally conscious, and cost-effective IBC solutions.

Development of Liners for the Green Hydrogen Supply Chain

The emerging green hydrogen economy presents a high-value opportunity for specialized IBC liners capable of safely transporting hydrogen-derived liquids such as ammonia and methanol. Standard liners are often unsuitable, creating demand for chemically resistant, high-performance solutions.

Projects like Air Products’ green ammonia facility in Saudi Arabia highlight the scale of opportunity, with production of 600 tonnes of carbon-free hydrogen per day necessitating reliable logistics for hydrogen derivatives. Methanol transport presents additional challenges due to its solvent properties, which can degrade traditional plastics, and its corrosive effect on metals, emphasizing the need for specialized liners. Companies with advanced polymer science and coextrusion capabilities can capitalize on this emerging, high-value market.

Expansion of Closed-Loop Reusable Liner Services

Another key opportunity lies in moving from single-use liners to managed, reusable services, where liners are collected, cleaned, tested, and reused multiple times. This model supports the circular economy, reduces environmental impact, and creates recurring revenue streams for manufacturers.

Solutions like Goodpack’s reusable IBC leasing model illustrate the viability of closed-loop liner services, minimizing waste and emissions while enhancing operational efficiency. Academic research confirms that reusable IBCs outperform single-use systems in environmental performance, with benefits increasing with the number of cycles. Reconditioning liners reduces manufacturing demand and provides cost-effective solutions for end-users. Additionally, regulations such as the EU Packaging and Packaging Waste Regulation (PPWR) encourage reusable packaging adoption, creating strong market pull for service-based liner solutions.

Competitive Landscape: Integrated Rigid-Plus-Liner Systems, Circular Services, and High-Barrier Films

The global IBC liner market is led by companies combining materials science, cleanroom production, and container lifecycle services. Winners offer aseptic, high-barrier liners matched to reconditioned or recycled-content IBCs, and increasingly layer in digital IDs for asset and batch tracking.

SCHÜTZ: Circular IBC systems with recycled plastics and smart IDs

Overview. SCHÜTZ couples in-house plastics with liner manufacturing and IBC assembly, delivering tight quality control across ECOBULK/RECOBULK systems. In August 2025, it launched GREEN LAYER IBCs made from recycled plastic and promoted INFO-ID QR access to packaging data.

Market role. SCHÜTZ supplies aseptic, high-barrier, and standard liners tailored to food, chemicals, and pharma, integrating liners with RECONTAINER collection/reconditioning for circularity. The strategy centers on closed-loop systems, digital traceability, and lower-impact materials without compromising hygiene or mechanical strength.

Mauser Packaging Solutions: Lifecycle services and global capacity expansion

Overview. Mauser’s strength is rigid packaging plus services across the container lifecycle. It expanded production and regional presence via acquisitions in September 2024 (South Africa) and January 2024 (Consolidated Container Company).

Market role. Mauser’s aseptic, high-barrier, and standard liners protect products from food ingredients to industrial chemicals while its Recover Syst-M program advances reuse and recycling. Strategy: grow through M&A, broaden regional availability, and embed sustainability in reconditioning and liner supply to reduce customers’ total cost and footprint.

Scholle IPN (SIG): Liquid expertise with fitments, films, and aseptic know-how

Overview. Now part of SIG (June 2022), Scholle IPN brings bag-in-box and spouted pouch leadership to IBC liner solutions, pairing barrier films, aseptic fitments, and filling equipment.

Market role. Portfolio includes aseptic and high-barrier IBC liners used from wine and juices to chemicals and personal care. Strategy focuses on low-carbon, high-performance liquid systems, leveraging SIG’s scale to deliver integrated film-fitment-filler ecosystems that elevate product safety and throughput.

TPS Rental Systems: One-stop rental, liners, and pooling services

Overview. TPS specializes in IBC rental and services, offering a full suite from containers and liners to accessories and cleaning. In August 2025, it highlighted in-house liner/component production; in January 2025, TPS joined HB RTS, strengthening its European platform.

Market role. TPS supplies EVOH, LDPE/MDPE oxygen-barrier, and metallized polyester liners, including aseptic/irradiated variants for high-sterility needs. Strategy: provide a cost-efficient “one-stop-shop” that compresses lead times, enables pooling, and enhances traceability and hygiene across rotating fleets.

IPI Global: Safety-first solutions for chemicals and hazardous goods

Overview. IPI Global serves chemical, paints, inks, and lubricants markets with compliant IBCs and liner systems. In August 2025, it showcased the ProBlend Mixing System; in April 2025, it co-produced training content on closed transfer (Micro Matic) for safe pentane handling.

Market role. IPI’s liner and container portfolio targets stringent safety and quality standards to ensure secure transport/storage of hazardous goods. Strategy: application-specific engineering, training, and partnerships that improve operator safety, reduce volatile loss, and raise filling/decanting efficiency.

Intermediate Bulk Container Liner Market Share Insights

Form-Fit Liners Hold Largest Market Share by Product Type in Intermediate Bulk Container Liners

Form-fit liners capture 60% of the IBC liner market in 2025, underscoring their efficiency and technical superiority in protecting bulk liquids and powders. Engineered to match the exact dimensions of intermediate bulk containers, these liners reduce trapped air, minimize product residue, and enhance stability during filling and transport. Their dominance is closely linked to industries dealing with oxygen-sensitive or high-value materials such as edible oils, flavorings, lubricants, and pharmaceutical intermediates where product integrity and maximum yield are critical. Pillow liners continue to hold a notable share due to their versatility and lower cost, making them suitable for less viscous products and general-purpose industrial uses. Specialized liners in the “others” category, including sterile and barrier-enhanced versions, cater to high-purity pharmaceuticals, biopharmaceuticals, and fine chemicals. This segmentation demonstrates how form-fit liners dominate through performance-driven adoption, while pillow liners and specialty options provide adaptability and niche solutions.

Industrial Chemicals Dominate Market Share by Application in Intermediate Bulk Container Liners

Industrial chemicals represent 40% of the IBC liner market in 2025, making them the largest application segment by volume. The sector depends heavily on liners for transporting lubricants, solvents, additives, and resins, where product protection against contamination and container corrosion is crucial. The use of liners reduces cleaning requirements, prolongs IBC lifespan, and lowers overall operational costs, making them indispensable in large-scale industrial supply chains. The food and beverages industry follows with a 35% share, driven by demand for hygienic and certified liners to transport oils, syrups, concentrates, and dairy-based products while maintaining purity and preventing flavor migration. Pharmaceuticals & healthcare, although smaller in volume, represent a premium-driven application, where compliance with stringent regulatory frameworks (e.g., FDA, USP Class VI) ensures liner adoption for biopharmaceutical ingredients and sterile intermediates. Cosmetics and personal care industries also rely on liners for sensitive raw materials such as fragrances and essential oils, where oxidation or contamination risks could compromise product quality. This segmentation highlights how industrial chemicals secure volume leadership, while food, pharma, and cosmetics sustain value-driven adoption of advanced liner solutions.

United States IBC Liner Market Driven by Regulatory Compliance and Smart Dispensing Innovations

The U.S. Intermediate Bulk Container (IBC) liner market is shaped by a complex regulatory environment, including FDA and DOT requirements, which ensure safe transportation of chemicals, pharmaceuticals, and food products. The Drug Supply Chain Security Act (DSCSA) further drives adoption of variable data printing for traceable, compliant labeling on IBCs, enhancing supply chain security.

Technological innovations are transforming the market, such as CDF Corporation’s Form-Fit™ liners with perforated flaps for secure positioning during filling, and its Air-Assist® system for improved product dispensing of viscous liquids. Corporate investments are also reshaping the landscape; Sealed Air’s acquisition of Liquibox expands its CRYOVAC liquid packaging portfolio, strengthening capabilities for bulk liquid handling. Strong demand exists in food and beverage, industrial liquids, and household products sectors, where IBC liners are critical for safe, efficient, and sustainable transportation. Sustainability remains a key priority, with recyclable and eco-friendly liners reducing environmental impact while meeting regulatory expectations.

Germany IBC Liner Market Advancing Through Circular Economy Initiatives and Industry 4.0 Integration

Germany’s IBC liner market is heavily influenced by the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which mandates full recyclability or reusability by 2030. The Packaging Act (VerpackG) further incentivizes recyclable designs via modulated fees, favoring single-use and reusable IBC liners over traditional alternatives.

Technological advancements are at the forefront, supported by Industry 4.0 initiatives that integrate digital manufacturing technologies. Partnerships, such as Mauser Packaging Solutions and Rikutec Packaging in 2024, focus on reducing plastic waste and enhancing sustainable IBC solutions. Corporate investments, including Aran Group’s acquisition of IBA Germany in February 2024, enable development of 1,000-liter IBCs and strengthen Germany’s market position. These innovations drive efficiency, sustainability, and high-performance liquid handling capabilities.

China IBC Liner Market Expanding Through Green Policies and Smart Manufacturing

China’s IBC liner market is benefiting from governmental green initiatives, including the March 2024 “Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement,” which encourages sustainable material use and recycling. Regulatory reforms, such as GB/T 31268, curb excessive packaging and support more efficient bulk packaging solutions.

Technological investments are transforming production, with automation, AI, and “5G plus industrial internet” integration enhancing process flexibility and efficiency. Real-time tracking technologies like Greif’s GCube Connect improve supply chain visibility and performance. Domestic manufacturing expansion, led by companies such as CIMC Transpack Technology and Yantai Jinxiang Plastic, meets growing demand for high-quality, circular, and locally produced IBC liners.

India IBC Liner Market Gaining Momentum from Circular Economy Initiatives and Cold Chain Growth

India’s government initiatives promoting a circular economy are boosting the IBC liner market. Eco-friendly solutions and regulatory support for sustainable packaging encourage adoption of IBC liners for bulk liquid transport.

Technological advancements include automated production lines and specialized materials, such as liners derived from agricultural waste. Chill box solutions by Archian Foods Pvt. demonstrate innovative approaches to rural cold chain distribution. Corporate investments are rising, with expanding production to meet demand from the growing food processing and pharmaceutical sectors. Regulatory compliance, especially with FSSAI food safety standards, further drives the need for high-quality, hygienic, and safe IBC liners.

Brazil IBC Liner Market Strengthened by Sustainable Policies and Trade-Driven Growth

Brazil’s IBC liner market is shaped by sustainable waste management practices under the amended National Solid Waste Policy, encouraging domestic recycling programs. The EU-Mercosur trade agreement is expected to attract investment and diversify market participation.

Technological innovation focuses on specialized solutions for the food, beverage, and agricultural chemicals sectors. Strong export growth in goods like tomato paste and processed foods fuels demand for high-performance, safe, and sustainable IBC liners. Domestic and international players are investing in advanced solutions to meet rising logistical and regulatory requirements, driving efficiency in bulk liquid transportation.

United Kingdom IBC Liner Market Driven by EPR Regulations and Eco-Friendly Bulk Packaging

The UK’s Extended Producer Responsibility (EPR) legislation transfers the cost of handling packaging waste to businesses, imposing higher fees on non-recycled plastics. This incentivizes adoption of reusable or recyclable IBC liners to reduce environmental impact and costs.

Technological innovations focus on eco-friendly and recyclable solutions compliant with regulatory standards. Government bans on certain single-use plastics further promote alternative bulk packaging solutions. Key applications are concentrated in the chemicals, pharmaceuticals, and food and beverage sectors, where safe and efficient transportation of bulk liquids is essential. The market thrives on sustainable innovation and regulatory compliance, reinforcing eco-conscious supply chain practices.

Intermediate Bulk Container Liner Market Report Scope

Intermediate Bulk Container Liner Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.5 Billion

|

|

Market Size (2034)

|

$2.3 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Product Type (Form-Fit Liners, Pillow Liners, Others), By Material (PE, EVOH, Aluminum Foil, Others), By Capacity (Up to 1000 Liters, Above 1000 Liters), By Application (Food & Beverages, Industrial Chemicals, Cosmetics & Personal Care, Pharmaceuticals & Healthcare, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sealed Air Corporation, Scholle IPN, Liquibox, Greif, Inc., Amcor plc, Smarfit Kappa Group, CDF Corporation, IBA GmbH, ILC Dover LP, Rieke Packaging Systems, Peak Liquid Packaging, Aran Group, Arena Products, Inc., Qbig Packaging B.V., Mulitpac Systems

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Intermediate Bulk Container Liner Market Segmentation

By Product Type

- Form-Fit Liners

- Pillow Liners

- Others

By Material

- PE

- EVOH

- Aluminum Foil

- Others

By Capacity

- Up to 1000 Liters

- Above 1000 Liters

By Application

- Food & Beverages

- Industrial Chemicals

- Cosmetics & Personal Care

- Pharmaceuticals & Healthcare

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Intermediate Bulk Container Liner Market

- Sealed Air Corporation

- Scholle IPN

- Liquibox

- Greif, Inc.

- Amcor plc

- Smarfit Kappa Group

- CDF Corporation

- IBA GmbH

- ILC Dover LP

- Rieke Packaging Systems

- Peak Liquid Packaging

- Aran Group

- Arena Products, Inc.

- Qbig Packaging B.V.

- Mulitpac Systems

* List Not Exhaustive

Methodology

USDAnalytics employed a comprehensive and structured research methodology to evaluate the Intermediate Bulk Container (IBC) Liner Market, combining primary interviews with packaging engineers, logistics managers, and supply chain professionals across food & beverage, pharmaceuticals, chemicals, and personal care industries, alongside secondary research from corporate reports, regulatory documents, technical journals, and verified industry databases. Market sizing, CAGR projections, and forecasts were derived using both bottom-up and top-down approaches, validated against historical sales, material consumption, and adoption trends across major regions. The analysis incorporates innovations in form-fit, pillow, and high-barrier liners using PE, EVOH, aluminum foil, and coextruded films, alongside technological advancements such as IoT-enabled tracking, RFID integration, and aseptic dispensing systems. Sustainability considerations including single-use vs. reusable liner programs, circular economy initiatives, and regulatory frameworks like the EU Packaging and Packaging Waste Regulation (PPWR) and Extended Producer Responsibility (EPR) mandates were factored into growth projections. Regional dynamics for the U.S., Germany, China, India, Brazil, and the U.K. were examined, alongside competitive strategies of leading players including Sealed Air, SCHÜTZ, Mauser Packaging, Scholle IPN, TPS Rental Systems, and IPI Global, highlighting their innovations in aseptic, high-barrier, and sustainable IBC liner solutions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.