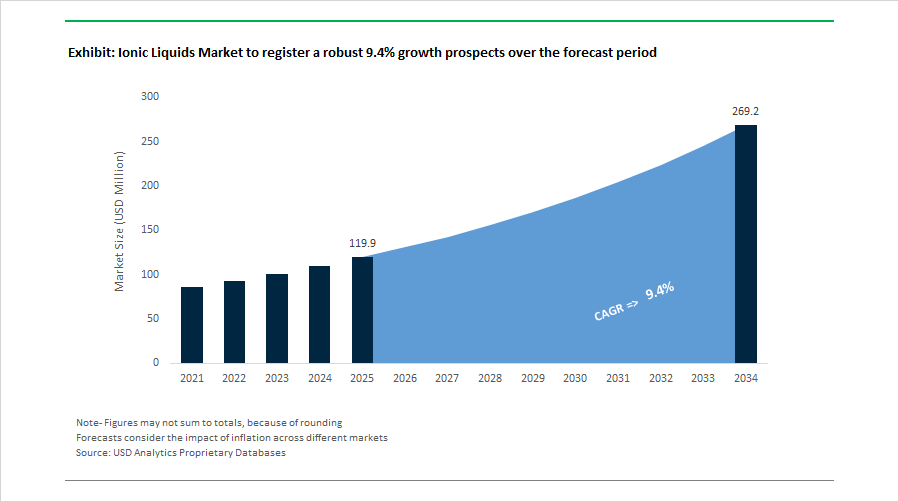

Ionic Liquids Market to Reach $269.1 Million by 2034 at 9.4% CAGR as Battery Electrolytes, Carbon Capture, and Green Solvents Accelerate Adoption

The Ionic Liquids Market is projected to expand from $119.9 Million in 2025 to $269.1 Million by 2034, reflecting a strong CAGR of 9.4%. This growth trajectory is anchored in the rapid commercialization of ionic liquid electrolytes for advanced batteries, the replacement of volatile organic compounds in chemical synthesis, and the integration of ionic liquids into carbon capture, biomass fractionation, and metal finishing processes. The sector is transitioning from laboratory-scale specialty solvents to industrial-scale platforms enabling energy storage, sustainable manufacturing, and circular carbon utilization.

Strategic consolidation and portfolio expansion defined 2024. In April 2024, Arkema acquired a 78% stake in Proionic, strengthening its position in non-flammable ionic liquid electrolytes for solid-state lithium-ion batteries. In 2024, BASF introduced a standardized green chemistry ionic liquid range aimed at replacing VOC-based solvents in synthesis and extraction workflows across its Verbund network. During the same year, Merck KGaA expanded its Cyphos phosphonium salt portfolio, supporting hydroformylation and dimerization catalysis in petrochemical processing. In August 2024, IOLITEC launched IL-0349-N1123 BTA, engineered for electrochemical CO2 reduction, enabling more efficient greenhouse gas conversion into value-added chemicals. The 2024 Gordon Research Conference further reinforced the industry pivot toward bio-derived ionic liquids, with academic and commercial stakeholders outlining the shift from petroleum-based cations to amino acid and sugar-derived structures.

Commercial scale-up accelerated through 2025. Lixea operationalized its Bio-Fractionation platform using low-cost ionic liquid solvents to convert wood waste into high-purity cellulose and lignin, presenting a lower-energy alternative to traditional pulping. Scionix expanded Deep Eutectic Solvent production to support chrome-free plating and safer electropolishing in the metal finishing industry. Solvionic entered a partnership with an automotive OEM to develop ionic liquid electrolytes for sodium-ion batteries, leveraging the wider electrochemical stability window of ionic systems to improve cycle life and safety. Evonik transitioned portions of its ionic liquid portfolio to ISCC PLUS-certified mass-balanced feedstocks, reducing carbon intensity for pharmaceutical and lubricant customers. Tokyo Chemical Industry broadened global bulk availability of room-temperature ionic liquids to support gas separation scale-up in North America and Europe.

Technological acceleration intensified in 2026. In January 2026, a major review from Nanjing Tech University confirmed that machine learning algorithms reduced ionic liquid candidate screening times from over 1,200 seconds to 4.12 seconds, enabling rapid evaluation across 10¹⁸ potential cation-anion combinations for carbon capture and electrochemical applications. Following the Arkema–Proionic integration, early 2026 saw the launch of a gel-polymer electrolyte combining ionic conductivity with polymer mechanical stability, targeting flexible electronics and medical sensors. These developments signal a structural shift in the ionic liquids industry toward data-driven formulation, battery-grade purity, and sustainable solvent engineering across energy, petrochemicals, advanced materials, and circular manufacturing ecosystems.

Key Trends and Strategic Opportunities in the Ionic Liquids Market

Industrial Scaling of Ionic Liquid Electrolytes for High-Safety Energy Storage

The global shift toward solid-state batteries and lithium-metal battery architectures is moving ionic liquids from laboratory-scale novelty into industrially relevant electrolyte systems. Their intrinsic non-flammability, negligible vapor pressure, and wide electrochemical stability window exceeding 5 volts position ionic liquids as a critical enabler for next-generation electric vehicle platforms and stationary energy storage systems where safety and durability are non-negotiable.

By 2025, large-scale battery material suppliers have begun integrating ionic liquids directly into Gigafactory qualification programs. BASF, which holds an estimated 24.8% leadership position in battery-grade ionic liquids, has accelerated the commercialization of imidazolium-based electrolytes. These materials now account for approximately 45.2% of the global battery-grade ionic liquid segment, reflecting their balance of ionic conductivity, chemical stability, and manufacturing scalability. Their growing adoption underscores a structural transition away from flammable carbonate solvents that have historically constrained battery safety thresholds.

Performance under extreme operating conditions is further strengthening adoption. Pyrrolidinium-based ionic liquids have gained rapid traction in automotive and consumer electronics applications, particularly in cold-climate markets. Field validation conducted during 2025 demonstrated that these electrolytes retain high ionic conductivity at sub-zero temperatures, directly addressing electric vehicle range degradation in winter conditions and improving cold-start reliability for energy-dense battery packs.

At the grid and industrial level, phosphonium-based ionic liquids are being prioritized for high-temperature energy storage systems. Capable of continuous operation at temperatures approaching 150°C, these electrolytes provide a critical safety buffer against thermal runaway in large-format cells used for renewable energy buffering and industrial load balancing. For utilities and infrastructure investors, this translates into lower insurance risk, longer asset lifetimes, and improved system-level resilience.

Deployment of Task-Specific Ionic Liquids for Industrial Carbon Management

Carbon capture economics are entering a decisive phase as regulatory and fiscal frameworks tighten globally. The implementation of the EU Carbon Border Adjustment Mechanism and the expansion of U.S. 45Q tax credits have shifted industrial focus toward capture technologies that materially reduce energy penalties. Task-Specific Ionic Liquids are emerging as a strategic alternative to conventional aqueous amine systems in post-combustion carbon capture.

In 2025, a landmark study leveraging generative deep learning to design ionic liquid structures identified an imidazolium-based TSIL capable of reducing regeneration energy requirements by at least 34% compared to monoethanolamine. This reduction directly improves capture economics by lowering steam demand and operational costs, making ionic liquid systems increasingly viable for cement, steel, and refining applications.

Beyond power generation, ionic liquids are gaining traction in biogas upgrading and synthetic fuel production. In July 2025, Japanese chemical manufacturers announced the adoption of ionic liquids for bio-LNG purification, where these solvents efficiently remove carbon dioxide and hydrogen sulfide in a single step. This capability is strengthening supply chains for decarbonized marine fuels and supporting Japan’s broader hydrogen and ammonia co-firing strategies.

Importantly, scale-up risk is diminishing. By late 2025, multiple government-backed programs in Asia-Pacific and North America had transitioned ionic liquid carbon capture technologies from laboratory vessels to 1,000-liter pilot reactors. These demonstrations validated long-term solvent stability and showed capture costs materially below those of traditional amine-based systems, signaling readiness for pre-commercial deployment.

High-Performance Lubricants for Extreme Aerospace, Robotics, and Energy Applications

Ionic liquids are unlocking a premium lubricant segment where conventional synthetic oils fail due to volatility, oxidation, or thermal breakdown. Their ultra-low vapor pressure and exceptional thermal stability make them particularly attractive for aerospace, defense, robotics, and deep-sea applications that demand maintenance-free operation under extreme conditions.

Aerospace and defense programs are increasingly qualifying ionic liquid lubricants for bearings and gear systems operating at high altitude and under vacuum-like conditions. In these environments, traditional oils can evaporate or chemically degrade, whereas ionic liquids maintain consistent film strength and lubricity, directly supporting mission-critical reliability and longer service intervals.

Tribological innovation is accelerating this opportunity. Research published in early 2025 introduced polyoxometalate-based ionic liquids as next-generation lubricant additives. These materials form oxide-rich tribofilms on stainless steel and high-performance alloys, delivering friction and wear reduction comparable to zinc dialkyldithiophosphate while avoiding its toxicity and ash formation concerns.

Energy infrastructure applications are also emerging as a commercial frontier. In collaboration with the U.S. Department of Energy, researchers at Oak Ridge National Laboratory demonstrated ionic liquid-based lubricant additives for aquatic turbines during 2024–2025 testing. Results showed 50% lower friction and a tenfold reduction in equipment wear versus commercial gear oils, while meeting stringent zero-toxicity standards for aquatic ecosystems. This positions ionic liquids as a strategic solution for hydropower, tidal energy, and offshore renewable assets.

Selective Depolymerization for Textile and Mixed Plastic Recycling

Chemical recycling is becoming central to circular economy strategies as mechanical recycling fails to address blended and contaminated polymer streams. Ionic liquids are emerging as a foundational technology for selective depolymerization, enabling high-purity material recovery from complex waste such as polycotton textiles and multilayer plastics.

In December 2025, a high-profile collaboration between RadiciGroup and The Lycra Company successfully demonstrated a closed-loop recycling process for mixed nylon and elastane textiles. Using ionic liquid-based selective dissolution, the project recovered high-purity nylon and Lycra from blended swimwear, which were subsequently re-spun into new garments. This milestone directly addresses one of the apparel industry’s most persistent recycling bottlenecks.

Polyurethane foam recycling represents another high-impact opportunity. A 2025 study published in Molecules detailed a scalable depolymerization route for polyurethane waste using imidazolium-based ionic liquids. The process achieved kilogram-scale reactions while recovering polyols with molecular structures equivalent to virgin materials, enabling true material circularity for insulation, automotive seating, and furniture applications.

From an economic standpoint, ionic liquid depolymerization operates under relatively mild conditions, typically between 80°C and 200°C, while achieving monomer recovery yields exceeding 95%. This combination of high yield and low thermal severity is particularly attractive for food-grade packaging and premium apparel brands that require virgin-equivalent material performance, positioning ionic liquids as a cornerstone technology for next-generation recycling infrastructure.

Ionic Liquids Market Share and Segmentation Insights

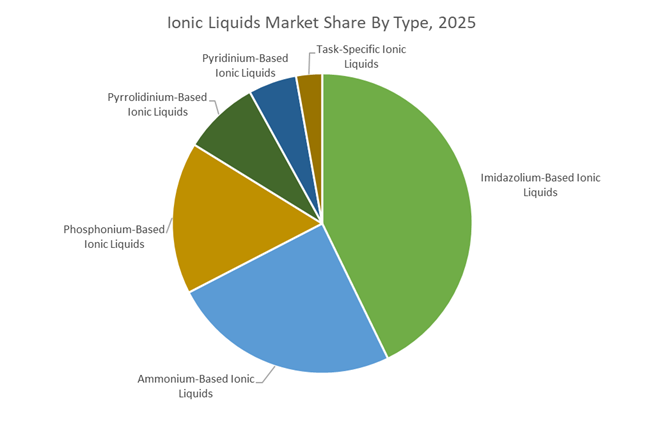

Imidazolium-Based Ionic Liquids Lead the Market Through Electrochemical Stability and Energy Storage Compatibility

Imidazolium-based ionic liquids held 42.80% of the Ionic Liquids Market share in 2025, making them the most widely used ionic liquid chemistry across industrial and advanced technology applications. These ionic liquids are valued for their low viscosity, high ionic conductivity, excellent thermal stability, and broad electrochemical window, properties that enable their use as advanced solvents and electrolytes in modern chemical processes. Imidazolium cations combined with various anions allow manufacturers to engineer tailored ionic liquid formulations with specific polarity, viscosity, and conductivity characteristics, supporting applications in chemical synthesis, catalysis, electrochemistry, and separation technologies. In 2025, the strongest growth driver for this segment is the rapid expansion of energy storage technologies, where imidazolium ionic liquids are used as electrolyte components in lithium-ion batteries, supercapacitors, and advanced electrochemical devices. Their non-flammable nature, wide operating temperature range, and improved electrochemical stability enhance battery safety and cycle life, making them attractive alternatives or additives to conventional organic carbonate electrolytes in high-performance energy storage systems.

Chemical and Petrochemical Sector Drives the Largest Consumption of Ionic Liquids

The chemical and petrochemical sector accounted for 42.80% of the Ionic Liquids Market share in 2025, positioning it as the leading industrial consumer of ionic liquid technologies. Ionic liquids function as green solvents, catalytic media, and selective separation agents in a wide range of chemical manufacturing processes, offering advantages such as low vapor pressure, high thermal stability, and tunable molecular structures that allow optimization for specific reactions. In petrochemical refining and chemical synthesis, ionic liquids enable improved reaction selectivity, enhanced catalyst performance, and simplified product separation, contributing to process intensification and operational efficiency. In 2025, one of the fastest-growing industrial applications involves acid gas removal and carbon capture, where ionic liquids are used to selectively absorb carbon dioxide (CO₂) and hydrogen sulfide (H₂S) from natural gas streams, refinery gases, and biogas upgrading systems. Compared with traditional amine-based solvents, ionic liquids can provide lower regeneration energy requirements and reduced corrosion, supporting their adoption in commercial gas processing facilities and emerging carbon capture technologies across the global energy sector.

Competitive Landscape in Ionic Liquids Market

BASF SE Commercializes Advanced Ionic Liquids Through BASIL and Basionic Platforms

BASF SE remains the foundational commercial pioneer in ionic liquids, having industrialized the BASIL process to enable biphasic acid scavenging at scale. Preliminary 2025 sales reached €59.7 billion, with 2026 priorities centered on enabling green transformation across its Chemicals and Materials segments. The Basionic portfolio includes imidazolium and pyridinium-based ionic liquids used as catalytic additives, selective scavengers, and specialty solvents in fine chemical synthesis. BASF is advancing commercialization of BMImTFSI, a high-stability ionic liquid critical for electrochemical and battery applications requiring broad voltage stability and low volatility. Leveraging its Zhanjiang Verbund site, the company is strengthening supply to Asian electronics and semiconductor manufacturers demanding electronic-grade purity. Its restructuring progress enhances operational agility in scaling advanced ionic liquid chemistries for energy storage and specialty materials markets.

Evonik Industries AG Aligns Ionic Liquids with Energy Transition Strategy

Evonik positions ionic liquids within its Specialty Additives and Smart Materials divisions, aligning R&D with biosolutions, energy transition, and circular economy priorities. The company targets an additional €1.5 billion in sales by 2032 through innovation-driven growth. Investment in anion exchange membranes and ionic liquid-based electrolytes supports green hydrogen electrolysis and next-generation battery platforms. Evonik is transitioning global production assets to operate on 100% renewable electricity to reduce Scope 2 emissions across chemical product lines. Under the TEGO and Noblyst brands, it markets ionic liquids optimized for flow chemistry, sustainable coatings, and specialty additive systems. Integration of energy-focused R&D with scalable manufacturing strengthens its competitive stance in electrochemical and catalytic ionic liquid applications.

Merck KGaA Dominates High-Purity Ionic Liquids for Electronics and Pharma

Merck KGaA leads the high-purity ionic liquids segment exceeding 99% purity, which is projected to command nearly half of total market demand due to stringent pharmaceutical and semiconductor standards. Operating as EMD Performance Materials in North America, the company supplies an extensive catalog including Cyphos phosphonium salts and diverse imidazolium derivatives for research and pilot-scale production. In March 2026, Merck reinforced its regional diversified supply architecture to support intensified demand for ultrapure chemical processing in semiconductor fabrication. The integration of ionic liquids into its Life Science division enhances API solubility, bioavailability, and biocatalytic efficiency. Its positioning at the intersection of electronics-grade purity and pharmaceutical compliance underpins premium-margin leadership.

Solvay S.A. Advances High-Voltage Battery and Extraction Applications

Solvay specializes in phosphonium-based ionic liquids for industrial catalysis and solvent extraction systems. Following corporate restructuring, the company is concentrating on essential chemicals and high-purity salt platforms for electronics and automotive industries. Recent development efforts focus on pyrrolidinium ionic liquids paired with fluorinated sulfonyl-imide anions, delivering energy density improvements of 15 to 20% in high-voltage battery systems operating up to 5.2 V. Solvay maintains dominance in extraction and separation processes, particularly in recovery of precious metals and rare earth elements from industrial waste streams. Capacity expansion for Nocolok flux technologies supports thermal management innovation in electric vehicles, indirectly reinforcing demand for associated high-performance ionic systems.

IoLiTec Drives Task-Specific Ionic Liquid Innovation for Next-Gen Batteries

IoLiTec operates as a pure-play specialist bridging academic research and industrial-scale ionic liquid deployment. In January 2026, the company initiated the SALSA project focused on aluminum-ion battery development using custom ionic liquid electrolytes. Recent product introductions include magnesium tetrakis(hexafluoroisopropoxy)borate, supporting magnesium-ion battery research and advanced energy storage systems. IoLiTec is proactively addressing the discontinuation of 3M Novec products by offering ionic liquid alternatives characterized by zero vapor pressure and superior thermal stability. Strategic collaborations with BASF and Metrohm enhance analytical validation and scalability of task-specific ionic liquid chemistries. Its specialization in customized electrolyte systems positions it at the forefront of emerging multivalent battery technologies.

Tatva Chintan Pharma Chem Expands Cost-Effective Scale in Asia-Pacific

Tatva Chintan Pharma Chem has emerged as a key global supplier enabling industrial-scale adoption of ionic liquids through cost-efficient manufacturing. With Asia-Pacific accounting for over half of global demand due to concentrated pharmaceutical and specialty chemical production, the company is rapidly expanding its regional footprint. It specializes in phase transfer catalysts, structured directing agents, and room-temperature ionic liquids, including high-volume imidazolium and quaternary ammonium salts. The Localization and Scale strategy emphasizes high-capacity production for global pharmaceutical and specialty chemical clients. Strengthened R&D investment targets biodegradable ionic liquids to address regulatory scrutiny surrounding persistent fluorinated chemistries, reinforcing long-term sustainability positioning in the evolving ionic liquids market.

Germany Ionic Liquids Market: Green Transformation, Battery Electrolytes, and PFAS Substitution

Germany is consolidating its position as a global innovation hub for ionic liquids through coordinated investment in green chemistry, battery technologies, and regulatory-driven substitution. In March 2025, BASF confirmed a stable €2.1 billion R&D budget for 2025 under its Winning Ways strategy, with ionic liquids prioritized as enablers of biodegradable solvents and digitally accelerated formulation. The integration of AI-based molecular modeling is shortening development cycles for task-specific ionic liquids, particularly for customized solvent systems required in coatings, catalysis, and separation technologies.

Electrochemical applications are advancing in parallel. In July 2025, the BMBF-backed ALBATROS project concluded successfully with participation from Iolitec, validating chloroaluminate ionic liquid electrolytes for aluminum-ion batteries at industrial scale. This milestone strengthens Germany’s role in post-lithium battery development. Iolitec further expanded domestic supply chains in January 2025 by commercializing magnesium tetrakis(hexafluoroisopropoxy)borate, a critical intermediate for magnesium-ion battery electrolytes and weakly coordinating anion chemistry. Sustainability transparency is becoming a market requirement. In December 2025, Evonik published verified Environmental Product Declarations for PROTECTOSIL building protection systems that incorporate ionic liquid-based additives, aligning with forthcoming 2026 EU lifecycle disclosure rules. Regulatory pressure is also reshaping demand as German producers introduced ionic liquid alternatives to discontinued 3M Novec and fluorinated fluids, positioning PFAS-free solutions for industrial heat transfer and surfactants ahead of 2026 mandates. Germany’s leadership was reinforced in July 2025 when it hosted COIL-10, where industry participants formalized 2026 partnerships around CO2 capture using task-specific ionic liquids.

China Ionic Liquids Market: High-End Chemicals, Electronics, and EV Scale-Up

China’s ionic liquids industry is expanding under a policy framework that emphasizes high-end chemical upgrading, electronics manufacturing, and electric vehicle scale. Under the MIIT high-end chemical blueprint for 2025–2026, ionic liquids are explicitly identified as future-ready materials for electronic-grade gas separation and precision processing. This directive is accelerating investment in imidazolium, pyrrolidinium, and task-specific ionic liquids tailored for semiconductors and advanced materials.

Industrial execution is progressing rapidly. In November 2025, Evonik completed trial production at its second polyamides reactor in Shanghai, using ionic liquid catalysts to double output of long-chain polyamides for automotive and technical textiles. BASF is integrating ionic liquid-based extraction processes at its Zhanjiang Verbund site as it enters its 2026 operational phase, supporting domestic electronics supply chains with higher-purity specialty chemicals. Battery ecosystems are also clustering internationally. Through the GIGAGREEN consortium, Chinese manufacturers and partners including Solvionic completed a 36-month assembly phase in Valencia in September 2025, focused on scaling ionic liquid electrolytes for EV batteries serving China’s mass market. At the application level, Jinkai Chemical expanded its portfolio of imidazolium-based ionic liquids in 2025 for antistatic and precision cleaning uses in the semiconductor hubs of Shenzhen and Suzhou.

United States Ionic Liquids Market: Refining Safety, Rare Elements, and Pharmaceutical Integration

The United States ionic liquids market is characterized by long-cycle industrial adoption, strategic resource processing, and emerging pharmaceutical use cases. In refining, Honeywell and Chevron continued commercial operation of the ISOALKYL ionic liquid alkylation technology through 2025, providing a safer alternative to hydrofluoric acid in gasoline production. With multiple 2026 licensing agreements under discussion, ionic liquid alkylation remains a cornerstone of U.S. downstream fuel safety strategy.

Resource security and healthcare applications are broadening the base. In late 2024, Ionic Rare Elements Limited secured UK and U.S. approvals to acquire SerenTech, which employs ionic liquid-based solvent extraction to refine rare earth elements critical for permanent magnets. In biotechnology, CAGE Bio achieved clinical milestones in 2025 for ionic liquid-based therapeutics targeting papulopustular rosacea, marking a shift toward ionic liquids as active pharmaceutical ingredients rather than solely processing aids. Regulatory dynamics are reinforcing coatings demand. EPA VOC limits effective in 2026 are accelerating transitions to water-borne and high-solid systems, driving increased use of ionic liquid matting agents and moisture scavengers among U.S. formulators.

France Ionic Liquids Market: Battery Passport Readiness and Energy Storage Innovation

France’s ionic liquids sector is anchored in electrochemical innovation and compliance with Europe’s emerging battery governance framework. Under the France 2030 plan, Solvionic secured EPSILON project funding to develop ultra-high-purity ionic liquid electrolytes exceeding 99.9% purity. These materials are designed to meet the traceability and performance thresholds mandated by the European Battery Passport, positioning France as a critical node in compliant battery supply chains.

Product innovation is accelerating toward commercialization. In July 2025, Solvionic introduced Solviolyte, an ionic liquid formulation engineered to enhance interfacial stability in all-solid-state batteries, with pilot production lines targeted for 2026. Beyond batteries, France is advancing safe energy storage solutions. The EMPHASIS and GREENCAP projects reached final stages in late 2025, validating ionic liquid-based supercapacitors with improved thermal stability and safety profiles for aerospace and renewable energy systems. These initiatives underscore France’s role in translating ionic liquid research into deployable energy technologies.

Ionic Liquids Industry: Country-Level Strategic Snapshot

Ionic Liquids Market County Level Snapshot

|

Region

|

Primary Strategic Driver

|

Key Application Focus

|

Structural Direction

|

|

Germany

|

Green transformation and PFAS substitution

|

Battery electrolytes, CO2 capture, building protection

|

Digitalized, biodegradable ionic liquid innovation

|

|

China

|

High-end chemical upgrading and EV scale

|

Electronics, polyamides, battery electrolytes

|

Policy-led scale with industrial integration

|

|

United States

|

Refining safety and resource security

|

Alkylation, rare earths, pharmaceuticals

|

Long-cycle adoption with diversified use cases

|

|

France

|

Battery Passport compliance and energy storage

|

High-purity electrolytes, supercapacitors

|

Electrochemical specialization with regulatory alignment

|

Ionic Liquids Market Report Scope

Ionic Liquids Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$119.9 Million

|

|

Market Size (2034)

|

$269.1 Million

|

|

Market Growth Rate

|

9.4%

|

|

Segments

|

By Type (Ammonium-Based Ionic Liquids, Imidazolium-Based Ionic Liquids, Phosphonium-Based Ionic Liquids, Pyrrolidinium-Based Ionic Liquids, Pyridinium-Based Ionic Liquids, Task-Specific Ionic Liquids), By Application (Process Chemicals, Performance Chemicals, Electrochemistry, Environmental Applications, Biotechnology), By End-Use Industry (Chemical and Petrochemical, Energy Storage and Renewables, Pharmaceuticals and Healthcare, Electronics and Semiconductors, Automotive and Aerospace, Paper and Pulp)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Evonik Industries AG, Merck KGaA, IoLiTec Ionic Liquids Technologies GmbH, Solvionic SA, Proionic GmbH, Tokyo Chemical Industry Co., Ltd., Syensqo, Strem Chemicals, Inc., Tatva Chintan Pharma Chem Pvt. Ltd., Chevron Phillips Chemical Company, The Chemours Company, Reinste Nanoventure, Scionix Ltd., Jinkai Chemical Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ionic Liquids Market Segmentation

By Type

- Ammonium-Based Ionic Liquids

- Imidazolium-Based Ionic Liquids

- Phosphonium-Based Ionic Liquids

- Pyrrolidinium-Based Ionic Liquids

- Pyridinium-Based Ionic Liquids

- Task-Specific Ionic Liquids

By Application

By End-Use Industry

- Chemical and Petrochemical

- Energy Storage and Renewables

- Pharmaceuticals and Healthcare

- Electronics and Semiconductors

- Automotive and Aerospace

- Paper and Pulp

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ionic Liquids Industry

- BASF SE

- Evonik Industries AG

- Merck KGaA

- IoLiTec Ionic Liquids Technologies GmbH

- Solvionic SA

- Proionic GmbH

- Tokyo Chemical Industry Co., Ltd.

- Syensqo

- Strem Chemicals, Inc.

- Tatva Chintan Pharma Chem Pvt. Ltd.

- Chevron Phillips Chemical Company

- The Chemours Company

- Reinste Nanoventure

- Scionix Ltd.

- Jinkai Chemical Co., Ltd.

*- List not Exhaustive