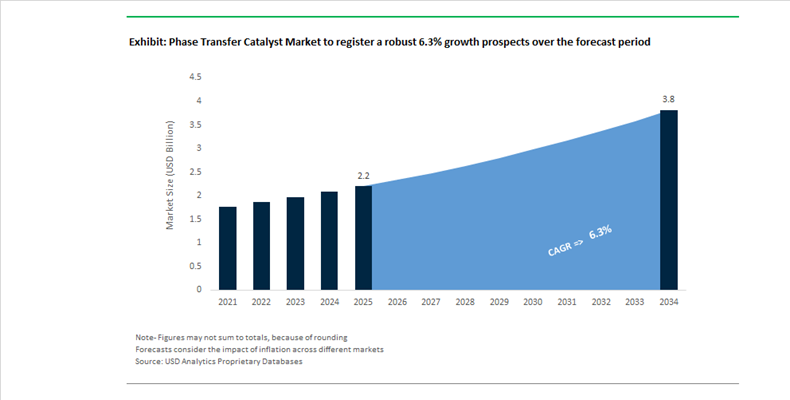

Phase Transfer Catalyst Market Size 2025–2034: $2.2 Billion to $3.8 Billion at 6.3% CAGR Supported by Pharmaceutical Synthesis Innovation and Capacity Expansion in India

The global phase transfer catalyst (PTC) market is projected to grow from $2.2 billion in 2025 to $3.8 billion by 2034, registering a CAGR of 6.3%. Growth is supported by rising demand for quaternary ammonium and phosphonium salts in pharmaceutical intermediates, agrochemical synthesis, polymer modification, and fine chemical production. Phase transfer catalysis remains essential in biphasic reaction systems, enabling efficient transport of reactive ions across immiscible phases while reducing reaction time, energy consumption, and solvent dependency. Increasing emphasis on green chemistry, stereoselective synthesis, and continuous flow manufacturing is reshaping PTC design and application strategies across high-value chemical sectors.

Structural consolidation in quaternary ammonium supply chains accelerated in late 2023 and 2024 when Global Amines Company Pte. Ltd., a joint venture between Wilmar and Clariant, completed acquisition and integration of Clariant’s quats business. Since quaternary ammonium compounds represent the dominant chemical class of commercial PTCs, this consolidation strengthened upstream feedstock control and improved scale efficiencies for catalyst manufacturers. In March 2025, SACHEM agreed to divest its Asia-based operations to NAGASE & CO., LTD., enabling Nagase to expand its regional presence in electronics-grade and pharmaceutical-grade PTC distribution while allowing SACHEM to concentrate on high-purity markets in North America and Europe. These transactions reflect ongoing geographic specialization within the global PTC supply chain.

India is emerging as a central growth engine for phase transfer catalyst manufacturing. In April 2025, the Indian Ministry of Commerce and Industry reported a 69% decadal increase in manufacturing FDI, directly benefiting domestic specialty chemical producers. In January 2026, Tatva Chintan Pharma Chem Limited announced groundbreaking plans for a new facility in Jolva, Dahej, with capital expenditure of ₹250–275 crores. The plant is designed to expand production of quaternary ammonium and phosphonium PTCs serving pharmaceutical and agrochemical intermediates. During its January 2026 earnings call, Tatva Chintan reported ₹279 million in PTC revenue for Q3 FY26, reflecting 13% year-on-year growth driven by steady demand from specialty chemical clients aligned with “Make in India” initiatives.

Technological advancements are redefining catalyst performance benchmarks. In October 2024, researchers from the Phipps Group published findings on a chiral Cinchona-derived catalyst enabling stereoselective hydrogen atom transfer in radical reactions. This breakthrough expands the application of asymmetric phase transfer catalysis in synthesizing single-enantiomer drug intermediates, strengthening PTC relevance in advanced pharmaceutical manufacturing. In February 2024, technical reviews documented progress in carbon-supported heterogeneous PTC systems, enabling aqueous-phase reactions with simplified catalyst recovery. These developments support industry movement toward solvent minimization and recyclable catalyst formats.

Flow chemistry integration is influencing catalyst portfolio design. In October 2025, Evonik introduced its Noblyst® F catalyst series optimized for continuous flow applications. While heterogeneous in nature, the product launch reflects a broader trend of aligning catalyst systems, including phase transfer catalysts, with automated pharmaceutical synthesis platforms. Earlier, in March 2024, Evonik launched Octamax, a sustainable catalyst system for fuel desulfurization featuring advanced regeneration processes. These innovations signal cross-sector emphasis on recyclability and energy-efficient catalytic performance.

Corporate restructuring is reinforcing R&D agility. Throughout 2025 and into early 2026, Evonik implemented its “Tailor Made” efficiency program, reducing administrative layers and eliminating 2,000 roles globally. In February 2026, the company introduced a dynamic dividend policy targeting 40% to 60% of adjusted net income, enhancing financial flexibility for reinvestment in catalytic technologies within its Active Oxygens and Catalysts divisions.

Structural Shift Toward High-Value, Technology-Intensive Phase Transfer Catalysts

Strategic Shift to High-Performance Specialty Catalysts in Pharmaceutical Synthesis

The Phase Transfer Catalyst market is undergoing a decisive move away from commodity ammonium salts toward high-performance, structure-specific catalysts that deliver measurable gains in yield, selectivity, and regulatory compliance. In pharmaceutical and agrochemical synthesis, the tolerance for variability is shrinking, and manufacturers are prioritizing catalysts that support high enantiomeric purity, reproducibility, and simplified downstream purification.

A critical inflection point emerged in late 2024 with the commercialization of chiral phase transfer catalysts derived from Cinchona alkaloids. These systems enable stereoselective hydrogen atom transfer pathways, allowing API manufacturers to synthesize non-racemic intermediates without relying on metal-based chiral complexes. This capability is particularly valuable as regulators increasingly scrutinize trace metal contamination in drug substances.

Yield economics are reinforcing this shift. Comparative reaction studies conducted during 2024–2025 demonstrated that advanced dual-site catalysts such as 4,4'-bis(tributylammoniomethyl)-1,1'-biphenyl dichloride can increase conversion rates from below 1% to over 80% in targeted esterification and alkylation reactions. These step-change efficiency gains significantly reduce catalyst loading, solvent usage, and reaction time, offsetting higher unit prices and improving total cost of ownership for pharmaceutical producers.

Commercially, suppliers are responding with portfolio specialization. SACHEM has introduced its Salego™ PTC range specifically for pharmaceutical biphasic systems, engineered to minimize residual ionic impurities and streamline regulatory filings. This trend signals a broader repositioning of PTCs from low-cost auxiliaries to performance-critical inputs in regulated manufacturing environments.

Integration of PTC Technology into Continuous Flow Manufacturing Platforms

The acceleration of continuous flow chemistry across pharmaceutical production is redefining catalyst design requirements. As manufacturers migrate from batch reactors to microreactors and tubular flow systems, PTCs must operate reliably under narrow residence times, elevated heat transfer rates, and tightly controlled stoichiometry.

Regulatory validation of continuous manufacturing has accelerated adoption. Global pharmaceutical leaders such as Pfizer and Eli Lilly have secured approvals for drugs produced via continuous processes, signaling regulatory acceptance of flow-based production. This transition elevates the importance of thermally stable, predictably soluble PTCs that prevent phase separation or localized hot spots that could trigger runaway reactions.

A parallel innovation stream is emerging around catalyst recovery. Research published in 2025 highlights the development of polymer-bound and immobilized PTCs designed for continuous reuse. These catalysts can be retained within packed-bed reactors, eliminating separation steps and reducing waste generation. Such designs directly address one of the historic limitations of liquid-liquid phase transfer systems, namely catalyst loss and contamination.

Patent activity underscores the strategic direction. Analysis of more than 2,200 patents issued between 2010 and late 2024 shows that roughly 42% focus on heterogeneous catalysis and continuous processing architectures. This signals a long-term commitment to flow-compatible catalytic systems and positions advanced PTCs as foundational components of Industry 4.0 chemical manufacturing.

Enabling Sustainable Chemistry Through CO₂ Utilization and Bio-Based Polymers

Phase transfer catalysts are increasingly central to the chemical industry’s decarbonization agenda. Their ability to facilitate reactions under mild, aqueous, or solvent-reduced conditions makes them well suited for processes that replace fossil-derived feedstocks and toxic intermediates.

A landmark development occurred in October 2025 when Evonik Oxeno, LIKAT, and Ruhr University Bochum announced a catalytic platform enabling the direct conversion of carbon dioxide and green hydrogen into ester intermediates. While bimetallic systems anchor the chemistry, phase-transfer-enabled mechanisms play a critical role in managing biphasic reactivity and eliminating carbon monoxide from the value chain.

In parallel, biopolymer production is emerging as a structurally attractive demand segment. With government-backed expansion of sustainable polymers in markets such as India, PTCs are increasingly used to activate monomers for bio-based polyethylene and polylactic acid under low-energy conditions. Their role in enabling quasi-aqueous reaction environments aligns with global mandates to reduce solvent toxicity and improve atom efficiency.

From an environmental performance perspective, advanced PTC systems are enabling reactions with near-complete atom economy by eliminating auxiliary reagents and hazardous solvents. Green chemistry publications in 2025 highlight multiple C–C coupling reactions where PTC-enabled pathways achieve full material utilization, reinforcing their role as enablers of scalable, sustainable chemical production.

Deployment in Next-Generation Battery Electrolyte and Binder Synthesis

The transition toward high-energy-density lithium-ion batteries and solid-state battery architectures is opening a technically demanding but high-margin opportunity for phase transfer catalysts. Battery materials manufacturing requires anhydrous, metal-free, and highly controlled synthesis routes where PTCs offer clear advantages.

In December 2025, MU Ionic Solutions, a Mitsubishi Chemical affiliate, received the Asia IP Elite award for its proprietary electrolyte licensing strategy. These platforms rely on PTC-assisted synthesis to achieve sub-ppb metal impurity levels, which are essential for long cycle life and thermal stability in advanced cells.

The industry is also moving toward solvent-free and low-solvent polymerization routes for binders and polyether electrolytes. Studies published during 2024–2025 identify long-chain quaternary ammonium salts such as didecyl dimethyl ammonium bromide as effective phase transfer enhancers under aerobic and high-temperature conditions. These properties are critical for battery-grade materials that must withstand aggressive electrochemical environments.

At the materials science level, PTCs are being explored for their role in shaping the solid electrolyte interphase layer. Research indicates that uniform, ion-permeable organic films formed through PTC-mediated reactions can suppress lithium dendrite growth while maintaining ionic conductivity. This positions phase transfer catalysts as indirect but strategically important contributors to battery safety, performance consistency, and long-term reliability.

Taken together, these trends and opportunities confirm that the Phase Transfer Catalyst market is transitioning from a mature, cost-driven segment into a high-value, innovation-led space closely aligned with pharmaceuticals, sustainable chemistry, and energy storage technologies.

Phase Transfer Catalyst Market Competitive Landscape

The Phase Transfer Catalyst (PTC) Market is shifting toward high-purity, green synthesis and continuous flow chemistry, driven by pharmaceutical, semiconductor, and agrochemical demand. Competitive dynamics center on chiral catalysts, ultra-high-purity formulations, and scalable manufacturing, with India emerging as a key hub under China+1 diversification strategies.

Evonik integrates advanced catalysis and renewable manufacturing to lead high-performance PTC innovation

Evonik Industries AG is a global leader in high-performance catalysis, leveraging its Advanced Technologies and Active Oxygens integration to deliver full-stack synthesis solutions. The company reported €1.87 billion EBITDA in 2025 and is prioritizing specialty catalysts under its Next Markets Program. Its Chlorocel™ 909 innovation reflects a focus on reducing side reactions and improving process efficiency, a principle extended to custom PTC formulations. Evonik has transitioned catalyst production to renewable electricity, aligning with pharmaceutical decarbonization targets. Backward integration into hydrogen peroxide and tertiary amines ensures stable feedstock supply. This combination of sustainability, innovation, and supply chain control reinforces its leadership.

Tatva Chintan accelerates global expansion with semiconductor-grade PTCs and high-margin product mix

Tatva Chintan Pharma Chem Ltd. is emerging as a high-growth player in the PTC market, driven by strong financial and operational performance. The company reported a 54.8% YoY revenue increase to ₹133.07 crores in Q3 FY2026, supported by a 298% surge in EBITDA. Its new Jolva facility, commissioned in 2026, eliminates production bottlenecks for pharma and agro intermediates. Tatva is entering the semiconductor chemicals space, targeting ultra-high-purity PTCs for advanced electronics. Currently, PTCs contribute 24% of total revenue, with focus on esterification and amino acid synthesis. This expansion into high-value applications positions Tatva as a key global competitor.

SACHEM focuses on ultra-high-purity PTCs and semiconductor-grade blending capabilities after Asia divestment

SACHEM, Inc. is repositioning as a precision chemistry leader following the divestment of its Asia operations to NAGASE. The company is concentrating on ultra-high-purity catalyst production in North America and Europe, supported by its advanced Austin headquarters and CleanFlex™ facilities. Its Catana™ PTC portfolio enables cost-efficient synthesis by replacing hazardous reagents with inorganic bases, reducing waste by up to 20%. The CleanFlex™ plant achieves impurity levels in the ppt range, meeting stringent semiconductor standards. This focus on high-purity and specialized applications strengthens SACHEM’s niche leadership. Its strategy aligns with growing demand for contamination-free catalyst systems.

TCI expands chiral PTC portfolio to support asymmetric synthesis and sustainable organic chemistry

Tokyo Chemical Industry Co., Ltd. (TCI) plays a critical role in global R&D by supplying a vast portfolio of phase transfer catalysts and linkers. In 2026, the company introduced advanced chiral PTCs designed for asymmetric synthesis and next-generation polymer chemistry. Its expanding catalog includes over 90 linkers and numerous quaternary salts, supporting high-throughput catalyst screening. TCI is also advancing solid-state phase transfer technologies using covalent organic frameworks (COFs). Its products enable greener synthesis by functioning effectively in mixed aqueous-organic systems, reducing reliance on toxic solvents. This focus on innovation and sustainability strengthens its position in research-driven markets.

BASF drives industrial-scale catalyst innovation with AI-driven reactors and 3D-printed catalyst technology

BASF SE is redefining catalyst manufacturing through large-scale industrialization and digital innovation. The company is launching a commercial 3D-printed catalyst plant in Ludwigshafen, utilizing X3D technology to enhance surface area and reaction efficiency. Its AI-driven reactor systems optimize PTC-mediated reactions in real time, improving yield and reducing waste. BASF achieved €1.7 billion in cost savings in 2025 and targets €2.3 billion by 2026 through operational optimization. Its ability to produce up to 10,000 tonnes/year of catalysts ensures unmatched scale. This integration of AI, additive manufacturing, and Verbund efficiency positions BASF as a dominant force in next-generation catalysis.

Phase Transfer Catalyst Market Share and Segmentation Insights

Quaternary Ammonium Salts Lead Phase Transfer Catalyst Demand in Pharmaceutical and Agrochemical Synthesis

Quaternary ammonium salts accounted for 58.60% of the Phase Transfer Catalyst Market by type in 2025, reflecting their widespread use in industrial organic synthesis processes. These catalysts facilitate the transfer of ionic reactants between immiscible phases, significantly improving reaction efficiency in pharmaceutical synthesis, agrochemical manufacturing, and polymer production. Their versatility, cost effectiveness, and availability in diverse structural variants make them the most widely used phase transfer catalysts at industrial scale. In 2025, development of chiral quaternary ammonium phase transfer catalysts is gaining attention in pharmaceutical synthesis, enabling asymmetric reactions that produce single enantiomer drug intermediates with high selectivity and yield in advanced pharmaceutical manufacturing processes.

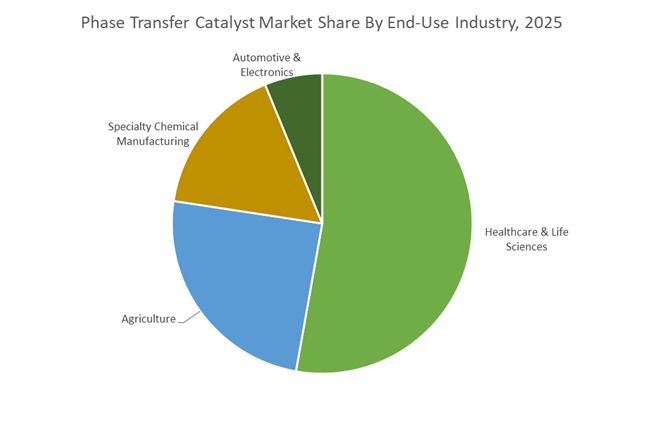

Healthcare and Life Sciences Sector Drives Phase Transfer Catalyst Consumption in API Manufacturing

Healthcare and life sciences represented 52.80% of the Phase Transfer Catalyst Market by end-use industry in 2025, reflecting strong demand from pharmaceutical manufacturing and active pharmaceutical ingredient synthesis. Phase transfer catalysts enable efficient reactions between aqueous and organic phase reactants, improving yield and selectivity in complex chemical synthesis processes used in drug manufacturing. Pharmaceutical companies increasingly rely on specialized catalytic systems to optimize reaction pathways and production efficiency. In 2025, the industry shift toward green chemistry in pharmaceutical production is increasing adoption of phase transfer catalysis because these catalysts allow reactions to proceed under milder conditions with reduced solvent consumption, supporting sustainability objectives in pharmaceutical process development.

India – Domestic Scale-Up Anchored in Pharma, Policy, and Ports

India’s phase transfer catalyst industry is entering a structurally accelerated phase, underpinned by pharmaceutical expansion, fiscal incentives, and export-oriented infrastructure. As per the Ministry of Commerce and Industry in April 2025, India’s pharmaceutical sector is on track to reach USD 130 billion by 2030. This trajectory is directly translating into rising domestic demand for ammonium- and phosphonium-based phase transfer catalysts, which are critical in multi-step API synthesis, heterocyclic chemistry, and fluorination reactions. Local API manufacturers are increasingly favoring in-country PTC sourcing to reduce solvent intensity, shorten reaction cycles, and comply with tightening global impurity thresholds.

Policy support is materially reinforcing this demand shift. The BioE3 Policy (2025) and the expanded Production Linked Incentive scheme now explicitly cover specialty catalysts, positioning PTCs as strategic intermediates rather than commoditized reagents. Foreign direct investment inflows into manufacturing reached USD 165.1 billion in 2025, with a disproportionate share flowing into integrated chemical clusters in Gujarat and Andhra Pradesh where PTC production, API manufacturing, and downstream formulation are co-located. Beyond pharmaceuticals, India is also emerging as an innovation testbed. Between September 2024 and 2025, domestic research groups such as Snehasrusthi Group successfully commercialized PTC-enabled bio-stimulants for agriculture, marking a functional expansion of PTC usage beyond traditional industrial chemistry. Complementing this, the creation of a dedicated Chemical Committee for Ports in 2025 is reducing export lead times for PTC-derived intermediates into APAC markets, while NITI Aayog-backed funding is strengthening industry–CSIR collaboration in chiral phase transfer catalyst development.

China – Regulatory-Driven Substitution and High-End Localization

China’s phase transfer catalyst market is being reshaped by environmental regulation and industrial self-sufficiency mandates rather than pure volume growth. The Draft Environmental Code released in April 2025 represents a watershed moment. By penalizing the continued use of high-polar hazardous solvents such as DMSO and DMF, the code is structurally favoring PTC-enabled biphasic reaction pathways that minimize solvent load and waste generation. This regulatory shift is pushing both fine chemical and pharmaceutical manufacturers to redesign synthesis routes around quaternary ammonium and phosphonium salts.

On the supply side, domestic producers such as Volant-Chem and Shandong Kunda expanded ammonium salt production lines through 2025 to align with Made in China 2025 localization goals. The MIIT 2025–2026 Action Plan reinforces this direction by mandating 5% annual growth in the chemical sector while offering tax rebates for waste-reduction technologies, a category where PTCs are explicitly referenced. Importantly, China is also elevating PTCs into the electronics domain. Semiconductor-grade phase transfer catalysts are being prioritized to support domestic chip fabrication, with policymakers targeting a 90% self-sufficiency ratio in high-purity process chemicals by late 2026. This positions PTCs as part of China’s strategic materials stack rather than auxiliary reagents.

United States – R&D-Led Transition and Portfolio Rationalization

The U.S. phase transfer catalyst landscape is defined by research intensity and regulatory substitution dynamics. According to the State of U.S. Science and Engineering report (2024–2025), national R&D expenditure reached USD 806 billion, with a growing share directed toward sustainable chemical manufacturing. This has accelerated the development of ionic liquid-based and next-generation PTC systems that deliver higher selectivity while enabling compliance with stricter environmental and worker-safety standards.

Market structure is simultaneously tightening. In March 2025, SACHEM Inc. finalized the sale of its Asia operations to NAGASE & CO., allowing it to redeploy capital toward North American and European growth segments. Regulatory pressure is a major driver. Updated TSCA requirements in 2025 have accelerated the replacement of legacy catalysts in specialty polymers and resins with ammonium salt-based PTCs that offer improved toxicological profiles. As a result, PTC adoption in the U.S. is increasingly compliance-driven and innovation-led rather than cost-led.

Japan – Precision Chemistry and Regional Control

Japan’s role in the phase transfer catalyst industry is anchored in precision chemistry and regional distribution control. In late 2025, Tokyo Chemical Industry introduced advanced PTC reagents designed to function efficiently in biphasic systems using low-cost, nonpolar aprotic solvents. These products are strategically positioned to support seamless scale-up from laboratory synthesis to commercial pharmaceutical production, a critical bottleneck in global drug development.

Strategic consolidation has further strengthened Japan’s position. NAGASE & CO.’s acquisition of SACHEM’s Asian business in 2025 has effectively centralized PTC distribution, application support, and technical services for the APAC region within Japan. Concurrently, Japanese firms are aligning with the national SDGs chemical roadmap by developing plant-based organocatalysts, such as D-Galactan-derived systems, as lower-impact alternatives to conventional phase transfer catalysts. This positions Japan at the intersection of green chemistry, high purity, and regional influence.

Germany – Industrial Innovation and Sustainability-Linked Catalysis

Germany’s phase transfer catalyst market is being shaped by industrial innovation and sustainability-led capital deployment. In December 2025, BASF announced a breakthrough in catalyst manufacturing using its X3D® 3D-printing technology. By enabling customized catalyst geometries, this approach improves mass transfer, optimizes reaction kinetics, and reduces pressure drops in industrial reactors, directly enhancing the performance of PTC-enabled processes.

Capacity expansion is reinforcing this technological edge. BASF is constructing a new catalyst production facility in Ludwigshafen, scheduled to begin operations in 2026, with a dedicated focus on high-performance and application-specific catalysts. Parallel to this, Evonik’s 2025 Factbook confirms that more than 80% of its R&D is now aligned with sustainability targets. Alkoxide-based and next-generation phase transfer catalysts are being scaled across its global network, including Singapore and Argentina, positioning Germany as both an innovation nucleus and a standards-setter for sustainable catalysis.

Comparative Snapshot – Phase Transfer Catalyst Industry by Country

Phase Transfer Catalyst Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Strategic Focus

|

Market Character

|

|

India

|

Pharma expansion and policy incentives

|

Localization, chiral PTCs, exports

|

Scale-up driven, policy-supported

|

|

China

|

Environmental regulation and self-sufficiency

|

Solvent substitution, electronics-grade PTCs

|

Regulation-led, localization-focused

|

|

United States

|

R&D intensity and TSCA compliance

|

Ionic liquids, safer ammonium PTCs

|

Innovation- and compliance-driven

|

|

Japan

|

Precision chemistry and regional control

|

High-purity reagents, green organocatalysts

|

Quality-led, APAC hub

|

|

Germany

|

Industrial innovation and sustainability

|

3D-printed catalysts, low-impact PTCs

|

Technology-led, sustainability-centric

|

Phase Transfer Catalyst Market Report Scope

Phase Transfer Catalyst Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.2 Billion

|

|

Market Size (2034)

|

$3.8 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Type (Quaternary Ammonium Salts, Phosphonium Salts, Crown Ethers, Cryptands & Polyethylene Glycols, Ionic Liquids), By Application (Pharmaceutical Synthesis, Agrochemicals, Polymers & Resins, Specialty Chemicals, Waste Management & Water Treatment), By End-Use Industry (Healthcare & Life Sciences, Agriculture, Automotive & Electronics, Specialty Chemical Manufacturing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SACHEM Inc., Evonik Industries AG, BASF SE, Tokyo Chemical Industry Co. Ltd., NAGASE & CO. Ltd., Tatva Chintan Pharma Chem Limited, Sinopec Shanghai Catalysts Co. Ltd., Volant-Chem Corp., Nippon Chemical Industrial Co. Ltd., Pat Impex, Merck KGaA, Eastman Chemical Company, Clariant AG, Solvay SA, W. R. Grace & Co.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Phase Transfer Catalyst Market Segmentation

By Type

- Quaternary Ammonium Salts

- Phosphonium Salts

- Crown Ethers

- Cryptands & Polyethylene Glycols

- Ionic Liquids

By Application

- Pharmaceutical Synthesis

- Agrochemicals

- Polymers & Resins

- Specialty Chemicals

- Waste Management & Water Treatment

By End-Use Industry

- Healthcare & Life Sciences

- Agriculture

- Automotive & Electronics

- Specialty Chemical Manufacturing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Phase Transfer Catalyst Industry

- SACHEM Inc.

- Evonik Industries AG

- BASF SE

- Tokyo Chemical Industry Co. Ltd.

- NAGASE & CO. Ltd.

- Tatva Chintan Pharma Chem Limited

- Sinopec Shanghai Catalysts Co. Ltd.

- Volant-Chem Corp.

- Nippon Chemical Industrial Co. Ltd.

- Pat Impex

- Merck KGaA

- Eastman Chemical Company

- Clariant AG

- Solvay SA

- W. R. Grace & Co.

*- List not Exhaustive