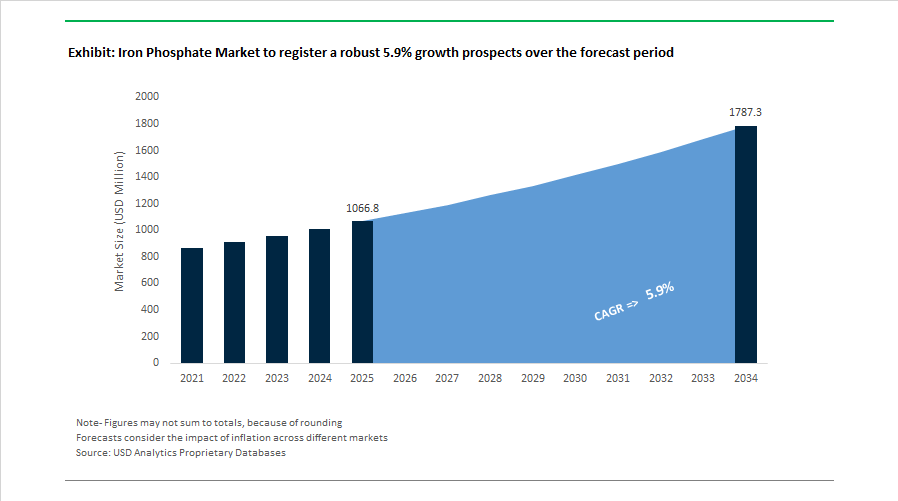

Iron Phosphate Market to Reach $1,787.1 Million by 2034 as LFP Battery Chemistry Anchors Global Energy Storage Expansion

The Iron Phosphate Market is projected to expand from $1,066.8 Million in 2025 to $1,787.1 Million by 2034, reflecting a CAGR of 5.9%. Market momentum is overwhelmingly linked to lithium iron phosphate (LFP) cathode materials, which have transitioned from an entry-level EV chemistry to a dominant platform for grid-scale storage, standard-range electric vehicles, and commercial transport electrification. Structural cost advantages, thermal stability, and supply chain resilience have positioned iron phosphate as a strategic material in the global battery ecosystem.

Upstream integration and localization strategies accelerated in 2024–2025. In December 2024, Saudi Arabian Mining Company (Ma’aden) completed the acquisition of Mosaic’s stake in the Waad Al Shamal Phosphate Company, consolidating its position as a major phosphate producer capable of supporting battery-grade derivatives. In January 2025, ICL formed a €285 million joint venture with Shenzhen Dynanonic to establish LFP cathode active material production in Spain, leveraging ICL’s specialty phosphate capabilities to supply Europe’s emerging gigafactory cluster. That same month, LG Energy Solution signed a multi-year agreement to supply LFP pouch cells to a North American automaker for electric trucks and SUVs, signaling the normalization of iron-based chemistries in Western automotive platforms. By March 2025, SVOLT finalized plans for its second European gigafactory in Spain, dedicated to high-volume LFP and LMFP production.

Technological evolution also strengthened iron phosphate’s competitiveness. In May 2025, Gotion High-Tech reported a 15% increase in energy density for its lithium manganese iron phosphate (LMFP) production cells, narrowing the performance gap with nickel-rich chemistries while preserving safety and cost benefits. In November 2025, Saudi Arabia’s Bisha grid-scale storage project deployed 2,618 MWh of LFP cells supplied by BYD, underscoring the chemistry’s dominance in stationary applications. The project required substantial volumes of iron phosphate-based cathode materials, reinforcing demand visibility for producers.

Pricing and profitability dynamics shifted sharply in late 2025 into 2026. Energy-storage-grade LFP material prices nearly doubled from ¥30,000 per ton in mid-2025 to ¥59,000 per ton by early 2026, driven by rising sulfur and ferrous sulfate costs and a rebound from a loss-making cycle in 2024. Hunan Yuneng forecast 2025 net profits of up to 1.4 billion yuan, a year-on-year increase exceeding 135%, reflecting tightened supply conditions. In January 2026, major producers—including Hunan Yuneng, Wanrun New Energy, Defang Nano, and Andatech—announced coordinated maintenance shutdowns representing roughly half of total market share, strategically moderating capacity after sustained 100% utilization.

Outside China, governments are reinforcing alternative supply chains. In January 2026, Canada approved funding for Arianne Phosphate’s purified phosphoric acid development, aligned with G7 critical minerals initiatives to support non-Chinese LFP ecosystems. Meanwhile, the European Union introduced a directive mandating a 20% increase in phosphorus recovery from wastewater sludge, strengthening circular sourcing pathways for industrial iron phosphate. Benchmark Mineral Intelligence further institutionalized the market in February 2026 by launching CIF North America and Europe price assessments for 314Ah LFP cells, improving transparency as global utility-scale storage deployment accelerates.

Key Trends and Strategic Opportunities in the Iron Phosphate Market

Global Capacity Race for Battery-Grade Lithium Iron Phosphate (LFP) Precursors

The iron phosphate market is undergoing a structural transformation as Lithium Iron Phosphate chemistry becomes the default choice for mass-market electric vehicles and stationary energy storage. Automotive OEMs such as Tesla, Ford, and BYD have accelerated LFP adoption to reduce battery cost volatility, enhance thermal safety, and extend cycle life. This downstream shift has triggered an unprecedented upstream investment cycle focused on battery-grade iron phosphate and ferric phosphate intermediates.

In December 2025, the U.S. Department of Energy and multiple state-level agencies disclosed more than USD 12 billion in cumulative planned investments for domestic cathode and precursor manufacturing through 2027. These projects are directly linked to Inflation Reduction Act incentives that reward FEOC-compliant supply chains, forcing U.S. and European battery ecosystems to localize iron and phosphorus sourcing rather than rely on Chinese imports. For decision makers, this marks iron phosphate’s elevation from a commodity chemical to a strategically protected battery material.

Vertical integration is emerging as a competitive necessity. Chemical producers and battery developers are commissioning dedicated ferric phosphate lines engineered to achieve ultra-high purity levels approaching 99.9999%. In the U.S., partnerships such as the Kore Power–ICL Group collaboration illustrate how cathode manufacturers are locking in closed-loop access to iron and phosphate feedstocks, insulating LFP economics from the price shocks historically associated with nickel and cobalt markets.

Technology evolution is reinforcing this trend. LFP platforms are rapidly transitioning toward Lithium Manganese Iron Phosphate, where manganese doping lifts energy density toward 230 Wh/kg. This narrows the performance gap with high-nickel chemistries while preserving iron phosphate’s inherent safety and cost advantages, sustaining long-term demand for high-purity iron phosphate inputs.

Compliance-Driven Adoption in High-Performance Animal Nutrition

Beyond batteries, regulatory pressure in animal nutrition is reshaping demand for iron phosphate as a functional feed additive. Following the EU-wide ban on pharmacological zinc oxide in June 2022, iron phosphate has emerged as a compliant alternative for maintaining gut health in weaned piglets without contributing to heavy-metal accumulation in soil and groundwater.

Data referenced by the European Food Safety Authority show that historical zinc oxide usage increased zinc loading in pig slurry by close to 30%. Replacing medicinal zinc with high-purity ferric phosphate blends has become a standard compliance pathway for European producers, particularly in regions subject to stringent nitrate and heavy-metal discharge limits.

From a productivity perspective, iron phosphate is no longer viewed solely as a micronutrient. Precision-dosed iron-based mineral systems are increasingly formulated to stabilize intestinal microflora. Industry trials cited in 2024–2025 demonstrate feed conversion ratio improvements of 3 to 5% versus legacy diets, translating directly into margin protection for commercial swine operations under rising feed cost pressures.

Transition to Non-Toxic Iron Phosphate Conversion Coatings

One of the most commercially attractive growth avenues for iron phosphate lies in surface treatment and corrosion protection. Regulatory action under REACH in Europe and parallel U.S. EPA initiatives are accelerating the elimination of hexavalent chromium from metal pretreatment processes, creating strong pull for iron phosphate conversion coatings in automotive and aerospace manufacturing.

Iron phosphate coatings form an insoluble, tightly adherent crystalline layer that enhances paint adhesion and corrosion resistance. In automotive e-coat and powder coating lines, these systems now routinely achieve salt-spray resistance beyond 1,000 hours, meeting OEM durability specifications while avoiding the toxicity and waste management burden associated with zinc or chromium systems.

Operational economics further strengthen adoption. Iron phosphate pretreatment can be implemented as a single-stage clean-and-coat process, reducing energy consumption by an estimated 15 to 20% and sharply lowering hazardous sludge generation. For Tier-1 suppliers facing ESG-linked procurement audits, this combination of regulatory compliance and cost efficiency positions iron phosphate as a preferred long-term technology.

Circular Economy Integration Through Phosphorus Recovery

Phosphorus scarcity and geopolitical concentration of rock phosphate reserves are opening a strategic opportunity for iron phosphate derived from secondary sources. Wastewater treatment plants are increasingly recovering phosphorus in the form of vivianite, a naturally occurring iron phosphate mineral, from anaerobic digestion systems.

By 2025, pilot installations in the Netherlands and Germany demonstrated vivianite recovery rates of 60 to 80% of total influent phosphorus using magnetic separation technologies. This recovered material represents a local, low-carbon feedstock suitable for fertilizer applications and, with further refinement, for industrial iron phosphate production.

Recovered iron phosphate is also enabling the development of controlled-release fertilizers, where iron-phosphate and struvite blends limit nutrient runoff and reduce eutrophication risks. These engineered products align closely with Clean Water Act objectives in the United States and similar nutrient-loading regulations in Europe, creating a regulatory-supported market for circular iron phosphate solutions that link wastewater management, agriculture, and industrial materials supply.

Iron Phosphate Market Share and Segmentation Insights

Iron Phosphate (FePO₄) Leads the Market as a Critical Precursor for Lithium Iron Phosphate Battery Cathodes

Iron phosphate (FePO₄) accounted for 52.80% of the Iron Phosphate Market share in 2025, making it the dominant product type due to its strategic role in the rapidly expanding lithium iron phosphate (LFP) battery industry. Iron phosphate serves as the primary precursor for LFP cathode materials used in lithium-ion batteries, which are widely adopted in electric vehicles, stationary energy storage systems, and power electronics applications. LFP battery chemistry offers several advantages including enhanced thermal stability, long cycle life, improved safety, and lower production costs compared with nickel-manganese-cobalt (NMC) cathodes, making it increasingly attractive for automotive and grid-scale storage applications. In 2025, the global transition toward LFP-based electric vehicle batteries, particularly in China and increasingly in Europe and North America, has significantly increased demand for battery-grade iron phosphate. Manufacturers producing cathode precursor materials now require strict control of particle morphology, chemical purity, and consistency, as these properties directly influence battery performance, charging stability, and energy density.

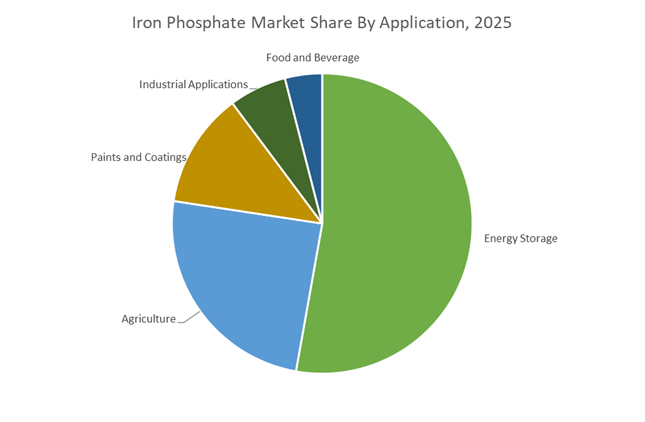

Energy Storage Applications Drive the Largest Demand for Iron Phosphate

Energy storage accounted for 52.80% of the Iron Phosphate Market share in 2025, establishing it as the dominant application segment for iron phosphate materials. Iron phosphate is a key precursor used in manufacturing lithium iron phosphate cathodes for lithium-ion batteries, which are widely deployed in electric vehicles, stationary battery storage systems, renewable energy integration, and backup power infrastructure. The global expansion of electric mobility and renewable energy systems has significantly increased demand for battery chemistries that offer long operational lifetimes, high thermal stability, and reduced reliance on expensive metals such as cobalt and nickel. LFP batteries meet these requirements, making them a preferred choice for many automotive manufacturers producing entry-level and mid-range electric vehicles. In 2025, the growth of utility-scale grid energy storage and distributed battery storage systems has further accelerated iron phosphate consumption. Large-scale battery installations supporting solar and wind energy integration rely heavily on LFP technology because of its excellent cycle durability and enhanced safety characteristics, creating sustained demand for iron phosphate beyond the automotive battery supply chain.

Competitive Landscape in Iron Phosphate Market

BASF SE Integrates Battery-Grade and Food-Grade Iron Phosphate Capabilities

BASF SE leverages its integrated Verbund model to serve both battery materials and high-purity nutrition applications within the iron phosphate value chain. In late 2025, BASF entered a long-term strategic partnership with a leading Chinese battery manufacturer to co-develop ultra-high-purity iron phosphate precursors, targeting a 15% reduction in cathode manufacturing costs for lithium iron phosphate batteries. The company’s 2026 Group EBITDA guidance of €6.2 billion to €7.0 billion reflects continued earnings growth from its Nutrition and Care segment, particularly specialty mineral salts. BASF supplies low heavy-metal iron phosphates for infant formula, clinical nutrition, and pharmaceutical use, meeting stringent impurity thresholds. Under its Winning Ways strategy, the company aims to achieve a €2.3 billion annual cost reduction run rate by the end of 2026, reallocating capital toward sustainable energy materials and advanced cathode precursor production.

Budenheim Strengthens Ultra-Pure Iron Phosphate for Early Life Nutrition

Chemische Fabrik Budenheim KG is a leading specialty phosphate producer focused on high-purity mineral salts for sensitive nutrition markets. Its expanded 5,000 square meter House of Nutrition facility in Germany added 4,400 tonnes of annual production capacity for iron, magnesium, and calcium phosphates. A €57 million investment in ultra-pure production lines has introduced HEPA-filtered cleanroom environments and advanced particle engineering processes that improve dispersibility and bioavailability. Budenheim targets the Early Life and Medical Nutrition segments, where iron phosphate serves as a taste-neutral fortificant in infant cereals, clinical meal replacements, and fortified beverages. Participation in Food Ingredients China and Vitafoods Europe in 2026 underscores its strategy to capture growth in APAC and EMEA markets driven by rising demand for clean-label mineral fortification.

ICL Group Builds European LFP Cathode Production Platform

ICL Group has repositioned its iron phosphate strategy toward lithium iron phosphate battery materials, capitalizing on its upstream phosphate integration. In early 2026, the company formalized a joint venture with Shenzhen Dynanonic to establish LFP cathode production in Europe, with an initial investment of approximately €285 million. The facility at ICL’s Sallent, Spain site is being repurposed from a former potash operation to anchor large-scale LFP manufacturing within the European Union. ICL’s 2026 EBITDA target of $1.4 billion to $1.6 billion reflects its emphasis on specialty growth engines, including battery materials and food-grade acid integration. As the only global specialty minerals company with significant upstream phosphate control actively transitioning into battery materials in the Western hemisphere, ICL is positioned to support Europe’s automotive electrification strategy.

Innophos Expands Clean-Label and Bioavailable Iron Phosphate Solutions

Innophos Holdings focuses on functional mineral solutions aligned with clean-label and bioavailability demands in health and nutrition markets. In 2025 and 2026, the company introduced VersaCal Bright, a calcium and iron phosphate-based whitening alternative designed to replace titanium dioxide in food applications facing regulatory scrutiny. Its Chelamax Technology supports iron and magnesium mineral salts through a patented three-step validation process that confirms full chelation and optimized absorption for dietary supplements. In February 2026, Innophos announced participation at the Nutri Ingredients Summit in Brazil, promoting high-purity iron phosphates tailored to metabolic health and GLP-1 support formulations. Expansion through its São Paulo hub strengthens its Latin American footprint in bakery, beverage, and fortified nutrition sectors.

Shenzhen Dynanonic Scales Nano-Lithium Iron Phosphate Leadership

Shenzhen Dynanonic is a top-tier global supplier of nano-sized lithium iron phosphate and its precursors, scaling annual capacity to over 265,000 tons by 2026 from just 500 tons a decade earlier. The company remains among the top three global LFP cathode material suppliers, serving major electric vehicle battery manufacturers. Its proprietary liquid-phase synthesis technology enables consistent nano-scale iron phosphate precursor production with optimized particle size distribution and enhanced energy density performance. In 2025, Dynanonic achieved a 30% cost advantage compared to nickel-based cathode chemistries, accelerating LFP adoption in mass-market electric vehicles. The European joint venture with ICL in Spain marks its first major manufacturing expansion outside China, strengthening supply chain proximity to European automotive OEMs and reinforcing global competitiveness in battery-grade iron phosphate materials.

China Iron Phosphate Market: Policy-Led Scale, Supply Discipline, and Energy Storage Pull

China remains the global center of gravity for iron phosphate and LFP precursor manufacturing, with growth shaped by coordinated industrial policy, automotive demand cycles, and emerging supply-side discipline. Under the 2025–2026 National Non-ferrous Metals Strategy, the Ministry of Industry and Information Technology mandated the upgrading of high-end chemical products, explicitly prioritizing high-purity iron phosphate for next-generation batteries and stationary energy storage. This policy backdrop translated into record operational intensity during 2025. Domestic output of LFP precursors reached a monthly peak of 355,800 tons in September 2025, while cumulative year-to-date production climbed to 2.51 million tons, reflecting a 66% year-on-year increase driven by strong domestic EV sales and grid-scale storage deployments.

By early 2026, market behavior shifted toward stabilization. Leading producers such as Hunan Yuneng, Defang Nano, and Wanrun New Energy coordinated one-month maintenance shutdowns, temporarily removing an estimated 28,000 to 65,000 tons of supply. This marked a notable move toward supply discipline in response to overcapacity pressures. On the demand side, energy storage bid-winning volumes surged to 272 GWh by late 2025, a 191% increase, structurally favoring iron phosphate chemistries for large-format, long-life battery systems. Strategic downstream integration also intensified. Contemporary Amperex Technology Co., Limited issued a 500 million yuan advance payment to Jiangxi Shenghua, a subsidiary of Fulin Jinggong, to lock in high-compaction cathode capacity targeting 500,000 tons for the 2026 cycle. Environmental governance is tightening in parallel, with 2026 SAMR directives requiring a 1.5% annual efficiency gain in co-occurring mineral recovery during phosphate smelting, reinforcing the shift toward cleaner, higher-yield iron phosphate production.

United States Iron Phosphate Market: Strategic Reshoring and Policy-Driven Integration

The United States iron phosphate industry is being reshaped by national security priorities, federal funding, and clean energy legislation aimed at building a domestic LFP supply chain. In March 2025, the invocation of the Defense Production Act through an executive order on American mineral production granted the Development Finance Corporation authority to fast-track financing for domestic mining and processing projects, including battery-grade iron and phosphate. This was reinforced by more than $19.2 billion in federal financing approved or under review during 2025 for North American mineral projects, with the Department of Defense allocating $883.7 million across 20 initiatives to strengthen the energy transition supply base.

Operational proof points began to emerge by late 2025. First Phosphate Corp. successfully produced commercial-grade LFP 18650 cells using entirely North American-sourced critical minerals, achieving 2,000-cycle life with 80% capacity retention. This milestone validated the technical feasibility of a non-Asian iron phosphate supply chain. The Inflation Reduction Act is amplifying this momentum, with 2026 domestic-content tax credit tiers accelerating investments in localized iron phosphate cathode production. Beyond batteries, iron phosphate demand is diversifying. The U.S. Department of Agriculture announced $30.8 million in research funding in mid-2025 to advance iron phosphate as a low-toxicity molluscicide, expanding its role in organic agriculture and reinforcing demand stability outside the energy sector.

South Korea Iron Phosphate Market: Automotive Alignment and Recycling Depth

South Korea’s iron phosphate trajectory is tightly linked to its automotive OEM ecosystem and a strategic pivot toward LFP chemistries. SK On confirmed plans to begin mass production of LFP batteries by mid-2026, targeting supply agreements with Ford, Volkswagen, and Hyundai. This announcement catalyzed parallel alignment from LG Energy Solution and Samsung SDI, both of which have adjusted 2026 roadmaps to include domestic LFP output.

Upstream infrastructure is developing in tandem. L&F fully commissioned its LFP cathode pilot lines in January 2025 and is preparing for full-scale production in 2026 under the Ministry of Trade, Industry and Energy’s national LFP technology program. Recycling is emerging as a structural pillar. Qingyan New Material invested 60 million yuan into a cathode recycling facility designed to process 9,000 metric tons annually by late 2025, supporting circular supply of iron phosphate materials and mitigating raw material volatility.

European Union Iron Phosphate Market: Strategic Autonomy and Circular Phosphorus

In the European Union, iron phosphate development is being shaped by strategic autonomy objectives and regulatory clarity across chemicals, fertilizers, and green finance. In July 2025, the European Commission launched the Critical Chemicals Alliance to map strategic molecules and production assets, explicitly targeting white phosphorus and iron-based intermediates critical to renewable energy and battery applications. This initiative reflects a broader effort to reduce reliance on external suppliers for phosphorus value chains.

Regulatory refinements are reinforcing market structure. Updated guidance under the Fertilising Products Regulation issued in December 2025 clarified product function categories for iron phosphate-based fertilizers, directly influencing labeling, compliance, and cross-border trade from 2026 onward. At the same time, the expansion of EU taxonomy criteria for green finance is tightening requirements for phosphorus recovery. Public consultations closing in December 2025 proposed an 80% recovery mandate from wastewater and sewage sludge incineration ash to qualify for sustainable investment status, positioning recycled iron phosphate streams as strategically attractive inputs for both agriculture and energy storage.

Iron Phosphate Industry: Country-Level Strategic Snapshot

Iron Phosphate Market County Level Snapshot

|

Region

|

Primary Policy Driver

|

Core Demand Anchor

|

Structural Direction

|

|

China

|

MIIT high-end materials strategy and SAMR efficiency mandates

|

EV batteries and grid-scale energy storage

|

Large-scale production with emerging supply discipline

|

|

United States

|

DPA, IRA, and federal critical minerals funding

|

Domestic LFP batteries and agriculture

|

Reshoring and vertically integrated supply chains

|

|

South Korea

|

Automotive OEM alignment and national LFP programs

|

Passenger EVs and recycling

|

OEM-linked scale-up with circular material flows

|

|

European Union

|

Critical Chemicals Alliance and green finance taxonomy

|

Energy storage and fertilizers

|

Strategic autonomy with high recovery standards

|

Iron Phosphate Market Report Scope

Iron Phosphate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1066.8 Million

|

|

Market Size (2034)

|

$1787.1 Million

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Type (Iron Phosphate, Ferric Phosphate, Ferrous Phosphate), By Product Grade (Battery Grade, Food and Pharmaceutical Grade, Agricultural Grade, Industrial Grade), By Application (Energy Storage, Agriculture, Paints and Coatings, Food and Beverage, Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hunan Yuneng New Energy Battery Material Co., Ltd., Shenzhen Dynanonic Co., Ltd., Hubei Wanrun New Energy Technology Co., Ltd., BYD Company Ltd., Contemporary Amperex Technology Co., Limited, W. R. Grace & Co., Budenheim, First Phosphate Corp., L&F Co., Ltd., SK On Co., Ltd., Gotion High-Tech Co., Ltd., Prayon S.A., ICL Group Ltd., Compass Minerals International, Inc., A123 Systems LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Iron Phosphate Market Segmentation

By Type

- Iron Phosphate

- Ferric Phosphate

- Ferrous Phosphate

By Product Grade

- Battery Grade

- Food and Pharmaceutical Grade

- Agricultural Grade

- Industrial Grade

By Application

- Energy Storage

- Agriculture

- Paints and Coatings

- Food and Beverage

- Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Iron Phosphate Industry

- Hunan Yuneng New Energy Battery Material Co., Ltd.

- Shenzhen Dynanonic Co., Ltd.

- Hubei Wanrun New Energy Technology Co., Ltd.

- BYD Company Ltd.

- Contemporary Amperex Technology Co., Limited

- W. R. Grace & Co.

- Budenheim

- First Phosphate Corp.

- L&F Co., Ltd.

- SK On Co., Ltd.

- Gotion High-Tech Co., Ltd.

- Prayon S.A.

- ICL Group Ltd.

- Compass Minerals International, Inc.

- A123 Systems LLC

*- List not Exhaustive