Isophthalic Acid Market to Reach $4.8 Billion by 2034 as Recycling Mandates and Specialty Resins Reshape Global Trade Flows

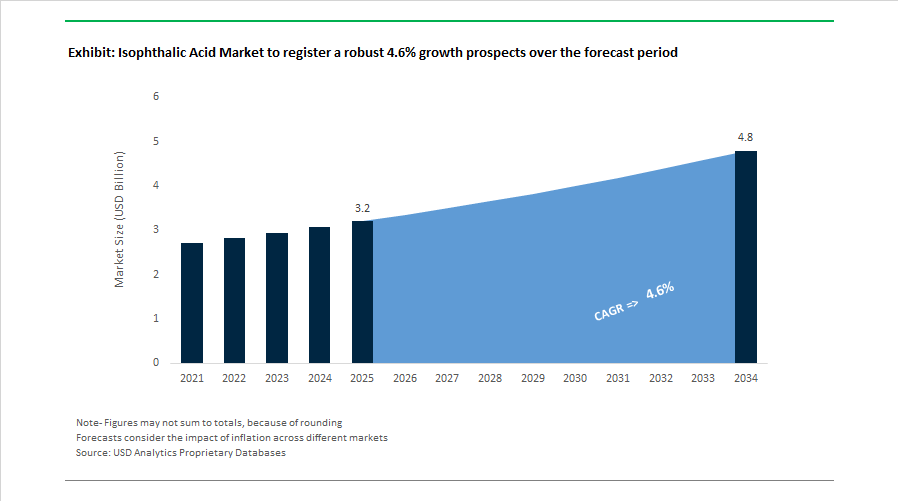

The Isophthalic Acid (PIA) Market is projected to expand from $3.2 billion in 2025 to $4.8 billion by 2034, reflecting a CAGR of 4.6%. Market dynamics are being reshaped by regulatory pressure on recycled PET (rPET), regional production rationalization, and a strategic shift by major producers toward higher-value specialty polyester applications. Isophthalic acid remains a critical comonomer in PET copolymers, coatings, and engineering plastics, where it enhances clarity, chemical resistance, heat stability, and mechanical toughness.

A structural turning point emerged in early 2026 when industry confirmations indicated that the United States would cease domestic PIA production entirely. Following multiple plant closures driven by unsustainable profitability and elevated operating costs, North America has transitioned to a fully import-dependent model. Downstream PET resin and coatings manufacturers are now sourcing primarily from South Korea and China, where producers benefit from integrated paraxylene feedstocks and scale advantages. This development increases trade exposure and pricing sensitivity for U.S. converters, while strengthening Asia-Pacific’s dominance in global supply.

In contrast, Asia has expanded capacity and strategic positioning. Between 2022 and 2024, Sinopec and Mitsubishi Gas Chemical (MGC) collectively added more than 180,000 metric tons of PIA capacity to serve packaging growth across the region. In November 2025, MGC signed a long-term agreement to procure 1 million tons per year of ultra-low-carbon methanol under its Carbopath™ initiative, aiming to decarbonize feedstock streams used in purified isophthalic acid production at its Mizushima facility. Meanwhile, Indorama Ventures launched its “IVL 2.0” transformation strategy in March 2025, optimizing its Combined PET and PIA assets through asset-light restructuring and operational discipline after a prolonged market downturn. In December 2025, Indorama ranked first globally in ChemScore 2025, reinforcing its ESG leadership within the purified isophthalic acid value chain.

Regulation is a central growth catalyst. Effective January 1, 2025, the European Union mandated that PET beverage bottles contain at least 25% recycled content. Incorporating recycled feedstock often compromises polymer performance; high-purity isophthalic acid is therefore increasingly used to restore clarity, barrier integrity, and mechanical strength in rPET blends. This has elevated demand for specialty-grade PIA capable of meeting strict food-contact and optical standards.

Producers are also pivoting toward differentiated applications. In October 2025, Indorama introduced the deja™ Care fiber platform, utilizing isophthalic acid-modified polyesters for hygiene and soft-skin textiles. In February 2026, Lotte Chemical announced a strategic restructuring toward high-performance specialty materials, expanding its “Super EP” engineering plastics portfolio and completing its Yulchon compounding plant in 2026 to serve electronics and automotive sectors. Concurrently, specialty manufacturer Arvee Laboratories commercialized a lower-carbon 5-hydroxyisophthalic acid (5-HIA) process, achieving a 15% emissions reduction for advanced polymer applications in medical devices and energy storage.

Structural Trends and High-Impact Opportunities in the Isophthalic Acid (IPA) Market

Strategic Capacity Investment Driven by PETG and High-IPA Copolyester Packaging Demand

The Isophthalic Acid market is experiencing a structurally driven demand upswing as packaging producers pivot away from conventional PET toward IPA-rich copolyesters such as PETG. This shift is directly linked to premiumization trends in cosmetics, personal care, and beverages, where brand owners are prioritizing glass-like clarity, chemical resistance, and shatterproof performance without compromising recyclability. Unlike standard PET, IPA-modified resins deliver higher impact strength and design flexibility, enabling thicker-walled containers that elevate shelf aesthetics while remaining compatible with existing PET recycling infrastructure.

In early 2025, Eastman Chemical and SK Chemicals finalized capacity expansions targeting medical-grade and luxury packaging applications, responding to a documented 15–20% surge in PETG demand. These investments underscore IPA’s rising strategic importance as a molecular stabilizer that enhances clarity and durability in high-value packaging formats. For decision makers, this signals a long-term volume shift toward specialty-grade IPA rather than commoditized polyester intermediates.

Regulatory pressure in Europe is reinforcing this trajectory. Under the EU Single-Use Plastics Directive, beverage bottles are required to contain at least 25% recycled content by 2025, increasing to 30% by 2030. IPA plays a critical role in stabilizing the molecular weight of recycled PET, enabling closed-loop rPET bottles to retain transparency and impact resistance across multiple recycling cycles. As brand owners push for food-grade rPET at scale, IPA demand is becoming structurally embedded in circular packaging strategies rather than discretionary polymer upgrades.

Feedstock-Linked Supply Chain Volatility in the Meta-Xylene and Aromatics Complex

Despite strong downstream demand, IPA producers continue to face margin pressure due to structural volatility in the aromatics value chain. Isophthalic acid production depends on meta-xylene, a minor but essential isomer within the mixed xylenes pool. Because global refineries prioritize paraxylene for PTA and polyester fiber markets, IPA manufacturers are often exposed to feedstock tightening during periods of strong PX demand.

In late 2025, the U.S. Energy Information Administration highlighted that while Brent crude prices were projected to moderate toward USD 62 per barrel, aromatics pricing remained elevated. This divergence is driven by persistent demand for high-octane gasoline blending components, which competes directly with chemical-grade xylene supply. As a result, meta-xylene prices have remained structurally high, forcing IPA producers to implement dynamic pricing mechanisms to offset 15–20% year-on-year feedstock fluctuations.

To mitigate this exposure, regional players are accelerating backward integration. In India and China, companies such as Deepak Nitrite are investing in integrated aromatics complexes designed to co-produce meta-xylene and IPA. By 2026, these facilities aim to internalize feedstock supply, reduce reliance on merchant markets, and improve margin resilience. For procurement and strategy leaders, this trend highlights a widening competitiveness gap between integrated producers and standalone IPA manufacturers.

IPA-Based Polyester Polyols for Premium and Weatherable Coatings

A high-margin opportunity is emerging for isophthalic acid in polyester polyols used in industrial, automotive, and architectural coatings. The aromatic structure of IPA-based polyols provides superior resistance to UV radiation, hydrolysis, and chemical attack compared to adipic acid-based alternatives, making them increasingly indispensable in demanding environments.

Performance validation studies conducted during 2024–2025 show that IPA-based polyurethane coatings deliver approximately 35% higher gloss retention and significantly improved salt-spray resistance. These attributes are driving adoption in coastal infrastructure, heavy machinery, and long-life automotive components where maintenance cycles and corrosion risks directly affect lifecycle costs.

The global transition toward zero-VOC powder coatings is amplifying this opportunity. IPA’s high glass transition temperature prevents powder agglomeration during storage and transport, enabling smoother application and thinner coating layers. As industrial finishers seek to reduce material consumption while meeting stricter emissions regulations, IPA-based polyols are becoming the backbone of next-generation powder coating formulations.

High-Temperature Amorphous Polyamides for 5G and Electric Vehicle Platforms

Isophthalic acid is also gaining strategic importance in amorphous polyamides such as PA 6I/6T, which are increasingly replacing metals and glass in high-temperature, high-precision applications. These materials offer exceptional dimensional stability, transparency, and heat resistance, aligning with the needs of next-generation electronics and electric vehicles.

By late 2025, the rapid expansion of 5G infrastructure and AI-enabled consumer electronics had driven strong demand for transparent polyamides used in internal optical components and SMT connectors. These resins retain structural integrity at lead-free soldering temperatures above 260°C, a performance threshold that conventional engineering plastics struggle to meet.

In the automotive sector, OEMs are specifying IPA-based amorphous polyamides for coolant reservoirs and fluid management systems in electric vehicles. Unlike semi-crystalline nylons, these materials maintain permanent transparency, enabling visual fluid inspection while offering long-term resistance to aggressive coolants and thermal cycling. As EV architectures continue to consolidate components and extend service lifetimes, IPA’s role in advanced polymer systems is becoming increasingly entrenched across high-growth end-use industries.

Isophthalic Acid Market Share and Segmentation Insights

Industrial Grade Isophthalic Acid Dominates Due to Cost-Effective Resin Manufacturing for Large-Scale Applications

Industrial grade isophthalic acid accounted for 58.60% of the Isophthalic Acid Market share in 2025, making it the most widely used purity grade across industrial polymer and resin production. Industrial grade material is extensively utilized in unsaturated polyester resins (UPR), polyethylene terephthalate (PET) modification, coatings, and composite materials, where high-volume production prioritizes cost efficiency while maintaining adequate chemical purity. In unsaturated polyester resin manufacturing, isophthalic acid improves chemical resistance, mechanical strength, and thermal stability, making it a preferred monomer in fiberglass reinforced plastics used in construction and marine structures. Industrial grade isophthalic acid also plays a critical role in PET copolymer modification, where it enhances clarity, toughness, and resistance to stress cracking in plastic packaging materials. In 2025, resin producers increasingly utilize optimized intermediate-purity isophthalic acid grades designed specifically for PET bottle resin modification. These grades balance production costs with controlled impurity levels, ensuring stable polymerization performance and improved processing characteristics in high-speed bottle manufacturing operations.

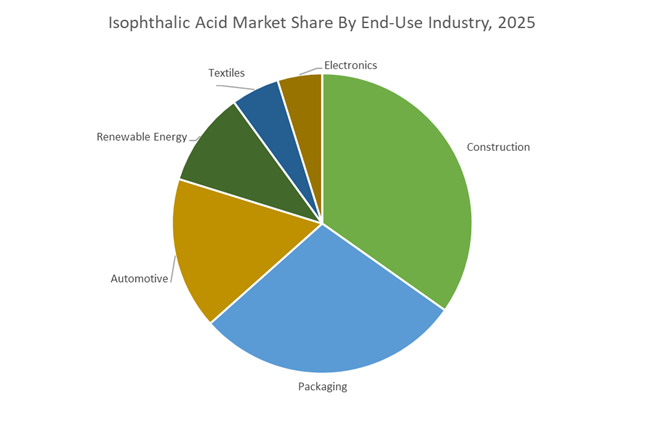

Construction Industry Drives the Largest Demand for Isophthalic Acid-Based Resins

Construction accounted for 34.80% of the Isophthalic Acid Market share in 2025, establishing it as the largest end-use sector for isophthalic acid derivatives. Isophthalic acid is a key feedstock for producing isophthalic polyester resins, which are widely used in fiberglass reinforced composites for structural and infrastructure applications. These resins provide superior corrosion resistance, durability, and chemical stability, making them ideal for demanding environments such as water and wastewater systems, marine structures, industrial tanks, pipes, and building panels. In construction materials, isophthalic polyester resins are commonly reinforced with glass fibers to produce composite pipes, storage tanks, grating systems, and structural profiles capable of withstanding harsh environmental exposure. In 2025, global infrastructure investment and urban development are accelerating demand for high-performance composite construction materials, particularly in water treatment infrastructure and industrial facilities. Aging infrastructure across North America and Europe is also driving rehabilitation and replacement projects, increasing adoption of corrosion-resistant composite materials based on isophthalic resin chemistry for long-term structural reliability.

Competitive Landscape in Isophthalic Acid Market

Indorama Ventures Expands North American PTA and PIA Integration

Indorama Ventures Public Company Ltd. remains a dominant player in the global PET and isophthalic acid value chain, leveraging vertical integration across aromatics, PTA, and polyester resins. The Corpus Christi Polymers joint venture with Alpek and FENC is targeting commercial start-up during 2025–2026, adding approximately 1.3 million metric tons of PTA and PIA capacity to North America. This expansion strengthens regional feedstock security and reduces reliance on imports. Indorama’s recycling roadmap targets 750,000 tons per year of rPET capacity by mid-decade, influencing demand for high-purity PIA modifiers that maintain mechanical strength and clarity in recycled packaging. Under its IVL 2.0 strategy, the company is focusing on deleveraging and asset debottlenecking across Europe and the United States to increase throughput in specialty packaging resins. Annual capital expenditure guidance of $0.8 billion to $1.0 billion reflects commitment to scale optimization and specialty integration.

Lotte Chemical Leads Global PIA Capacity and Process Efficiency

Lotte Chemical Corporation operates the world’s largest single-site PIA production footprint, with annual capacity of approximately 520,000 tons. As a major exporter to Europe and North America, the company plays a central role in global PET and unsaturated polyester resin supply chains. In 2025–2026, Lotte introduced Korea’s first PIA-added semi-nonflammable insulation material, achieving a 30% reduction in fire spread and smoke generation to meet stricter safety standards. Through AI-driven digital R&D, Lotte has improved oxidation reactor yields by 10% while reducing energy consumption by roughly 18%, enhancing margin resilience. The proposed joint venture in Vietnam announced in late 2025 signals expansion into Southeast Asia to serve growing packaging, textile, and construction resin demand.

Mitsubishi Gas Chemical Focuses on High-Purity Specialty PIA

Mitsubishi Gas Chemical positions itself as a high-purity PIA supplier for advanced electronics, optical polymers, and semiconductor packaging materials. Under its Medium-Term Management Plan 2026, the company is emphasizing quality-driven growth within its high-performance products division. In February 2026, MGC discontinued construction at its Netherlands specialty chemicals site, consolidating production toward high-efficiency Asian hubs to preserve capital discipline. Its portfolio includes OPE derivatives and ultra-pure PIA grades critical for optical clarity and dimensional stability in electronic components. Sustainability initiatives include collaboration with Panasonic to develop eco-friendly urea resins utilizing CO2-derived methanol, targeting emissions reductions of 20 to 30% compared to conventional synthesis pathways.

INEOS Strengthens Low-Carbon and Circular Polymer Integration

INEOS Group has reinforced its global position in PTA and PIA through acquisition-led expansion and energy-efficient asset upgrades. In February 2026, the company secured a €300 million grant from the French government to enhance energy efficiency and low-carbon precursor production across its petrochemical assets. Project One, its next-generation ethylene facility, is designed to operate at roughly half the carbon footprint of current leading crackers, indirectly strengthening feedstock competitiveness for downstream aromatics and polyester intermediates. Under its Circular Economy Pillar, INEOS is scaling Recycl-IN polymer grades containing up to 70% recycled content, increasing the need for specialty PIA modifiers that preserve resin integrity. Integration of the Oxochimie joint venture enhances its derivative portfolio serving coatings and ink industries.

Perstorp Advances Bio-Based and Coatings-Focused PIA Applications

Perstorp AB, owned by PETRONAS Chemicals Group, concentrates on specialty PIA applications in coatings and emulsifiers. Its Neptem emulsifier range, recognized with the Environmental Pioneer Award in 2025, utilizes PIA to enhance waterborne alkyd performance while lowering volatile organic compound content. The company promotes RE-carbonizing chemicals by incorporating mass-balanced bio-based feedstocks, enabling reduced carbon footprint PIA derivatives for environmentally sensitive markets. At PaintIndia 2026, Perstorp showcased next-generation liquid cooling fluids and high-purity resin precursors targeting automotive OEM and data center thermal management systems. A rightsizing initiative launched in August 2025 supports margin expansion and strengthens its specialty presence in APAC through its Shanghai laboratory platform.

Eastman Chemical Expands High-Purity and Circular PIA Capabilities

Eastman Chemical Company maintains strong positioning in high-purity PIA for food-contact plastics, medical-grade polymers, and advanced polyester fibers. In 2025–2026, Eastman launched a new ultra-high-purity PIA grade engineered for applications requiring superior chemical resistance and regulatory compliance. Its molecular recycling platform at Kingsport, Tennessee utilizes methanolysis to depolymerize waste polyesters into monomers, creating a closed-loop system for PIA-based resins. Eastman remains strategically focused on paints and coatings, where PIA enhances durability, weatherability, and corrosion resistance in automotive and aerospace finishes. Process optimization initiatives have reduced manufacturing waste by approximately 7% while increasing product consistency to 95.5%, strengthening supply reliability for high-specification markets.

United States Isophthalic Acid Market: Capacity Integration and Low-VOC Resin Repositioning

The United States isophthalic acid industry has entered a structurally stronger phase following decisive consolidation and downstream innovation. In 2025, Eastman Chemical Company completed the integration of INVISTA’s isophthalic acid business, an acquisition valued at USD 1.6 billion that effectively streamlined North American production assets and strengthened domestic supply reliability for high-performance copolyesters. This consolidation has reduced operational redundancies while improving feedstock flexibility for paints, coatings, PET modification, and engineering resins. From a cost perspective, the U.S. Energy Information Administration’s 2025–2026 outlook for softer Brent crude pricing has eased pressure on meta-xylene economics, indirectly stabilizing isophthalic acid operating costs and supporting margin normalization across the value chain.

Downstream, U.S. demand is being reshaped by regulatory and performance-driven material selection. Eastman’s early-2025 launch of a PIA-integrated, solvent-free resin platform positions isophthalic acid at the center of architectural coatings designed for green building certifications and low-VOC compliance. Packaging applications are also expanding, as food and beverage manufacturers increasingly specify PIA-modified polymers to prevent flavor scalping and improve heat resistance in multilayer containers. Export momentum remains intact, with shipment volumes rising 7% in H1 2025, supported by infrastructure refurbishment programs in Latin America and Europe. By late 2025, tighter inventory management led to a marginal domestic price firming, reflecting disciplined supply control ahead of anticipated 2026 demand from PET bottle and coatings producers.

India Isophthalic Acid Market: Domestic Integration and Policy-Backed Scale-Up

India’s isophthalic acid market is transitioning from import dependency toward integrated domestic production, supported by coordinated industrial policy. The July 2025 NITI Aayog roadmap for chemical hubs outlines a clear ambition to lift India’s share of the global chemicals value chain to 5–6% by 2030, with aromatic dicarboxylic acids such as PIA identified as strategic intermediates under the Production-Linked Incentive framework. Reliance Industries Limited remains the dominant domestic producer, supplying high-purity grades above 99% for paints, coatings, and polyester applications, while distributors such as Golden Dyechem have locked in forward supply agreements for 2026.

Structural demand growth is being reinforced by India’s textile and polymer modernization programs. Investments in high-performance polyester fibers for technical textiles are driving increased use of PIA derivatives to improve dye uptake, dimensional stability, and export-grade consistency. Under the Aatmanirbhar Bharat initiative, incentives are increasingly targeted at backward integration, encouraging petrochemical players to reduce reliance on imported meta-xylene by co-locating aromatics and isophthalic acid production. The 2025 Opex subsidy scheme for incremental output of critical chemicals further enhances the economics of domestic capacity expansion, directly addressing India’s import bill for aromatic acids while supporting long-term supply security.

China Isophthalic Acid Market: Policy-Directed Upgrading and EV Material Demand

China’s isophthalic acid industry is being shaped by industrial policy and downstream electrification trends rather than pure volume expansion. The Ministry of Industry and Information Technology’s 2025–2026 target of 5% annual growth in chemical sector added value explicitly prioritizes high-end PIA grades, particularly for applications linked to electric vehicles, advanced composites, and emerging 3D printing materials. Following a Lunar New Year production slowdown in early 2025, market balances improved, correcting the oversupply conditions that characterized late 2024 and restoring operational discipline among producers.

On the demand side, EV manufacturing is a critical growth vector. Chinese OEMs are increasing the use of fiberglass-reinforced and chemically stable resins based on isophthalic acid for battery casings and lightweight body panels, where thermal resistance and long-term durability are essential. At the same time, petrochemical clusters in Ningbo and Yanshan are accelerating vertical integration of meta-xylene feedstocks, insulating PIA producers from global aromatics price volatility. This integration strategy is enhancing cost predictability and supporting China’s broader objective of self-sufficiency in high-performance polymer intermediates.

South Korea Isophthalic Acid Market: High-Purity Exports and Technology Differentiation

South Korea’s isophthalic acid market remains export-oriented, with pricing and purity as its main competitive levers. In 2025, export prices from the Busan hub recovered noticeably in the second half of the year as global packaging converters replenished inventories ahead of peak seasonal demand. After volatility earlier in the cycle, FOB prices stabilized in Q2 2025, providing a more predictable environment for contract negotiations with overseas buyers.

Lotte Chemical continues to anchor the market through proprietary in-house PIA production technology, supplying ultra-high-purity grades exceeding 99.9%. These materials are increasingly specified for specialty copolyesters where optical clarity, process consistency, and thermal performance are critical. South Korea’s emphasis on technological differentiation rather than capacity expansion positions it as a premium supplier to global resin and packaging markets.

Spain and European Union Isophthalic Acid Market: Regulatory-Led Resin Reformulation

Across Spain and the wider European Union, regulatory mandates are the primary force reshaping isophthalic acid demand. The EU Packaging and Packaging Waste Regulation, which requires all packaging to be recyclable by 2030, is already influencing 2026 R&D priorities. Resin formulators are increasingly relying on PIA-modified PET to enhance clarity, toughness, and processability in recyclable packaging structures. Parallel single-use plastics rules requiring 25% recycled content in PET bottles by 2025 further elevate the role of isophthalic acid in mitigating brittleness and performance loss in high-recycled-content formulations.

Market pricing in Spain reflected these dynamics in 2025, with isophthalic acid prices rebounding by 1.71% in Q3 as coatings demand recovered and a weaker euro raised import costs. For European buyers, PIA is evolving from a niche modifier into a strategic enabler for compliance-driven packaging and coatings reformulation, particularly as sustainability criteria tighten across the region.

Isophthalic Acid Industry: Country-Level Strategic Summary

Isophthalic Acid Market County Level Snapshot

|

Region

|

Core Strategic Driver

|

Key Industry Focus

|

Structural Impact

|

|

United States

|

Capacity consolidation and green coatings

|

Low-VOC resins, food-safe packaging

|

Supply security and export resilience

|

|

India

|

Policy-backed domestic integration

|

Paints, textiles, polyester fibers

|

Reduced import dependence

|

|

China

|

MIIT-led upgrading and EV demand

|

Battery casings, advanced composites

|

High-end material positioning

|

|

South Korea

|

Technology and purity leadership

|

Specialty copolyesters

|

Premium export orientation

|

|

Spain & EU

|

Packaging sustainability regulation

|

Recyclable and recycled PET

|

Compliance-driven resin innovation

|

Isophthalic Acid Market Report Scope

Isophthalic Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.2 Billion

|

|

Market Size (2034)

|

$4.8 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Purity Grade (High Purity Grade, Industrial Grade, Reagent Grade), By Application (PET Resin Production, Unsaturated Polyester Resins, Alkyd Resins, Surface Coatings, Specialty Polymers, Plasticizers and Lubricants), By End-Use Industry (Packaging, Automotive, Construction, Textiles, Electronics, Renewable Energy)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Lotte Chemical Corporation, Eastman Chemical Company, Indorama Ventures, Mitsubishi Gas Chemical Company, Inc., Formosa Chemicals & Fibre Corp., SABIC, China Petrochemical Corporation, INEOS, Reliance Industries Limited, Perstorp, Hengyi Petrochemical, Mitsubishi Chemical Group, LG Chem, Beijing Yanshan Petrochemical, Shandong Hongxin Chemicals Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Isophthalic Acid Market Segmentation

By Purity Grade

- High Purity Grade

- Industrial Grade

- Reagent Grade

By Application

- PET Resin Production

- Unsaturated Polyester Resins

- Alkyd Resins

- Surface Coatings

- Specialty Polymers

- Plasticizers and Lubricants

By End-Use Industry

- Packaging

- Automotive

- Construction

- Textiles

- Electronics

- Renewable Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Isophthalic Acid Industry

- Lotte Chemical Corporation

- Eastman Chemical Company

- Indorama Ventures

- Mitsubishi Gas Chemical Company, Inc.

- Formosa Chemicals & Fibre Corp.

- SABIC

- China Petrochemical Corporation

- INEOS

- Reliance Industries Limited

- Perstorp

- Hengyi Petrochemical

- Mitsubishi Chemical Group

- LG Chem

- Beijing Yanshan Petrochemical

- Shandong Hongxin Chemicals Co., Ltd.

*- List not Exhaustive