Liquid Floor Coatings Market Size, High-Durability Flooring Demand, and Industrial Application Outlook

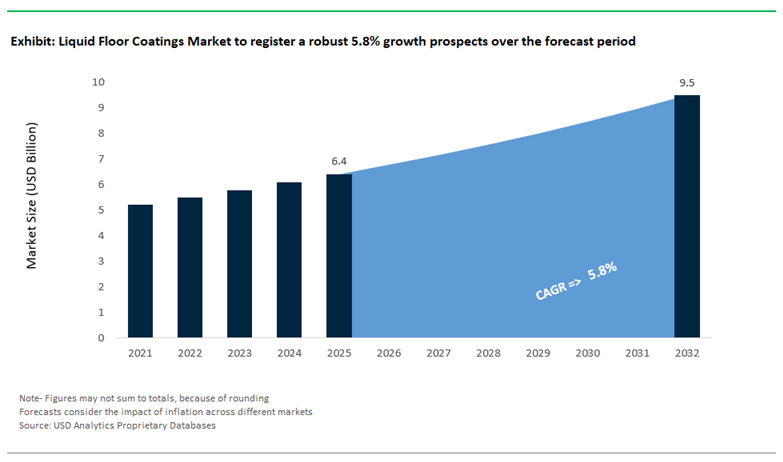

The global liquid floor coatings market was valued at $6.4 billion in 2025 and is projected to reach $9.5 billion by 2032, expanding at a CAGR of 5.8%. This growth is driven by increasing demand for epoxy floor coatings, polyurethane (PU) floor coatings, self-leveling floor coatings, and liquid-applied industrial flooring systems across commercial, industrial, and residential sectors. These coatings are widely adopted for their seamless finish, chemical resistance, abrasion resistance, and ease of maintenance, making them critical in warehouses, manufacturing plants, healthcare facilities, retail spaces, and infrastructure projects.

A key growth driver is the rising need for high-performance flooring solutions capable of withstanding heavy mechanical loads, chemical exposure, and high foot traffic. Industries such as logistics, pharmaceuticals, food processing, and automotive manufacturing are increasingly deploying liquid floor coatings to ensure operational efficiency, hygiene compliance, and long-term durability. Additionally, the shift toward rapid-curing and fast return-to-service coatings is gaining traction, enabling minimal downtime in commercial environments.

Sustainability and innovation are also reshaping the market. The adoption of low-VOC, waterborne, and environmentally friendly floor coatings is accelerating due to stringent regulations and corporate sustainability targets. Advanced technologies such as flowable hydraulic cement underlayments (FHCU), polymer-modified coatings, and high-elasticity systems are improving adhesion, flexibility, and performance under dynamic stress conditions. Regionally, the Middle East and Asia-Pacific are emerging as key growth markets due to large-scale infrastructure projects, while North America and Europe continue to lead in high-performance industrial flooring technologies and innovation.

Market Analysis: Strategic Acquisitions, Rapid-Cure Innovations, and Digital Transformation Driving Market Evolution

The liquid floor coatings industry is undergoing significant transformation driven by strategic expansion, material innovation, and increasing focus on high-performance applications. In March 2026, Master Builders Solutions completed the acquisition of Arkaz Al Sharq Building Materials, significantly strengthening its presence in Saudi Arabia’s construction chemicals and liquid flooring market. This move directly targets the region’s Vision 2030 giga-projects, highlighting the growing demand for advanced liquid-applied flooring systems in large-scale infrastructure developments.

Material innovation is playing a central role in enhancing coating performance. In February 2026, BASF introduced Basonat® HI 3100, a next-generation aliphatic polyisocyanate designed to improve chemical resistance and curing speed in epoxy and polyurethane floor coatings. This development addresses the increasing demand for high-durability industrial flooring solutions capable of operating in aggressive environments. BASF further strengthened its portfolio with the Butonal® NX 4190 polymer dispersion, launched in February 2025, which enhances elasticity and mechanical durability in flooring systems exposed to heavy stress.

Operational efficiency and digitalization are also reshaping market strategies. Sika AG announced a major digital transformation investment in February 2026, targeting automation across its liquid flooring supply chain, with expected savings of CHF 80 million by late 2026. This reflects a broader industry trend toward streamlined production, supply chain optimization, and improved delivery timelines for large-scale projects.

Product innovation is increasingly focused on application efficiency and reduced downtime. In January 2026, PPG Industries showcased rapid-return-to-service liquid flooring coatings, enabling foot traffic in under four hours, a significant advantage for commercial interiors and retail environments. Similarly, Sherwin-Williams launched its Pro-Series High-Performance floor coatings in March 2025, designed for contractor-driven applications with high-build formulations that reduce the number of coating layers required in warehouse and industrial settings.

Sustainability is becoming a defining competitive factor. Bona reported a 46% reduction in Scope 1 and 2 emissions in July 2025, alongside a strategic shift toward waterborne, low-VOC floor coatings, aligning with global environmental regulations. BASF also advanced the market by rebranding its self-leveling systems to Flowable Hydraulic Cement Underlayment (FHCU) in September 2025, supported by new Acronal® primer technologies that improve adhesion and performance of modern flooring systems.

Strategic portfolio realignment is further influencing market dynamics. PPG Industries’ October 2024 divestment of its North American architectural coatings business reflects a focused shift toward high-performance industrial and commercial floor coatings, reinforcing the trend of specialization within the industry.

Market Trend: Cold Storage Infrastructure Transition to Fast-Curing Polyaspartic Floor Coatings

The liquid floor coatings market is experiencing a structural shift in cold storage and logistics infrastructure, where polyaspartic aliphatic polyurea coatings are rapidly replacing conventional epoxy flooring systems. This transition is primarily driven by the operational need to minimize downtime in temperature-sensitive environments such as refrigerated warehouses and frozen food distribution centers. Polyaspartic coatings demonstrate the capability to cure at temperatures as low as -30°C, eliminating the constraints associated with epoxy systems that require controlled ambient conditions for proper curing.

From a productivity standpoint, polyaspartic floor coatings significantly reduce facility downtime. These systems achieve full cure for foot traffic within 1 to 2 hours, compared to the 24 to 72-hour curing cycles required for traditional industrial epoxy coatings. This translates into approximately 95% faster return-to-service timelines, which is critical in high-throughput logistics environments where downtime directly impacts supply chain efficiency. In addition, the superior flexibility of polyaspartic coatings, estimated at 98% to 100% higher than epoxy systems, allows them to withstand severe thermal contraction and expansion cycles typical of cold storage operations without cracking or delamination.

Durability and lifecycle performance further reinforce the adoption of polyaspartics. These coatings are engineered for service lives exceeding 20 years, compared to the 5 to 7-year replacement cycles commonly associated with epoxy flooring in high-traffic industrial settings. The extended lifecycle reduces maintenance frequency and long-term capital expenditure. Moreover, polyaspartic systems offer a broad application temperature window, eliminating the need for facility pre-heating or thawing during installation. This capability reduces energy consumption associated with maintenance operations by approximately 30%, aligning with sustainability goals and cost optimization strategies across cold chain logistics operators.

Market Trend: Antimicrobial Epoxy Floor Coatings with Silver-Ion Technology Reshaping Healthcare Hygiene Standards

Healthcare infrastructure is increasingly adopting antimicrobial liquid floor coatings incorporating silver-ion (Ag+) technology to address the persistent challenge of Healthcare-Associated Infections (HAIs). These advanced epoxy coatings function as a continuous, non-leaching antimicrobial barrier that actively inhibits microbial growth on floor surfaces, positioning them as a critical component of infection prevention strategies in hospitals and clinical environments.

Silver-ion infused coatings have demonstrated high efficacy in pathogen reduction, achieving up to 99.99% elimination of common bacteria such as E. coli and Staphylococcus within minutes of contact. This level of performance is particularly significant in high-risk zones such as intensive care units, surgical suites, and isolation wards. Unlike conventional disinfectants that rely on periodic manual application, antimicrobial floor coatings provide continuous 24/7 protection throughout their operational lifespan, typically ranging between 10 to 15 years. This persistent efficacy ensures a baseline level of hygiene independent of human intervention.

The ability of these coatings to mitigate biofilm formation further enhances their value proposition. Clinical studies indicate that antimicrobial flooring can reduce microbial reservoirs on surfaces by up to 73%, directly supporting infection control protocols. This is particularly relevant given that approximately 48% of healthcare staff may miss standard cleaning cycles, creating gaps in sanitation coverage. Silver-ion coatings act as an autonomous layer of defense, maintaining hygienic conditions between cleaning intervals. As healthcare systems prioritize patient safety, regulatory compliance, and operational efficiency, antimicrobial liquid floor coatings are emerging as a standard specification in modern hospital design and renovation projects.

Market Opportunity: FDA Sanitary Design Regulations Driving Demand for Seamless, Chemical-Resistant Industrial Floor Coatings

The evolving regulatory framework for food processing environments is creating significant growth opportunities for advanced liquid floor coatings. The U.S. Food and Drug Administration’s revised sanitary design guidelines for 2026 emphasize the elimination of microbial harborage points, driving demand for seamless, non-porous flooring systems that comply with HACCP and GMP standards. This regulatory shift is accelerating the adoption of high-performance polyurethane and epoxy coatings designed for hygienic processing environments.

A key requirement under the updated guidelines is the implementation of seamless flooring systems with integrated coving that extends up vertical surfaces. This design eliminates joints and grout lines, which are known to harbor up to 80% of bacteria in wet processing areas. As a result, manufacturers are increasingly specifying monolithic flooring solutions that enhance cleanability and reduce contamination risks. Additionally, thermal shock resistance has become a critical performance parameter, particularly in washdown zones where floors are exposed to rapid temperature fluctuations between 0°C and 82°C. Polyurethane mortar systems, with compressive strengths exceeding 6,000 PSI, are emerging as the preferred solution due to their ability to maintain structural integrity under extreme conditions.

Chemical resistance requirements are also intensifying, with coatings expected to withstand exposure to a wide pH range from 1 to 14. This ensures durability against aggressive cleaning agents, disinfectants, and organic acids commonly used in food processing. Furthermore, updated safety protocols mandate slip resistance ratings of R12 or R13 in wet environments, prompting the adoption of textured, aggregate-filled coatings that balance safety with hygiene. These regulatory developments are driving innovation and specification upgrades across the food and beverage industry, creating a robust demand pipeline for compliant liquid floor coating solutions.

Liquid Floor Coatings Market Share and Segmentation Insights

Self-Leveling Epoxy and Polyurethane Systems Capture 42% Share in Cleanroom and Industrial Flooring

The liquid floor coatings market by system type is dominated by self-leveling coatings, which account for 42% of the global market share in 2025, driven by their superior performance in seamless industrial flooring applications. These coatings—primarily epoxy, polyurethane, and MMA-based self-leveling systems—create joint-free, monolithic surfaces that are critical for food processing plants, pharmaceutical manufacturing units, and electronics cleanrooms, where hygiene and contamination control are paramount. Their ability to eliminate cracks and joints prevents the accumulation of bacteria, dust, and chemicals, making them the preferred choice for regulated environments. Additionally, self-leveling coatings offer significant labor efficiency advantages, as their flowable formulations reduce the need for manual troweling and multi-layer applications. This results in faster installation, reduced labor costs, and consistent surface finish, strengthening their position as the leading system type in high-performance flooring solutions.

Professional Flooring Contractors Hold 58% Share Due to Technical Expertise and Warranty Requirements

In the liquid floor coatings market by sales channel, professional flooring contractors dominate with a 58% market share in 2025, reflecting the technical complexity of coating application and the critical role of skilled execution. Liquid floor coatings require precise substrate preparation techniques such as moisture testing, shot blasting, and diamond grinding, along with accurate mixing ratios and strict environmental controls for temperature and humidity. These factors make professional expertise indispensable for ensuring optimal coating adhesion and durability. Furthermore, industrial clients demand long-term performance warranties ranging from 5 to 15 years, covering issues such as delamination, blistering, and chemical resistance, which only certified contractors can provide. This integration of product supply with professional installation services reinforces the dominance of contractors, making them the primary channel for delivering high-performance industrial flooring systems across manufacturing, logistics, and commercial sectors.

Competitive Landscape in the Liquid Floor Coatings Market

AkzoNobel drives sustainable innovation and strategic consolidation in liquid floor coatings

AkzoNobel continues to anchor the European liquid floor coatings market through its “Paint the Future” strategy, combining advanced decorative and protective technologies. The company reported €10.16 billion in revenue in 2025 and is pursuing an all-stock merger with Axalta to strengthen its global coatings leadership. Its recent “Rhythm of Blues 2026” Color of the Year collection reflects the integration of aesthetic flooring design with high-performance liquid chemistry for commercial interiors. AkzoNobel is heavily investing in Scope 3 emissions reduction and bio-attributed raw materials through collaborations with BASF and Arkema, replacing conventional petroleum-based resins. The divestment of its Pakistan operations in April 2026 highlights a strategic focus on higher-growth industrial and aerospace coatings segments.

PPG Industries expands automated coating systems and sustainable product innovation

PPG Industries maintains a strong position in high-performance liquid floor coatings by emphasizing automation and sustainability. The company has achieved over 3,000 installations of its MoonWalk® automated mixing system, now being adapted for precision in industrial floor coatings. Its $380 million investment in a new manufacturing facility, alongside a color innovation center in Tianjin, supports expansion into the Asia-Pacific region, which holds a 36% market share. PPG’s sustainability leadership is reinforced by its recognition on Barron’s 100 Most Sustainable U.S. Companies list for 2024 and 2025. The launch of PPG Enviroluxe™ Plus, incorporating recycled plastic content in hybrid powder-liquid systems, targets green building and environmentally compliant flooring solutions.

Sherwin-Williams strengthens global dominance through acquisitions and contractor-focused systems

The Sherwin-Williams Company leads the global coatings industry, driven by its extensive retail and contractor network. Its acquisition of Brazilian coatings leader Suvinil significantly enhances its footprint in South America, expanding liquid floor coating production and distribution. The company’s “Success by Design” strategy focuses on high-build epoxy and polyurethane systems, widely used in residential repaint and industrial flooring applications. Sherwin-Williams continues to leverage vertical integration to maintain cost control and supply reliability. Despite forecasting modest growth in 2026, the company is prioritizing operational efficiency and mitigating raw material cost volatility, ensuring resilience in a competitive and price-sensitive market environment.

Sika AG advances construction-driven liquid flooring with digital and sustainability initiatives

Sika AG remains a dominant force in construction-oriented liquid floor coatings, reporting CHF 11.20 billion in 2025 revenue while maintaining a strong 19.2% EBITDA margin. Its focus on high-traffic industrial flooring and integration with advanced repair technologies such as EHLA strengthens its position in infrastructure applications. The “Fast Forward” program launched in late 2025 is accelerating digital transformation and optimizing production across China and EMEA regions. Sika’s innovation pipeline includes MasterAtlas™ R3, a sustainable returned concrete initiative that integrates waste management into floor coating production. The company’s strong performance in the Middle East and Africa, particularly in infrastructure projects, underscores its ability to capitalize on large-scale construction and urban development trends.

RPM International (Stonhard) dominates high-performance industrial flooring systems

RPM International, through its Stonhard subsidiary, leads the premium industrial flooring segment with specialized liquid-applied systems designed for durability and hygiene. Its flagship products, Stonclad epoxy and Stonshield textured urethane, are widely used in food processing environments requiring high chemical resistance. Operating in over 25 countries, RPM’s “single-source” model integrates manufacturing and installation services, offering end-to-end solutions for industrial clients. The company is expanding into lifecycle services with its Stonkleen sustainable cleaning solutions, enhancing long-term floor maintenance. Additionally, its high-build mortar systems incorporate antimicrobial additives directly into the coating matrix, addressing stringent hygiene standards in healthcare and post-pandemic facility management environments.

BASF drives chemical innovation and regulatory-compliant floor coating solutions

BASF plays a pivotal role in the liquid floor coatings market by bridging raw material supply and finished coating systems through its Master Builders Solutions portfolio. In 2026, the company introduced Basonat® HI 3100, an advanced aliphatic polyisocyanate designed for high-durability industrial coatings. BASF is also leading regulatory innovation with the introduction of PFAS-free additives, aligning with global environmental and safety mandates. Its shift toward Flowable Hydraulic Cement Underlayment (FHCU), supported by Acronal® polymer dispersions, is redefining application efficiency and surface performance. The inauguration of a new MBT Construction Chemicals manufacturing facility in 2025 enhances regional supply chain resilience, enabling BASF to meet rising demand for sustainable and high-performance liquid flooring systems.

Japan’s Building Standards Law Revision Accelerating Demand for Slip-Resistant and Low-VOC Floor Coatings

Regulatory reforms in Japan’s construction sector are unlocking new growth avenues for liquid floor coatings, particularly in the context of safety and sustainability. The 2025/2026 revision of Japan’s Building Standards Law introduces stricter requirements for slip resistance in public and commercial spaces, alongside broader mandates aligned with national carbon neutrality targets. These changes are driving increased adoption of high-performance resin-based floor coatings in both new construction and renovation projects.

A central component of the revised law is the enforcement of higher Coefficient of Slip Resistance (CSR) values for flooring in areas exposed to moisture, such as building entrances, corridors, and transit hubs. This requirement is particularly significant given Japan’s aging population, where slip-and-fall incidents represent a major safety concern. As a result, developers and facility owners are prioritizing advanced liquid coatings that deliver consistent slip resistance without compromising durability or aesthetics.

The regulatory update is also triggering a wave of renovation activity. The removal of special exemptions for smaller wooden commercial structures is compelling thousands of buildings to upgrade their flooring systems to meet compliance standards. This is expected to drive substantial demand for fast-curing, slip-resistant coatings capable of minimizing disruption during retrofitting projects. In parallel, the integration of low-VOC and bio-based resin technologies is gaining traction as part of Japan’s Carbon Neutrality 2050 initiative. These environmentally compliant coatings contribute to improved building energy ratings and align with green construction practices.

Infrastructure resilience is another key driver, with increased specification of advanced coatings in urban transit systems and commercial hubs across cities such as Tokyo and Osaka. The convergence of safety mandates, sustainability goals, and large-scale renovation requirements is positioning liquid floor coatings as a critical material segment within Japan’s evolving construction and infrastructure landscape.

China Liquid Floor Coatings Market: Industrial Expansion and Sustainable Manufacturing Driving Demand

China dominates the global liquid floor coatings market, fueled by rapid industrialization, large-scale urban infrastructure projects, and aggressive environmental policies. As the largest producer and consumer, the country is leveraging initiatives such as the “14th Five-Year Plan for Energy-Saving and Environmental Protection”, which mandates a significant reduction in VOC emissions from industrial coatings. This regulatory push is accelerating the adoption of waterborne epoxy and polyurethane (PU) floor coatings, especially across electronics manufacturing and cleanroom environments.

The demand for self-leveling liquid floor coatings is surging in mega infrastructure developments, particularly in the Greater Bay Area, where precision flooring is critical for automated guided vehicles (AGVs). Additionally, China’s smart manufacturing ecosystem and pharmaceutical sector expansion are driving investments in durable, chemical-resistant floor coatings. Domestic capacity expansion by major players such as Nippon Paint China is further strengthening supply chains to cater to high-end warehousing, automotive, and semiconductor industries requiring ESD (electrostatic dissipative) coatings.

United States Liquid Floor Coatings Market: Innovation in High-Performance and Sustainable Flooring Solutions

The United States liquid floor coatings market is characterized by advanced material innovation, sustainability-driven regulations, and strong infrastructure investments. Regulatory frameworks such as SCAQMD Rule 1113 are compelling manufacturers to develop low-VOC, 100% solids, and water-based coatings, aligning with green building standards and environmental compliance.

Technological advancements in polyaspartic and methyl methacrylate (MMA) liquid coatings, offering ultra-fast curing times of 1–2 hours, are transforming applications in retail, food service, and commercial sectors. The Infrastructure Investment and Jobs Act (IIJA) has further accelerated demand for heavy-duty coatings in transportation and bridge construction. Additionally, product innovations such as antimicrobial floor coatings are gaining traction in healthcare-adjacent environments. The market is also witnessing consolidation, with acquisitions like Sunflower Industrial’s takeover of Desco Floor System, reflecting the growing importance of specialized flooring service providers.

India Liquid Floor Coatings Market: High-Growth Industrialization and Infrastructure Boom

India is emerging as the fastest-growing liquid floor coatings market, driven by large-scale industrialization and government-backed manufacturing initiatives. Programs like “Make in India” are catalyzing the development of electronics and EV manufacturing plants, significantly increasing the demand for high-performance epoxy and polyurethane flooring systems.

Infrastructure projects such as Multi-Modal Logistics Parks (MMLPs) under the Gati Shakti scheme are boosting demand for abrasion-resistant coatings in warehouses and logistics hubs. Regulatory updates to the National Building Code (NBC) are promoting eco-friendly, low-VOC materials, strengthening the adoption of sustainable liquid coatings. Strategic acquisitions, including BirlaNu’s acquisition of Clean Coats and JSW Paints’ stake in Akzo Nobel India, are enhancing domestic manufacturing capabilities. The Food & Beverage sector is also witnessing rapid adoption of seamless, non-porous coatings to comply with FSSAI hygiene standards, further expanding market opportunities.

Germany Liquid Floor Coatings Market: Engineering Excellence and Eco-Innovation Leadership

Germany leads the European liquid floor coatings market through its strong emphasis on engineering precision, durability, and environmental sustainability. The country’s alignment with the EU Green Deal has positioned it as a hub for bio-based and low-emission floor coating technologies, supporting zero-pollution manufacturing goals.

Technological innovations such as self-healing liquid coatings with micro-encapsulated resins are redefining durability standards by automatically repairing micro-cracks. Germany’s automotive OEM sector remains a major consumer, requiring coatings capable of withstanding extreme chemical exposure and mechanical stress. The widespread adoption of UV-cured (laser-cured) coatings enables rapid return-to-service in industrial plants, enhancing operational efficiency. Additionally, significant R&D investments by companies like BASF SE in 100% solids epoxy systems are reducing labor costs and eliminating the need for primers. Advanced solutions such as thermochromic coatings are also gaining traction in chemical processing environments.

UAE Liquid Floor Coatings Market: Smart Cities and Luxury Infrastructure Driving Advanced Coating Demand

The United Arab Emirates (UAE) represents a unique and rapidly evolving liquid floor coatings market, driven by luxury construction, smart city initiatives, and extreme climate requirements. Government programs such as the Dubai 2040 Urban Master Plan are promoting sustainable construction practices, including the adoption of coatings with a high solar reflectance index (SRI) to mitigate urban heat effects.

The demand for decorative metallic epoxy and 3D liquid coatings is particularly strong in high-end hospitality and retail developments. At the same time, advanced technologies such as cool-roof and cool-floor coatings are being deployed in logistics hubs to enhance energy efficiency. Infrastructure projects, including metro expansions and underground parking systems, are boosting the use of liquid-applied waterproofing membranes. Regulatory compliance with the Al Sa’fat green building system is further driving the adoption of low-VOC and sustainable coatings. The expansion of regional manufacturing by global players like Jotun and Hempel is strengthening the UAE’s role as a gateway to the MEA coatings market.

Japan Liquid Floor Coatings Market: High-Tech Precision and Functional Coating Innovations

Japan’s liquid floor coatings market is defined by high-performance materials, precision applications, and advanced functional innovations. The country is pioneering hybrid inorganic-organic coatings that combine polymer flexibility with ceramic hardness, offering superior durability and performance.

In high-tech industries such as robotics and semiconductor manufacturing, vibration-damping liquid coatings are critical for maintaining equipment precision. Japan also shows a strong preference for single-component coating systems, driven by labor shortages and the need for simplified application processes. Sustainability remains a key focus, with increasing adoption of VOC-free aqueous polyurethane dispersions (PUDs) to meet stringent environmental standards set by the JSIA. Ongoing refurbishment of aging infrastructure is further driving demand for moisture-tolerant primers and advanced coating systems. Strict enforcement of the Building Standard Law regarding formaldehyde emissions ensures high safety and quality standards across the market.

Liquid Floor Coatings Market Report Scope

Liquid Floor Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.4 Billion

|

|

Market Size (2032)

|

$9.5 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Resin Type (Epoxy, Polyurethane, Polyaspartic and Polyurea, Acrylic, Methyl Methacrylate, Vinyl Ester, Hybrid Systems), By Technology (Water-borne Coatings, Solvent-borne Coatings, 100% Solids, UV-Curable), By Component Count (One-Component, Two-Component, Three-Component), By System Type (Thin-film Coatings, High-build, Self-leveling Coatings, Broadcast, Floor Primers and Sealers), By End-Use Sector (Industrial, Commercial, Residential, Transportation and Infrastructure), By Functional Property (Anti-Slip, Anti-Static, Chemical and Acid Resistant, Antimicrobial, Thermal Shock Resistant, Decorative and Aesthetic), By Application Environment (Indoor, Outdoor, Cold Storage), By Sales Channel (Direct Sales, Specialty Industrial Distributors, Professional Flooring Contractors, Home Improvement)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., BASF SE, Sika AG, RPM International Inc., Axalta Coating Systems Ltd., Jotun Group, MAPEI S.p.A., Hempel A/S, Asian Paints Limited, Nippon Paint Holdings Co., Ltd., 3M Company, Arkema S.A., Flowcrete Group Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Liquid Floor Coatings Market Segmentation

By Resin Type

- Epoxy

- Polyurethane

- Polyaspartic and Polyurea

- Acrylic

- Methyl Methacrylate

- Vinyl Ester

- Hybrid Systems

By Technology

- Water-borne Coatings

- Solvent-borne Coatings

- 100% Solids

- UV-Curable

By Component Count

- One-Component

- Two-Component

- Three-Component

By System Type

- Thin-film Coatings

- High-build

- Self-leveling Coatings

- Broadcast

- Floor Primers and Sealers

By End-Use Sector

- Industrial

- Commercial

- Residential

- Transportation and Infrastructure

By Functional Property

- Anti-Slip

- Anti-Static

- Chemical and Acid Resistant

- Antimicrobial

- Thermal Shock Resistant

- Decorative and Aesthetic

By Application Environment

- Indoor

- Outdoor

- Cold Storage

By Sales Channel

- Direct Sales

- Specialty Industrial Distributors

- Professional Flooring Contractors

- Home Improvement

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Liquid Floor Coatings Industry

- Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- BASF SE

- Sika AG

- RPM International Inc.

- Axalta Coating Systems Ltd.

- Jotun Group

- MAPEI S.p.A.

- Hempel A/S

- Asian Paints Limited

- Nippon Paint Holdings Co., Ltd.

- 3M Company

- Arkema S.A.

- Flowcrete Group Ltd.

*- List not Exhaustive