Liquid Fluoroelastomers Market 2025–2034: PFAS Supply Realignment, Semiconductor-Grade FFKM Innovation, and EV Battery Sealing Driving $818.4 Million Outlook at 4.8% CAGR

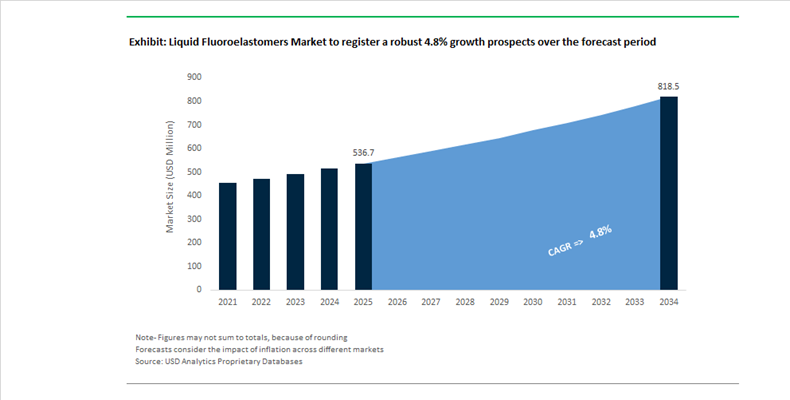

The Liquid Fluoroelastomers Market is projected to grow from $536.7 Million in 2025 to $818.4 Million by 2034, registering a CAGR of 4.8%. Market expansion is being shaped by regulatory-driven PFAS realignment, rising demand for ultra-high-purity perfluoroelastomers in semiconductor fabrication, and accelerating electrification trends requiring chemically resistant sealing systems for lithium-ion batteries and hydrogen fuel cells. Liquid fluoroelastomers, including FKM and FFKM grades, remain critical in extreme-temperature sealing, aggressive chemical processing, plasma etching environments, and advanced automotive fluid systems. However, environmental scrutiny around fluorinated chemistries is restructuring supply chains, raw material sourcing, and R&D investment priorities across the value chain.

In July 2025, AGC launched a surfactant-free AFLAS FFKM series manufactured without fluorinated polymerization solvents, specifically engineered for contamination-sensitive semiconductor manufacturing equipment at advanced nodes. In mid-2025, Syensqo secured multi-year battery-grade supply contracts with global automotive OEMs for Solef PVDF and related fluoroelastomer materials to support EV production hubs in North America and Europe through 2030. In late 2025, Chemours operationalized expanded capacity at its Corpus Christi facility, strengthening infrastructure to scale next-generation Viton liquid coatings and adhesives. At the K 2025 trade fair, Wacker introduced resource-efficient silicone-fluoro hybrid polymers that increasingly compete with traditional liquid fluoroelastomers in medical and food-contact applications by offering comparable chemical resistance with improved sustainability attributes. In November 2025, Shin-Etsu Chemical presented advanced SIFEL liquid fluoroelastomer formulations optimized for liquid injection molding and 3D printing of complex aerospace and electronics gaskets.

Structural supply adjustments intensified in late 2025 and early 2026. As of December 31, 2025, 3M ceased global manufacturing of PFAS and Dyneon fluoroelastomers, triggering significant customer migration toward alternative suppliers. In August 2025, Chemours entered a long-term strategic manufacturing agreement with SRF Limited in India, with operational scaling beginning in early 2026 to stabilize Viton supply without immediate capital expansion. In January 2026, Syensqo divested its Oil and Gas unit to concentrate on high-margin specialty polymers, including liquid fluoroelastomers for EV battery seals and hydrogen fuel cell components. By 2026, Daikin announced cessation of TFA and select fluorinated derivative production at its European facilities, reshuffling precursor availability within the regional supply chain. Concurrently, Kureha’s ¥70 billion PVDF expansion at its Iwaki Factory, reaching commercial operations in 2026, secures critical binder and coating materials frequently integrated with liquid fluoroelastomer systems in lithium-ion battery electrode architectures.

Strategic Trends and High-Value Opportunities Shaping the Liquid Fluoroelastomers Market

Trend: High-Purity Liquid Fluoroelastomer Capacity Expansion for Advanced Semiconductor Fabrication

The liquid fluoroelastomers market is being structurally reshaped by the escalating purity and contamination-control requirements of advanced semiconductor manufacturing. As logic and memory nodes continue to shrink, fabs are demanding elastomeric materials that can withstand aggressive plasma chemistries, high vacuum conditions, and repeated cleaning cycles while exhibiting near-zero outgassing and minimal ionic contamination. This has forced suppliers to move beyond conventional fluoropolymer production and invest in dedicated, cleanroom-certified liquid fluoroelastomer production lines aligned with semiconductor-grade specifications.

A pivotal development occurred in May 2025 when Solvay announced that nearly all of its fluoropolymers, including semiconductor-grade liquid fluoroelastomers, will be manufactured without fluorosurfactants by 2026. This transition is supported by a €40 million investment at its Spinetta Marengo site to implement a technical-zero water treatment system, ensuring zero liquid discharge of PFAS-related emissions. Parallel integration strategies are evident at Daikin, which has vertically integrated raw material purification, polymerization, and final LFT compounding to guarantee purity levels exceeding 99.999%. Industry disclosures from 2024 to 2025 indicate a broader shift toward Class 100 cleanroom processing and packaging, with liquid fluoroelastomers increasingly replacing solid FKM in complex semiconductor geometries due to superior flow behavior and the ability to form contamination-free, molded-in-place gaskets for next-generation fab equipment.

Trend: Low-Temperature and Alternative Curing LFT Systems for Electric Vehicle Battery Sealing

Electric vehicle battery design is introducing new thermal and process constraints that are accelerating innovation in liquid fluoroelastomer curing chemistries. As OEMs transition to larger, high-energy-density battery cells, exposure to elevated curing temperatures during sealing and gasketing is increasingly viewed as a yield and safety risk. In response, LFT formulators are commercializing systems that cure at significantly lower temperatures or through non-thermal mechanisms such as UV activation.

Material innovation was highlighted in June 2025 when Freudenberg Sealing Technologies showcased new elastomeric materials at Battery Show Europe designed to balance vibration resistance, thermal stability, and design flexibility for EV connectors and battery pack interfaces. These developments align with findings from a 2025 MDPI study on fluoroelastomer compatibility with automotive e-fluids, which emphasized the need to maintain mechanical integrity under continuous immersion in PAO and POE fluids at temperatures up to 120 degrees Celsius. Low-temperature curing liquid fluoroelastomers allow OEMs to assemble battery systems without exceeding the safe thermal limits of lithium-ion cells, typically below 100 degrees Celsius. From a manufacturing perspective, OEMs adopting these LFT systems are reporting cycle time reductions of 15 to 25% by eliminating prolonged oven ramp-up and cool-down stages, directly improving throughput and energy efficiency in EV assembly lines.

Opportunity: Liquid Fluoroelastomer Coatings for Green Hydrogen Infrastructure Protection

The rapid scale-up of green hydrogen production, storage, and transport infrastructure is creating a high-value opportunity for liquid fluoroelastomers as protective coating and lining materials. Hydrogen embrittlement and aggressive electrolytic environments pose significant durability challenges for conventional steels and alloys used in pipelines, storage vessels, and electrolyzers. Fluoropolymer-based coatings, including LFT-enabled systems, are increasingly viewed as a viable mitigation strategy.

A 2025 investigative study indexed by PubMed demonstrated that PVDF-graphene nanocomposite coatings can reduce hydrogen permeation by up to 31.6%, validating the broader potential of fluoropolymer chemistries for hydrogen barrier applications. In parallel, surface engineering leaders such as Oerlikon and Impact Coatings are scaling PVD and thermal spray solutions for PEM and alkaline electrolyzers. Liquid fluoroelastomers are being qualified as flexible, chemically resistant binders within these coating systems to enhance durability of bipolar plates and porous transport layers. Infrastructure retrofitting is further expanding addressable demand. The allocation of USD 9 billion in U.S. federal funding for clean hydrogen hubs under the Bipartisan Infrastructure Law is accelerating interest in spray-on LFT linings that enable existing natural gas pipelines and storage assets to be repurposed for hydrogen service without full replacement.

Opportunity: Qualification of Liquid Fluoroelastomers for Single-Use Biopharmaceutical Systems

The transition from stainless steel equipment to single-use systems in biopharmaceutical manufacturing is opening a specialized, regulation-intensive growth segment for liquid fluoroelastomers. In these applications, elastomers are no longer ancillary components but critical materials that directly contact high-value biologics, placing extreme emphasis on extractables, leachables, and biocompatibility.

Liquid fluoroelastomers used in pharmaceutical seals must now comply with USP Class VI, FDA 21 CFR 177.2600, and 3-A Sanitary Standards. Specialty seal manufacturers such as Midwest Gasket Corp highlighted in February 2025 the industry-wide shift toward metal-detectable and ultra-low extractable Viton-based LFT grades to safeguard drug purity. LFTs are particularly well suited for single-use bioreactors and sanitary tri-clamp gaskets due to their ability to mold complex, integrated geometries while withstanding aggressive sterilization simulations, including extraction tests at temperatures up to 121 degrees Celsius. Supply chain strategy is also evolving. In response to past disruptions, biopharma customers are increasingly mandating localized sourcing. During 2025, Sartorius and DuPont expanded regional centers of excellence in North America and Europe, reinforcing a regional-for-regional supply model for high-purity, pharmaceutical-grade liquid fluoroelastomers.

Fluoroelastomers Market Share and Segmentation Insights

Fluorocarbon Elastomers Dominate Liquid Fluoroelastomers Market with High Chemical and Thermal Resistance

Fluorocarbon elastomers (FKM) held 58.60% of the Liquid Fluoroelastomers Market share in 2025, establishing them as the dominant product category used in high-performance sealing and elastomer applications. FKM-based liquid fluoroelastomers are widely valued for their exceptional resistance to fuels, oils, solvents, and aggressive chemicals, along with superior thermal stability and long-term durability under extreme operating conditions. These properties make fluorocarbon elastomers essential for manufacturing automotive seals, gaskets, O-rings, fuel system components, and industrial sealing systems where exposure to high temperatures and chemically aggressive fluids is common. The ability of FKM materials to maintain mechanical integrity, elasticity, and sealing performance in demanding environments supports their broad adoption across automotive, oil and gas, aerospace, and industrial processing industries. In 2025, significant innovation has focused on low-temperature FKM formulations, enabling improved flexibility and elasticity in cold environments while preserving the high-temperature resistance that defines fluorocarbon elastomers. These advancements support expanded use in automotive powertrain systems, aerospace sealing components, and high-altitude operating environments where conventional elastomers may become brittle.

Automotive Industry Leads Liquid Fluoroelastomer Consumption Driven by Advanced Powertrain Sealing

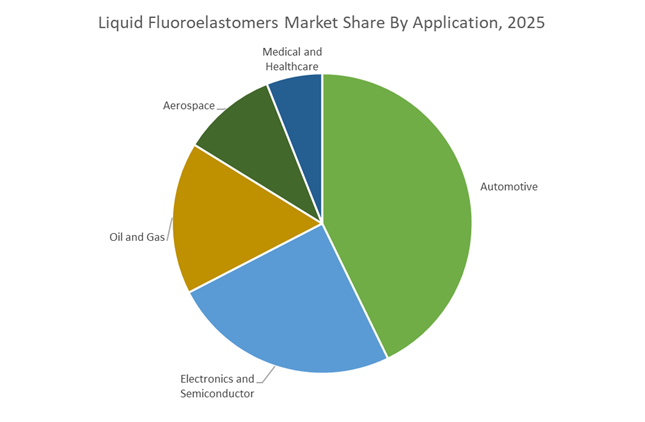

Automotive applications accounted for 42.80% of the Liquid Fluoroelastomers Market share in 2025, making the sector the largest consumer of high-performance fluoroelastomer sealing materials. Liquid fluoroelastomers are extensively used in fuel system seals, engine gaskets, transmission components, turbocharger hoses, and high-performance O-ring sealing systems, where durability under high temperature, pressure, and chemical exposure is essential. Modern automotive systems increasingly rely on advanced elastomer materials that resist degradation from fuels, lubricants, and aggressive additives, ensuring long-term reliability and reduced maintenance in demanding operating conditions. In 2025, the rapid global transition toward electric vehicles (EVs) and electrified powertrains has introduced new application opportunities for liquid fluoroelastomers. EV platforms require reliable sealing solutions for battery cooling systems, thermal management circuits, electric motor housings, and power electronics modules where exposure to advanced coolants and elevated operating temperatures can compromise conventional elastomers. As EV production scales globally, liquid fluoroelastomers are increasingly specified for high-performance automotive sealing systems designed for next-generation electric mobility platforms.

Liquid Fluoroelastomers Market Competitive Landscape

The liquid fluoroelastomers (FKM/FFKM) market in 2026 is driven by PFAS-free polymerization, liquid injection molding (LIM), and ultra-high-purity materials for EV and semiconductor applications. Competition centers on non-surfactant synthesis, circular fluoropolymer recovery, and high-performance sealing solutions for 800V architectures and sub-2nm fabrication environments.

Daikin leads PFAS capture and next-gen fluoroelastomer manufacturing for EV and semiconductor markets

Daikin Industries is setting the benchmark in sustainable liquid fluoroelastomer production through its Green Transformation strategy, achieving commercialization of PFAS-reduced manufacturing technologies in 2026. Its investment of over $300 million in advanced capture systems targeting 99.9% PFAS recovery positions it ahead of tightening global regulations. By combining surface modification technologies with data-driven electrolyte design for lithium-ion batteries, Daikin is aligning its FKM/FFKM portfolio with high-voltage EV systems and semiconductor processing requirements, reinforcing leadership in high-purity, low-viscosity elastomers.

Chemours expands Viton portfolio and liquid cooling ecosystem for high-performance applications

The Chemours Company is strengthening its Advanced Performance Materials segment by integrating liquid fluoroelastomers with next-generation thermal management systems. Its Viton™ APA grades are increasingly adopted in high-voltage automotive cabling and data center hardware, supporting high-density electronics. Strategic partnerships for immersion and direct-to-chip cooling solutions, capable of reducing energy consumption by up to 90%, highlight Chemours’ expansion beyond traditional elastomers into fluid-material ecosystems. Capital raised through a $700 million offering is accelerating its liquid cooling venture and reinforcing its position in high-growth fluorochemical applications.

AGC advances surfactant-free fluoroelastomers with circular fluoropolymer validation

AGC Inc. is differentiating through clean chemistry innovations, introducing fluoroelastomers manufactured without surfactants or fluorinated solvents, directly addressing PFAS-related regulatory pressures. Its UL2809-certified PTFE production using recycled fluorite establishes a circular supply chain model for fluoropolymers. Under its AGC plus-2026 strategy, the company is prioritizing high-margin liquid resins for automotive electronics and semiconductor fabrication. Expansion in U.S. semiconductor hubs supports demand for ultra-high-purity materials required in advanced node manufacturing.

Shin-Etsu integrates fluorosilicone and FKM technologies for next-generation electronics

Shin-Etsu Chemical is leveraging its leadership in silicones and semiconductor materials to develop hybrid fluorosilicone and liquid FKM solutions tailored for AI-driven devices and automated mobility systems. Its ¥83 billion investment in lithography materials capacity strengthens its position in semiconductor ecosystems, while automation-driven manufacturing enhances cost efficiency and supply stability. With a portfolio of over 5,000 silicone variants integrated with fluoroelastomers, Shin-Etsu is uniquely positioned to deliver high-performance sealing and insulation materials for advanced electronics and infrastructure applications.

3M exits PFAS production while transitioning to alternative elastomer platforms

3M Company (Dyneon) is undergoing a structural transformation by fully exiting PFAS manufacturing, reshaping its advanced materials portfolio. The company is actively reformulating seals, gaskets, and battery components to meet performance requirements without PFAS inputs, particularly in automotive and aerospace sectors. Collaboration with extrusion partners ensures continuity of supply during the transition phase. By removing PFAS from a significant portion of its product portfolio, 3M is positioning itself for long-term compliance with global environmental regulations while exploring alternative high-performance elastomer chemistries.

United States: Immersion Cooling Scale-Up and Semiconductor-Grade Liquid Fluoroelastomers

The United States liquid fluoroelastomers market is being reshaped by hyperscale data center cooling requirements and the re-localization of semiconductor-grade sealing materials. In May 2025, Chemours announced a strategic partnership to accelerate commercialization of its Opteon™ two-phase immersion cooling fluids. These dielectric liquid fluoro-formulations are engineered for large-scale deployment in AI data centers from 2026 onward, with validated reductions of up to 90% in cooling energy consumption versus conventional air-cooled architectures. This development positions liquid fluoroelastomers and related fluorinated fluids as core infrastructure enablers for next-generation compute density rather than niche specialty materials.

In parallel, U.S. industrial policy is reinforcing domestic supply of ultra-high-purity elastomeric materials. Under the CHIPS Act, manufacturers expanded production lines in late 2025 for ultra-low outgassing liquid FFKM to support sub-2nm lithography nodes scheduled for 2026. Automotive electrification is reinforcing this trend, with U.S. OEMs integrating liquid FKM-based dielectric coatings into battery thermal management systems to withstand fast-charging temperature spikes above 200°C. Regulatory developments are also influencing material design. Following mid-2025 EPA updates, producers are transitioning toward non-fluorosurfactant synthesis routes to ensure long-term eligibility for federal aerospace and defense contracts.

Japan: Precision LIMS Manufacturing and Semiconductor Process Enablement

Japan’s liquid fluoroelastomers market is advancing through high-precision manufacturing, miniaturization, and semiconductor process support. In late 2025, Shin-Etsu Chemical reported expanded output of its SIFEL® liquid fluoroelastomer series, which utilizes a perfluoropolyether backbone. These materials are increasingly deployed in Liquid Injection Molding Systems to automate the production of complex micro-seals for 2026 consumer electronics and automotive platforms, where dimensional accuracy and chemical resistance are non-negotiable.

Beyond sealing, Japanese electronics firms showcased new liquid fluoroelastomer potting gels in October 2025 for sensor encapsulation. These formulations deliver extreme solvent resistance and moisture permeability as low as one-twentieth of standard silicone, enabling reliable operation in fuel-exposed automotive environments. Shin-Etsu is also scaling specialized liquid fluoro-coatings for photomask pellicles used in ArF and KrF excimer laser lithography, reinforcing Japan’s role in global semiconductor materials supply chains. Looking ahead, the Ministry of Economy, Trade and Industry 2026 roadmap highlights fluorinated anode binders and liquid-phase fluoro-additives as critical to improving cycle life and conductivity in next-generation lithium-ion batteries.

China: Policy-Driven Expansion of High-End Liquid Fluoro-Polymers

China’s liquid fluoroelastomers market is expanding under direct industrial policy support and accelerated localization of semiconductor materials. The Ministry of Industry and Information Technology released its 2025–2026 growth plan targeting a 5% annual increase in chemical sector added value, with explicit emphasis on high-end specialty rubbers and electronic chemicals such as liquid FKMs. This has translated into capacity build-outs within designated chemical parks optimized for water and energy availability, supporting high-performance fibers, membranes, and elastomeric systems derived from liquid fluoro-polymers.

At the application level, China is moving rapidly toward domestic semiconductor material self-sufficiency. Syensqo showcased its first commercial non-fluorosurfactant perfluoroelastomers at SEMICON China 2025, targeting dry etching and chemical mechanical polishing steps in domestic fabs. Concurrently, leading producers are deploying AI-enabled process optimization across elastomer synthesis lines to cut VOC emissions and improve yield consistency by 2026. These developments signal a transition from volume-driven fluorochemicals to precision-engineered liquid elastomers aligned with electronics and advanced manufacturing demand.

India: Global Manufacturing Integration and Data Center Cooling Adoption

India is emerging as a strategic manufacturing and deployment hub for liquid fluoroelastomers, driven by global partnerships and domestic infrastructure expansion. In May 2025, Navin Fluorine International signed a manufacturing agreement with Chemours to produce specialized liquid cooling fluids, with production scheduled to begin in early 2026. This positions India within the global supply chain for AI-infrastructure-grade fluorochemicals rather than solely as a regional consumer market.

Domestic policy support is reinforcing this shift. The Production Linked Incentive scheme has catalyzed new integrated fluorochemical complexes in Gujarat’s Dahej region, expanding capacity for high-performance liquid FKM formulations aimed at electric vehicles and electronics. As India’s data center footprint expands, local manufacturers are increasingly qualifying two-phase immersion cooling liquids with global technology leaders, including compatibility testing for next-generation storage and memory devices. Liquid fluoroelastomers are therefore moving into a strategic role at the intersection of digital infrastructure and advanced materials manufacturing.

Germany: EV Thermal Stress and Hydrogen Infrastructure Applications

Germany’s liquid fluoroelastomers market is being propelled by electric vehicle adoption, sustainability mandates, and emerging hydrogen infrastructure. The German Association of the Automotive Industry projects close to one million new electric passenger car registrations in 2026, a 17% year-on-year increase. This growth is directly translating into higher demand for liquid fluoroelastomer gaskets and seals capable of withstanding the thermal cycling and chemical exposure specific to German-engineered battery electric vehicles.

Sustainability considerations are shaping product portfolios alongside performance requirements. In 2025, German producers introduced non-fluorosurfactant perfluoroelastomers with certified mass-balance chain-of-custody, aligning with 2026 European Green Deal benchmarks. Beyond mobility, late-2025 pilot projects in Germany are testing liquid fluoroelastomer-based diaphragms and valve components for hydrogen refueling stations. Superior permeation resistance compared to conventional elastomers positions these materials as enabling components for the safe scaling of hydrogen mobility and energy storage infrastructure.

Liquid Fluoroelastomers Market: Country-Level Strategic Snapshot

Liquid Fluoroelastomers Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Strategic Focus Area

|

Industrial Implication

|

|

United States

|

AI data centers and semiconductors

|

Immersion cooling fluids, ultra-low outgassing FFKM

|

Liquid fluoroelastomers become core digital infrastructure materials

|

|

Japan

|

Precision electronics and fabs

|

LIMS automation, photomask coatings

|

High-value micro-sealing and lithography enablement

|

|

China

|

Policy-led localization

|

Domestic semiconductor-grade liquid FKMs

|

Shift from volume fluorochemicals to high-end elastomers

|

|

India

|

Global manufacturing integration

|

Two-phase cooling fluids, EV materials

|

India positioned as export-oriented fluorochemical hub

|

|

Germany

|

EV growth and hydrogen rollout

|

Sustainable liquid seals and diaphragms

|

Fluoroelastomers embedded in energy transition systems

|

Liquid Fluoroelastomers Market Report Scope

Liquid Fluoroelastomers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$536.7 Million

|

|

Market Size (2034)

|

$818.4 Million

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Product Type (Fluorocarbon Elastomers, Fluorosilicone Elastomers, Perfluoroelastomers), By Processing Method (Liquid Injection Molding, Adhesives and Coatings, Potting and Encapsulation), By Application (Automotive, Electronics and Semiconductor, Aerospace, Oil and Gas, Medical and Healthcare)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Daikin Industries, Chemours Company, Shin-Etsu Chemical, Syensqo, 3M Company, Momentive Performance Materials, Wacker Chemie, Dow, AGC, Navin Fluorine International, James Walker Group, HaloPolymer, Guanheng New Material Technology, Saint-Gobain Performance Plastics, Greene Tweed

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Liquid Fluoroelastomers Market Segmentation

By Product Type

- Fluorocarbon Elastomers

- Fluorosilicone Elastomers

- Perfluoroelastomers

By Processing Method

- Liquid Injection Molding

- Adhesives and Coatings

- Potting and Encapsulation

By Application

- Automotive

- Electronics and Semiconductor

- Aerospace

- Oil and Gas

- Medical and Healthcare

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Liquid Fluoroelastomers Market

- Daikin Industries

- Chemours Company

- Shin-Etsu Chemical

- Syensqo

- 3M Company

- Momentive Performance Materials

- Wacker Chemie

- Dow

- AGC

- Navin Fluorine International

- James Walker Group

- HaloPolymer

- Guanheng New Material Technology

- Saint-Gobain Performance Plastics

- Greene Tweed

*- List not Exhaustive