Live Game Streaming Platforms Market: Expansion Driven by Creator Monetization and Content Diversification

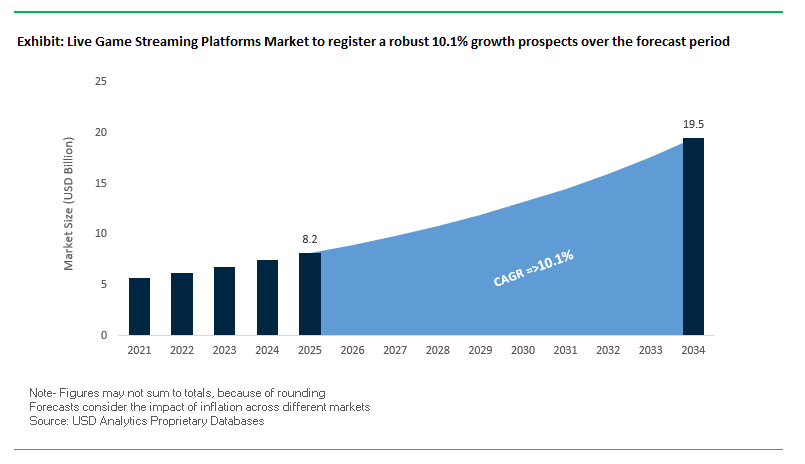

The global live game streaming platforms market is transforming at an incredible pace with the convergence of gaming, entertainment, and interactive media. The market size in 2025 is USD 8.2 billion and is forecasted to rise to USD 19.5 billion by 2034 at a CAGR of 10.1%. The growth is supported by record-breaking viewer engagement, growth in non-gaming content, and platform-level innovation in creator monetization and interactivity.

For industry professionals, the market trend is in three key areas growing viewer engagement, competitive platform strategies, and revenue diversification. Live game streaming is no longer niche entertainment; it is mainstream entertainment today, engaging both hardcore gamers and casual viewers with esports tournaments, real-time conversations, and social interactions. Platforms are pushing beyond the typical gaming to include "Just Chatting," live sports, and music, and thus bringing them to their role as end-to-end entertainment platforms.

Key Insights:

- Record-breaking audience engagement: Q2 2025 viewership reached 9.1 billion hours watched, up 5% YoY.

- Content diversification is expanding audiences beyond gaming into lifestyle, sports, and entertainment.

- Co-streaming impact: Esports tournament hours rose 6% in Q2 2025, heavily influenced by creator-led commentary streams.

- Market share shifts: Twitch remains the leader but lost 4.6% share as YouTube Gaming and Kick gained traction.

- Creator-first strategies: Platforms are lowering monetization barriers to onboard new talent faster.

Key Global Developments Shaping the Live Game Streaming Sector

The live game streaming platform market has been dominated by significant advancements in monetization, creator incentives, and content moderation in the last year.

Twitch, in July 2025, was the first to make available monetization channels like Bits, subscriptions, emotes, and badges to all global broadcasters, ending the Affiliate and Partner exclusivity. The move is to lower the barrier to entry and creator retention in a more competitive marketplace. June 2025, however, saw YouTube Gaming introduce new creator-focused features, such as support for long-form content, tutorials, and analytics integration as a one-stop content destination for gaming creators.

Kick's launch in March 2025 of the "Kick Road Campaign," in collaboration with Streams Charts, brought in a $50,000 reward for streamers with fewer than 100 simultaneous viewers. The move represents Kick's two-pronged approach of drawing in top-tier creators and incentivizing grass-root creators. Kick diversified its content base even further in October 2024 in collaboration with UFC, a bold move into live sports and wider entertainment genres.

TikTok LIVE also blurred the boundaries between entertainment and commerce. Its February 2025 shoppable livestream with singer Tate McRae showed the power of in-stream product sales to drive engagement and revenue. Before that, in June 2025, TikTok introduced AI-based content creation tools and new content filters to achieve the most personalized and viewer-centric strategy. South Korean market leader AfreecaTV maintained its hold on esports, renewing deals with LCK leagues in 2025 and introducing lifestyle content creators to broaden its content.

Trends and Opportunities in the Live Game Streaming Platforms Industry

Cloud-Based Co-Play Engines Transforming Passive Viewing into Interactive Play

Cloud-based co-play engine integration is transforming audience participation by enabling viewers to participate in live game streams directly without downloading or running the game locally. This technology leverages remote rendering and low-latency streaming to enable real-time co-op play, in-game decision voting, and audience challenges. From the streamer's perspective, this significantly improves session retention time, as interactive engagement encourages viewers to remain online longer. Platforms leveraging cloud scalability can host thousands of concurrent interactive viewers with zero performance degradation. Additionally, co-play enables premium monetization streams, where fans pay for exclusive participation rights, drive key game result drivers, or gain access to secret in-game events. Beyond games, this infrastructure is adaptable for live concerts, sports viewing parties, and interactive storytelling, with cross-industry growth prospects.

AI-Generated Personalized Casters Driving Tailored Streaming Experiences

The use of AI-powered commentary avatars allows platforms to provide hyper-personalized game casting to everyone. AI casters are capable of adjusting tone, emphasis, and pace from real-time viewer behavior, preferences, and chat activity, providing statistical deep-dives for competitive viewers or high-level overviews for casual viewers. Advanced natural language processing and translation abilities allow streams to be watched in multiple languages at once, eliminating global language barriers. AI avatars also allow for chat moderation, highlight reel creation, and live analytics creation for viewers and creators, taking production workload off of streamers. As virtual influencer technology continues to develop, these AI casters are also a new type of brandable digital personality, allowing creators to cast themselves outside of live streams.

Gambling-Licensed Prediction Streaming as a Monetization Catalyst

Combining real-money wagering and prediction markets with live game streams is a viable, engagement-based opportunity. With collaboration with regulated iGaming licensees, sites can offer wagering on game outcomes, individual in-game events, or skill contests turning viewers into invested stakeholders. This does impose KYC, age verification, and responsible gaming protection requirements, but the potential is viable. Streamers are rewarded for wagering volume through commission, with sites having the ability to leverage AI risk assessment to ensure user protection and retention. As esports wagering markets continue to grow globally, prediction streaming can be an upscale content segment, drawing both hard-core fans and casual viewers seeking larger stakes entertainment.

Education-Driven Esports Leagues for STEM Skill Development

Educational esports platforms are emerging as a bridge between competitive gaming and STEM education. Through the creation of school and university esports leagues with structured STEM integration, platforms can tap into institutional budgets and long-term youth engagement. Games such as Minecraft: Education Edition can teach coding and design basics, and physics games such as Rocket League can illustrate real-world mechanics principles. In addition to technical skills, esports leagues also foster soft skills such as leadership, communication, and problem-solving skills valued by employers today. With proper curriculum alignment, educational esports platforms can align with edtech companies, universities, and corporate sponsors to create talent pipelines from games to tech careers.

Live Game Streaming Platforms Market Share and Segmentation Insights

By Content Type: E-Sports as the Core Growth Engine with Diversification into Creative Formats

E-sports has 40% share driven by international competition, franchise leagues, and the explosive growth of co-streamed competitive events. Twitch and YouTube Gaming have sustained viewer growth through community-driven restreaming and enhanced interactive features. Casual gaming has 25% share, with independent game highlights and mobile games reaching more people. "Just Chatting" and creative content are the fastest-growing genres, bringing gaming together with IRL interaction, music, art, and code streams successfully drawing in non-gaming viewers. Sustained category diversification suggests a mature ecosystem where live streaming is a full-spectrum entertainment platform.

.png)

By Revenue Model: Advertising Leads While Hybrid Monetization Gains Traction

Advertising dominates at 35%, in the form of in-stream video advertising, sponsor overlay, and sponsored segments. But penetration of ad-blockers forces platforms to diversify. Subscriptions come next at 30% with ad-free viewing, loyalty badges, and exclusive content access. Donations and tips continue to be a key backbone for creator-fan economies, enabling direct engagement. Sponsorship partnerships from gaming gear to lifestyle brands are growing in value and variance. Merchandise sales enable streamers to capitalize on personal brands, and live shopping integrations are emerging as a new commerce model, especially in APAC markets where shoppable streams are already mass-market. The most successful platforms in 2025 will likely be those that combine multiple monetization streams for both revenue robustness and creator engagement.

Competitive Landscape – Strategic Positioning of Leading Live Game Streaming Platforms

The live game streaming platforms market is shaped by a mix of dominant global brands and region-specific leaders, each with distinct content strategies, monetization models, and technology investments. Competitive intensity is driven by aggressive creator acquisition, content diversification, and innovation in viewer engagement tools. Key players included are Twitch (Amazon.com, Inc), YouTube (Alphabet Inc), Facebook Gaming (Meta Platforms, Inc), AfreecaTV, Huya Live, Douyu, Nimo TV, Bilibili, Trovo Live, Kick, Caffeine.TV, DLive, Mildom, Niconico, Mobcrush, Others.

Twitch – Leader in Creator-Driven Live Gaming

Twitch is the leading brand in live game streaming and is firmly embedded in gaming and esports communities. Its flexible monetization model subscriptions, Bits, and ad revenue has raised the industry benchmark. In July 2025, the service made a strategic shift by opening monetization to all streamers globally with the goal of speeding up talent onboarding and retention. Twitch continues to develop community tools and experiments ad innovation like picture-in-picture ads to optimize viewer experience and advertiser ROI.

YouTube Gaming – Taking Advantage of Google's Ecosystem for Multi-Format Content

YouTube Gaming leverages Google's unparalleled audience reach and cross-format content ability to combine live streams with pre-recorded video and Shorts. The Partner Program, Super Chat, membership, and expanding live commerce features on the site offer robust revenue streams. YouTube launched advanced creator tools and analytics, led by AI, in June 2025 to further optimize content and target audiences. Its approach is focused on becoming the one-stop-shop for gaming content and aggressively poaching top creators from competing platforms.

Kick – Disruptive Monetization Model with Rapid Expansion

Kick has rapidly established itself with its 95/5 share of revenue, giving creators a market-leading share of subscription revenue. Ambitions include the signing of leading streamers and word-of-mouth growth through initiatives such as the March 2025 Kick Road Campaign. Kick's expansion into live sports via UFC agreements (October 2024) is evidence of an entertainment push extended, on one hand, to attract non-gaming audiences while retaining its gaming-based roots.

TikTok LIVE – Short-Form Discovery Drives Live Engagement

TikTok LIVE leverages its massive global user base and AI-recommended algorithm to push short-form viewers into its live streams. Its own mix of shoppable streams, virtual gifting, and interactive challenges has positioned it as a leader in live social commerce. In February 2025, TikTok's shoppable event with Tate McRae demonstrated the platform's potential for entertainment and e-commerce convergence, and June 2025 releases AI-powered content creation tools for creators.

AfreecaTV – Regional Powerhouse with Robust Esports Presence

AfreecaTV dominates the South Korean market with local content and high esports engagement. Its virtual currency, the Star Balloons, facilitates direct creator-viewer monetization, with high community interaction. In 2025, the platform expanded LCK esports sponsorships and invited lifestyle content creators to its platform, further entrenching its strategy of expanding appeal without diluting its competitive gaming focus.

United States: Innovation Leadership and Multi-Platform Monetization

The United States dominates the live game streaming platforms market through its combination of platform diversity, high consumer engagement, and a robust creator economy. Platforms such as Twitch, YouTube Gaming, and Facebook Gaming continue to enhance user interactivity through advanced features like real-time chat integration, channel loyalty rewards, and interactive overlays. These tools not only boost viewer retention but also give content creators sophisticated ways to monetize streams, from subscription tiers and virtual tipping to integrated e-commerce options. The rise of Netflix’s entry into cloud gaming highlights the market’s fluidity, as non-traditional entertainment giants test live game streaming as a new revenue stream, signaling a broader convergence between streaming media and gaming entertainment.

Mobile gaming has emerged as a crucial growth segment, with 5G network rollouts enabling high-quality, low-latency streams on smartphones. U.S. streaming platforms are partnering with mobile game publishers to secure exclusive streaming rights, further strengthening their position in this fast-growing vertical. Start-ups like Kick are disrupting the space with creator-friendly revenue splits and feature-rich mobile apps, driving competitive innovation. The market’s strong capital investment environment also ensures ongoing technology adoption, from AI-driven personalized recommendations to advanced moderation tools that enhance community safety and inclusivity.

China: Scale, Regulation, and E-Commerce Synergy

China’s live game streaming sector is one of the world’s largest, fueled by a massive internet user base and a cultural embrace of live digital entertainment. Platforms such as Huya, Douyu, and Bilibili command millions of daily active users, offering a mix of competitive gaming broadcasts, influencer-led streams, and variety content that blurs the line between gaming and interactive social entertainment. The integration of e-commerce into live streaming where influencers sell products directly during gameplay has become a defining feature of the Chinese market, driving significant cross-industry revenue streams.

However, the sector operates under a strict regulatory environment, with government oversight determining platform content policies, advertising standards, and even operational licenses. Past shutdowns of non-compliant platforms underscore the importance of compliance for long-term sustainability. Backed by tech giants like Tencent, Alibaba, and Baidu, China’s live streaming platforms benefit from deep financial resources, enabling rapid innovation in streaming technology, content discovery algorithms, and interactive engagement tools. The convergence of live streaming with online retail, coupled with a growing middle-class appetite for gaming content, positions China as both a domestic powerhouse and a key exporter of platform models to other regions.

South Korea: Domestic Platform Dominance After Twitch Exit

South Korea’s live game streaming landscape underwent a major shift following Twitch’s market exit, creating an opportunity for local platforms to dominate. AfreecaTV, already a long-established streaming leader, capitalized on its loyal community and esports heritage to retain a large share of migrating users. Meanwhile, Naver’s new platform Chzzk is making aggressive inroads, offering polished UI, competitive streamer revenue models, and exclusive content partnerships. Early adoption by popular Korean streamers has accelerated Chzzk’s growth, particularly among younger viewers attracted to interactive titles like Minecraft.

South Korea’s technology infrastructure characterized by ultra-fast broadband and high smartphone penetration supports a thriving streaming ecosystem with minimal latency. The market also benefits from the country’s strong esports culture, where game streaming is not just entertainment but a mainstream sport. Platforms are leveraging this by broadcasting tournaments, interactive fan events, and live commentary, deepening viewer engagement. The post-Twitch vacuum has fostered a competitive yet collaborative environment, with domestic platforms investing heavily in creator acquisition, mobile streaming quality, and interactive features to secure long-term dominance.

Germany: Government-Supported Gaming Ecosystem and Event-Driven Engagement

Germany’s live game streaming market benefits from a supportive policy framework that recognizes gaming as a significant cultural and economic sector. The federal government’s Games Strategy and funding programs offering up to €8 million per project extend beyond game development to infrastructure like server capacity and live operations, directly aiding streaming platforms. This institutional backing enhances Germany’s appeal for both domestic startups and international platforms seeking European expansion.

Major gaming events such as Gamescom in Cologne serve as global showcases for digital games and live streaming platforms, drawing millions of virtual and physical attendees. These events amplify Germany’s role as a content hub, providing opportunities for live streaming platforms to broadcast exclusive gameplay reveals, tournaments, and developer panels. The market’s growth is also fueled by rising broadband penetration, a tech-savvy population, and increasing integration of German content creators into global streaming networks, enabling local talent to reach international audiences with ease.

Japan: High-Tech Infrastructure and Esports-Driven Growth

Japan’s live game streaming platforms market thrives on a foundation of high-speed internet access and widespread 5G coverage, ensuring ultra-low latency streaming for both desktop and mobile users. The country’s robust esports ecosystem featuring major tournaments in titles like Street Fighter, League of Legends, and Valorant drives large-scale audience engagement, with platforms like Niconico, OPENREC.tv, and YouTube Gaming broadcasting events to millions of viewers.

Influencer-driven marketing is increasingly shaping platform growth, as young audiences follow gaming personalities across multiple streaming and social media channels. Brands are partnering with these influencers to launch interactive campaigns that blend gaming with product promotion. Platform innovation is also evident, with services experimenting in virtual event broadcasting and hybrid physical-digital fan experiences, expanding audience interaction beyond traditional gameplay streams. As gaming culture continues to merge with mainstream entertainment in Japan, the live streaming market is set to expand its role in both domestic and global esports broadcasting.

Live Game Streaming Platforms Market Report Scope

Live Game Streaming Platforms Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.2 Billion

|

|

Market Size (2034)

|

$19.5 Billion

|

|

Market Growth Rate

|

10.1%

|

|

Segments

|

By Platform (Desktop/PC, Mobile, Console), By Content Type (E-sports, Casual Gaming, Creative Content, Just Chatting), By Revenue Model (Advertising, Subscriptions, Donations/Tips, Sponsorships, Merchandise Sales), By Viewer Demographics (Age Group, Gender, Geographic Region), By Technology (Cloud-based Streaming, Peer-to-Peer Streaming)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Twitch (Amazon.com, Inc), YouTube (Alphabet Inc), Facebook Gaming (Meta Platforms, Inc), AfreecaTV, Huya Live, Douyu, Nimo TV, Bilibili, Trovo Live, Kick, Caffeine.TV, DLive, Mildom, Niconico, Mobcrush, Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Live Game Streaming Platforms Market Segmentation

By Platform

- Desktop/PC

- Mobile

- Console

By Content Type

- E-sports

- Casual Gaming

- Creative Content

- Just Chatting

By Revenue Model

- Advertising

- Subscriptions

- Donations/Tips

- Sponsorships

- Merchandise Sales

By Viewer Demographics

- Age Group

- Gender

- Geographic Region

By Technology

- Cloud-based Streaming

- Peer-to-Peer Streaming

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Live Game Streaming Platforms Market

- Twitch (Amazon.com Inc)

- YouTube (Alphabet Inc)

- Facebook Gaming (Meta Platforms Inc)

- AfreecaTV

- Huya Live

- Douyu

- Nimo TV

- Bilibili

- Trovo Live

- Kick

- Caffeine.TV

- DLive

- Mildom

- Niconico

- Mobcrush

* List Not Exhaustive

Research Coverage

This report investigates the Live Game Streaming Platforms Market, offering an in-depth analysis of market expansion driven by creator monetization, content diversification, and advanced audience engagement strategies. It reviews global trends, regional developments, platform-level innovations, and emerging technologies shaping the competitive landscape. By examining breakthroughs in AI-generated personalized casters, cloud-based co-play engines, and integrated monetization models, this report delivers actionable intelligence for investors, platform operators, and content creators. Highlights include strategic positioning of leading platforms like Twitch, YouTube Gaming, Kick, and AfreecaTV, as well as region-specific growth patterns in the United States, China, South Korea, Germany, and Japan. With coverage of both established and disruptive players, this report is an essential resource for industry professionals seeking to navigate evolving revenue models, regulatory landscapes, and content strategies in a rapidly scaling market. Scope includes-

- Segmentation: By Platform (Desktop/PC, Mobile, Console), By Content Type (E-sports, Casual Gaming, Creative Content, Just Chatting), By Revenue Model (Advertising, Subscriptions, Donations/Tips, Sponsorships, Merchandise Sales), By Viewer Demographics (Age Group, Gender, Geographic Region), By Technology (Cloud-based Streaming, Peer-to-Peer Streaming)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic Data: 2021 to 2024; Forecast Data: 2025 to 2034.

- Companies: Profiles and strategies of 15+ leading companies, including Twitch, YouTube, Facebook Gaming, AfreecaTV, Huya Live, and Kick.

Methodology

The study adopts a hybrid research approach, combining extensive secondary research from credible industry databases, trade journals, and platform performance reports with primary insights from interviews with key stakeholders, including streaming platform executives, esports tournament organizers, and content monetization experts. Quantitative modeling incorporates audience metrics, monetization patterns, and technological adoption rates to forecast market performance from 2025 to 2034. Regional analysis leverages both macroeconomic and sector-specific indicators to identify growth hotspots, while competitive mapping applies Porter’s Five Forces and SWOT frameworks to evaluate strategic positioning. The methodology ensures data triangulation for accuracy, delivering fact-based, actionable insights tailored for decision-making in the live game streaming industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.