Market Overview: Low-Frequency NVH Control Is Shifting from Design Tuning to A Materials-Led Constraint

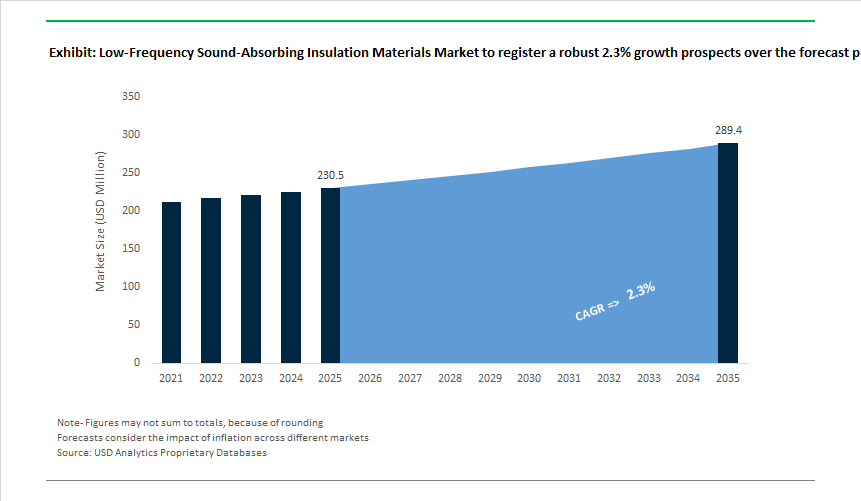

The Low-Frequency Sound-Absorbing Insulation Materials Market is valued at USD 230.5 million in 2025 and is projected to reach USD 289.4 million by 2035, growing at a modest 2.3% CAGR. Despite its limited size, the market holds outsized strategic importance because low-frequency noise and vibration (typically below ~500 Hz) has become one of the hardest-to-solve comfort, compliance, and productivity challenges across electric mobility, heavy industry, and modern buildings. In these regimes, traditional lightweight absorbers fail, forcing OEMs and specifiers to treat low-frequency NVH not as a tuning issue, but as a material-selection problem.

In electric vehicles, the removal of internal combustion noise exposes previously masked low-frequency road, tire, and structure-borne vibrations, making them perceptually dominant-often experienced as a significant increase in cabin boom and resonance. As a result, automotive OEMs are increasingly specifying mass-loaded vinyl, viscoelastic damping layers, engineered acoustic foams, and hybrid composites that can attenuate low-frequency energy without imposing unacceptable weight penalties. This shift elevates low-frequency acoustic materials from secondary trim components to platform-level NVH enablers, particularly around battery enclosures, floor systems, and chassis interfaces where vibration transmission is most pronounced.

Industrial and infrastructure applications reinforce the market’s structural relevance. A majority of heavy rotating and reciprocating machinery generates dominant acoustic energy in the 20-200 Hz range, where airborne absorption is ineffective and vibration isolation becomes critical. Here, demand centers on viscoelastic damping systems, high-density mineral wool, and mechanically decoupled insulation assemblies that convert vibrational energy into heat and prevent structure-borne noise propagation. For operators, effective low-frequency control directly impacts equipment longevity, worker safety, and regulatory compliance, making performance reliability more important than material cost optimization.

Building and transport regulations are further tightening performance expectations. Residential, commercial, and transit specifications increasingly reference low-frequency-weighted sound reduction metrics, pushing designers to achieve wall and partition performance levels of Rw(C;Ctr) ≥50 dB in traffic- and equipment-exposed environments. This regulatory pressure is expanding demand for insulation systems that deliver verified low-frequency insertion loss while meeting fire safety, indoor air quality, and health requirements such as formaldehyde-free binders and self-extinguishing behavior.

Material choice reflects application-specific trade-offs. Mineral wool continues to anchor industrial and building demand due to its strong absorption at targeted low-frequency bands and inherent fire resistance. In contrast, engineered polyurethane and melamine foams, advanced nonwovens, and hybrid damping composites are gaining specification in EVs and aerospace cabins, where comparable low-frequency performance must be achieved with reduced mass and thickness. As EV adoption, urban density, and industrial automation increase, low-frequency sound-absorbing materials are evolving into a precision materials niche defined by performance validation, compliance, and integration into system-level NVH strategies, rather than volume growth alone.

Market Analysis: Product Launches, Capacity Moves and EV/Rail Use Cases

Recent industry activity underlines a simultaneous push on automotive EV acoustics, building-grade mineral wool innovation, and capacity expansion for stone/glass wool aimed at data-centre and multi-family housing demand. In October 2024 Bridgestone developed a vibration-damping foam for high-speed rail (Shinkansen), demonstrating early cross-pollination of low-frequency solutions from rail to other transport sectors. Through 2025 automotive manufacturers and suppliers accelerated productisation for EV NVH: September 2025 3M launched an acoustic nonwoven tailored to absorb road noise in EV cabins, and August 2025 Autoneum announced deployment of hybrid noise-absorption systems on a new European EV platform to tackle chassis-borne booming below 250 Hz.

Building and industrial markets saw parallel activity: November 2025 Owens Corning introduced a formaldehyde-free mineral wool for interior partitions in the U.S., addressing healthy-building certification requirements while improving sound damping; November 2025 Mag-Isover (Saint-Gobain) launched a glass-wool product optimised for traditional Japanese timber homes where low-frequency impact and traffic noise are problematic. October 2025 Rockwool North America started operations at a new stone wool plant in West Virginia to increase regional supply of fire-resistant acoustic insulation for data centres and multifamily housing. India and regional OEMs also pushed product innovation: September 2025 TIKIDAN introduced sheet-based systems (M.A.D., Impactodan) for soaking up low-frequency structural vibrations in residential/commercial buildings.

Low-Frequency Sound-Absorbing Insulation Materials Market Trends and Opportunities

High-Density, Micro-Perforated Panels for Data Center Noise Abatement

Hyperscale data centers are emerging as the single most disruptive source of low-frequency noise globally. High-velocity cooling fans, transformers, and UPS systems generate persistent tonal noise in the 63–250 Hz band, which is inadequately captured by traditional dBA-weighted standards. This has triggered a regulatory pivot toward C-weighted (dBC) noise limits, directly elevating demand for materials capable of absorbing long-wavelength acoustic energy.

In March 2025, Prince William County revised its local noise ordinance to explicitly account for low-frequency emissions from data centers, prioritizing dBC measurements over dBA. This shift is structurally significant: dBC weighting captures bass-heavy mechanical noise that previously fell outside compliance frameworks, forcing operators to redesign acoustic envelopes rather than rely on setback distances alone.

Parallel zoning actions are accelerating this trend. In October 2025, Indiana’s Jay County Plan Commission proposed data center requirements mandating closed-loop water cooling and maximum noise levels of 50 dB at 1,000 feet, effectively embedding acoustic performance into site approval criteria. These constraints are driving adoption of high-density micro-perforated panels, composite acoustic barriers, and engineered berm systems, often exceeding six feet in height and tuned specifically for sub-250 Hz attenuation.

At the technology frontier, NTT Group announced the world’s first spatial Active Noise Control (ANC) system in November 2025. Unlike point-based ANC, this approach uses GPU-synchronized wavefront generation to suppress low-frequency noise across entire rooms with ~2 microseconds latency, targeting the fluctuating acoustic signatures typical of urban data hubs. While still complementary to passive insulation, spatial ANC is redefining expectations for future low-frequency noise mitigation strategies.

Viscoelastic Damping Integration for Aerospace and Rail Interiors

In aerospace and high-speed rail, low-frequency noise is increasingly addressed through structural damping rather than airborne absorption. Lightweight cabins and car bodies amplify “booming” effects in the 40–200 Hz range, making constrained-layer damping (CLD) a preferred solution over mass-heavy insulation.

Technical evaluations published in late 2025 show that bitumen-based and butyl rubber viscoelastic layers can reduce interior noise by 5–8 dBA in high-speed railcars, with peak effectiveness between 125–250 Hz—the frequency range most correlated with passenger discomfort. This performance profile has made CLD materials indispensable in modern rolling stock, where weight penalties must be minimized.

By December 2025, more than 18 commercial aircraft families and 15 wide-body programs had integrated advanced viscoelastic sandwich panels into floors, sidewalls, and fuselage skins. Industry data indicates that viscoelastic polymers now account for ~45% of CLD output, reflecting a decisive shift away from metal-heavy damping solutions.

Material innovation is accelerating this transition. Nearly 47% of acoustic material suppliers reported a 2025 pivot toward lightweight metal–polymer and composite-based CLD systems, enabling up to 15% secondary insulation weight reduction while simultaneously improving fatigue resistance in vibration-prone structures. This dual benefit—acoustic comfort plus structural durability—is reshaping procurement priorities across both aerospace and rail OEMs.

Acoustic Retrofits for Multifamily Housing Under IBC 2024/2025

Building codes are emerging as a powerful demand engine for low-frequency insulation, particularly in dense urban housing. Updates to the 2024 International Building Code (IBC) and related energy codes emphasize performance-based compliance for Impact Insulation Class (IIC) and Sound Transmission Class (STC), pushing developers toward engineered acoustic assemblies rather than prescriptive designs.

In 2024 alone, over 2,500 commercial and residential developments globally adopted advanced acoustic membranes and viscoelastic layers to justify compliance in multifamily (R-2) occupancies. This has elevated demand for Mass-Loaded Vinyl (MLV) and decoupled wall systems capable of attenuating low-frequency structure-borne noise from mechanical rooms, elevators, and adjacent units.

The market is notably shifting from standard 1 lb/sq ft MLV toward custom 2 lb/sq ft densities, particularly in mixed-use developments where residential units coexist with retail or mechanical infrastructure. These thicker barriers—often ~¼ inch—are increasingly specified in party walls and equipment enclosures to suppress bass transmission that conventional drywall assemblies cannot address.

A parallel trend is the rise of multifunctional acoustic drywall, combining low-frequency damping with moisture resistance and fire protection. In 2025, residential construction remains the dominant application, accounting for over 45% of soundproof drywall demand, as builders seek integrated solutions that satisfy multiple code requirements within constrained wall thicknesses.

Noise Mitigation for EV Powertrains and Road Noise

Vehicle electrification has fundamentally altered the automotive acoustic landscape. The absence of internal combustion engine noise exposes low-frequency road roar (20–150 Hz) and inverter-related tonal noise, making NVH control a critical differentiator in EV design.

OEMs are increasingly supplementing passive insulation with Road-Noise Active Noise Control (RANC). Hyundai Motor Group has commercialized RANC systems that use wheel-mounted sensors and inverted soundwaves to cancel road noise in real time. This approach allows manufacturers to reduce unsprung mass by replacing heavy passive dampers with lighter active systems—an important efficiency gain for EV platforms.

Powertrain evolution is compounding this need. In 2025, Garrett Motion unveiled electric powertrains operating at up to 35,000 rpm, where high-frequency switching can excite low-frequency electromagnetic resonance in motor housings. These architectures require specialized viscoelastic layers and damping blocks to prevent structural amplification of tonal noise.

Beyond comfort, acoustic design is becoming a safety consideration. Research presented by the Acoustical Society of America in December 2025 indicates that pink noise, which concentrates energy in lower frequencies, is the most effective EV approach sound for pedestrian awareness. This insight is steering OEMs toward low-frequency-biased sound signatures that improve safety without adding to high-frequency urban noise pollution.

Market Share Analysis: Low-Frequency Sound-Absorbing Insulation Materials Market

Market Share by Product Form: Rigid Boards & Slabs Anchoring Low-Frequency Noise Control Economics

Rigid boards and slabs command approximately 35% of the Low-Frequency Sound-Absorbing Insulation Materials Market because low-frequency acoustics is fundamentally a mass-and-resistance problem, not a surface-treatment one. Bass frequencies below 200 Hz carry long wavelengths and high energy, which lightweight foams and blankets physically cannot dissipate. High-density mineral wool and fiberglass boards succeed precisely because they combine structural mass with engineered airflow resistance, allowing them to convert acoustic pressure into heat through internal friction. Industry-standard configurations—such as 100 mm rigid slabs at around 60 kg/m³ density—consistently achieve absorption coefficients approaching 0.90 at 125 Hz, a performance threshold that effectively defines “true” low-frequency control in studios, industrial plants, and commercial buildings. This segment’s share is reinforced by regulatory and safety constraints: rigid slabs are typically rated Euroclass A1 non-combustible, making them permissible in mechanical rooms, stairwells, and public infrastructure where polymer-based absorbers are restricted. Equally important is performance predictability over time—rigid boards maintain airflow resistivity within the critical 5–50 kPa·s/m² window, ensuring they remain absorptive rather than reflective as buildings age. In economic terms, rigid boards dominate because they deliver repeatable, code-compliant bass attenuation with a single material system, minimizing redesign risk for architects and acoustic consultants working under increasingly strict urban noise standards.

Market Share by Application: Building & Construction Driving Structural Demand for Bass Attenuation

Building and construction accounts for around 40% of total market demand, making it the largest application segment as low-frequency noise shifts from a niche acoustic concern to a mainstream urban compliance issue. Modern building codes now explicitly target low-frequency performance through metrics such as the Ctr traffic noise correction factor, reflecting the reality that HVAC systems, generators, rail lines, and road traffic generate persistent bass energy that traditional insulation fails to address. Rigid low-frequency slabs integrated into wall cavities and service enclosures can improve Ctr ratings by 8–10 dB, a decisive margin for meeting 2025 municipal noise ordinances in dense cities. This application dominance is also driven by mechanical room acoustics, where boilers, chillers, and backup generators operate continuously in the 50–100 Hz range; rigid boards consistently outperform thermal insulation alone by up to 15 dB of additional attenuation, reducing occupant complaints and retrofit costs. Sustainability further strengthens construction demand: leading products now incorporate 80%+ recycled content, aligning low-frequency acoustic performance with LEED and BREEAM certification requirements. Finally, developers favor rigid boards for their zero-settlement, multi-decade durability, as acoustic failures caused by sagging materials are costly to remediate post-occupancy. Together, regulatory pressure, ESG alignment, and lifecycle reliability position building and construction as the structural demand engine sustaining the market’s largest share.

Competitive Landscape: Mineral-Wool Giants, Automotive NVH Specialists and Adhesive/Nonwoven Innovators

The competitive set comprises global mineral-wool incumbents, dedicated automotive NVH specialists, elastomeric and foam innovators, plus adhesives and nonwoven suppliers that enable easy integration on high-volume production lines. Market winners combine proven low-frequency performance data, lightweight formulation options for mobility, and health/sustainability credentials for building markets.

Saint-Gobain (ISOVER/Certainteed) Leads With High-Efficacy Mineral Wool and Lightweight Industrial Solutions

Saint-Gobain is a global leader in glass and stone mineral wool under the ISOVER and CertainTeed brands, offering products engineered to absorb up to 95% of sound energy at target frequencies for industrial and building use. Their ULTIMATE™ U TECH line provides equivalent industrial sound insulation at roughly half the weight of traditional stone wool, and they complement core acoustic insulation with laminated acoustic glazing (PVB interlayers) to improve façade Rw(Ctr) performance. Saint-Gobain’s push on formaldehyde-free and health-oriented products aligns with green-building specifications, making its portfolio a frequent choice for architects and industrial specifiers seeking high low-frequency attenuation with sustainability credentials.

Autoneum Focuses Solely On Vehicle NVH With Hybrid Materials Tuned For EV Low-Frequency Booming

Autoneum is a global automotive NVH specialist with solutions in nearly 1 in 3 vehicles worldwide; it develops hybrid absorption systems and proprietary materials that mitigate low-frequency booming (<250 Hz) in EV chassis. The company’s lightweight fiber-based acoustic materials achieve significant mass savings (often >20% vs MLV) while meeting automotive fire-safety standards. Autoneum operates ~50 production and tech centres globally, enabling tight OEM integration and localized material tuning for regional vehicle platforms.

Knauf Insulation Scales Mineral Wool With Sustainability and Specifier Support For Low-Frequency Build Performance

Knauf is a major mineral wool manufacturer using ECOSE™ formaldehyde-free binder technology; its product data explicitly provides Rw(C;Ctr) metrics (e.g., partition values like Rw(C;Ctr)=50(−4;−10) dB), enabling specifiers to validate low-frequency performance for partitions and façades. Knauf’s portfolio (Ultracoustic P Panels, Acoustic Rolls) targets internal sound transfer and impact noise between dwelling units, and the company supports architects with RIBA-accredited CPD and acoustic calculators - a valuable service for winning project specifications where low-frequency metrics matter.

Armacell Supplies Elastomeric Damping and High-Density Mass-Loaded Barriers For Industrial and Transport Use

Armacell’s ArmaFlex® and ArmaSound® ranges include flexible elastomeric foams and mass-loaded barriers (ArmaSound Barrier EX) engineered for damping and decoupling in HVAC, industrial piping and transport systems. Their mass-loaded products achieve high sound-reduction indices (≥25 dB at 2 mm thickness) and ArmaSound® Industrial Systems combine acoustic absorption with thermal insulation-reducing corrosion under insulation (CUI) risk in oil & gas while addressing low-frequency noise. Armacell’s transport-grade foams meet fire standards (e.g., FMVSS 302), making them suitable for bus, rail and marine damping applications.

3M Applies Adhesive and Nonwoven Expertise To Lightweight Automotive Acoustic Solutions and Viscoelastic Damping

3M leverages adhesives and nonwoven technology to produce pre-applied damping pads, acoustic composites and a September 2025 lightweight nonwoven targeted at EV cabin road-noise absorption. Their Scotch Damp viscoelastic tapes and damping foils convert low-frequency panel vibrations into heat and streamline installation in high-volume automotive lines. Longstanding OEM relationships and assembly-friendly formats (pre-applied pads, die-cut parts) make 3M a preferred supplier for OEMs seeking manufacturing efficiency plus proven low-frequency NVH performance.

Singapore has become one of the world’s most policy-driven markets for ultra-low-frequency noise control, particularly for dense urban construction. Effective April 1, 2025, the National Environment Agency (NEA) mandated ≥6 m perimeter noise barriers for construction projects valued above US$50 million and located within 75 m of sensitive receptors. Crucially, the regulation specifies performance against structural and ground-borne low-frequency vibration, not just broadband airborne noise—reshaping procurement toward high-mass systems that attenuate <250 Hz bands.

Enforcement intensity is unprecedented. From 2025, projects must deploy AI-enabled real-time noise logging with continuous data capture; penalties include fines up to US$20,000 and immediate stop-work orders for monitoring lapses. This has triggered rapid uptake of mass-loaded vinyl (MLV), multi-layer acoustic quilts, and hybrid barrier assemblies engineered to absorb rumble and vibration in confined corridors. Singapore’s model is now a reference case for outcome-based, digitally enforced acoustic regulation.

China: Ecological Code Integration and Metamaterial R&D

China is embedding noise pollution control into national environmental law via the Draft Ecological and Environmental Code released by the National People’s Congress on April 30, 2025. The code consolidates air, water, and noise statutes, introduces unified penalties, and mandates Clean Production Auditing—directly affecting insulation manufacturers’ material choices and lifecycle reporting. This legal consolidation elevates low-frequency attenuation from a compliance add-on to a core industrial KPI.

Industrial responses are twofold. Circular supply is expanding through BASF’s loopamid® facility in Shanghai (operational in early 2025), enabling recycled polyamide-based foams and textiles for automotive low-frequency insulation. In parallel, the MIIT 2025–2027 Action Plan prioritizes membrane-type acoustic metamaterials with sub-100 Hz targeting, accelerating domestic capabilities for narrowband attenuation demanded by EV cabins and urban infrastructure.

Germany: Zero-Pollution Targets and Bio-Hybrid Acoustic Systems

Germany leads Europe’s transition toward source-oriented noise mitigation, aligning building and transport policy with the EU’s 2030 zero-pollution ambition. In 2025, building codes emphasized upstream measures—reducing vibration at origin—driving adoption of bio-based mineral wool, natural-fiber hybrids, and recycled fiber composites engineered for low-frequency damping. These materials meet stringent carbon-footprint reporting under the EU Environmental Noise Directive (END).

Transport policy reinforces demand. Federal funding expanded regular rail grinding and trackside damping along ICE high-speed corridors, where ground-borne vibration is the dominant nuisance. German suppliers are also integrating aerogel-enhanced composites and hybrid absorbers to achieve deep attenuation below 250 Hz while maintaining recyclability—positioning Germany as the benchmark for circular, performance-verified acoustic materials.

South Korea: EV Cabin Comfort and Cleanroom Vibration Control

South Korea’s focus sits at the intersection of EV acoustics, AAM readiness, and precision manufacturing. Amendments to the Noise and Vibration Control Act (effective reporting from 2025) require semi-annual inspections for vehicles and industrial sites, elevating low-frequency performance as a compliance metric. With the national EV fleet surpassing 200,000 in late 2025, acoustic comfort ratings now influence energy-efficiency standards—pressuring OEMs to deploy elastomeric foams and tuned resonant structures that address tire and road noise.

Industrial clustering adds a second demand vector. The designation of Gwangju as an advanced semiconductor and packaging hub in 2025 has created specialized requirements for ultra-low-vibration insulation in cleanrooms. Suppliers are scaling 3D-printed resonant absorbers and micro-cellular elastomers that suppress structure-borne noise without particle shedding—critical for high-yield fabs.

United States: Infrastructure Modernization and AI-Optimized Absorption

In the United States, low-frequency acoustic demand is being pulled by transport infrastructure upgrades and green building certification. The U.S. Department of Transportation (DOT) FY 2025 Performance Plan prioritizes Climate and Sustainability, channeling funding into noise-optimized pavements and advanced barriers for environmental-justice corridors—applications dominated by low-frequency truck and tire noise.

Buildings amplify the pull-through. With 46,000+ residential projects achieving LEED certification in mid-2024 (and momentum continuing into 2025), demand surged for insulation emphasizing recycled content and deep-bass absorption, including Advanced Fiberglas™ systems. On highways, a U.S.-led consortium reported a 34% improvement in absorption efficiency (May 2025) using AI-optimized acoustic metamaterials, signaling a shift from thickness-led designs to data-driven, frequency-selective solutions.

India: Enforcement-Led Adoption and Domestic Manufacturing Scale-Up

India’s market is accelerating through enforcement and localization. In November 2025, the Central Pollution Control Board (CPCB) tightened guidance under the Noise Rules, 2000, reinforcing Silence Zones (100 m) around hospitals and schools and compelling developers to integrate structural vibration control into new projects. This has materially expanded demand for impact-damping systems in dense urban builds.

Domestic capability is rising in parallel. In September 2025, TIKIDAN launched M.A.D. and Impactodan systems engineered for low-frequency structural noise in high-rise applications. Policy alignment from Bharat Tex 2025 is further channeling textile waste into high-performance acoustic panels, linking sustainability goals with <250 Hz attenuation for rail and real estate.

2025 Strategic Matrix: Low-Frequency Sound-Absorbing Insulation

Low-Frequency Sound-Absorbing Insulation Matrix

|

Country

|

Primary Market Driver

|

2025 Strategic Milestone

|

Key Material Technology

|

|

Singapore

|

Urban density & construction

|

NEA perimeter barrier mandate (Apr 2025)

|

High-mass MLV, acoustic quilts

|

|

China

|

Environmental legislation

|

Draft Ecological & Environmental Code

|

Recycled PA6, acoustic metamaterials

|

|

Germany

|

Zero-pollution mandates

|

END-aligned building/rail updates

|

Bio-hybrids, aerogels

|

|

South Korea

|

EV & AAM comfort

|

Revised Noise & Vibration Control Act

|

3D-printed resonant absorbers

|

|

United States

|

Infrastructure modernization

|

DOT FY 2025 Performance Plan

|

Advanced fiberglas, AI-metamaterials

|

|

India

|

Real estate & rail

|

TIKIDAN launches (Sep 2025)

|

Structural vibration dampeners

|

Low-Frequency Sound-Absorbing Insulation Materials Market Report Scope

Low-Frequency Sound-Absorbing Insulation Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$230.5 Million

|

|

Market Size (2035)

|

$289.4 Million

|

|

Market Growth Rate

|

2.3%

|

|

Segments

|

By Material Type (Mineral Wool, Foams, Acoustic Metamaterials, Natural/Bio-based Fibers, Specialty Materials), By Product Form (Blankets & Rolls, Rigid Boards & Slabs, Acoustic Panels & Baffles, Foam Sheets & Die-cut Parts, Lagging & Wraps), By Technology (Passive Absorption, Passive Reflection/Isolation, Active–Passive Hybrids, Metamaterial-based), By End-User Industry (Automotive & Transportation, Building & Construction, Aerospace & Defense, Industrial & OEM, Electronics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Saint-Gobain S.A., Rockwool International A/S, Knauf Insulation, Autoneum Holding Ltd., BASF SE, 3M Company, Armacell International S.A., Owens Corning, Huntsman International LLC, Johns Manville, Kingspan Group plc, DuPont de Nemours Inc., Trelleborg AB, Soprema Group, Toray Industries Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Low-Frequency Sound-Absorbing Insulation Materials Market Segmentation

By Material Type

- Mineral Wool

- Foams

- Acoustic Metamaterials

- Natural/Bio-based Fibers

- Specialty Materials

By Product Form

- Blankets & Rolls

- Rigid Boards & Slabs

- Acoustic Panels & Baffles

- Foam Sheets & Die-cut Parts

- Lagging & Wraps

By Technology

- Passive Absorption

- Passive Reflection/Isolation

- Active-Passive Hybrids

- Metamaterial-based

By End-User Industry

- Automotive & Transportation

- Building & Construction

- Aerospace & Defense

- Industrial & OEM

- Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Low-Frequency Sound-Absorbing Insulation Materials Market

- Saint-Gobain S.A.

- Rockwool International A/S

- Knauf Insulation

- Autoneum Holding Ltd.

- BASF SE

- 3M Company

- Armacell International S.A.

- Owens Corning

- Huntsman International LLC

- Johns Manville

- Kingspan Group plc

- DuPont de Nemours, Inc.

- Trelleborg AB

- Soprema Group

- Toray Industries, Inc.

*- List not Exhaustive