Lubricant Viscosity Grade Improvers Market 2025–2034: Ultra-Low Viscosity Engine Oils, EV Transmission Fluids, and Polymer Innovation Driving $4.5 Billion Outlook at 5.5% CAGR

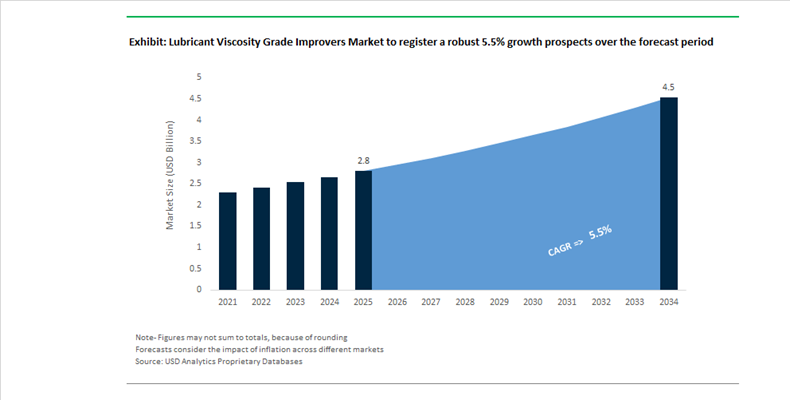

The Lubricant Viscosity Grade Improvers Market is projected to grow from $2.8 billion in 2025 to $4.5 billion by 2034, registering a CAGR of 5.5%. Demand is being propelled by the global transition toward ultra-low viscosity engine oils such as SAE 0W-20 and 0W-16, extended drain heavy-duty lubricants, and electrified transmission fluids for hybrid and battery electric vehicles. Viscosity index improvers, typically high-molecular-weight polymeric additives such as olefin copolymers and polymethacrylates, are critical for maintaining shear stability, oxidative durability, and fuel efficiency across wide temperature ranges. Increasing OEM specifications, tighter emissions standards, and the need for improved cold-start performance are reshaping polymer architecture design and molecular weight distribution control within advanced lubricant formulations.

In December 2024, Chevron U.S.A. completed a refinery retrofit in Pasadena, Texas, enhancing flexibility to process lighter crude slates and secure high-quality base oil supply for blending with advanced viscosity modifiers in the automotive aftermarket. In mid-2025, Chevron Oronite received Volvo VDS-5 approval for its OLOA 61530 heavy-duty additive package, incorporating specialized viscosity modifier technology to meet stringent oxidation resistance and extended drain interval requirements. In September 2025, Afton Chemical launched a dedicated additive for hydrogen-fueled heavy-duty engines featuring a tailored viscosity grade improver system designed to manage moisture condensation and thermal stress in Hydrogen Internal Combustion Engine applications. During 2025, Evonik expanded the application scope of its VISCOPLEX pour point depressants and viscosity modifiers in chemical recycling, improving the handling and flow properties of pyrolysis oils to support circular economy initiatives.

Strategic supply chain reinforcement and e-mobility innovation intensified in early 2026. In January 2026, Infineum launched P6188, an advanced viscosity modification technology approved against Volkswagen 508 00 and 509 00 standards, enabling stable ultra-low viscosity SAE 0W-20 oils with enhanced wear protection. In the same month, Infineum signed a strategic framework agreement with Rianlon to strengthen Asia-Pacific manufacturing capacity for critical additive components, including viscosity index improver polymers. Afton Chemical released updated technical insights in January 2026 emphasizing specialized viscosity modifiers for Electrified Transmission Fluids that require high dielectric strength and superior thermal management. In February 2026, Lubrizol inaugurated its Shanghai Innovation Center following its 2025 Singapore facility launch, accelerating development of local-for-local polymeric viscosity modifiers for Asian EV markets. In February 2026, Evonik streamlined its North American distribution network to reinforce supply security for specialty additive customers, complementing ongoing polymer innovation and global logistics optimization within the viscosity improver value chain.

Strategic Trends and High-Impact Opportunities in the Lubricant Viscosity Grade Improvers Market

Trend: High-Shear Stable Polymer Innovation for Ultra-Low Viscosity EV Driveline Fluids

The rapid adoption of electric vehicles is redefining performance thresholds for viscosity grade improvers, particularly in e-fluids used within integrated electric drive units. Unlike conventional internal combustion drivetrains, EV drivelines expose lubricants to extreme rotational speeds that frequently exceed 18,000 RPM while simultaneously demanding high dielectric strength and copper compatibility. This operating environment is accelerating the shift away from legacy olefin copolymers toward advanced styrene-isoprene and polyalkylmethacrylate chemistries that can deliver stable viscosity under severe mechanical shear.

In late 2025, Infineum disclosed that its latest generation of e-fluid viscosity modifiers met driveline efficiency benchmarks at roughly one third of the treat rate required by conventional PMA systems. This reduction is strategically important for ultra-low viscosity grades such as SAE 0W-8 and 0W-12, where additive overloading can compromise dielectric performance. Shear stability has emerged as a defining differentiator. Infineum reported that its EV-specific VGIs have accumulated operational data equivalent to more than one trillion miles across battery electric and hybrid platforms, validating their resistance to permanent viscosity loss under sustained centrifugal stress. Thermal management is reinforcing this trend. The EVOGEN platform from Lubrizol, expanded in December 2025, integrates novel polymer architectures that suppress copper corrosion while maintaining viscosity stability. This enables direct immersion cooling of electric motors, a design approach capable of improving thermal efficiency by up to 20% compared with indirect cooling systems and positioning high-shear stable VGIs as enablers of next-generation EV architectures.

Trend: Capacity Expansion and Consolidation for Hydrogenated Styrene Block Copolymers in Industrial Greases

Beyond automotive electrification, industrial demand is reshaping the viscosity grade improvers market through increased adoption of hydrogenated styrene block copolymers in high-performance greases. Wind energy, heavy mining, and steel processing applications require lubricants that can withstand extreme pressure, vibration, and extended service intervals without oil bleed or structural collapse. HSBC-based polymers are increasingly preferred because they function as both viscosity index improvers and co-thickeners, reducing reliance on traditional lithium soap systems.

Strategic supply moves underscore this shift. In December 2025, Lubrizol announced the global rollout of its HybriCal grease thickener system, a lithium-free technology that uses advanced polymer synergies to meet industrial EP requirements while lowering environmental impact. Wind turbine operators are now mandating HSBC-based greases for pitch and yaw bearings, where maintenance cycles can exceed five years. Technical studies from Chevron Phillips Chemical indicate that these polymers deliver superior low-bleed performance, ensuring lubricant retention even in offshore installations exposed to constant vibration and moisture. To support rising demand, Chevron Phillips Chemical confirmed in late 2025 that key monomers and specialty polymers such as HE 100 and HE 300 have been pre-registered across major regulatory jurisdictions, signaling long-term investment in captive production capacity for high-viscosity synthetic lubricant applications.

Opportunity: Bio-Derived Viscosity Modifiers for Environmentally Acceptable Marine Lubricants

Regulatory transformation in the marine sector is creating a non-discretionary growth opportunity for biodegradable viscosity grade improvers. The replacement of the Vessel General Permit with the Vessel Incidental Discharge Act has made the use of Environmentally Acceptable Lubricants mandatory for oil-to-sea interfaces, including stern tubes and thrusters. Under the 2025 VIDA framework, at least 90% of a lubricant formulation must be biodegradable and non-bioaccumulative, fundamentally altering additive selection criteria.

Polyalkylmethacrylate-based viscosity modifiers have emerged as a preferred solution due to their inherent low-temperature fluidity and compatibility with synthetic esters. Evonik responded to this regulatory pull by increasing its PAMA production capacity by approximately 15% during 2024 and 2025 to serve the expanding EAL segment. Life cycle assessments published in MDPI in June 2025 indicate that modern bio-based lubricant systems enabled by high-performance green additives can reduce friction losses by up to 40% and deliver carbon emission reductions of 30 to 60% compared with mineral oil formulations. Additional momentum is expected from the EPA Design for the Environment program, which is introducing enhanced labeling for safer lubricants. This initiative is likely to accelerate third-party certification requirements, pushing vessel operators toward certified, VGI-enabled EALs to avoid compliance penalties in U.S. and European waters.

Opportunity: Low-Pour-Point Polymer Packages for Arctic Operations and Cold-Chain Logistics

Expanding Arctic energy exploration and the rapid growth of global cold-chain logistics are creating a specialized demand for viscosity grade improvers that ensure lubricant flow at temperatures below minus 40 degrees Celsius. In these environments, wax crystallization and viscosity spike represent critical failure risks for hydraulic systems, compressors, and transport equipment. As a result, formulators are increasingly deploying composite polymer strategies that combine VGIs with advanced pour point depressants.

Research published in ACS Omega in 2024 demonstrated that terpolymer-based systems and nanoparticle-integrated PPDs can reduce the pour point of waxy base oils by up to 18 degrees Celsius, significantly extending operability in sub-zero conditions. Commercial deployment is accelerating as logistics and energy companies prioritize reliability. Major suppliers such as Shell and ExxonMobil are focusing on high-viscosity-index polymer packages that prevent wax appearance in cold-chain fluids. The use of ethylene-vinyl acetate and specialized acrylate terpolymers has demonstrated up to 75% viscosity reduction at low temperatures, ensuring pumpability during cold starts. Despite broader industry pivots toward decarbonization, continued investment in northern latitude operations sustains a durable niche for advanced VGI technologies capable of maintaining film strength across temperature differentials exceeding 100 degrees Celsius from startup to full operation.

Lubricant Viscosity Grade Improvers Market Share and Segmentation Insights

Olefin Copolymer Technology Leads Viscosity Grade Improvers Market for Modern Engine Oil Formulations

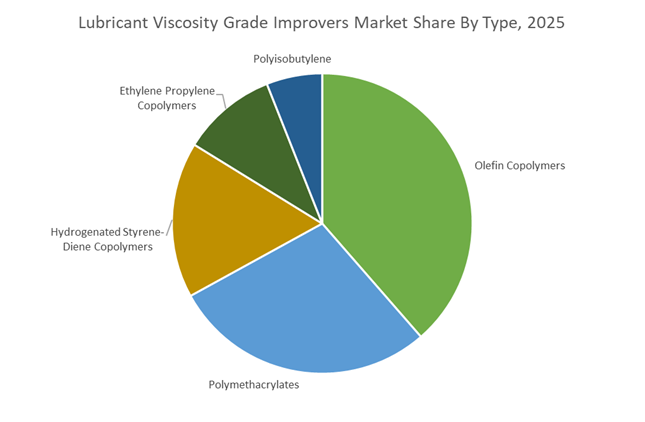

Olefin copolymers (OCP) accounted for 38.60% of the Lubricant Viscosity Grade Improvers Market share in 2025, positioning them as the most widely used polymer technology for controlling lubricant viscosity across temperature ranges. OCP-based viscosity index improvers are extensively used in automotive engine oils, transmission fluids, and industrial lubricants, where they ensure consistent lubrication performance under both cold-start and high-temperature operating conditions. These polymers expand at elevated temperatures to maintain oil film thickness while minimizing viscosity loss during mechanical stress, making them critical for multigrade lubricant formulations used in modern engines and equipment. Olefin copolymers are widely preferred due to their high thickening efficiency, excellent shear stability, and cost-effective production, enabling lubricant formulators to meet stringent industry specifications while maintaining competitive pricing. In 2025, innovation in OCP chemistry has focused on enabling ultra-low viscosity engine oil grades such as 0W-16 and 0W-20, where advanced polymer structures deliver effective thickening performance at lower polymer concentrations while maintaining shear stability and long-term viscosity control in demanding engine environments.

Automotive and Transportation Sector Drives the Largest Demand for Viscosity Grade Improvers

Automotive and transportation applications accounted for 62.80% of the Lubricant Viscosity Grade Improvers Market share in 2025, making the sector the dominant consumer of viscosity control additives globally. Modern vehicles require high-performance lubricant formulations to support engine oils, automatic transmission fluids, gear oils, and drivetrain lubricants, all of which depend on viscosity index improvers to maintain stable lubrication under varying temperature and load conditions. The global fleet of passenger vehicles, commercial trucks, buses, and heavy-duty transportation equipment generates continuous demand for lubricants that meet stringent OEM performance specifications. Viscosity grade improvers ensure lubricants maintain optimal oil film thickness, reduced friction, and reliable protection for engine and transmission components, even under high-shear operating conditions. In 2025, increasing alignment between global lubricant performance standards such as API, ACEA, and ILSAC has encouraged additive manufacturers to develop advanced polymer systems capable of meeting multiple regulatory and OEM specifications simultaneously, enabling lubricant producers to formulate globally standardized products while maintaining consistent performance across diverse automotive markets.

Lubricant Viscosity Grade Improvers Market Competitive Landscape

The lubricant viscosity grade improvers market in 2026 is driven by ultra-low viscosity (0W-8, 0W-12) engine oils, high-shear-stability polymers, and EV-compatible dielectric fluids. Competitive differentiation is centered on precision polymer architecture, dispersant synergy, and stay-in-grade performance under extreme thermal and mechanical stress conditions.

Lubrizol leads dispersant-polymer integration with next-gen OCP viscosity modifiers

The Lubrizol Corporation maintains leadership through advanced olefin copolymer (OCP) technologies engineered for high thickening efficiency and superior low-temperature pumpability aligned with ILSAC GF-7 standards. Its strength in dispersant-viscosity modifiers (DVMs) enables dual-function performance, combining viscosity control with soot handling for extended drain intervals. Expansion in India and localized R&D in Southeast Asia support region-specific lubricant solutions, particularly for high-load urban driving conditions and emerging markets requiring durable, fuel-efficient formulations.

Infineum advances EV-compatible viscosity modifiers with dielectric stability and ultra-low viscosity performance

Infineum International is aligning its polymer innovation with electrification trends, developing viscosity index improvers that maintain stable dielectric properties and corrosion protection in e-axle and battery cooling systems. Its P6188 technology, approved for SAE 0W-20 standards, demonstrates optimized polymer design for friction reduction in modern engines. Expansion of its India blending facility enhances regional supply, while renewable energy integration in polymer synthesis supports OEM-driven green procurement requirements and low-carbon additive production.

Evonik sets benchmark in PMA polymers with high shear stability and energy-efficient lubrication

Evonik Industries leads in polymethacrylate (PMA) viscosity modifiers, delivering high-shear stability and thermal resistance required for precision industrial and automotive applications. Its VISCOPLEX® portfolio enables “fill-for-life” lubricants, reducing maintenance frequency and lifecycle costs. The NUFLUX™ platform enhances hydraulic and gear oil efficiency by maintaining optimal viscosity across wide temperature ranges. With a focus on high-margin comb polymers and resource-efficient materials, Evonik supports energy savings in wind turbines, automated factories, and advanced drivetrain systems.

Afton Chemical develops fuel-flexible viscosity modifiers for hydrogen and GDI engines

Afton Chemical is differentiating through fuel-agnostic additive systems that address emerging hydrogen combustion and high-biofuel environments. Its HiTEC® 12582 additive introduces specialized viscosity modifiers capable of managing water emulsification and thermal stress in hydrogen engines. Expansion of the HiTEC® 5700 series provides flexible OCP and PMA polymer options for global blenders. Strong positioning in gasoline direct injection (GDI) engines ensures compatibility with high-temperature, downsized powertrains, while regional manufacturing integration enhances supply efficiency in Latin America.

Chevron Oronite strengthens OCP performance through PARATONE portfolio and base oil integration

Chevron Oronite leverages its PARATONE® brand to deliver high-performance OCP viscosity modifiers optimized for API SP and GF-6 lubricant categories. Its polymers balance thickening efficiency with low-temperature cranking performance, enabling compliance with ultra-low viscosity grades. Vertical integration with Chevron’s Group II and III base oils allows precise formulation optimization and cost-effective treat rates. Expanded distribution in the Middle East and Africa supports growing demand for high-performance lubricants in developing automotive and industrial markets.

United States: TOP TIER+ Alignment and Electrification-Ready Polymer Architectures

The United States lubricant viscosity grade improvers market is being reshaped by the convergence of tighter gasoline standards, electrification, and sustainability-linked capital allocation. In August 2025, Afton Chemical introduced the HiTEC® 65522 series, the first viscosity modifier–integrated gasoline performance additive approved under the new TOP TIER+™ specification. The formulation directly targets stochastic pre-ignition mitigation in 2026 model-year Gasoline Direct Injection engines, signaling a shift toward multifunctional polymer systems that deliver viscosity control, deposit management, and engine protection within a single additive architecture.

Shear stability under ultra-low viscosity regimes is another defining theme. Chevron Oronite presented new insights in September 2025 on Renewable Resource Base Oil trends, emphasizing next-generation VII polymers engineered to maintain high-temperature high-shear viscosity in 0W-8 and 0W-12 formulations. Feedstock security underpins these advances. Chevron Corporation finalized a multi-year investment program spanning 2025–2026, allocating substantial resources to downstream chemical chains in the Gulf of Mexico and Permian to secure olefin inputs for viscosity modifiers. Sustainability alignment is also accelerating adoption. Following an EcoVadis Gold rating in September 2025, Evonik Industries prioritized the U.S. rollout of Scopeblue polymers, targeting a material reduction in product carbon footprint for heavy-duty engine oil applications by 2026. Electrification adds a further layer, with Afton’s March 2025 debut of its ETF platform introducing high-dielectric viscosity improvers for integrated e-axles in electric truck fleets. Portfolio focus is tightening as well. In December 2025, Mitsubishi Chemical Group completed the transfer of select U.S. additive assets to concentrate on licensing high-performance VI polymers, including those used in advanced cooling fluids for AI data centers.

China: Digital Manufacturing, Emissions Foresight, and Localized Polymer Supply

China’s lubricant viscosity grade improvers landscape is evolving through digitalization mandates, forward-looking emissions compliance, and accelerated localization of polymer supply. In August 2025, the Ministry of Industry and Information Technology released a digital transformation roadmap for machinery and chemical sectors, targeting hundreds of excellence-level smart factories by 2027. Automated blending and real-time quality control for high-precision additive polymers are central to this initiative, directly benefiting VII production efficiency and consistency.

Regulatory anticipation is shaping product design. At its Asia-Pacific Innovation Summit in Shanghai in November 2025, Lubrizol launched Lubrizol® CV1150, a low-ash viscosity modifier engineered to protect diesel particulate filters under forthcoming China VII emission standards. Electrified mobility is further redefining requirements. Lubrizol’s late-2025 introduction of a dedicated PHEV lubricant solution in China addresses frequent stop-start cycles by stabilizing viscosity through multi-component polymer blends that manage water emulsification without sacrificing fuel economy. Supply chain localization is accelerating under the 2025–2026 work plan, with incentives for domestic production of Polymethacrylate and Olefin Copolymer VII chemistries to reduce reliance on imports. Sustainability considerations are also expanding beyond formulations. In November 2025, Lubrizol and Fulai New Material signed a memorandum to co-develop waterborne, low-VOC additive systems, integrating recyclable rheology modifiers aligned with greener industrial lubricant packaging.

Singapore: ASEAN Innovation Anchor and Low-Carbon Additive Logistics

Singapore has consolidated its role as the principal innovation and logistics hub for viscosity grade improvers across Southeast Asia and adjacent markets. In July 2025, Lubrizol inaugurated its Southeast Asia Innovation Center in Jurong, dedicated to local-for-local R&D. The center focuses on tailoring viscosity modifiers to high-humidity, high-temperature operating conditions prevalent across ASEAN industrial corridors, shortening development cycles for regional OEMs.

Manufacturing depth is expanding in parallel. Afton Chemical completed a major expansion of its Jurong Island facility in 2025, enabling domestic production of specialized dispersants and VI improvers previously supplied from North America. Sustainability leadership reinforces Singapore’s strategic value. Infineum reported in late 2025 that its Singapore operations are fully powered by renewable energy, delivering a substantial reduction in Scope 1 and 2 emissions under an ongoing annual sustainability investment program. With robust port and regulatory infrastructure, Singapore was reaffirmed as Afton’s primary additive manufacturing and export gateway in late 2025, serving India and the Middle East during the 2026 cycle.

Germany: Certified Circular Polymers and Energy-Efficiency Benchmarks

Germany continues to set the pace for certified sustainability and polymer engineering rigor in viscosity grade improvers. In October 2025, LANXESS launched an ISCC PLUS–certified version of its Additin RC 2515 at the Mannheim site. Produced with a high share of renewable raw materials, the additive is optimized for viscosity stability in non-ferrous metalworking applications, reflecting rising demand for low-carbon industrial lubricants.

Energy efficiency requirements are sharpening polymer performance criteria. At the UNITI Mineral Oil Technology Congress in April 2025, Chevron Oronite outlined updated high-temperature high-shear benchmarks for gas engines, underscoring how polymer architecture must evolve to meet EU 2026 efficiency mandates. Financing mechanisms are reinforcing this trajectory. In September 2025, Evonik Industries issued a green hybrid bond, allocating capital toward the 2026 rollout of bio-based viscosity modifiers and related membrane technologies, further anchoring Germany’s leadership in sustainable additive innovation.

India: Capacity Expansion and Indigenous Polymer Development

India’s lubricant viscosity grade improvers market is advancing through rapid capacity expansion and ecosystem-level collaboration. In December 2025, Lubrizol reported the doubling of production capacity at its Dahej facility and confirmed progress on a new innovation center to support 2026 demand for high-performance engine oils. This expansion strengthens domestic availability of advanced VI polymers while improving responsiveness to local operating conditions.

Policy-backed innovation frameworks are amplifying these investments. In late 2025, the Indian government announced plans to expand national Science and Technology clusters significantly, creating collaborative platforms for the development of homegrown lithium-free grease thickeners and viscosity modifiers. Strategic partnerships throughout 2025 have extended Lubrizol’s reach into medical and industrial segments, accelerating adoption of polymer technologies such as Noverite™ GP250B that preserve lubricant durability under India’s high ambient temperatures and variable load profiles.

Lubricant Viscosity Grade Improvers Market: Country-Level Strategic Snapshot

Lubricant Viscosity Grade Improvers Market County Level Snapshot

|

Country

|

Primary Strategic Focus

|

Key Developments

|

Strategic Implication

|

|

United States

|

Fuel standards and electrification

|

TOP TIER+ VI integration, ultra-low viscosity stability, e-fluid polymers

|

Multifunctional, low-carbon VII systems gain priority

|

|

China

|

Digitalization and emissions foresight

|

Smart factories, China VII-ready low-ash VIIs, localized PMA and OCP

|

Scale-up of high-precision, compliant polymer supply

|

|

Singapore

|

Regional R&D and logistics

|

ASEAN-focused innovation center, expanded Jurong production, renewables

|

Fast customization and low-carbon regional exports

|

|

Germany

|

Certified sustainability and efficiency

|

ISCC PLUS polymers, EU efficiency benchmarks, green financing

|

Premium circular VI solutions for industrial and OEM use

|

|

India

|

Capacity growth and indigenous innovation

|

Dahej expansion, new S&T clusters, tropicalized formulations

|

Strong domestic base with global-grade polymer development

|

Lubricant Viscosity Grade Improvers Market Report Scope

Lubricant Viscosity Grade Improvers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.8 Billion

|

|

Market Size (2034)

|

$4.5 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Type (Olefin Copolymers, Polymethacrylates, Hydrogenated Styrene-Diene Copolymers, Polyisobutylene, Ethylene Propylene Copolymers), By Physical Form (Solid Concentrates, Liquid Solutions), By Application (Automotive Engine Oils, Gear and Transmission Fluids, Industrial Lubricants, Greases), By End-Use Industry (Automotive and Transportation, Manufacturing and Construction, Power Generation and Energy, Marine and Aerospace, Mining and Agriculture)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Lubrizol Corporation, Infineum International, Chevron Oronite, Afton Chemical, Evonik Industries, Sanyo Chemical Industries, LANXESS, BASF, Mitsui Chemicals, Richful Lube Additive, Eni, Nouryon, Vanderbilt Chemicals, Nippon Oil and Energy, Dover Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Lubricant Viscosity Grade Improvers Market Segmentation

By Type

- Olefin Copolymers

- Polymethacrylates

- Hydrogenated Styrene-Diene Copolymers

- Polyisobutylene

- Ethylene Propylene Copolymers

By Physical Form

- Solid Concentrates

- Liquid Solutions

By Application

- Automotive Engine Oils

- Gear and Transmission Fluids

- Industrial Lubricants

- Greases

By End-Use Industry

- Automotive and Transportation

- Manufacturing and Construction

- Power Generation and Energy

- Marine and Aerospace

- Mining and Agriculture

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Lubricant Viscosity Grade Improvers Market

- Lubrizol Corporation

- Infineum International

- Chevron Oronite

- Afton Chemical

- Evonik Industries

- Sanyo Chemical Industries

- LANXESS

- BASF

- Mitsui Chemicals

- Richful Lube Additive

- Eni

- Nouryon

- Vanderbilt Chemicals

- Nippon Oil and Energy

- Dover Chemical

*- List not Exhaustive