Luxury Vinyl Tiles Market Overview – Growth, Value, and Key Industry Insights

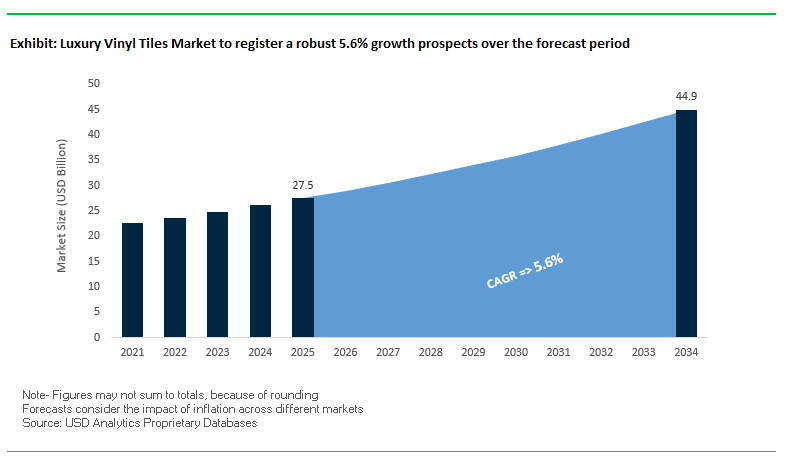

The global Luxury Vinyl Tiles (LVT) market is set to expand from $27.5 billion in 2025 to $44.9 billion by 2034, registering a steady CAGR of 5.6%. This sustained growth is driven by design innovation, sustainability commitments, and rising adoption across both residential and commercial sectors. The market has transitioned from being utility-focused to design-led, with Embossed-in-Register (EIR) technology now widely adopted to replicate natural surfaces like wood, stone, and ceramic with remarkable realism.

Durability and performance are critical in driving LVT adoption. With enhanced wear layers, LVT products offer resistance to scratches, scuffs, and stains, making them ideal for kitchens, offices, and retail spaces. The ease of installation is another growth enabler, with advanced click-lock and loose-lay systems aligning with the surge in DIY home renovation projects worldwide. Furthermore, the green building movement has accelerated demand for LVT with low-VOC and recyclable options, aligning with sustainability certifications such as LEED and consumer focus on healthier indoor environments.

Key Insights at a Glance

- Market Value Growth: $27.5B in 2025 → $44.9B by 2034 (CAGR 5.6%).

- Design-Driven Demand: EIR technology enables ultra-realistic wood, stone, and ceramic finishes.

- Performance Edge: Scratch-, stain-, and scuff-resistant surfaces support high-traffic installations.

- DIY-Friendly: Click-lock and loose-lay systems reduce installation costs and timelines.

- Sustainability: Rising adoption of PVC-free, recyclable, and low-VOC LVT for green building certifications.

Market Analysis – Recent Industry Developments and Strategic Trends

The Luxury Vinyl Tiles market is undergoing rapid innovation, with companies launching sustainable flooring lines, enhancing digital retail strategies, and investing in next-generation installation systems. A key development came in April 2025, when Shaw Industries won a 2025 Edison Award for its PVC-free, recyclable EcoWorx™ Resilient Flooring, signaling a major push toward circular flooring solutions. Similarly, in March 2025, Karndean Designflooring introduced Karndean Design Aesthetics, an initiative aimed at enhancing consumer shopping journeys with boutique-style, customizable experiences.

Financial and operational restructuring is also shaping the market. In May 2025, Mohawk Industries reported net earnings of $73 million for Q1, emphasizing restructuring efforts designed to streamline operations and generate $100 million in benefits by the end of 2025. Parallel to this, Shaw Floors leveraged its brand presence by returning as the official sponsor of the College Football Playoff in January 2025, reaffirming its strong consumer marketing strategies.

Sustainability remains a cornerstone for LVT manufacturers. In August 2025, Shaw Industries’ Kellie Ballew was recognized among North America’s Top 100 Chief Sustainability Officers by the IWBI, underscoring leadership in environmental stewardship. Meanwhile, industry analysts reported in August 2025 that the rigid LVT segment is projected to reach $9.2 billion by 2034, driven by rising demand for durable, moisture-resistant products suitable for high-traffic commercial and residential areas.

Emerging Trends and Strategic Opportunities Shaping the Global Luxury Vinyl Tiles Market

Accelerated Investment in Domestic and Regional Manufacturing Capacity

The Luxury Vinyl Tiles (LVT) market is witnessing a significant shift toward regional and domestic production, driven by the need to mitigate supply chain risks, rising logistics costs, and global trade uncertainties. Major manufacturers are strategically investing in new production facilities in North America and Europe, moving away from the traditional Asia-centric manufacturing model. For example, a leading manufacturer is building a $120 million LVT plant in Georgia, U.S., reflecting the strategic emphasis on domestic investment. This reshoring trend allows companies to reduce lead times and shipping costs, exemplified by Armstrong Flooring’s “Quick Ship” LVT collection, which ensures delivery within 5–10 business days. Additionally, regional production protects manufacturers from the volatility of tariffs and international trade policies, offering greater cost predictability. Government incentives, including tax credits and grants in regions supporting domestic manufacturing, further encourage these strategic investments, ensuring the LVT sector remains resilient and responsive to evolving market demands.

Rigorous Focus on Material Health and Transparency

Consumer awareness and green building regulations are driving a shift toward healthier, transparent LVT materials, with manufacturers prioritizing phthalate-free formulations and third-party certifications. Many LVT products now carry ASSURE CERTIFIED™ and FloorScore® certifications, ensuring low VOC emissions and adherence to stringent indoor air quality standards. Companies like Therdex are leading in phthalate-free innovations using organic, soy-based plasticizers, while projects under LEED and other green building standards increasingly specify low-emission, verified flooring materials. The emphasis on Material Health Declarations (HPDs) and Environmental Product Declarations (EPDs) ensures that LVT products meet rigorous environmental and safety requirements, making them attractive for architects, designers, and eco-conscious consumers. This trend not only enhances product credibility but also supports sustainable building initiatives across residential, commercial, and institutional segments.

Development of Advanced Closed-Loop Recycling and End-of-Life Programs

The LVT market has a significant opportunity to strengthen its circular economy credentials by implementing take-back and recycling programs. Leading initiatives, such as Tarkett’s ReStart® program, provide a hassle-free method for collecting used flooring and diverting it from landfills. Advancements in both mechanical and chemical recycling enable manufacturers to convert post-consumer and post-industrial vinyl waste into high-quality new products. Additionally, designing “circular-ready” flooring solutions, such as those by Forbo, allows for easier disassembly and recycling at the product’s end-of-life, ensuring sustainable material recovery. These initiatives align with Extended Producer Responsibility (EPR) regulations and offer manufacturers a competitive edge while contributing to environmental stewardship and reduced waste.

Integration of Digital Tools for Specification, Installation, and Visualization

Digital transformation presents a lucrative growth avenue for LVT manufacturers through the adoption of Building Information Modeling (BIM), digital twins, and augmented reality (AR) tools. Providing high-resolution digital assets as Revit families or BIM objects enables architects and designers to embed LVT products accurately in project plans, streamlining the specification process. AR visualization tools allow stakeholders to preview LVT designs in real-world settings, enhancing confidence in product selection. Additionally, digital installation and maintenance guides offered via apps or websites improve installation accuracy and product longevity, as demonstrated by companies like Daltile. This integration of technology not only facilitates early specification locking but also enhances the overall user experience, positioning digital-savvy manufacturers as industry leaders in innovation and service excellence.

Competitive Landscape – Leading Players Driving the Luxury Vinyl Tiles Market

The global LVT market is highly competitive, with leading companies driving growth through sustainable product innovations, advanced installation technologies, and global brand expansion. Key players include Tarkett S.A., Mohawk Industries, Shaw Industries, Forbo Group, and Mannington Mills. Each company differentiates itself through unique sustainability strategies, product portfolios, and operational strengths, making the competitive landscape dynamic and innovation-driven.

Tarkett S.A. – Sustainability and Innovation at Scale

Tarkett is a global pioneer in flooring solutions, offering LVT with advanced designs and performance features. Under its impacT 2027 strategy, the company emphasizes customer experience, sustainability leadership, and innovative design. Its Cradle to Cradle-certified products reinforce circular economy commitments, enabling disassembly and reuse to reduce waste. With a strong integration of global scale and localized expertise, Tarkett continues to shape the premium LVT market with design-forward, eco-friendly solutions.

Mohawk Industries, Inc. – Operational Restructuring and Vertical Integration

Mohawk remains one of the world’s largest flooring companies, with a strong LVT portfolio recognized for durability and ease of installation. In Q1 2025, Mohawk highlighted restructuring initiatives expected to generate $100 million in operational savings by year-end. Its vertically integrated model gives it control across the supply chain, allowing faster product rollouts and competitive pricing, particularly in U.S. markets. Mohawk’s focus on simplifying operations and expanding design-driven products solidifies its position as a key player.

Shaw Industries Group, Inc. – Innovation Through Sustainability

A Berkshire Hathaway subsidiary, Shaw Industries leads with sustainability at its core. Its EcoWorx™ Resilient Flooring earned a 2025 Edison Award, showcasing its role in sustainable innovation. The company’s sustain[HUMAN]ability® strategy combines environmental stewardship with product excellence, making Shaw a frontrunner in eco-conscious flooring. With brand investments such as sponsoring the College Football Playoff, Shaw strengthens its consumer visibility while expanding its advanced LVT offerings for both residential and commercial markets.

Forbo Group – Acoustic and Functional Design Leadership

Forbo has carved a niche with its Allura LVT brand, renowned for versatile designs and strong sustainability focus. Recent innovations like the Allura Decibel acoustic LVT and Allura Click Flexcore highlight its commitment to functionality, offering superior sound reduction and installation flexibility without adhesives. With a balance of design freedom and high-performance flooring solutions, Forbo remains a trusted choice in the commercial and residential segments.

Mannington Mills, Inc. – Tradition Meets Modern Innovation

Mannington, a century-old brand, is known for its ADURA® LVT collection, blending durability and stylish design. In 2025, the company launched new ADURA® products tailored to consumer demand for high-performance, aesthetically refined flooring. Mannington emphasizes domestic manufacturing, reinforcing its Made in the USA advantage for supply chain reliability and quality assurance. Its heritage, combined with ongoing innovation, positions it as a strong competitor in the global LVT landscape.

Luxury Vinyl Tiles Market Share Insights

Rigid Core LVT Dominates Market Share by Product Type in the Luxury Vinyl Tiles Industry

Rigid core luxury vinyl tiles (LVT), encompassing stone plastic composite (SPC) and wood plastic composite (WPC), command an overwhelming 72% share of the global LVT market. Their dominance reflects their unmatched combination of dimensional stability, indentation resistance, and DIY-friendly click-lock installation systems that make them the default choice for both homeowners and contractors. Rigid core formats not only displace traditional sheet vinyl and laminate but are increasingly competing with ceramic tiles and hardwood, especially in high-moisture zones like kitchens, bathrooms, and basements. Their widespread adoption is further fueled by aesthetic versatility, superior performance in floating installations, and compatibility with underfloor heating systems, reinforcing their position as the industry’s growth engine.

Residential Sector Leads Market Share by Application in the Luxury Vinyl Tiles Market

The residential segment contributes 65% of global LVT demand, making it the primary driver of industry expansion. Homeowners increasingly favor LVT for its ability to mimic premium materials like natural wood and stone at lower cost, while offering waterproofing and durability advantages. Rising renovation activity and new housing construction—particularly in North America, Europe, and Asia-Pacific—are accelerating adoption. Importantly, the DIY installation potential of rigid core LVT has opened the market to a broader consumer base, enabling retailers to capture share through home improvement stores and online platforms. By combining performance, affordability, and visual appeal, residential demand has become the anchor for long-term market growth.

United States Luxury Vinyl Tiles Market Accelerates Through Low-VOC Innovations and Reshoring Initiatives

The U.S. luxury vinyl tiles (LVT) market is strongly shaped by stringent environmental regulations, with the EPA and state-level air quality boards driving the shift toward phthalate-free and low-VOC formulations. Technological advancements in digital printing and rigid core LVT technology are enhancing realism and durability, with Shaw Industries investing $90 million to more than double resilient flooring output by 2026.

Corporate investments are focused on reshoring production to mitigate supply chain risks, exemplified by Mohawk Industries’ SolidTech Essentials line, which emphasizes quality and domestic manufacturing. Key applications include residential renovations, remodeling, and DIY installations, while commercial sectors like healthcare, hospitality, and retail are increasingly adopting LVT due to its durability, low maintenance, and design versatility. Sustainability remains central, with products like Shaw Industries’ EcoWorx™ resilient flooring winning accolades for circular design innovation and recyclable materials.

Germany’s LVT Market Leads in Circular Economy and High-Performance Flooring Solutions

Germany’s luxury vinyl tiles market operates under strict EU REACH regulations, encouraging the adoption of low-VOC, phthalate-free formulations. German manufacturers are leaders in technological innovation, with initiatives such as the Circular Flooring Project promoting recycling and reducing waste. Products are increasingly designed for easy end-of-life de-inking and recyclability, meeting the sustainability expectations of commercial developers and environmentally conscious consumers.

Corporate investments in high-performance LVT solutions support compliance with stringent environmental regulations while catering to demand for durable and sustainable flooring. Germany’s focus on the circular economy has positioned the market as a hub for eco-friendly resilient flooring innovations, driving adoption in both residential and commercial projects.

China’s LVT Market Benefits From Green Policies and Domestic Manufacturing Expansion

China’s luxury vinyl tiles market is heavily influenced by governmental initiatives under the dual-carbon goal, with over CNY 2.6 trillion allocated to urban renewal projects, providing significant opportunities for durable, sustainable LVT flooring. Regulatory reforms are pushing manufacturers toward low-VOC standards, while innovations like rigid planks with antimicrobial coatings are gaining traction in healthcare and aged-care sectors.

Technological advancements in digital printing and extrusion lines have improved efficiency and product realism, reducing ex-factory costs. The focus on domestic manufacturing supports substitution for imported products, with local companies expanding production capacity to meet the booming residential and commercial renovation demand, positioning China as a rapidly growing hub for high-quality, circular LVT solutions.

India’s LVT Market Expands With Smart Cities Initiatives and Advanced Flooring Technologies

India’s luxury vinyl tiles market is experiencing growth driven by the Make in India initiative and Smart Cities programs, which promote modern, sustainable building materials. Technological innovations focus on realistic wood and stone imitations, enhanced water resistance, and scratch durability, with thicker planks providing improved acoustic insulation for urban living spaces.

Corporate investments are increasing to establish new production facilities, supporting the rise of modular construction and prefabricated components, which simplify LVT installation in large-scale residential and commercial projects. Rising disposable incomes and urbanization are fueling adoption in the residential and commercial construction sectors, making India a key growth market for high-performance, easy-to-maintain LVT flooring.

Japan’s LVT Market Drives Innovation With Antimicrobial and High-Performance Flooring

Japan’s luxury vinyl tiles industry leverages advanced precision manufacturing, with brands like Sangetsu and Tajima leading innovation in antimicrobial vinyl flooring. Sales of antimicrobial LVT grew by 45% between 2020 and 2022, highlighting rising consumer and institutional demand. Regulatory policies encouraging low-VOC and green-certified products have further spurred innovation in safe and sustainable flooring solutions.

Major players focus on specialty and value-added LVT products, including antibacterial, wax-free, and hypochlorous acid-resistant vinyl sheets suitable for high-traffic commercial and healthcare environments. Innovations in functionality, such as acoustic insulation and durability, combined with the trust associated with the “Made in Japan” label, reinforce Japan’s position as a premium market for resilient, high-quality LVT solutions.

Brazil’s LVT Market Sees Growth Through Sustainable Materials and Moisture-Resistant Solutions

Brazil’s luxury vinyl tiles market is supported by the National Solid Waste Policy, which encourages sustainable construction practices. Technological advancements focus on durable, cost-effective, and aesthetically pleasing LVT, with inkjet printing technology enabling realistic replication of tropical hardwoods and regional stones at lower installation costs.

Corporate investments in local manufacturing facilities reduce reliance on imports and strengthen the domestic supply chain. LVT adoption is rising in the residential and commercial sectors, with products valued for moisture resistance in tropical climates. Increasing urbanization and middle-class growth are driving demand for modern, resilient, and easy-to-maintain flooring solutions, positioning Brazil as an emerging market in the global LVT landscape.

Luxury Vinyl Tiles Market Report Scope

Luxury Vinyl Tiles Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$27.5 Billion

|

|

Market Size (2034)

|

$44.9 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Product Type (Rigid Core LVT, Flexible LVT), By Application (Residential, Commercial), By Installation Method (Click-Lock, Glue-Down, Loose Lay, Peel & Stick)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mohawk Industries, Inc., Shaw Industries Group, Inc., Tarkett S.A., Armstrong Flooring, Inc., Mannington Mills, Inc., Gerflor Group, Forbo Flooring Systems, Karndean International LLC, Beaulieu International Group, IVC Group (part of Mohawk Industries), B.I.G. (Belgian International Group), Metroflor Corporation, Congoleum Corporation, Novalis Innovative Flooring, CFL Flooring

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Luxury Vinyl Tiles Market Segmentation

By Product Type

- Rigid Core LVT

- Flexible LVT

By Application

By Installation Method

- Click-Lock

- Glue-Down

- Loose Lay

- Peel & Stick

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Luxury Vinyl Tiles Market

- Mohawk Industries, Inc.

- Shaw Industries Group, Inc.

- Tarkett S.A.

- Armstrong Flooring, Inc.

- Mannington Mills, Inc.

- Gerflor Group

- Forbo Flooring Systems

- Karndean International LLC

- Beaulieu International Group

- IVC Group (part of Mohawk Industries)

- B.I.G. (Belgian International Group)

- Metroflor Corporation

- Congoleum Corporation

- Novalis Innovative Flooring

- CFL Flooring

* List Not Exhaustive

Methodology

The research methodology for the global Luxury Vinyl Tiles (LVT) market integrates both primary and secondary research approaches to provide actionable insights for industry professionals. Primary research involved structured interviews with flooring manufacturers, product designers, sustainability officers, and construction sector experts to capture first-hand perspectives on material innovations, installation technologies, digital visualization tools, and sustainability strategies. Secondary research comprised comprehensive analysis of company reports, trade publications, regulatory frameworks, market news, and financial disclosures to validate market trends, growth drivers, and regional developments. Market sizing, CAGR estimations, and segment forecasts were developed using a combination of top-down and bottom-up approaches, incorporating product type, application, installation method, and regional factors. Special focus was placed on trends like Embossed-in-Register (EIR) design adoption, low-VOC and phthalate-free formulations, rigid core dominance, and digital tools integration for design and installation. The methodology ensures that USDAnalytics delivers precise, data-driven insights into the global LVT market, covering performance, sustainability, and technology-led innovation.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.