Market Overview: High-Decomposition MDH, LSZH Adoption, and High-Purity Demand Reshape the Global Magnesium Hydroxide Market

The Magnesium Hydroxide Market is increasingly emerging as a specification-driven materials market, anchored in non-halogenated flame retardancy, safer wastewater neutralization, and rising demand for high-purity engineered grades in electronics and energy systems. While absolute market size figures vary by application, the market’s structural attractiveness is defined less by volume growth and more by regulatory pull, processing advantages, and substitution economics versus legacy chemistries.

A primary driver is thermal performance differentiation. Magnesium Hydroxide (MDH) decomposes in the 340-490°C range, approximately 100°C higher than aluminum hydroxide (ATH). Today, this higher decomposition threshold is becoming decisive as polymer processors move toward higher-temperature resins and faster cycle times. MDH allows polypropylene (PP), polyethylene (PE), and engineering plastics to be processed at elevated temperatures without premature decomposition, preserving flame-retardant effectiveness while maintaining mechanical properties. As polymer compounding becomes more performance-intensive, MDH is increasingly specified not as an alternative, but as a processing enabler.

Regulatory pressure around fire safety and smoke toxicity is accelerating demand structurally. LSZH (Low Smoke Zero Halogen) standards are now embedded across European construction codes, rail and metro systems, data centers, tunnels, and high-occupancy buildings. In these environments, halogenated flame retardants are no longer acceptable. MDH has become a core mineral FR for LSZH cable compounds, where achieving UL-94 V-0 ratings typically requires 50-60 phr loadings. This, in turn, is shifting demand toward surface-modified and particle-engineered MDH grades that enable high filler loadings without unacceptable viscosity, brittleness, or loss of tensile strength.

Beyond polymers, wastewater treatment is reinforcing MDH’s industrial relevance. Municipalities and industrial operators are increasingly replacing caustic soda with MDH due to its mild alkalinity, safer handling profile, and reduced corrosion risk. In biological treatment systems, MDH provides controlled pH adjustment that supports microbial activity; field data shows BOD removal improvements of approximately 30% when MDH is integrated into treatment regimes. As water utilities focus on operator safety, infrastructure longevity, and compliance reliability, MDH is shifting from a niche neutralizing agent to a preferred long-term chemistry.

The market’s highest growth vector lies in high-purity magnesium hydroxide. Synthetic precipitation routes are enabling >99% purity MDH, unlocking advanced applications where impurity control is critical. These grades are increasingly specified in semiconductor encapsulation, electronic insulation systems, and lithium-ion battery components (including separators and safety layers). Demand for these ultra-pure grades is expanding at >20% year-on-year, driven by electrification, miniaturization, and stricter contamination thresholds in electronics manufacturing.

From a strategic standpoint, the magnesium hydroxide market is transitioning from a bulk mineral business to a formulation- and purity-driven specialty materials market. Competitive advantage is shifting toward producers that can deliver consistent particle morphology, surface treatment capability, high-purity synthesis, and application-specific technical support. As LSZH mandates tighten, polymer processing temperatures rise, and electronics purity standards advance, MDH is becoming a non-substitutable material input across multiple regulated industries.

Market Analysis: Flame-Retardant Expansion, High-Purity MDH Pilots, and Regulatory Shifts Drive Momentum

The Magnesium Hydroxide Industry experienced significant scale-ups, regulatory tailwinds, and material innovations. In October 2025, Martin Marietta Magnesia Specialties introduced a new generation of surface-treated magnesia slurries optimized for municipal wastewater pH control-highlighting the sector’s focus on high-dispersion, reactive MDH formulations. Capacity expansion accelerated further in July 2025, when Russia’s CJSC NikoMag completed its ramp-up from 25,000 to 40,000 t/year, specifically targeting Europe’s non-halogenated flame-retardant sector, which is undergoing structural growth due to LSZH cable mandates and stricter building codes. Business expansion also continued regionally with POSCO Chemical’s May 2025 announcement to build a new MDH manufacturing plant in Vietnam, strategically positioned to supply the rapidly growing Southeast Asian electronics and construction sectors shifting away from halogenated additives.

Regulatory changes are reshaping global adoption patterns. In March 2025, the European Commission issued new guidelines restricting halogenated flame retardants in public transport cable systems, prompting a surge in MDH-based LSZH compound development. The technology frontier advanced in January 2025, when researchers demonstrated a synergistic system enabling UL-94 V-0 performance in epoxy resins with only 5% MDH loading, a breakthrough that challenges historical assumptions of high additive loading. Specialty and food-grade applications expanded as well-Nedmag’s November 2024 launch of high-purity MDH powder certified for E528 food use highlights rising demand from nutraceuticals and pharmaceuticals.

The consolidation wave continued with Huber Engineered Materials’ September 2024 acquisition of MAGNIFIN Magnesiaprodukte, strengthening its European production foothold in specialty MDH powders. In parallel, India’s August 2024 investment in precipitation technology for high-purity MDH reflects global efforts to support FGD installations and environmental compliance.

Magnesium Hydroxide Market Trends and Opportunities

Trend 1: Shift to Magnesium Hydroxide Slurry in Marine Scrubber Systems

The global maritime sector is steadily moving away from caustic soda–based scrubbing systems toward magnesium hydroxide (Mg(OH)₂) slurry, reflecting a broader re-prioritization of operational safety, chemical logistics, and long-term compliance risk. One of the most decisive factors behind this shift is the superior neutralization efficiency and volumetric advantage of high-solids Mg(OH)₂ slurry. In operational terms, industry data from 2025 shows that roughly 0.6 kg of 60% Mg(OH)₂ slurry delivers the same hydroxide availability as 1.0 kg of 50% NaOH, allowing shipowners to reduce onboard chemical storage volumes—an especially critical constraint for container vessels, VLCCs, and LNG carriers. This advantage is amplified by the non-hazardous classification of magnesium hydroxide. Unlike caustic soda, Mg(OH)₂ is non-ADR and self-buffering, with a maximum equilibrium pH of around 10, materially reducing crew exposure risks and eliminating the possibility of accidental over-alkalization during discharge. Regulatory developments are further accelerating adoption. Following the IMO MEPC 82 session, the expansion of Emission Control Areas to include the Canadian Arctic and the Norwegian Sea from March 2026 has triggered a new retrofit cycle, particularly among vessels operating in environmentally sensitive waters. Here, Mg(OH)₂’s lower scaling tendency in seawater and reduced fouling of scrubber internals translate directly into lower maintenance downtime and higher system availability compared to lime or caustic systems. Collectively, these factors are repositioning magnesium hydroxide slurry from a niche alternative into the default chemical standard for next-generation marine exhaust gas cleaning systems.

Trend 2: High-Purity, Nano-Particulate Grades for Precision Process Industries

Beyond bulk environmental applications, the magnesium hydroxide market is experiencing a rapid move toward high-purity and nano-engineered grades tailored for advanced process industries where chemical precision directly impacts yield and performance. A prime example is the lithium extraction ecosystem, particularly Direct Lithium Extraction (DLE) technologies, where Mg(OH)₂ plays a critical role in pH stabilization during selective precipitation. Recent 2025 pilot studies and patent filings demonstrate that maintaining pH tightly within the 10.1–10.4 range using magnesium hydroxide significantly reduces lithium losses to the filtrate, pushing recovery yields beyond 90%—a material improvement over lime- or caustic-based systems that tend to overshoot and destabilize brine chemistry. Parallel innovation is unfolding in polymer engineering and advanced materials. Nano-particulate Mg(OH)₂ developed in 2024–2025 shows up to 40% higher dispersion efficiency in polymer matrices, enabling uniform flame retardancy and smoke suppression at lower filler loadings. Controlled trials indicate smoke density reductions of roughly 33% in high-spec plastics, making nano-Mg(OH)₂ increasingly attractive for aerospace interiors, semiconductor cleanroom components, and specialty cable insulation. This technological migration toward engineered grades is reshaping supply dynamics. By Q3 2025, high-purity Mg(OH)₂ prices rose sharply—approaching $800/MT in the U.S. and over $1,000/MT in Brazil—reflecting both capacity rationalization at major production sites and surging demand from lithium processing hubs and flame-retardant compounders. The result is a market increasingly bifurcated between bulk commodity applications and high-margin, specification-driven specialty segments.

Opportunity 1: Compliance-Driven Wastewater Neutralization Under Tightened Regulations

Stricter wastewater discharge regulations across mining, power generation, and heavy industry are creating a structurally durable opportunity for magnesium hydroxide as a predictable, compliance-oriented neutralization agent. Under the EPA’s Strategic Plan 2022–2026, enforcement of industrial effluent standards intensified through 2024–2025, culminating in updated Power Plant Effluent Limitation Guidelines that effectively mandate zero-discharge or near-zero discharge outcomes for several pollutant categories. In this regulatory environment, Mg(OH)₂ is increasingly favored over caustic soda because its slower dissolution kinetics generate larger, denser flocs during heavy-metal precipitation. These flocs are easier to dewater and filter, directly improving solids handling efficiency. Field data from 2025 mining operations shows that magnesium hydroxide–based systems can reduce sludge hauling and disposal costs by up to 20% compared with lime, which often produces voluminous calcium carbonate scales that foul pipelines and clarifiers. Additionally, Mg(OH)₂’s buffering behavior is particularly valuable for facilities employing biological treatment stages. By preventing sudden pH excursions, it protects microbial populations in anaerobic digesters and secondary treatment systems, ensuring consistent nutrient removal even during acidic influent spikes. As regulators increasingly scrutinize both effluent quality and operational resilience, magnesium hydroxide is emerging as a risk-mitigation chemical rather than a simple reagent, reinforcing its long-term role in industrial water treatment.

Opportunity 2: Flame Retardant and Smoke Suppressant for EV and E-Mobility Systems

The electrification of transport is opening a high-growth downstream opportunity for magnesium hydroxide as a halogen-free flame retardant and smoke suppressant in electric vehicle (EV) components. Battery enclosures, cable insulation, and connector housings are now engineered to withstand extreme thermal events while complying with increasingly stringent fire safety standards such as UL-94 V0 and ECE R100. Magnesium hydroxide is particularly well suited to this role because it decomposes endothermically at 330–340°C, absorbing heat and releasing water vapor that cools the polymer matrix and dilutes flammable gases during thermal runaway scenarios. This decomposition temperature is significantly higher than that of alumina trihydrate (ATH), which begins to break down around 200°C, limiting ATH’s usability in high-temperature engineering plastics common in EV platforms. As a result, magnesium hydroxide usage in EV-related flame-retardant systems increased by an estimated 18% during 2024–2025, according to industry assessments. Regulatory alignment further reinforces this trend. More than 60% of industrial users have transitioned away from halogenated flame retardants to comply with EU REACH and parallel global toxicity regulations. Within newly developed halogen-free systems, magnesium hydroxide now accounts for over half of all formulations, with Asia-Pacific—particularly Japan and China—driving innovation in nano-engineered grades. As EV architectures continue to evolve toward higher energy densities and stricter safety validation, magnesium hydroxide is becoming a core functional material embedded directly into next-generation mobility platforms rather than an optional additive.

Market Share Analysis: Magnesium Hydroxide Market

Market Share by Grade: Industrial / Technical Magnesium Hydroxide Locks in Volume Leadership Through Cost-Critical Applications

Industrial-grade magnesium hydroxide accounts for approximately 58% of global volume and over 76% of market revenue, reflecting its structural entrenchment in large-scale, cost-sensitive applications rather than specialty chemistry niches. Its dominance is anchored in infrastructure and environmental projects where procurement decisions are driven by throughput reliability, handling safety, and total lifecycle cost. Industrial Mg(OH)₂ has emerged as the preferred alkaline agent for wastewater neutralization and flue-gas desulfurization because its self-buffering behavior at pH ~10.5 eliminates the operational risks associated with caustic soda overdosing, reducing plant downtime and compliance exposure. From a materials-processing perspective, its 330°C thermal stability threshold—validated by suppliers such as Huber Advanced Materials—allows polymer compounders to run higher processing temperatures than Alumina Trihydrate, unlocking faster cycle times and broader resin compatibility. The segment’s revenue skew is further reinforced by regional price dispersion—USD 465/MT in China versus USD 780/MT in the U.S. (Q1 2025)—which has elevated industrial-grade Mg(OH)₂ into a strategic sourcing material rather than a commoditized filler. Scale is the final moat: global trade volumes exceeded 1.1 million tons in late 2024, with exporters such as Nedmag and Huber operating at capacities that smaller specialty producers cannot replicate. Collectively, these factors explain why industrial/technical grades remain the market’s economic backbone despite faster growth in niche formulations.

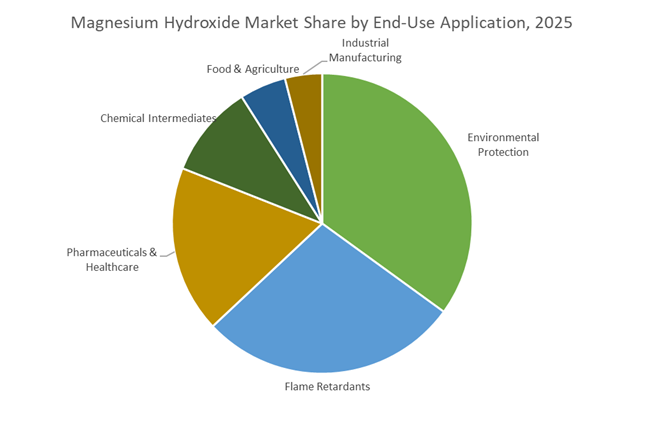

Market Share by Application: Environmental Protection Drives Non-Discretionary Demand and Regulatory Lock-In

Environmental protection represents around 35% of magnesium hydroxide demand, making it the single largest application segment and the most resilient to economic cycles. This share is sustained by regulatory compulsion rather than discretionary consumption: wastewater treatment plants, power utilities, and maritime operators increasingly favor magnesium hydroxide because it combines safe alkalinity, non-hazardous handling, and regulatory compliance in a single input. Technical bulletins from Nedmag and Martin Marietta highlight that Mg(OH)₂’s buffering ceiling prevents biological shock in activated-sludge systems—a critical operational advantage as environmental discharge limits tighten across North America and Europe. The application base expanded materially in 2025 with the rise of marine exhaust gas scrubbers, where magnesium hydroxide is replacing sodium-based reagents due to its non-corrosive behavior and safer onboard storage; Nedmag’s MH53S (Mare) rollout underscores how maritime decarbonization has become a demand multiplier. Parallel to this, environmental regulation is converging with materials policy: 62% of new halogen-free flame-retardant systems now incorporate Mg(OH)₂, positioning environmental compliance and fire safety as mutually reinforcing demand drivers. Even incremental innovation—such as nano-dispersed grades delivering 40% higher dispersion efficiency and 33% lower smoke density—feeds back into environmental and EV-related safety standards, locking magnesium hydroxide deeper into regulatory-driven procurement. This combination of mandatory use cases, safety advantages, and cross-sector applicability explains why environmental protection continues to anchor market share in 2025.

Competitive Landscape: Specialty Additive Leaders and High-Purity MDH Producers Expand Global Capacity

The Magnesium Hydroxide competitive landscape is defined by strategically integrated chemical companies that combine ore access, synthetic precipitation expertise, and specialization in flame-retardant or environmental formulations. Global players are investing in ultrafine MDH, surface-modified grades, and high-purity products to meet accelerating demand in LSZH cables, semiconductor materials, pharmaceutical ingredients, and wastewater treatment systems. Control of feedstock, ability to refine particle morphology, and regulatory-certified production are key differentiators.

Huber Engineered Materials - Specialty Flame-Retardant MDH Leader With European Expansion Strength

Huber Engineered Materials (HEM) holds a dominant position in the non-halogenated flame-retardant additives market, offering a comprehensive portfolio of treated and untreated MDH grades via its Martinswerk division. The company strengthened its European presence through the full acquisition of MAGNIFIN, providing high-quality MDH powders for demanding polymer applications. Its R&D strategy emphasizes ultra-fine, sub-micron MDH particles to reduce required loadings and preserve mechanical properties in LSZH compounds. HEM’s automotive-grade MDH products are certified for EV battery casings and thermal management components, meeting stringent fire performance standards.

Martin Marietta Magnesia Specialties - Vertically Integrated Magnesia Producer Advancing Wastewater and FGD MDH Applications

Martin Marietta leverages secure access to high-purity magnesite ore deposits in the U.S., ensuring high-consistency MDH supply for industrial and environmental markets. Its MagSorp® MDH slurry is widely used across municipal wastewater treatment facilities due to its high reactivity and predictable pH-control characteristics. The company is also a major supplier of MDH for flue gas desulfurization systems, benefiting from the industry’s shift away from lime-based scrubbers. Additionally, Martin Marietta provides pharmaceutical- and food-grade MDH, meeting USP and FCC standards for antacids and supplements.

Nedmag B.V. - Brine-Based High-Purity Magnesium Hydroxide Producer For Flame-Retardant and Specialty Markets

Nedmag utilizes ancient seawater brine deposits in the Netherlands to produce exceptionally pure MDH with minimal trace metals-an important requirement for high-performance flame-retardant and insulation materials. Its product lineup supports applications such as drilling fluids, cement slurries, and high-temperature pH control environments. Nedmag continues to advance sustainable production practices, optimizing energy efficiency in brine extraction and processing, an attribute valued by green construction and electronics manufacturers seeking low-impurity MDH.

Kyowa Chemical Industry - Surface-Engineered MDH Leader For Advanced Polymer Additives

Kyowa Chemical is known globally for precision-engineered synthetic MDH produced via specialized precipitation methods, allowing tight control over particle size and morphology. Its Magnifine® series includes surface-treated MDH with superior dispersibility in polymer matrices, enabling formulators to maintain mechanical properties at high loading levels. Kyowa’s R&D focus includes composite flame-retardant systems combining MDH with other metal hydroxides for high-performance coatings and engineering plastics. The company is also a key supplier of MDH used as acid scavengers and heat stabilizers in the electronics and polymer processing sectors.

The United States continues to dominate the high-purity synthetic magnesium hydroxide market, with 2025 marked by decisive consolidation and pricing discipline aimed at securing domestic supply chains for halogen-free flame retardants (HFFR), aerospace polymers, and infrastructure materials. The most consequential development was Martin Marietta Materials’ acquisition of Premier Magnesia in July 2025, bringing critical Nevada and Pennsylvania assets under a single operational umbrella. This move strengthens U.S. self-sufficiency in both natural and synthetic magnesia while aligning with Martin Marietta’s SOAR 2025 strategy focused on margin stability and downstream integration.

Pricing dynamics also shifted structurally in late 2025. Huber Engineered Materials announced global price increases across its Magnifin®, Vertex®, and Zerogen® magnesium hydroxide grades, effective January 2026, citing sustained inflation in logistics, labor, and imported ATH feedstock tariffs. From a demand standpoint, regulatory momentum remains favorable: NFPA-tracked demand for non-halogenated flame retardants rose 12% in 2025, reinforcing magnesium hydroxide’s role as the preferred mineral additive in PVC, polyethylene, and wire & cable insulation.

China – Environmental Tightening and Tiered Export Economics

China remains the world’s largest producer of magnesium compounds, but its 2025 strategy reflects a clear pivot toward environmentally constrained, quality-segmented output under the “Dual Carbon” framework. Capacity expansions in Ningxia are being executed with cleaner process technologies to stabilize supply while avoiding the extreme price volatility seen in earlier cycles. Rather than chasing volume, Chinese producers are prioritizing process efficiency and emissions control, particularly for magnesium hydroxide grades used in refractories and environmental applications.

On the trade front, dual-use export licensing scrutiny intensified throughout 2025, especially for high-purity magnesium derivatives. This has resulted in a tiered pricing regime, where certified, low-emission material commands a premium in EU and U.S. markets. Domestically, China’s steel industry continues to absorb large volumes of magnesium hydroxide for basic refractory castables, particularly in steel transfer and ladle systems, ensuring a stable internal demand base even as exports face regulatory friction.

Japan – Nano-Grade Precision for 5G, 6G, and Semiconductors

Japan occupies the ultra-high-end segment of the magnesium hydroxide market, where particle engineering and purity standards define competitive advantage. In 2025, UBE Corporation (via Ube Material Industries) intensified promotion of nano-sized magnesium hydroxide grades optimized for 5G/6G substrates, offering high thermal conductivity and minimal moisture absorption—critical for signal integrity in high-frequency electronics.

Demand spillovers from the semiconductor sector were equally significant. Japanese producers reported a 15% increase in consumption of magnesium-based additives for semiconductor CMP slurries during late 2024–2025, reflecting tighter integration between electronic chemicals and mineral additives. Beyond electronics, Japan remains the global quality benchmark for pharmaceutical-grade magnesium hydroxide, with companies such as Kyowa Chemical Industry sustaining leadership in USP/EP grades for antacid and clinical nutrition applications.

Brazil – Vertically Integrated Refractory Supply Hub

Brazil is leveraging its position as a top-three global magnesite producer to build a vertically integrated magnesium hydroxide value chain anchored in refractories. At MagForum 2025, RHI Magnesita highlighted the strategic role of its Brumado operations, with a clear objective to achieve over 75% “local-for-local” production across the Americas by H2 2026. This integration reduces logistics exposure and improves supply security for steel and cement customers.

Market economics tightened in 2025, with Brazilian magnesium hydroxide prices reaching ~$1,034/MT by September, supported by constrained output and 12.7% EBITA margin improvements driven by internal cost-reduction programs. However, late-2025 U.S. tariffs on Brazilian raw materials and finished goods forced exporters to re-route volumes toward European and Asian corridors, subtly reshaping Brazil’s trade orientation.

Israel – Dead Sea–Driven Specialty and Environmental Grades

Israel maintains a structurally unique position in the magnesium hydroxide market through its Dead Sea mineral base, enabling consistent production of high-value specialty grades. ICL Group (Dead Sea Bromine) sustained strong export performance in 2025, with the Netherlands (45%) and the U.S. (31%) accounting for the majority of shipment value. Despite regional geopolitical volatility, logistics remained resilient, with 139+ bills of lading recorded through December 2025.

Product strategy has increasingly favored liquid magnesium hydroxide suspensions, which are gaining traction as safer alternatives to caustic soda in industrial wastewater treatment. These magnesia slurries offer controlled neutralization kinetics and improved handling safety, positioning Israel as a preferred supplier for environmental compliance-driven applications rather than bulk refractories.

France – REACH Compliance and Circular Magnesium Systems

France has emerged as a pricing and compliance anchor within the European magnesium hydroxide market, driven by stringent EU REACH and sustainability mandates. By Q3 2025, domestic prices reached ~$751/MT, reflecting steady demand from polymers and construction as OEMs aggressively replace halogenated flame retardants. French producers successfully implemented cost-plus pricing models, passing through higher energy and compliance costs without demand erosion.

A defining milestone was the RAPTOR project, unveiled in November 2025 by an EU-backed consortium led by RHI Magnesita. This AI-enabled refractory recycling platform marks a significant step toward a circular economy for magnesia-based materials, reinforcing France’s role as a hub for green construction additives and recycled magnesium hydroxide systems.

2025 Strategic Matrix: Magnesium Hydroxide National Comparison

Magnesium Hydroxide National Comparison

|

Country

|

Primary Market Driver

|

2025 Key Milestone

|

Primary Application Focus

|

|

United States

|

Consolidation & defense

|

Martin Marietta–Premier Magnesia acquisition

|

High-purity HFFR, infrastructure

|

|

China

|

Environmental reform

|

Ningxia green capacity stabilization

|

Refractories, wastewater treatment

|

|

Japan

|

5G & semiconductor precision

|

Nano-grade magnesium hydroxide rollout

|

5G dielectrics, pharma

|

|

Brazil

|

Vertical integration

|

75% local-for-local production target

|

Steel refractories, exports

|

|

Israel

|

Mineral advantage

|

Stable Dead Sea export flows

|

Liquid slurries, environmental

|

|

France

|

EU REACH & circularity

|

RAPTOR refractory recycling launch

|

Green construction additives

|

Magnesium Hydroxide Market Report Scope

Magnesium Hydroxide Market

|

Parameter

|

Details

|

|

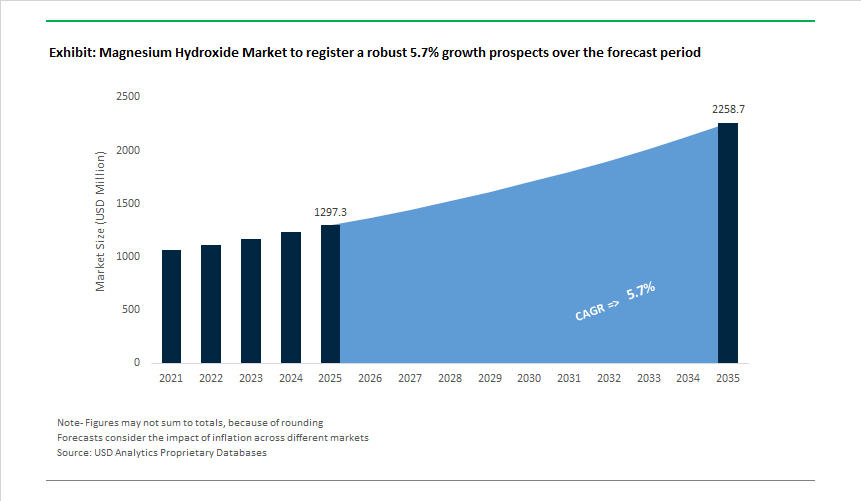

Market Size (2025)

|

$1297.3 Million

|

|

Market Size (2035)

|

$2258.3 Million

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Grade (Industrial/Technical, Pharmaceutical, Food & Feed, Reagent/Ultra-High Purity), By Form (Powder, Slurry/Liquid Suspension, Granular/Pelletized), By Production Process (Natural Brucite Mining, Synthetic, Precipitation), By End-Use Application (Environmental Protection, Flame Retardants, Pharmaceuticals & Healthcare, Chemical Intermediates, Food & Agriculture, Industrial Manufacturing)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Martin Marietta Magnesia Specialties LLC, Kyowa Chemical Industry Co. Ltd., Huber Engineered Materials, ICL Group Ltd., Konoshima Chemical Co. Ltd., Tateho Chemical Industries Co. Ltd., Nedmag B.V., Framatome (Haverhill Chemicals/KMT Partner), Kanto Chemical Co. Inc., Sinwon Chemical Co. Ltd., Hebei Messi Biology Co. Ltd., WBCIL, Xinyang Mineral Group, Garrison Minerals LLC, Sino Meir International

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Magnesium Hydroxide Market Segmentation

By Grade

- Industrial / Technical Grade

- Pharmaceutical Grade

- Food and Feed Grade

- Reagent/Ultra-High Purity Grade

By Form

- Powder

- Slurry / Liquid Suspension

- Granular / Pelletized

By Production Process

- Natural Brucite Mining

- Synthetic

- Precipitation

By End-Use Application

- Environmental Protection

- Flame Retardants

- Pharmaceuticals & Healthcare

- Chemical Intermediates

- Food & Agriculture

- Industrial Manufacturing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Magnesium Hydroxide Market Segmentation

- Martin Marietta Magnesia Specialties, LLC

- Kyowa Chemical Industry Co., Ltd.

- Huber Engineered Materials

- ICL Group Ltd (Israel Chemicals Ltd)

- Konoshima Chemical Co., Ltd.

- Tateho Chemical Industries Co., Ltd.

- Nedmag B.V.

- Framatome (Haverhill Chemicals/KMT Partner)

- Kanto Chemical Co., Inc.

- Sinwon Chemical Co., Ltd.

- Hebei Messi Biology Co., Ltd.

- WBCIL

- Xinyang Mineral Group

- Garrison Minerals, LLC

- Sino Meir International

*- List not Exhaustive