Marine Grease Market 2025–2034: Hybrid Bunkering Logistics, Lithium-Free Thickeners, and Digital Condition Monitoring Driving $692.1 Million Outlook at 4.1% CAGR

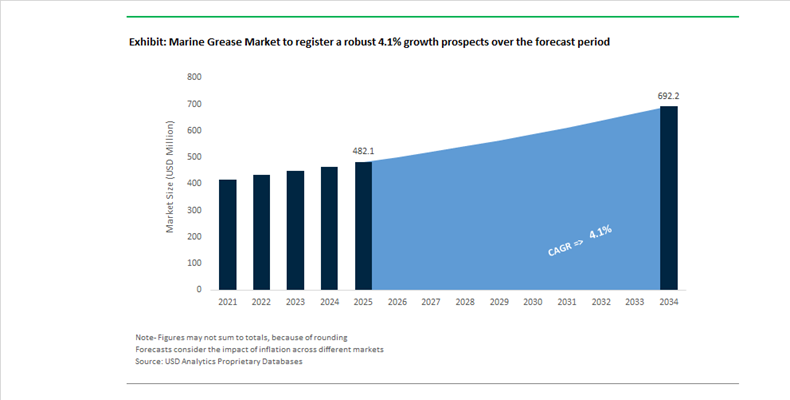

The Marine Grease Market is projected to grow from $482.1 Million in 2025 to $692.1 Million by 2034, registering a CAGR of 4.1%. Demand is supported by expanding global seaborne trade, modernization of dual-fuel marine engines, and stricter lubrication performance standards under IMO sulfur regulations. Marine greases, formulated with calcium sulfonate, lithium, and increasingly lithium-free thickener systems, are critical for propeller shafts, deck machinery, winches, stern tubes, and onboard bearings exposed to high salinity, moisture ingress, and extreme load conditions. Operators are prioritizing water resistance, corrosion inhibition, oxidative stability, and extended re-lubrication intervals to reduce dry-docking frequency and maintenance costs.

In April 2024, Castrol introduced the TLX range engineered for dual-fuel engines operating on low-sulfur fuels, focusing on acid neutralization and wear control under variable combustion conditions. In June 2025, Shell Marine inaugurated a lubricant and grease logistics hub in Busan, strengthening Asia-Pacific distribution with lead times reduced to approximately 48 hours for shipyards and fleet operators. Effective July 1, 2025, Shell completed the acquisition of Raj Petro Specialities, expanding its specialty marine grease portfolio across India and the Middle East. In July 2025, ExxonMobil’s authorized distributor Habot Marine Services renewed and expanded supply coverage across major South African ports, reinforcing regional availability along key Indian Ocean and South Atlantic trade routes.

Operational efficiency and sustainability initiatives accelerated in late 2025. In August 2025, Chevron partnered with Closelink to digitize procurement via its OnePort platform, enabling real-time inventory management and near-instant order processing for marine greases and lubricants. In September 2025, Lubrizol launched HybriCal, an anhydrous calcium-based lithium-free grease thickener meeting NLGI High-Performance Multiuse standards, mitigating lithium supply volatility for marine deck and shaft applications. In November 2025, TotalEnergies Lubmarine introduced the hybrid bunkering barge Tristar Eco Voyager in Fujairah, reducing carbon emissions by 35% during ship-to-ship grease and lubricant deliveries. In the same month, Shell Marine deployed its Shell Marine Sensor Service for real-time onboard grease condition monitoring, facilitating transition toward predictive maintenance models. Also in November 2025, SKF extended collaboration with INSA Lyon to develop intelligent grease systems integrated with IoT-enabled bearing diagnostics, targeting reduced unplanned downtime in marine propulsion and auxiliary systems. In December 2025, ENOC signed an agreement with HMS Bergbau AG to expand distribution of its STRATA marine range into Spain and Turkey, strengthening presence along Mediterranean shipping corridors.

Strategic Trends and High-Impact Opportunities in the Marine Grease Market

Trend: Non-Discretionary Transition to Environmentally Acceptable Lubricants Under VIDA

The marine grease market is undergoing a structural reset following the implementation of the EPA’s Vessel Incidental Discharge National Standards of Performance, which entered force in late 2024 and remains active through 2025. Under this framework, the use of Environmentally Acceptable Lubricants has shifted from a voluntary sustainability choice to a mandatory operational requirement for vessels operating in U.S. waters. The scope of compliance is extensive, covering more than 20 discharge categories, including stern tubes, thruster bearings, stabilizers, and wire ropes. This regulatory shift is directly reshaping procurement strategies for ship owners, fleet managers, and lubricant suppliers.

Enforcement intensity has increased materially. The U.S. Coast Guard is now responsible for verifying EAL usage and performance compliance, with penalties for non-compliance carrying both financial and operational risks. Industry disclosures from ExxonMobil and TotalEnergies confirm that certified EAL marine greases must demonstrate a minimum of 75% biodegradation within 28 days, while also meeting non-bioaccumulative and low-toxicity thresholds. Operational data from TotalEnergies Lubmarine shows that products such as BIOADHESIVE PLUS and BIOMULTIS EP 2 are being standardized across global fleets to ensure seamless compliance across both legacy VGP requirements and the newer VIDA regime. From a technology standpoint, operators are increasingly favoring synthetic ester-based EAL greases over vegetable oil alternatives. While vegetable-based greases offer biodegradability, they often lack oxidative stability under wide temperature swings. Synthetic esters provide superior hydrolytic resistance and durability, enabling reliable performance over five-year dry-dock intervals, which is now a baseline expectation for deep-sea vessels.

Trend: Shift Toward Calcium Sulfonate Complex and Polyurea Thickener Systems

A second major trend in the marine grease market is the accelerated move away from lithium-based thickeners toward calcium sulfonate complex and polyurea systems. This transition is driven by a combination of lithium price volatility, supply chain risk, and the superior performance characteristics of alternative thickener chemistries in saltwater environments. Calcium sulfonate complex greases are emerging as the default choice for deck machinery, cranes, winches, and open gear applications where water ingress and extreme pressure loading are persistent challenges.

Performance benchmarks published in 2025 indicate that calcium sulfonate complex greases consistently deliver dropping points above 260 degrees Celsius, significantly outperforming traditional lithium soaps in marine conditions. These greases offer inherent extreme pressure capability and natural corrosion resistance, often requiring up to 50% fewer supplemental anti-wear additives to achieve equivalent NLGI grades. Field data from offshore oil and gas operations further highlights their mechanical stability. Studies on high-load winches and cranes show that calcium sulfonate systems maintain structural integrity under shear, extending re-lubrication intervals and reducing maintenance labor costs by an estimated 15 to 20%. In parallel, polyurea greases are gaining traction in electric and hybrid marine systems. As vessels adopt all-electric auxiliary motors and high-speed generators, polyurea formulations are preferred for their oxidation resistance at elevated RPMs and their ability to deliver low-noise, low-vibration performance. These attributes are increasingly critical for passenger ferries and naval platforms where acoustic signatures and operational comfort are tightly specified.

Opportunity: High-Dielectric Marine Greases for Electric and Hybrid Propulsion Systems

The electrification of marine propulsion is creating a high-margin opportunity for advanced marine grease formulations engineered for dielectric performance. The growing deployment of electric azimuth thrusters and submerged pod drives is redefining lubricant requirements beyond mechanical protection. In 2025, SCHOTTEL announced multiple electric ferry programs in the United Kingdom, underscoring the rapid scale-up of electrically driven propulsion architectures.

These systems impose unique demands on grease chemistry. High dielectric strength is essential to provide electrical insulation within integrated motor housings and to prevent stray current corrosion in stator windings. At the same time, pod drives operate with high-speed bearings in confined, submerged environments, requiring greases that maintain a stable lubricating film at elevated RPMs without generating excessive churning heat. Low-viscosity polyalphaolefin-based greases are emerging as a preferred solution, balancing thermal control with bearing protection. Seal compatibility is also becoming a decisive factor. As OEMs such as Wärtsilä transition to advanced fluoropolymer sealing materials, there is a growing opportunity for chemically inert grease formulations that do not induce seal swelling or degradation over multi-year service intervals. Suppliers capable of delivering dielectric stability, thermal resilience, and seal compatibility in a single formulation are well positioned to capture disproportionate value in the e-marine segment.

Opportunity: Bio-Based Carbon Content to Support Net-Zero Fleet Strategies

Beyond compliance-driven EAL adoption, leading shipping companies are increasingly demanding marine greases with certified bio-based carbon content to support voluntary decarbonization commitments. Global operators such as Maersk and Hapag-Lloyd are extending Scope 3 emissions accounting into auxiliary consumables, including lubricants. This shift is creating a new premium tier within the marine grease market focused on renewable carbon intensity rather than biodegradability alone.

In its 2025 Sustainability and Climate Progress Report, TotalEnergies outlined a reinforced target to reduce the carbon intensity of its energy products by 17%, accelerating development of marine greases formulated with high bio-based content derived from animal fats and waste vegetable oils. These formulations allow ship owners to report measurable carbon reductions in sustainability audits without compromising operational reliability. Industry-wide collaboration is also increasing. Shell, in its All Hands on Deck 2.0 framework, emphasized that bio-circular lubricant innovation must run in parallel with alternative marine fuels such as bio-LNG and green methanol to meet the International Maritime Organization’s Net-Zero 2050 ambition. A practical illustration of this opportunity is emerging in Port of Rotterdam, where incentive programs for environmentally advanced vessels are driving strong demand for bio-based greases among tugboat operators and dredging fleets. These operators benefit from reduced port fees under the Environmental Ship Index, reinforcing bio-grease adoption as both a sustainability and economic decision.

Marine Grease Market Share and Segmentation Insights

Mineral Oil Marine Grease Leads Marine Lubrication Market Through Cost Efficiency and Proven Performance

Mineral oil marine grease accounted for 58.60% of the Marine Grease Market share in 2025, making it the most widely used lubricant type across commercial and industrial marine operations. Mineral oil–based greases are extensively utilized for ship maintenance, marine equipment lubrication, and vessel component protection, providing reliable lubrication performance in environments characterized by saltwater exposure, high humidity, and fluctuating operating temperatures. These greases deliver essential properties including water resistance, corrosion protection, mechanical stability, and load-bearing capacity, which are critical for maintaining the reliability of marine machinery. Mineral oil formulations also benefit from established global supply chains, cost-effective production, and compatibility with existing marine lubrication systems, allowing ship operators to maintain fleets efficiently while controlling operational expenses. In 2025, tightening environmental regulations affecting marine lubricant discharge have begun influencing market dynamics. Regulations such as environmentally acceptable lubricant (EAL) requirements in regulated waters are encouraging the gradual adoption of synthetic and bio-based marine greases, particularly for equipment exposed to marine ecosystems.

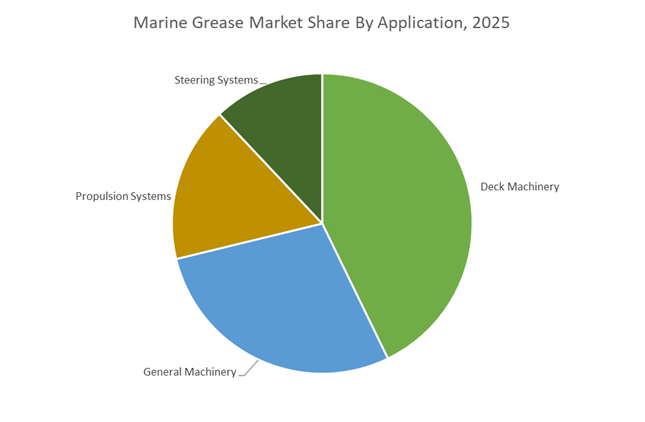

Deck Machinery Drives the Largest Demand for Marine Grease in Ship Operations

Deck machinery accounted for 42.80% of the Marine Grease Market share in 2025, establishing it as the largest application segment for marine lubrication systems. Deck equipment including cargo cranes, winches, hatch covers, anchor handling systems, and mooring equipment operates in some of the harshest marine environments, where continuous exposure to saltwater spray, heavy mechanical loads, and extreme weather conditions can accelerate component wear and corrosion. Marine greases are therefore critical for ensuring reliable lubrication, corrosion protection, and long-term operational stability of these mechanical systems. Effective lubrication reduces friction, prevents metal surface damage, and maintains operational safety during cargo handling and vessel operations. In 2025, the increasing size of commercial vessels and the expansion of global maritime trade have driven the use of larger cargo handling equipment with higher load capacities, which places additional stress on deck machinery components. As a result, lubricant manufacturers have developed high-performance marine grease formulations with enhanced extreme-pressure performance, superior adhesion, and improved resistance to wash-off, ensuring consistent lubrication performance in demanding marine operating environments.

Marine Grease Market Competitive Landscape

The marine grease market in 2026 is defined by calcium sulfonate complex thickener systems, synthetic ester-based EALs, and high-load durability under extreme marine conditions. Competitive differentiation is driven by VIDA/VGP compliance, seawater washout resistance, and high-shear stability for offshore wind, deep-sea shipping, and critical deck equipment lubrication.

Shell strengthens marine grease leadership with integrated supply chain and specialty portfolio expansion

Shell plc (Shell Marine) maintains global leadership through its integrated lubricants supply chain and continued expansion in high-performance marine greases. The Bekasi grease manufacturing plant enhances Asia-Pacific production capacity, while the acquisition of Raj Petro Specialities strengthens its specialty fluids portfolio. Its upgraded formulations aligned with API SQ standards ensure compatibility with next-generation marine engines and auxiliary systems. Under its “Powering Progress” strategy, Shell is advancing collaborative innovation in low-carbon marine lubricants tailored for evolving maritime decarbonization requirements.

ExxonMobil advances EAL-compliant greases with digital integration and low-emission focus

ExxonMobil Marine is positioning itself at the center of the energy transition by integrating high-performance marine greases with digital fleet management tools. Its investment of up to $30 billion in lower-emission solutions supports the development of biolubricants and EAL-compliant greases for stern tubes and propeller systems. Integration of MFMS and eBDN technologies enhances transparency and operational efficiency. Backed by advanced R&D capabilities, ExxonMobil delivers high-reliability grease formulations capable of maintaining performance under extreme thermal and mechanical stress conditions.

Castrol accelerates EAL adoption with synthetic ester greases for extreme marine environments

Castrol (BP Group) is driving adoption of environmentally acceptable lubricants through its BioTrans GB range, formulated with saturated synthetic esters for superior EP protection and seawater resistance. Designed to meet VIDA regulations, these greases operate across a wide temperature range (-25°C to +100°C), ensuring durability in harsh marine environments. Expanded distribution across key global hubs supports vessels using alternative fuels, while extensive field validation reinforces OEM approvals and performance credibility in high-load applications.

Chevron leverages calcium sulfonate technology for high-load and corrosion-resistant marine greases

Chevron Marine Lubricants is strengthening its position through calcium sulfonate complex grease technology, offering inherent corrosion resistance and high load-carrying capacity in seawater-exposed systems. Integration with Hess Corporation enhances feedstock security, while portfolio expansion supports mixed-fleet operators with standardized lubrication solutions. With significant CAPEX allocated toward low-carbon initiatives, Chevron is advancing bio-based grease development while maintaining performance leadership in demanding marine and offshore applications.

TotalEnergies expands biodegradable marine grease portfolio for offshore wind and compliance-driven markets

TotalEnergies Marine Lubricants is focusing on biodegradable, EAL-compliant greases aligned with European offshore wind expansion and stringent environmental regulations. Increased availability across major ports supports maintenance of renewable energy infrastructure and deep-sea fleets. Its “Multi-Energy” strategy integrates bio-based surfactants and marine lipids into lubricant formulations, while portfolio rationalization prioritizes high-margin, high-performance products. Proven resistance to seawater washout and compliance with EPA and IMO standards position TotalEnergies as a key supplier in sustainable marine lubrication solutions.

United States: Regulatory-Driven Shift to Environmentally Acceptable Marine Greases

The United States marine grease market is being reshaped by compliance-led procurement and capital reallocation toward low-emission lubricant systems. Under the U.S. Environmental Protection Agency’s Vessel General Permit requirements that continue to anchor 2026 compliance, vessels longer than 79 feet are required to use Environmentally Acceptable Lubricants at oil-to-sea interfaces. This mandate has structurally shifted procurement behavior, with an estimated 85% of deck machinery grease demand now directed toward biodegradable, non-bioaccumulative marine grease formulations. These requirements are accelerating the replacement of conventional lithium-based greases with calcium-thickened and ester-based products across ports and inland waterways.

Upstream investment is reinforcing this transition. Chevron finalized its 2026 capital expenditure plan in December 2025, allocating a significant portion of downstream investment to U.S. facilities for scaling next-generation lubricants and marine greases. Portfolio rationalization has followed, with Chevron Marine Products completing a global grease transition in late 2025 that prioritizes sprayable calcium-thickened greases for open-gear applications. Parallel momentum is visible at ExxonMobil, which confirmed in December 2025 that its 2030 greenhouse gas intensity targets are expected to be achieved by 2026. This is directly influencing production pathways for the Mobil SHC Aware grease portfolio through more carbon-efficient manufacturing and expanded bio-based ester feedstock sourcing. Offshore capital deployment of approximately USD 7.0 billion in 2026 across U.S. deepwater assets is further driving demand for extreme-pressure marine greases in subsea and drilling systems.

China: Shipbuilding-Led First-Fill Demand and Localization of Specialty Greases

China’s marine grease market is expanding primarily through shipbuilding dominance and first-fill lubricant demand. Entering 2026, China controlled more than 45% of the global ship order book, creating sustained requirements for initial grease fills in propulsion, steering, and deck machinery systems. Modern vessel designs are increasing the use of lithium complex and polyurea-thickened greases that deliver high load-bearing capacity and long service intervals, particularly for large container ships and LNG carriers.

Policy alignment is reinforcing domestic production. The Ministry of Industry and Information Technology’s 2026 work plan emphasizes localization of high-end marine chemicals, incentivizing Chinese blenders to develop high-purity grease components previously sourced from Europe. This has accelerated investment in domestic thickener technology and additive packages. Under the Industrial Digital Transformation Blueprint, grease blending plants in Jiangsu and Zhejiang have implemented AI-driven batch monitoring systems to ensure consistent NLGI Grade 2 and 3 output for export markets. Infrastructure expansion is also shaping application demand. The rapid rollout of LNG bunkering ports in 2025 has increased usage of cryogenic-stable marine greases in loading arms and vapor return systems at hubs such as Ningbo-Zhoushan, embedding LNG compatibility as a core specification in China’s marine grease supply chain.

Norway: Arctic Compliance and Cold-Temperature Performance Innovation

Norway’s marine grease market is being driven by alternative fuel adoption and extreme operating environments. According to data released by DNV in late 2025, order books included 966 LNG dual-fuel newbuilds, sharply increasing demand for greases compatible with alternative fuel seals and elastomers. These requirements extend beyond lubrication performance to chemical compatibility, particularly in hybrid propulsion systems operating in cold waters.

As bio-bunker fuel adoption slowed in late 2025 due to deferred International Maritime Organization frameworks, Norwegian operators redirected sustainability budgets toward Environmentally Acceptable Greases to meet stringent Arctic environmental standards. Domestic chemical firms are piloting low-temperature flowable greases in NLGI 0 and 00 grades for autonomous winches and deck systems, with a focus on maintaining shear stability at temperatures as low as minus 40 degrees Celsius. This focus positions Norway as a development hub for cold-climate marine grease technologies rather than a volume consumption market.

United Arab Emirates: Heat-Resilient Formulations and Global Distribution Leverage

The United Arab Emirates marine grease market is anchored in bunkering infrastructure leadership and extreme-climate formulation expertise. In November 2025, TotalEnergies Lubmarine launched the region’s first hybrid lubricants bunkering barge, Tristar Eco Voyager, at the Port of Fujairah. This platform enables ship-to-ship delivery of high-performance marine greases while reducing carbon intensity by approximately 35%, aligning logistics efficiency with decarbonization goals.

Fujairah’s role as a global port distribution hub has expanded further, with TotalEnergies supplying marine greases across more than 1,000 ports worldwide and positioning the UAE as the primary node for calcium sulfonate complex greases serving Middle Eastern and Central Asian shipping routes. Regional research centers in Dubai completed testing in 2025 for desert-grade marine greases engineered to prevent oil separation at ambient temperatures exceeding 50 degrees Celsius. These formulations are increasingly specified for deck machinery and port equipment exposed to extreme thermal stress, reinforcing the UAE’s specialization in high-temperature marine lubrication.

Singapore: Biofuel Compatibility and Regulatory Precision

Singapore’s marine grease market reflects its role as a global bunkering and regulatory benchmark hub. In 2025, bio-blend consumption reached 1.2 million tons, accelerating demand for ester-based marine greases compatible with biofuels in hybrid engine rooms. This compatibility requirement is influencing grease selection across harbor craft, offshore support vessels, and LNG bunkering operations.

Regulatory tightening is shaping supplier qualification. The Maritime and Port Authority of Singapore began implementing enhanced sustainability requirements in 2026 for waste-based lubricants, favoring grease manufacturers that utilize recycled feedstocks compliant with updated European renewable directives. Infrastructure investment is also affecting demand. Singapore’s commissioning of new LNG bunkering vessels in 2026 to resolve barge bottlenecks is increasing consumption of water-resistant, heavy-duty marine greases used in offshore transfer equipment, reinforcing the port’s influence on global marine grease specifications.

Country-Level Strategic Positioning in the Marine Grease Market

Marine Grease Market County Level Snapshot

|

Country / Region

|

Primary Market Driver

|

Core Marine Grease Focus

|

Policy or Institutional Influence

|

Competitive Positioning

|

|

United States

|

Environmental compliance and offshore capex

|

Biodegradable EP and EAL greases

|

EPA VGP and corporate GHG targets

|

Regulatory-driven volume transition

|

|

China

|

Shipbuilding first-fill demand

|

Lithium complex and polyurea greases

|

MIIT localization and digitalization

|

Scale with export consistency

|

|

Norway

|

Arctic operations and LNG fleets

|

Low-temperature EAGs

|

DNV green shipping standards

|

Cold-climate performance leadership

|

|

United Arab Emirates

|

Bunkering logistics and extreme heat

|

Calcium sulfonate complex greases

|

Port-led decarbonization

|

High-temperature specialization

|

|

Singapore

|

Biofuel adoption and port regulation

|

Ester-based and water-resistant greases

|

MPA sustainability framework

|

Specification-setting hub

|

Marine Grease Market Report Scope

Marine Grease Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$482.1 Million

|

|

Market Size (2034)

|

$692.1 Million

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Type (Mineral Oil Marine Grease, Synthetic Marine Grease, Bio-Based Marine Grease), By Thickener Type (Lithium-Based, Calcium-Based, Aluminum-Based, Polyurea), By Consistency (NLGI Grade 0, NLGI Grade 1, NLGI Grade 2, NLGI Grade 3), By Application (Deck Machinery, Propulsion Systems, Steering Systems, General Machinery), By End-Use Sector (Commercial Shipping, Offshore Oil and Gas, Naval Vessels, Recreational Boating)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Shell, ExxonMobil, TotalEnergies, Chevron, BP, Sinopec, ENEOS, Gulf Oil Marine, Idemitsu Kosan, FUCHS, Vickers Oils, Klüber Lubrication, PetroChina, Panolin

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Marine Grease Market Segmentation

By Type

- Mineral Oil Marine Grease

- Synthetic Marine Grease

- Bio-Based Marine Grease

By Thickener Type

- Lithium-Based

- Calcium-Based

- Aluminum-Based

- Polyurea

By Consistency

- NLGI Grade 0

- NLGI Grade 1

- NLGI Grade 2

- NLGI Grade 3

By Application

- Deck Machinery

- Propulsion Systems

- Steering Systems

- General Machinery

By End-Use Sector

- Commercial Shipping

- Offshore Oil and Gas

- Naval Vessels

- Recreational Boating

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Marine Grease Market

- Shell

- ExxonMobil

- TotalEnergies

- Chevron

- BP

- Sinopec

- ENEOS

- Gulf Oil Marine

- Idemitsu Kosan

- FUCHS

- Vickers Oils

- Klüber Lubrication

- PetroChina

- Panolin

*- List not Exhaustive