Marine Hydrolyzed Collagen Market 2025–2034: Ultra-Low Molecular Weight Peptides, Clinical Validation, and Sustainable Traceability Driving $2.8 Billion Outlook at 8.7% CAGR

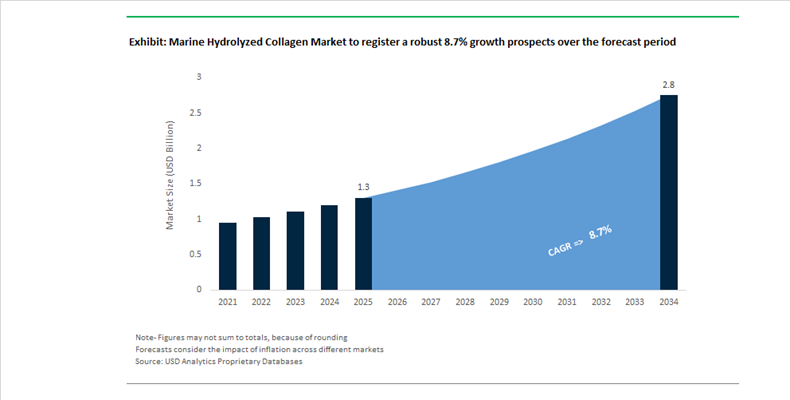

The Marine Hydrolyzed Collagen Market is projected to expand from $1.3 billion in 2025 to $2.8 billion by 2034, registering a CAGR of 8.7%. Market growth is fueled by rising demand for fish-derived collagen peptides in nutricosmetics, ready-to-drink functional beverages, joint health supplements, regenerative medicine, and premium skincare. Marine collagen, predominantly Type I derived from fish skin and scales, is valued for its high bioavailability, low molecular weight peptide profile, and superior solubility compared to bovine alternatives. Increasing consumer focus on “beauty from within,” clean-label sourcing, and clinically validated efficacy is accelerating innovation in enzymatic hydrolysis, peptide standardization, and traceable marine supply chains.

In October 2024, RTI Surgical completed the acquisition of Collagen Solutions to secure engineered medical-grade collagen for tissue engineering and wound care applications, reinforcing consolidation in high-purity marine and xenograft collagen supply. In late 2024, Inlife Healthcare launched Japanese-sourced hydrolyzed marine collagen peptides in India, reflecting regional demand for imported, premium-grade anti-aging supplements. In December 2024, MBRF Global Foods announced a 50% stake acquisition in Brazil’s Gelprime, finalized in October 2025, enabling expanded hydrolyzed collagen output for global food and health markets. During 2025, Darling Ingredients’ Rousselot strengthened Peptan Marine traceability protocols for wild-caught white fish sources, responding to sustainability verification standards and growing interest in certified blue beauty ingredients.

Innovation intensified through 2025 and early 2026. In early 2025, PB Leiner introduced SOLUGEL Supra with an average molecular weight of approximately 500 Da and 45% di- and tri-peptides, optimized for rapid absorption in RTD beverages and functional foods. At Vitafoods Asia 2025, TSI Group launched collagen and creatine gummies targeting joint health and athletic recovery. In October 2025, a 30-day clinical study on C-Shortz RTD containing 7,500 mg of sea bass skin collagen demonstrated significant improvements in skin hydration and hyperpigmentation, strengthening science-backed marketing claims. Thai Union expanded its strategic investment in Jellagen to scale jellyfish-derived Collagen Type 0 for medical research and premium skincare. In early 2026, Nestlé Health Science entered a biotech partnership to advance precision-hydrolyzed marine collagen formulations under its Vital Proteins line. Concurrently, suppliers including Amicogen and Weishardt accelerated development of algae-derived collagen-mimetic peptides positioned for the emerging vegan-marine segment, integrating complete amino acid profiles to support endogenous collagen synthesis.

Strategic Trends and Growth Opportunities in the Marine Hydrolyzed Collagen Market

Trend: Vertical Integration and Traceable Marine Sourcing as a Competitive Differentiator

The marine hydrolyzed collagen market is undergoing a structural shift toward vertically integrated and fully traceable supply chains, driven by tightening sustainability disclosure requirements under the EU Green Deal and rising premium brand scrutiny in North America and Europe. Ingredient manufacturers are increasingly bypassing fragmented open-market sourcing in favor of direct relationships with fisheries and seafood processors, ensuring consistent access to fish skins and scales that meet rigorous environmental and ethical standards. According to the 2025 annual disclosures from Marine Stewardship Council, more than 20.6% of global wild marine catch is now engaged in its certification program, materially expanding the pool of verified low-carbon marine biomass available for collagen extraction.

This shift toward certified sourcing is being reinforced by consolidation across the value chain. In December 2025, Darling Ingredients, through its collagen brand Rousselot, entered a definitive agreement with Tessenderlo Group to combine their collagen and gelatin businesses. The strategic rationale centers on circular economy execution, converting fish processing by-products into high-value bioactive peptides with end-to-end traceability. Market evidence from late 2024 shows that MSC-certified marine collagen peptides are commanding price premiums in the U.S. and EU, where consumers increasingly equate traceability with quality, safety, and environmental responsibility. For suppliers, transparency has moved from a compliance requirement to a revenue lever, particularly in premium nutraceutical, beauty-from-within, and clinical nutrition segments.

Trend: Ultra-Low Molecular Weight Peptide Engineering to Maximize Bioavailability

R&D investment in ultra-low molecular weight marine collagen peptides, typically below 2,000 Daltons, has emerged as the dominant innovation theme in 2025. Through advanced enzymatic hydrolysis and precise process control, manufacturers are engineering peptide profiles that demonstrate faster intestinal absorption and more predictable biological activity. A randomized controlled trial published in PubMed in September 2025 confirmed that low-molecular-weight collagen peptides significantly improved skin hydration and reduced wrinkle depth within eight weeks, with benefits persisting even after a washout period. These outcomes are reshaping formulation strategies, enabling lower daily dosages while maintaining clinical efficacy.

Beyond dermatological benefits, suppliers are expanding the scientific narrative around metabolic and musculoskeletal support. At the 2025 Rousselot Innovation Days, researchers highlighted emerging evidence of metabolic synergy between GLP-1 weight-loss therapies and specific marine collagen peptides, particularly in preserving lean muscle mass during rapid fat reduction. Comparative studies from GELITA further validated that fish-derived bioactive collagen peptides now achieve parity with mammalian sources for skin health outcomes. The key differentiator lies in achieving a narrow and consistent molecular weight distribution, which ensures reproducible bioactivity across different fish species and production batches. As a result, molecular precision has become a core competitive benchmark rather than a technical differentiator.

Opportunity: Clinical Nutrition Solutions for Sarcopenia and Bone Health

The aging global population is transforming marine hydrolyzed collagen into a clinically relevant nutrition ingredient for sarcopenia, osteoporosis, and musculoskeletal resilience. No longer confined to cosmetic applications, marine collagen peptides are being incorporated into medical-grade foods and supplements designed for active aging. A 2025 meta-analysis published in Frontiers in Nutrition reported statistically significant improvements in bone mineral density at the femoral neck and spine following collagen peptide supplementation, particularly when combined with vitamin D and calcium. Standardized mean differences ranging from 0.40 to 0.58 highlight collagen’s role in improving bone turnover markers and structural integrity.

Muscle health represents an equally compelling avenue. Clinical evidence indicates that collagen peptides support muscle performance with effect sizes around 0.60, positioning Type I marine collagen as a strategic input in sarcopenia prevention programs. This is accelerating adoption across hospital nutrition, rehabilitation products, and senior-focused dietary supplements. Parallel innovation is emerging in regenerative medicine, where marine collagen’s biocompatibility is being leveraged in orthopedic scaffolds, wound dressings, and tissue engineering matrices. In 2025, Rousselot advanced multiple gelatin and collagen prototypes for medical device applications, underscoring the convergence between nutrition and biomaterials in high-value healthcare markets.

Opportunity: High-Clarity Marine Collagen for Premium RTD Beverage Formulations

The rapid expansion of the Ready-to-Drink beauty and protein beverage segment is creating strong demand for marine collagen that delivers high clarity, neutral flavor, and acid stability. The global protein and collagen RTD drinks market reached approximately $1.42 billion in 2024, fueled by consumer preference for convenient, multifunctional nutrition. These formulations require collagen peptides that dissolve rapidly, remain stable at low pH, and do not impart fishy off-notes, even in citrus or tea-based matrices.

Advances in deodorization, desalting, and lipid removal are enabling suppliers to eliminate amines such as trimethylamine oxide and oxidation byproducts that historically limited marine collagen use in beverages. Industry feedback indicates that collagen peptides below 3 kDa have become the functional standard for RTD applications due to superior solubility and reduced sensory impact. In 2025, commercial launches such as collagen-infused RTD teas demonstrated stable performance at pH levels between 3.0 and 4.0, while accommodating electrolytes and B-vitamins without compromising clarity or shelf life. As premium beverage brands prioritize clean-label positioning and sensory neutrality, high-purity marine hydrolyzed collagen is emerging as a critical enabler of differentiation and margin expansion in the RTD nutrition ecosystem.

Marine Hydrolyzed Collagen Market Share and Segmentation Insights

Fish-Derived Collagen Leads Marine Hydrolyzed Collagen Market Through Scalable Byproduct Utilization

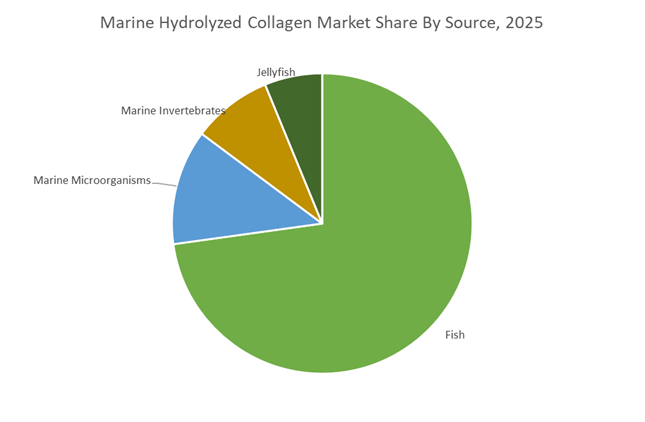

Fish-derived collagen accounted for 72.80% of the Marine Hydrolyzed Collagen Market share in 2025, making it the dominant raw material source for marine collagen peptide production. Marine collagen extracted from fish skin, scales, and bones of species such as tilapia, cod, salmon, and snapper provides a highly scalable and cost-efficient supply chain for collagen manufacturing. These raw materials are widely available as byproducts of the seafood processing industry, allowing manufacturers to convert fishery waste streams into high-value functional ingredients. Fish collagen is also widely preferred in global markets because it avoids religious and cultural restrictions associated with bovine and porcine collagen, supporting adoption across diverse consumer populations. The ingredient is known for high bioavailability, low molecular weight peptide structure, and rapid absorption, making it particularly suitable for nutraceutical and cosmetic applications. In 2025, marine collagen suppliers increasingly emphasize circular economy sourcing models, utilizing upcycled fishery waste streams to reduce environmental impact while strengthening sustainability narratives that resonate strongly with environmentally conscious consumers and wellness-focused brands.

Nutraceuticals and Dietary Supplements Drive the Largest Demand for Marine Hydrolyzed Collagen

Nutraceuticals and dietary supplements accounted for 62.80% of the Marine Hydrolyzed Collagen Market share in 2025, making them the leading application segment for marine collagen ingredients. Consumers increasingly incorporate marine collagen peptides into daily supplement routines aimed at improving skin health, hair strength, nail growth, joint mobility, and overall wellness. Hydrolyzed marine collagen is typically marketed in powder, capsule, liquid, and functional beverage formats, enabling convenient consumption across multiple demographic groups. The rising popularity of beauty-from-within nutraceuticals and anti-aging supplementation has significantly expanded the global marine collagen consumer base. In 2025, supplement brands have increasingly shifted toward science-backed product positioning, investing in clinical research that demonstrates measurable benefits such as improved skin elasticity, enhanced hydration levels, and reduced wrinkle depth associated with marine collagen peptide consumption. These validated claims strengthen consumer confidence and enable premium product positioning within the rapidly growing global collagen supplements and functional nutrition market.

Marine Hydrolyzed Collagen Market Competitive Landscape

The marine hydrolyzed collagen market in 2026 is driven by ultra-low molecular weight peptides (<1 kDa), high bioavailability, and clinically validated multifunctional benefits across skin, metabolic health, and recovery. Competitive dynamics focus on peptide precision, MSC/FOS-certified sourcing, and advanced enzymatic hydrolysis to deliver premium nutraceutical and cosmeceutical ingredients.

Rousselot leads bioactive marine collagen innovation with clinically validated multifunctional peptides

Rousselot is redefining marine hydrolyzed collagen through its Peptan® platform, focusing on clinically proven benefits beyond skin health, including hair follicle stimulation and metabolic support. Its Nextida™ GC technology targets GLP-1-related satiety pathways, positioning collagen in weight management ecosystems. Clinical validation of improved skin density and hydration strengthens its premium positioning. With a “360-degree beauty” approach, Rousselot integrates marine peptides into diverse delivery formats aligned with high-end nutraceutical and cosmeceutical demand.

Gelita scales marine collagen capacity with targeted bioactive peptide systems

Gelita AG is expanding its leadership through significant investment in marine collagen infrastructure, including a $60 million Norway facility expansion to double capacity by 2027. Its VERISOL® F peptides deliver targeted beauty-from-within benefits at low dosages, enhancing formulation efficiency. Innovation in functional formats such as OPTIBAR® addresses technical challenges in sports nutrition. Gelita’s expertise in bioactive collagen peptides (BCP®) enables precise functionality, supporting applications across skincare, performance nutrition, and functional foods.

Weishardt advances tripeptide collagen for rapid absorption and premium sustainability positioning

Weishardt (Naticol®) is differentiating through tripeptide-focused marine collagen, with its Naticol® x3Peptide delivering ≥25% tripeptides for enhanced bioavailability and faster systemic absorption. Its MSC and FOS certifications strengthen sustainability credentials, aligning with EU regulatory expectations. Expansion into sports recovery with Naticol® Xsport targets muscle repair and injury prevention. Neutral sensory properties enable application in clear beverages and functional drinks, addressing key formulation barriers in premium nutrition products.

Nitta Gelatin strengthens Asia-Pacific supply with clinical-grade marine peptide production

Nitta Gelatin is leveraging its strong presence in Asia-Pacific to scale production of high-purity marine collagen through its Gelixer® CollagenPep platform. Strategic restructuring and investment in R&D talent support innovation in clinical-grade peptide formulations. Its integrated extraction infrastructure ensures consistent raw material supply, while expansion in India and China positions the company to meet rising demand for bioavailable collagen in nutraceutical, pharmaceutical, and cosmeceutical applications.

Seagarden delivers traceable, ultra-pure marine collagen with species-specific sourcing

Seagarden AS is a pure-play marine collagen specialist, focusing on wild-caught cod (Gadus morhua) to ensure consistent peptide profiles and high Type I collagen content. Its vertically integrated, fully traceable supply chain aligns with premium sustainability requirements. With ultra-low molecular weight (~3 kDa) and high solubility, its products are optimized for functional beverages and on-the-go formats. Ongoing development of synergistic marine blends expands its positioning into holistic bone, joint, and wellness solutions.

Norway: Arctic-Sourced Collagen Leadership and Bioavailability Differentiation

Norway has consolidated its position as a premium-origin hub in the marine hydrolyzed collagen market by structurally integrating seafood waste valorization with pharmaceutical-grade processing. In late 2025, Norwegian processors expanded the Blue-to-Beauty initiative, scaling enzymatic hydrolysis infrastructure capable of processing more than 10,000 metric tons of North Atlantic cod skin annually. This capacity expansion is not volume-driven but quality-led, with a clear focus on Type I marine collagen destined for nutraceutical, medical aesthetics, and pharmaceutical channels. The use of cold-adapted enzymes has delivered a reported 15% efficiency gain by preserving triple-helix integrity at lower processing temperatures, directly supporting higher bioactivity and purity benchmarks demanded by advanced applications.

Commercial positioning is being reinforced through policy and clinical validation. Under Norway’s 2026 Export Strategy, government-backed grants now incentivize certification of marine collagen as Sustainable Arctic Sourced, explicitly targeting premium North American medical aesthetics buyers. Clinical data released in December 2025 by Oslo-based researchers demonstrated that Norwegian liquid marine collagen peptides achieve 1.5 times faster absorption compared with bovine collagen, accelerating reformulation activity for 2026 launches. Product innovation is also diversifying at the species level, with Bergen-based producers introducing salmon-derived L-type hydrolyzed collagen characterized by elevated hydroxyproline content, positioning it for joint health and tissue regeneration applications.

India: Cost Rationalization, Traceability, and Ethno-Collagen Innovation

India’s marine hydrolyzed collagen market is transitioning from a cost-driven export play to a traceability-led and formulation-driven ecosystem. A pivotal inflection point came in November 2025 when the Government of India reduced GST on fish extracts and marine value-added products from 12% to 5%. This fiscal rationalization materially lowers production costs and enhances India’s competitiveness in supplying marine collagen to global nutraceutical and cosmetic brands. Parallel infrastructure development under the Pradhan Mantri Matsya Sampada Yojana is embedding collagen extraction at the coastal level, with climate-resilient villages increasingly equipped for primary fish-skin processing.

Industrial scale-up is now visible in dedicated assets. In mid-2025, major Indian nutraceutical groups commissioned a USD 15 million marine collagen facility in Gujarat, designed to supply Halal-certified hydrolyzed collagen for export-oriented protein supplements. Digital transparency is emerging as a differentiator. The launch of the National Marine Fisheries Census in October 2025 enables geo-referenced traceability, allowing manufacturers to offer catch-to-capsule documentation to international retailers. On the product side, Indian pharmaceutical firms are leading the 2026 trend toward Ethno-Collagen blends, combining marine hydrolyzed collagen with botanicals such as Ashwagandha to address the global holistic and preventive wellness segment.

China: AI-Optimized Hydrolysis and Medical Device Acceleration

China remains the world’s dominant manufacturing base for marine hydrolyzed collagen, accounting for more than 40% of global fish-skin-derived output. However, strategic emphasis is shifting from scale to molecular precision. Under the Ministry of Industry and Information Technology 2025 high-end supply mandate, Eco-Smart hydrolysis hubs in Jiangsu are deploying AI-optimized processing that consistently produces collagen peptides below 1,000 Daltons, a critical threshold for enhanced absorption in cosmetic serums and medical nutrition products.

Source diversification and regulatory acceleration are reinforcing this evolution. By early 2026, Chinese producers increasingly favored Asian Seabass and Silver Carp skins, which are preferred in skincare for superior moisturizing performance. At the upstream frontier, the National Development and Reform Commission signaled in 2025 a policy pivot toward deep-sea biodiversity, incentivizing extraction of rare marine biopolymers from deep-sea sponges for advanced wound-healing technologies. Regulatory pathways are tightening in parallel, with the National Medical Products Administration streamlining approval processes for marine-derived new biological ingredients, reducing time-to-market for collagen-based medical devices by roughly 30%.

Thailand: By-product Maximization and Tropical Formulation Stability

Thailand’s marine hydrolyzed collagen market is defined by near-total utilization of aquaculture by-products and strong alignment with premium Asian cosmetics demand. Throughout 2024 and 2025, Thai Union Group expanded investments into the collagen value chain, including strategic stakes in UK biotech ventures such as Jellagen, which specializes in non-mammalian jellyfish collagen for medical-grade scaffolds. This positions Thailand at the intersection of food, biotech, and regenerative medicine supply chains.

Operational efficiency milestones are equally significant. By July 2025, Thai aquaculture leaders achieved a 90% utilization rate of Tilapia and Asian Seabass by-products, diverting skins almost exclusively into high-value hydrolyzed collagen streams for Japanese cosmetic brands. Scientific innovation is supporting tropical-market suitability. Research published in mid-2025 demonstrated a marine hydrolyzed collagen formulation capable of maintaining emulsion stability for up to six months under high-temperature conditions, a critical advancement for skincare products distributed in Southeast Asia, the Middle East, and Africa.

United States: Premiumization, Upcycling Credentials, and Medical Nutrition Adoption

The United States marine hydrolyzed collagen market is being shaped by premium product launches, sustainability signaling, and expanding clinical acceptance. In January 2026, U.S. nutrition leaders such as GNC are scheduled to roll out high-end Premier Collagen product lines featuring marine-sourced collagen from Naticol, reinforcing marine collagen’s positioning in the anti-aging and beauty-from-within category. Sustainability is becoming a purchase driver, following Rousselot achieving Upcycled Certified status in April 2025 for its Peptan marine collagen peptides, resonating with environmentally conscious consumers.

Clinical and regulatory momentum is accelerating parallel demand. In 2025, FDA filings for marine-derived bioactive peptides increased by approximately 20%, reflecting growing physician recognition of marine hydrolyzed collagen in addressing muscle atrophy, joint degeneration, and medical nutrition needs. This expansion beyond supplements into medical food applications underscores the U.S. market’s evolution toward evidence-backed, high-purity collagen solutions rather than commoditized protein powders.

Country-Level Strategic Positioning in the Marine Hydrolyzed Collagen Market

Marine Hydrolyzed Collagen Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Differentiators

|

Policy or Institutional Catalyst

|

Primary Application Orientation

|

|

Norway

|

Arctic-sourced premium collagen

|

Faster absorption, cold extraction

|

Export subsidies, sustainability certification

|

Medical aesthetics, joint health

|

|

India

|

Cost efficiency and traceability

|

GST reduction, ethno-collagen blends

|

PMMSY, GST reform

|

Nutraceuticals, wellness

|

|

China

|

Precision hydrolysis and medical devices

|

Sub-1,000 Dalton peptides

|

MIIT, NDRC, NMPA reforms

|

Cosmetics, wound care

|

|

Thailand

|

Full by-product utilization

|

Tropical stability formulations

|

Aquaculture optimization

|

Premium cosmetics

|

|

United States

|

Premiumization and upcycling

|

Certified sustainability, FDA momentum

|

FDA medical food pathways

|

Anti-aging, clinical nutrition

|

Marine Hydrolyzed Collagen Market Report Scope

Marine Hydrolyzed Collagen Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.3 Billion

|

|

Market Size (2034)

|

$2.8 Billion

|

|

Market Growth Rate

|

8.7%

|

|

Segments

|

By Source (Fish, Jellyfish, Marine Microorganisms, Marine Invertebrates), By Form (Powder, Liquid, Capsules and Tablets, Granular), By Type (Type I Collagen, Type II Collagen, Multi-Collagen Blends), By Distribution Channel (Online, Offline), By End-Use Application (Nutraceuticals and Dietary Supplements, Cosmetics and Personal Care, Pharmaceutical and Medical, Food and Beverage)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Rousselot, Gelita, Nitta Gelatin, Ashland, Thai Union Group, Amicogen, Titan Biotech, Nippi Collagen, Weishardt, Collagen Solutions, Lapi Gelatin, Italgelatine, ET-Chem, Gelnex, ArcticZymes Technologies

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Marine Hydrolyzed Collagen Market Segmentation

By Source

- Fish

- Jellyfish

- Marine Microorganisms

- Marine Invertebrates

By Form

- Powder

- Liquid

- Capsules and Tablets

- Granular

By Type

- Type I Collagen

- Type II Collagen

- Multi-Collagen Blends

By Distribution Channel

By End-Use Application

- Nutraceuticals and Dietary Supplements

- Cosmetics and Personal Care

- Pharmaceutical and Medical

- Food and Beverage

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Marine Hydrolyzed Collagen Market

- Rousselot

- Gelita

- Nitta Gelatin

- Ashland

- Thai Union Group

- Amicogen

- Titan Biotech

- Nippi Collagen

- Weishardt

- Collagen Solutions

- Lapi Gelatin

- Italgelatine

- ET-Chem

- Gelnex

- ArcticZymes Technologies

*- List not Exhaustive