Market Overview: Sterilization-Proof Polymers and Biocompatible Composites Drive USD 58.9 B Medical Engineered Materials Market

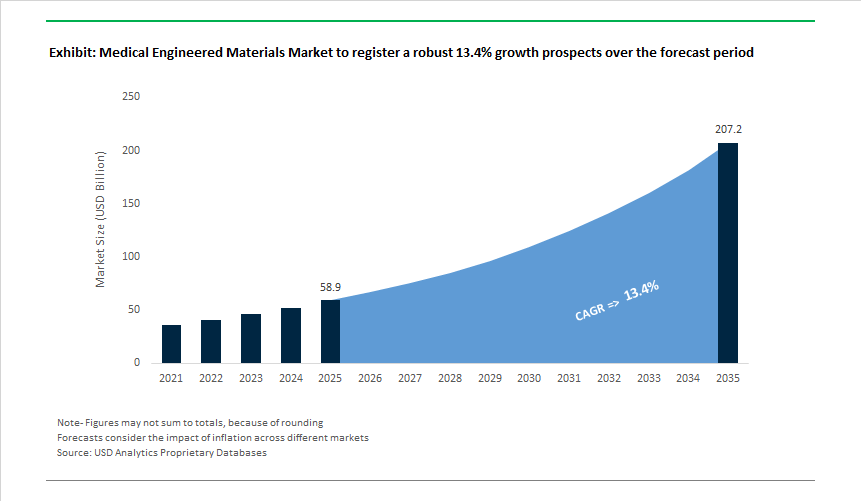

The Medical Engineered Materials Market reaches USD 58.9 billion in 2025 and is projected to surge to USD 207.1 billion by 2035, advancing at a 13.4% CAGR, as material performance becomes inseparable from clinical safety, regulatory clearance, and hospital economics. Unlike general healthcare consumables, engineered medical materials are now selected at the intersection of sterilization survivability, chemical resistance, biocompatibility, and lifecycle cost, making them foundational inputs for device OEMs, hospital systems, and biopharmaceutical manufacturers.

A primary growth engine is the structural shift toward reusable, sterilization-intensive medical devices driven by infection-control mandates and cost pressure on hospitals. High-performance polymers such as polyphenylsulfone (PPSU) and related sulfone-based materials are increasingly non-substitutable in reusable surgical instruments, trays, and equipment housings because they retain over 90% of tensile strength after hundreds of steam-autoclave cycles, resist hydrolysis, and maintain dimensional stability under repeated thermal shock. In parallel, the expansion of aggressive hospital disinfection protocols has elevated demand for chemically hardened PC/ABS and specialty copolymer blends capable of tolerating exposure to dozens of hospital-grade disinfectants without stress cracking, embrittlement, or discoloration-failure modes that directly trigger device recalls and regulatory scrutiny.

On the manufacturing side, single-use systems (SUS) in biopharmaceutical production represent a second structural demand pillar. Medical-grade thermoplastic polyurethane (TPU) tubing, silicone assemblies, and multilayer polymer films are being specified with ultra-low extractables and leachables profiles-often below 10 parts per billion-to protect biologic drug purity across upstream and downstream processes. As biologics, cell therapies, and mRNA platforms scale, these material requirements are becoming qualification gates rather than differentiators, embedding engineered polymers deeply into validated manufacturing workflows with long replacement cycles.

Implantable materials further reinforce the market’s defensiveness. In orthopedics and spine applications, PEEK-based and ceramic-reinforced composites are increasingly designed with elastic moduli closer to cortical bone, reducing stress shielding by up to 25% compared with traditional metallic implants. This materials-driven improvement in load transfer supports better bone remodeling, longer implant life, and lower revision rates-outcomes that directly influence reimbursement, surgeon preference, and hospital procurement decisions.

Sterility assurance extends beyond devices into medical packaging, where microbial-barrier materials such as high-performance spunbond polyolefins must consistently deliver >99.999% microbial barrier efficiency under dynamic handling, transportation, and storage conditions. Failure at the packaging-material level can compromise Sterility Assurance Level (SAL), exposing OEMs to recall risk irrespective of device design quality.

Market Analysis: M&A, Cleanrooms and Circular Medical Plastics Reshape Industry Landscape

The recent trajectory of the medical engineered materials industry is defined by a blend of M&A in high-value therapies, capacity expansion in contract manufacturing, and early but meaningful moves toward a circular economy for medical plastics. In February 2025, Stryker’s USD 4.9 billion acquisition of Inari Medical significantly expanded its interventional endovascular device portfolio, directly increasing demand for specialized polymer catheters, delivery systems and engineered tubing that must balance pushability, torque, kink resistance and biocompatibility. This was followed in August 2025 by Sanofi’s USD 1.9 billion acquisition of Dren Bio, highlighting how biologics and next-generation therapeutics are amplifying requirements for advanced biopharma processing materials, single-use assemblies and polymer-based drug delivery systems capable of preserving complex molecules.

Material sustainability and circularity clearly moved up the strategic agenda. In February 2025, Covestro expanded its portfolio of low-carbon footprint medical-grade materials, including Makrolon® RE polycarbonate based on mass-balanced bio-waste feedstock, giving OEMs a credible pathway to reduce device-level CO₂ without sacrificing sterilization compatibility or optical clarity. Later, in December 2025, Covestro entered a strategic partnership with Allmed to conduct a recycling feasibility study for artificial kidney filters, exploring the recovery of high-quality medical-grade polycarbonate from complex, multi-material devices and testing the viability of a closed-loop model for dialysis components. In parallel, Microbix Biosystems launched its QAPs™ quality assessment products and QUANTDx™ reference materials on Copan® FLOQSwabs® in December 2025, underscoring the role of specialized polymer swab materials in reliable H3N2 flu testing and broader in vitro diagnostics (IVD) quality assurance.

Manufacturing and infrastructure investments are also reshaping the landscape. In November 2025, Jabil announced plans to invest about USD 70 million over three years in a new dedicated medical device manufacturing facility in Mississippi (U.S.), strengthening global contract manufacturing capacity for engineered-material-intensive devices and supporting nearshoring trends. Cleanroom and process-control solutions are advancing in parallel: AES Clean Technology introduced its CleanLock Module in April 2024, providing an engineered cleanroom solution that is critical for maintaining material purity, particulate control and regulatory compliance in pharmaceutical and device manufacturing lines. On the other hand, STEMart expanded into Pilot Production Services in April 2024 in the U.S., helping OEMs bridge from development to scaled manufacturing, including validation and characterization of engineered materials for new devices and disposables. Across this period, the converging themes are clear: higher performance requirements, more stringent sterilization and disinfectant resistance, rising sustainability expectations, and increased reliance on global EMS/CMOs to industrialize complex material formulations.

Medical Engineered Materials Market Trends and Opportunities

Bioresorbable Metallic Alloys for Pediatric and Cardiovascular Implants

A decisive trend in implantable materials is the transition away from permanent metals toward bioresorbable alloys that eliminate the need for secondary removal surgeries—an especially critical advantage in pediatric and cardiovascular care. The challenge has been synchronizing mechanical integrity with biological healing, a balance that zinc-based alloys are now achieving.

Recent peer-reviewed studies published in late 2025 position zinc as the “Goldilocks” bioresorbable metal. Magnesium alloys degrade too rapidly (typically 1–2 mm/year), risking premature loss of support, while iron degrades too slowly (around 0.01 mm/year), persisting beyond clinical necessity. By contrast, newly optimized Zn–Mg and Zn–Li alloys demonstrate controlled degradation rates of 0.05–0.2 mm/year, closely matching the 3–6 month vascular remodeling window required for pediatric stents and cardiovascular scaffolds.

Mechanical performance has reached clinically viable thresholds. Advanced Zn–Ag and Zn–Cu alloy systems, refined through hot extrusion in 2025, have achieved ultimate tensile strengths of 270–350 MPa with elongation values above 25%. This enables thinner strut designs that preserve radial strength while reducing flow disturbance—a known contributor to late-stage thrombosis.

Equally important is early-stage biocompatibility. Electrochemically deposited hydroxyapatite (HAp) coatings are now being used to moderate initial Zn²⁺ ion release. Independent validation reported in late 2025 confirms that these coatings significantly reduce early cytotoxicity, allowing zinc alloys to transition from laboratory promise to regulatory-credible implant candidates.

Engineering of “Smart” Polymer Composites for Surgical Tools

Medical polymers are evolving from inert housings into active, stimuli-responsive systems that enhance precision in minimally invasive surgery (MIS) and interventional procedures. The defining characteristic of this trend is responsiveness at the point of use.

In 2025, light-responsive injectable hydrogels incorporating photothermal agents demonstrated a 35% improvement in localized therapeutic efficacy when activated by near-infrared (NIR) light. These composites enable surgeons to trigger drug release or localized tumor inhibition on demand, reducing systemic exposure and improving targeting accuracy.

Parallel advances in shape-memory polymers (SMPs) are changing device deployment strategies. SMP-based composites designed to respond to temperature or pH gradients can be delivered through narrow catheters and then expand into predefined 3D geometries at body temperature (37°C). Clinical evaluations indicate this approach can reduce incision size by up to 50%, directly lowering infection risk and recovery time.

The integration of sensing capability marks a further step change. Carbon–polymer nanocomposites developed in 2025 now embed functionalized carbon nanotubes into surgical tools, achieving strain detection resolutions near 0.1%. For robotic-assisted surgery, this enables real-time haptic feedback—transforming forceps and scalpels into data-generating instruments rather than passive implements.

High-Barrier, USP Class VI Films for Single-Use Bioprocessing

The rapid expansion of biologics manufacturing is creating a material-driven opportunity in single-use technologies (SUT), where contamination risk and regulatory compliance are paramount. As monoclonal antibodies and viral vectors scale, the materials used in fluid handling are becoming a primary determinant of batch integrity.

Regulatory guidance issued in 2025 emphasizes strict control of Leachables and Extractables (L&E), directly favoring USP Class VI–certified multilayer films. These engineered structures—commonly PE/EVOH/nylon combinations—are now standard for single-use bags and assemblies in high-value bioprocessing workflows. Their adoption is reinforced by upstream trends: over 70% of new upstream bioreactor capacity added in 2025 utilized single-use systems, driven by an ~80% reduction in cleaning and validation time compared to stainless steel.

Major suppliers, including Sartorius and Danaher, are investing heavily in ready-to-use flow paths and standardized polyethylene-based assemblies. The strategic objective is global supply-chain resilience, minimizing the risk of batch loss due to material variability or contamination events.

Tissue-Mimicking Hydrogels for Pre-Operative Planning

Personalized medicine is extending upstream into surgical planning, creating demand for tissue-mimicking engineered materials that replicate the mechanical response of human organs. In this context, hydrogels are emerging as a critical enabling platform.

A 2025 clinical materials study demonstrated that 3D-printable hydrogel systems can closely match the Young’s modulus and viscoelastic response of human dermis, enabling realistic suturing and incision training. Measured rupture forces aligned closely with human tissue benchmarks, improving surgeon preparedness for complex procedures.

More advanced dual-crosslinkable hydrogel platforms are now being used to fabricate patient-specific organ replicas directly from DICOM imaging data. These models allow surgeons to rehearse complex cardiovascular or orthopedic interventions, with case studies indicating 15–20% reductions in operating room time—a material improvement in both patient outcomes and hospital economics.

Supply-chain dynamics are adding urgency. Trade constraints introduced in 2025 on specialty polymer precursors have increased interest in domestic production of high-purity hydrogel reagents. This is accelerating innovation in enzyme-responsive and pH-sensitive networks that stabilize performance while reducing dependency on imported intermediates.

Market Share Analysis: Medical Engineered Materials Market

Market Share by Material Type: Medical Plastics Anchoring Scale, Sterility, and Regulatory Compliance

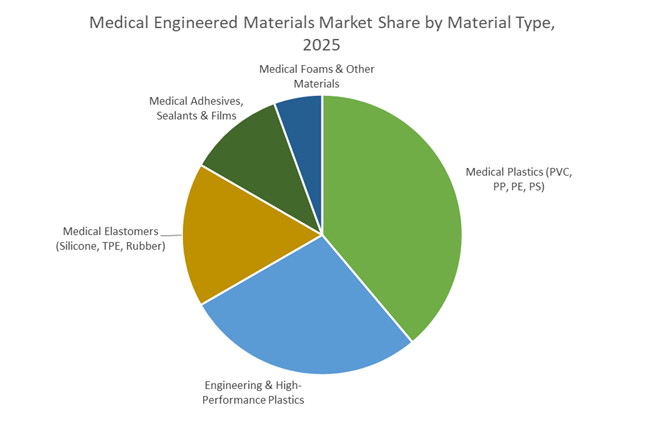

Medical plastics account for approximately 35% of the Medical Engineered Materials Market because they sit at the intersection of cost scalability, sterilization resilience, and regulatory acceptance, a combination no other material class matches at volume. PVC, polypropylene (PP), and polyethylene (PE) dominate hospital supply chains precisely because they tolerate ethylene oxide, gamma radiation, and steam sterilization without structural or chemical degradation, enabling safe mass production of critical devices. PVC alone represents around 31% of medical plastic compounds in 2025, reflecting its irreplaceable role in blood-contact applications such as IV tubing, dialysis sets, and blood bags where flexibility, transparency, and kink resistance are non-negotiable. At the same time, material innovation is reshaping share within plastics: random copolymer polypropylene is growing faster than homopolymers, driven by demand for crystal-clear labware and prefilled syringes that must balance optics with impact resistance. High-performance medical polycarbonates capable of withstanding 148°C autoclave cycles further extend plastics into semi-durable instruments, narrowing the gap between disposables and reusable devices. Layered onto this is a decisive regulatory shift toward phthalate-free, BPA-free, and low-emission formulations, positioning medical plastics as the most future-proof material platform under tightening EU MDR and North American compliance regimes.

Market Share by Application: Medical Disposables as the Non-Cyclical Demand Engine

Medical disposables and supplies represent around 40% of total market demand, making them the single largest application segment and the primary stabilizer of the medical engineered materials market. This dominance is structural rather than episodic, rooted in infection prevention protocols that increasingly mandate single-use devices across surgical, diagnostic, and inpatient care settings. In 2025, the disposables segment alone is valued at nearly USD 300 billion, underscoring its role as a recession-resistant pillar of global healthcare expenditure. Plastics are central to this scale: over 23% of all medical plastic compound demand flows directly into disposable products, meaning resin availability, formulation changes, or regulatory bans immediately ripple across hospital operations and OEM revenues. North America’s 38% revenue share reflects both high procedural volumes and stringent infection-control rules that limit reuse, particularly for catheters, syringes, and surgical drapes. Critically, disposables are not low-tech commodities—materials such as sterile barrier packaging with 10-year shelf-life guarantees enable global distribution, emergency stockpiling, and just-in-time hospital logistics. As healthcare systems prioritize patient safety, supply-chain resilience, and regulatory defensibility, medical disposables continue to pull material innovation and volume demand, securing their position as the largest and most strategically important application segment.

Competitive Landscape: Sulfone Polymers, Silicones, Tpus and UHMW-PE Anchor Leading Suppliers

Leading players in the Medical Engineered Materials Market differentiate themselves through deep polymer science, validated biocompatibility data, regulatory support (MAFs, ISO 10993, FDA) and increasingly, sustainability and circularity initiatives. High-performance sulfone polymers, PEEK and PAEK families, medical-grade silicones, TPUs and UHMW-PE dominate critical applications from reusable OR equipment and wearables to implants, catheters, filtration and SUS assemblies. The ability to deliver global supply assurance, process support and application-specific grades is now as important as intrinsic material performance.

Solvay (Syensqo) Leverages Sulfone and PEEK Portfolios For Demanding Reusable Medical Devices

Solvay (now Syensqo) offers one of the broadest portfolios of high-performance thermoplastics for healthcare, including sulfone polymers, PEEK and PARA. These materials, including Radel® PPSU, are engineered for best-in-class resistance to aggressive hospital disinfectants, making them a natural fit for reusable surgical equipment housings, sterilizable trays and high-stress structural components. On the implant side, Solvay supplies Zeniva® PEEK and other implantable biomaterials backed by extensive ISO 10993 biocompatibility data, targeting long-term orthopedic and spinal fusion applications where fatigue resistance and imaging compatibility are critical. The company’s AvaSpire® PAEK product family is positioned to close the cost-performance gap between PEEK and other high-performance polymers by improving ductility and processing flexibility for select structural parts. Solvay also differentiates through robust regulatory support, including FDA Master Access Files (MAFs) and region-specific specialists, enabling OEMs to shorten time-to-submission and reduce the documentation burden for new medical devices.

Dupont Builds Leadership in Medical-Grade Silicones, Tyvek® Packaging and Fluid Systems

DuPont is a key force in medical-grade silicone solutions, particularly under its Liveo® brand of silicone elastomers and skin adhesives. These materials underpin more than 60% of new wearable monitoring devices, delivering a combination of gentle skin adhesion, breathability and biocompatibility vital for long-term patient compliance. In packaging, DuPont’s Tyvek® continues to set the benchmark for breathable sterile barriers, offering >99.999% microbial barrier efficiency and maintaining sterility for a broad range of medical and pharmaceutical products. To support the surge in biopharma single-use systems, DuPont is expanding silicone tubing extrusion and elastomer mixing capacity at its HIMS facility in Michigan, ensuring secure supply of critical fluid-handling components. Coupled with its vertically integrated capabilities in precision extrusion, molding and catheter assembly, DuPont enables OEMs to accelerate the design and commercialization of complex fluid transfer and drug delivery systems built around engineered silicone and elastomer materials.

Covestro Drives Sustainable Medical-Grade Polycarbonate and Closed-Loop Dialysis Recycling

Covestro is a leading supplier of medical-grade polycarbonate, with Makrolon® widely used in over 75% of single-use drug delivery devices owing to its optical clarity, impact resistance and gamma sterilization compatibility. To address climate and ESG requirements, Covestro has broadened its low-carbon portfolio with Makrolon® RE (launched in February 2025) based on mass-balanced bio-waste feedstock, allowing OEMs to lower device CO₂ footprints without revalidating entire supply chains. For higher temperature demands, Covestro provides Apec® RE high-heat polycarbonate, enabling devices such as surgical lighting housings and anesthesia masks to withstand repeated steam sterilization cycles while retaining dimensional stability. Strategically, Covestro’s December 2025 partnership with Allmed on a recycling feasibility study for artificial kidney filters signals a push toward closed-loop polycarbonate recycling in complex medical devices, opening pathways for circular dialysis components and more sustainable material flows in high-volume disposables.

Lubrizol Advances Medical-Grade Tpus For Long-Term Implants and Interventional Devices

The Lubrizol Corporation is a global leader in medical-grade thermoplastic polyurethanes (TPUs), including Tecoflex® and Carbothane™, which are widely specified for long-term (>30-day) implantable Class III devices due to their biostability, elasticity and fatigue resistance. Its portfolio spans polycarbonate-based and polyether-based TPU chemistries, collectively covering about 90% of performance requirements for infusion catheters, interventional vascular devices and structural heart support components. Lubrizol extends beyond raw materials into contract manufacturing services, offering extrusion and molding of TPU and silicone components, and thereby providing OEMs with a vertically integrated pathway from polymer selection through to finished device assemblies. Innovation focus is centered on hydrophilic TPU grades such as Tecophilic®, which enable low-friction coatings on guidewires and catheters, improving trackability, reducing insertion forces, and enhancing overall patient safety and procedural efficiency.

Celanese Delivers UHMW-PE, POM and Filtration Media For Orthopedic and Life-Support Systems

Celanese plays a pivotal role in orthopedic and life-support applications through its GUR® Ultra-High Molecular Weight Polyethylene (UHMW-PE), which is the standard material for approximately 95% of joint replacement bearing surfaces owing to its exceptional wear resistance and proven biocompatibility. Beyond implants, Celanese supplies high-strength polyacetal (POM) and high-flow engineering resins for single-use and reusable surgical instrument handles, trays and housings that must endure repeated steam sterilization while maintaining dimensional stability and toughness. The company is also heavily invested in advanced hollow fiber membranes and polymer filter media used in hemodialysis cartridges and biopharma filtration systems, enabling high-efficiency separation processes for critical care and biologics manufacturing. With global manufacturing standards, full material traceability and comprehensive compliance documentation, Celanese ensures its polymer components meet the stringent ISO and FDA requirements for Class II and Class III devices, making it a preferred partner for high-risk, high-reliability medical applications.

The United States continues to anchor the global medical engineered materials market through a policy-driven emphasis on high-risk, high-reward biomaterials innovation and domestic supply resilience. In March 2025, the Advanced Research Projects Agency for Health (ARPA-H) submitted its $1.5 billion FY2025 budget request, with a substantial allocation directed toward the Health Science Futures office. This funding stream prioritizes bio-resorbable polymers, shape-memory alloys, and next-generation antimicrobial materials, reinforcing the U.S. leadership position in materials that directly enable minimally invasive surgery, regenerative medicine, and implantable device miniaturization.

Parallel to public funding, February 2025 marked a pivotal supply-chain realignment when SABIC entered strategic manufacturing collaborations with U.S.-based medical device OEMs to expand domestic availability of medical-grade PEEK and Ultem™ HU resins. This initiative materially shortens lead times for implant and diagnostic hardware manufacturers while reducing exposure to cross-border regulatory delays. Under ARPA-H’s Proactive Health mission, federal grants are also incentivizing antimicrobial engineered polymers aimed at reducing hospital-acquired infections (HAIs), positioning material science as a first-line preventive healthcare tool rather than a downstream enabler.

China: 2025 GMP Overhaul and Intelligent Material Traceability

China’s medical engineered materials market is undergoing a structural quality reset, shifting decisively from scale to compliance-driven sophistication. On November 4, 2025, the National Medical Products Administration (NMPA) released the revised Medical Device Good Manufacturing Practice (2025 GMP)—the first full revision since 2014. The new framework introduces dual-release systems and significantly tighter oversight of contract manufacturing and outsourced material suppliers, directly impacting producers of Class III medical-grade polymers and alloys.

A defining feature of the 2025 GMP is its push toward “intelligent manufacturing”. High-risk material suppliers are now required to deploy tamper-proof digital traceability systems that track every batch of resin or metal from synthesis through final device integration. This aligns with State Council Opinion No. 53 (2024), which targets high-quality development in domestic medtech. For global OEMs sourcing from China, compliance capability and digital lifecycle transparency are now as critical as material performance, fundamentally reshaping supplier qualification criteria.

India: ₹3,420 Crore PLI Realization and Medical Materials Infrastructure Build-Out

India has rapidly transitioned into a globally competitive supplier of medical engineered materials, driven by strong execution of Production Linked Incentive (PLI) schemes. As of September 2025, official data confirms that 22 greenfield medical device projects have been commissioned under the PLI framework, delivering ₹12,344 crore in cumulative eligible sales, including ₹5,869 crore in exports. These outputs span MRI coils, CT scan sub-assemblies, medical-grade liners, and polymer housings, underscoring India’s emergence as a materials-enabled medtech manufacturing base.

Capacity expansion is being reinforced by targeted ecosystem investments. In June 2025, Kerala approved a ₹215 crore investment for the CSIR-NIIST biopolymer facility at the Bio360 Life Science Park, focusing on sustainable medical plastics. Additionally, by November 2025, the central government had released ₹180 crore toward three specialized medical device parks offering shared biocompatibility, sterilization, and validation infrastructure. This common-facility approach materially lowers R&D barriers for domestic engineered-materials firms and accelerates time-to-market for compliant medical products.

Japan: GX 2040 Vision and High-Precision Fineceramic Leadership

Japan’s strategy in medical engineered materials is anchored at the intersection of decarbonization, precision manufacturing, and advanced ceramics. Following the January 18, 2025 Cabinet approval of the GX 2040 Vision, subsidies have been prioritized for energy-efficient ceramic kilns, circular production systems, and low-carbon fineceramic materials. This has strengthened Japan’s leadership in hermetic ceramic packages and low-loss interconnects, which are increasingly critical for MEMS-based medical sensors and wearable diagnostics.

Innovation momentum accelerated at the Advanced Ceramics Show 2025 (July), where Japanese manufacturers unveiled next-generation ceramic solutions for implantable and real-time monitoring devices. Further reinforcing Japan’s biomaterials edge, in November 2025, the Japan Science and Technology Agency (JST) announced a dual-stage PEG hydrogel sealant designed to prevent bile leakage post-surgery—highlighting Japan’s capability in highly specialized bio-adhesives that combine mechanical performance with biological compatibility.

Germany: EU MDR Compliance and PFAS-Free Medical Polymers

Germany remains Europe’s regulatory and sustainability benchmark for medical engineered materials, operating under the strict framework of the EU Medical Device Regulation (EU MDR). In January 2025, German chemical leaders, including BASF, introduced biocompatible polymers with reduced carbon footprints for surgical instruments, fully aligned with ISO 10993 sterility and safety requirements. These materials directly address hospital sustainability targets without compromising performance under repeated sterilization cycles.

A second structural shift is underway through PFAS-free elastomer commercialization, responding to evolving ECHA guidelines. German compounders are leading the replacement of legacy fluorinated elastomers in medical tubing, seals, and fluid-handling systems, targeting a multi-billion-dollar European medical resin market. Simultaneously, specialized compounding clusters are scaling biocompatible PEEK formulations capable of withstanding high-temperature autoclaving, reinforcing Germany’s role in high-reliability medical device materials.

Ireland: Galway Medtech Hub and Regenerative Material Innovation

Ireland has consolidated its position as a global innovation node for regenerative medical materials, leveraging deep medtech clustering in Galway. In 2025, the Regenerative Medicine Institute (REMEDI) announced a 3D-printed spinal implant based on proprietary bio-engineered scaffolds designed to actively promote tissue regeneration—demonstrating Ireland’s leadership in functional biomaterials rather than passive implants.

The ecosystem was further validated at the December 2025 Irish Medtech Awards, where firms such as West Pharmaceutical Services and Integer Holdings were recognized for advances in sustainable and complex medtech manufacturing. In parallel, Dublin-based Deciphex partnered with Novartis to apply AI-driven material discovery to preclinical studies, significantly compressing development timelines for next-generation biocompatible polymers.

2025 Strategic Matrix: Medical Engineered Materials Market

Medical Engineered Materials Market Matrix

|

Country

|

Primary Market Driver

|

2025 Strategic Milestone

|

Material / Technology Focus

|

|

United States

|

Federal health innovation

|

$1.5B ARPA-H FY25 request

|

Bio-resorbable polymers, SMAs

|

|

China

|

Regulatory modernization

|

Nov 2025 revised GMP

|

Digitally traceable resins

|

|

India

|

PLI-led localization

|

₹12.3k Cr cumulative PLI sales

|

MRI components, biopolymers

|

|

Japan

|

GX & precision ceramics

|

GX 2040 Cabinet approval

|

Fineceramics, PEG hydrogels

|

|

Germany

|

EU MDR & ESG

|

PFAS-free elastomer rollout

|

Sustainable medical polymers

|

|

Ireland

|

Regenerative medicine

|

REMEDI 3D-printed implants

|

Bio-scaffolds & AI-materials

|

Medical Engineered Materials Market Report Scope

Medical Engineered Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$58.9 Billion

|

|

Market Size (2035)

|

$207.1 Billion

|

|

Market Growth Rate

|

13.4%

|

|

Segments

|

By Material Type (Medical Plastics, Engineering Plastics, Standard Plastics, Medical Elastomers, Medical Foams, Medical Adhesives & Sealants, Medical Films), By Application (Medical Disposables, Medical Devices, Implantable Materials, Advanced Wound Care, Medical Wearables), By Processing Technology (Injection Molding, Extrusion, Additive Manufacturing, Solvent Casting, Form-Fill-Seal)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Evonik Industries AG, BASF SE, Covestro AG, Solvay S.A. / Syensqo, DuPont de Nemours Inc., Arkema S.A., SABIC, Celanese Corporation, Trelleborg AB, Mitsubishi Chemical Group, Eastman Chemical Company, Lubrizol Corporation, Teijin Limited, Zeon Corporation, Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Medical Engineered Materials Market Segmentation

By Material Type

- Medical Plastics

- Engineering Plastics

- Standard Plastics

- Medical Elastomers

- Medical Foams

- Medical Adhesives & Sealants

- Medical Films

By Application

- Medical Disposables

- Medical Devices

- Implantable Materials

- Advanced Wound Care

- Medical Wearables

By Processing Technology

- Injection Molding

- Extrusion

- 3D Printing (Additive Manufacturing)

- Solvent Casting

- Form-Fill-Seal

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Medical Engineered Materials Market

- Evonik Industries AG

- BASF SE

- Covestro AG

- Solvay S.A. / Syensqo

- DuPont de Nemours, Inc.

- Arkema S.A.

- SABIC

- Celanese Corporation

- Trelleborg AB

- Mitsubishi Chemical Group

- Eastman Chemical Company

- The Lubrizol Corporation

- Teijin Limited

- Zeon Corporation

- Huntsman Corporation

*- List not Exhaustive