Market Overview: Medical Rubber Stopper Industry Growth Trajectory

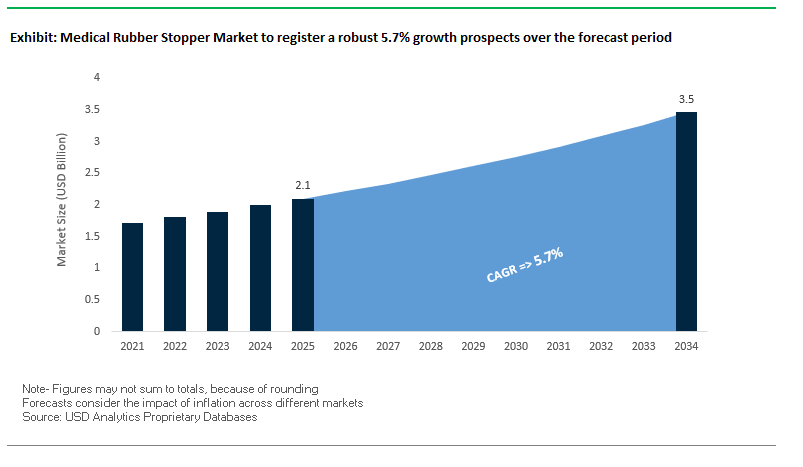

The global medical rubber stopper market is projected to reach $2.1 billion in 2025 and is forecasted to grow steadily to $3.5 billion by 2034, registering a healthy CAGR of 5.7%. This market growth is deeply tied to the rising demand for biologics, specialty injectables, and vaccines, which require high-performance containment solutions. For pharmaceutical companies and healthcare providers, medical rubber stoppers are not just packaging materials but critical components that ensure drug integrity, sterility, and patient safety. With biologics making up a rapidly growing share of new drug launches, the role of biocompatible and advanced rubber stoppers is becoming indispensable.

Professionals evaluating this industry will want to know: What drives market adoption? Which technologies are shaping stopper innovation? How are regulatory expectations influencing manufacturers? The answers lie in the growing emphasis on low-extractable, high-purity elastomers, innovations in barrier coatings, and the shift toward ready-to-use (RTU) components to streamline drug manufacturing.

Key Insights for Industry Professionals:

- Biologics boom fuels demand: Growth in monoclonal antibodies, cell therapies, and vaccines significantly drives the use of premium-grade rubber stoppers.

- Biocompatibility as a must-have: Low leachables and chemical stability are now central selection criteria for pharma companies.

- Sealing innovation: Advanced barrier coatings improve oxygen and moisture resistance, extending drug shelf life.

- Ready-to-use trend: RTU stoppers are rapidly adopted for reducing contamination risks and speeding up production cycles.

Market Analysis: Recent Developments and Strategic Shifts

The medical rubber stopper market has witnessed significant activity in recent years, with developments focused on laboratory expansions, sustainability goals, manufacturing optimization, and product innovation. In January 2025, West Pharmaceutical Services launched the Daikyo PLASCAP RUV Closures in a nested format, streamlining the filling process for drug manufacturers. By August 2025, West strengthened its European presence with a new analytical laboratory in Stolberg, Germany, providing advanced testing and documentation services for injectable packaging customers.

Datwyler Pharma Solutions has been a major driver of change, with its ForwardNow transformation program launched in December 2024, targeting growth from 2025 to 2027. By April 2025, the company began supplying serial components for GLP-1 therapies, a high-growth injectable drug class addressing diabetes and obesity. In July 2025, Datwyler restructured its U.S. operations, transferring production from Vandalia, Ohio to optimize its manufacturing footprint. Meanwhile, in August 2025, the company reported strong momentum in its transformation strategy, reinforcing its premium position in elastomeric components.

Other major players are also shaping industry trends. AptarGroup in June 2025 highlighted strong results from its pharmaceutical segment, with vial containment solutions contributing significantly. Asahi Kasei announced in July 2025 the construction of a new spinning plant in Japan for Planova™ virus removal filters, indirectly boosting demand for compatible stopper technologies used in biologics manufacturing. Additionally, Daikyo Seiko strengthened its environmental commitment in July 2025, with its greenhouse gas emission reduction targets certified as Science Based Targets, aligning with the industry’s increasing sustainability focus.

Breakthrough Trends and Opportunities Reshaping the Medical Rubber Stopper Market

Accelerated Adoption of Polymer-Based and Coated Elastomers

The medical rubber stopper market is undergoing a significant transition as pharmaceutical manufacturers increasingly adopt polymer-based and fluoropolymer-coated elastomers to ensure drug integrity and patient safety. Traditional bromobutyl stoppers, while long established, face growing scrutiny due to their potential to release extractables and leachables into sensitive biologics and vaccines. Industry experts highlight that the U.S. Pharmacopeia (USP) is preparing a new technical guide to manage oligomer leachables, reflecting the critical importance of stopper purity.

Equally pressing is the issue of particulate contamination caused by silicone oil coatings on conventional stoppers. Publications such as OnDrugDelivery emphasize how advanced fluoropolymer spray coatings create a barrier that prevents particle formation, removing the need for siliconization while ensuring ease of vial closure. Global regulations are reinforcing this shift, with USP <665> becoming official in May 2026 and ICH Q3E guidelines tightening requirements on extractables and leachables. These regulatory advancements are accelerating the demand for inert, low-leachables elastomer stoppers capable of meeting the standards of next-generation biologics.

Strategic Vertical Integration and Supply Chain Securement by Pharma Companies

Pharmaceutical companies are adopting vertical integration strategies and entering sole-source agreements to mitigate supply risks for critical packaging components. The COVID-19 pandemic highlighted how vulnerable global supply chains were, pushing manufacturers to secure high-purity stoppers and vials through long-term agreements. A recent case involved a major pharmaceutical player signing a multi-year deal with a packaging manufacturer to ensure uninterrupted supply for its oncology pipeline.

Companies are also investing in geographic diversification and nearshoring to reduce dependency on single supply regions. By qualifying suppliers across multiple continents, pharmaceutical giants are building resilience against logistical disruptions and raw material shortages. This trend demonstrates how supply chain resilience and guaranteed access to specialized stoppers are becoming as critical as drug innovation itself.

Development of Stopper Formulations for Lyophilized (Freeze-Dried) Drugs

The growing market for lyophilized injectables—spanning vaccines, biologics, and advanced therapies—creates a specialized opportunity for stopper manufacturers. Freeze-dried drugs are highly sensitive to moisture, requiring closures that prevent water vapor ingress while maintaining elasticity under extreme conditions. Companies like Aptar Pharma have developed bromobutyl-based lyophilization stoppers with low residual moisture and low permeability, safeguarding the stability of freeze-dried formulations.

Furthermore, advanced designs such as igloo- and two-legged stoppers are being engineered to withstand vacuum and temperature cycles inherent in lyophilization, while also allowing efficient water vapor escape during the process. As the pipeline of protein-based therapeutics and cell & gene therapies expands, the demand for specialized lyophilization-compatible closures will grow exponentially. This represents a high-value niche segment for medical stopper manufacturers, positioning them to capitalize on one of the fastest-growing areas of injectable drug delivery.

Integration of Traceability and Anti-Counterfeiting Features

Global regulations, particularly the U.S. Drug Supply Chain Security Act (DSCSA), are fueling demand for primary packaging with embedded traceability. Rubber stopper manufacturers are innovating with serialized codes, RFID tags, and unique physical identifiers to meet compliance needs while simultaneously addressing the escalating challenge of counterfeit drugs.

Companies such as Datwyler are pioneering “smart rubber” solutions by embedding RFID tags into stoppers during vulcanization, enabling each unit to carry a unique, tamper-proof digital identity. This not only enhances anti-counterfeiting efforts but also streamlines regulatory compliance by ensuring unit-level traceability throughout the pharmaceutical supply chain.

Beyond security, RFID-enabled stoppers improve supply chain efficiency by supporting automated inventory management. As noted by HID Global, RFID systems can scan multiple items simultaneously without requiring line of sight, drastically reducing the time and cost of logistics operations. For pharmaceutical companies, the adoption of intelligent, traceable stoppers presents both a compliance advantage and an operational efficiency boost.

Competitive Landscape: Leading Companies in the Medical Rubber Stopper Market

The competitive landscape of the global medical rubber stopper market is defined by a mix of multinational giants and specialized regional manufacturers. Companies are competing through innovation in barrier films, product purity, sustainability initiatives, and strategic expansions. Below are key players shaping the market.

West Pharmaceutical Services Strengthens Global Analytical Capabilities

West is a global leader in drug containment and delivery systems. Its rubber stoppers, plungers, and seals serve a wide range of biologics and specialty injectables. In August 2025, West opened a new analytical lab in Germany, expanding its technical support in Europe. With innovations such as FluroTec barrier film and Daikyo Crystal Zenith polymer, West offers superior drug protection, reduced extractables, and enhanced compliance with regulatory requirements.

Datwyler Pharma Solutions Expands GLP-1 Therapy Component Supply

Datwyler is a leading manufacturer of elastomeric components for injectables, focusing on high-performance, coated solutions. In April 2025, it began supplying components for GLP-1 therapies, reinforcing its role in diabetes and obesity drug delivery. The ForwardNow program and its U.S. production streamlining highlight its global growth strategy. Datwyler’s strength lies in premium elastomer solutions designed for sensitive biologics.

AptarGroup Drives Growth with PremiumCoat® Film-Coated Stoppers

Aptar is known for its drug delivery devices and pharmaceutical packaging. Its PremiumCoat® ETFE film-coated stoppers are designed to reduce leachables and improve drug stability, critical for biologics and vaccines. By June 2025, the company reported strong pharmaceutical results, reflecting the growing adoption of its containment solutions. Aptar’s sustainability and innovation-focused strategy positions it as a strong competitor in next-gen stopper solutions.

Daikyo Seiko Focuses on High-Purity Elastomeric Solutions

Daikyo Seiko specializes in pharmaceutical packaging and medical elastomers, including rubber stoppers and plungers. Its commitment to quality and sustainability was reinforced in July 2025, when its emission reduction targets were certified as Science Based Targets. Daikyo’s customized elastomeric solutions are highly regarded for compatibility with sensitive formulations, making it a key supplier for global pharma companies.

Jiangsu Hualan Leverages Strong Asian Market Presence

Jiangsu Hualan is a leading Chinese producer of rubber stoppers and pharmaceutical packaging materials. Its portfolio spans coated and uncoated stoppers for injections, infusions, and freeze-dried drugs. The company’s development of hyperpure and coated rubber stoppers demonstrates its strategy to serve the premium biologics market. Its stronghold in Asia’s booming pharma sector makes it a critical regional player with global ambitions.

Medical Rubber Stopper Market Share Insights

Stoppers for Vials Lead Market Share by Product Type in the Medical Rubber Stopper Industry

Stoppers for vials hold the largest market share, accounting for 55% of the medical rubber stopper market, underlining their indispensable role in parenteral drug packaging. Vials are the universal container for injectable formulations, including biologics, oncology drugs, vaccines, and antibiotics, making stopper performance critical for maintaining sterility and drug stability. These stoppers must withstand steam sterilization, gamma irradiation, and multiple punctures by hypodermic needles while maintaining resealability. The rise of lyophilized (freeze-dried) drugs, which almost exclusively rely on vial packaging, has further consolidated demand for vial stoppers with specialized ribbed designs that support vapor release during freeze-drying while ensuring a hermetic seal afterward. As biologics and complex injectables expand their share of the pharmaceutical pipeline, the role of vial stoppers as the primary elastomer closure system is cemented, sustaining their leadership within the market.

Lyophilization Applications Command Market Share in the Medical Rubber Stopper Industry

Lyophilization accounts for 40% of application share in the medical rubber stopper market, making it the most demanding and value-intensive use case. Freeze-drying is essential for the long-term stability of biologics, vaccines, peptides, and other moisture-sensitive drugs, and lyophilization stoppers are engineered with precision channels to allow sublimation of water vapor during the process while ensuring an airtight seal post-cycling. Their dominance is reinforced by the exponential growth of the biopharmaceutical industry, where more than half of pipeline drugs now require lyophilization for stability and global distribution. Furthermore, the surge in demand for cold-chain independent vaccines and injectable biologics, combined with regulatory scrutiny under USP <381> and EP 3.2.9 standards, has increased reliance on high-performance elastomer formulations. As freeze-dried drugs expand their share in oncology, rare disease treatment, and pandemic preparedness, lyophilization stoppers will remain the critical application segment driving technological innovation and premium pricing in the medical rubber stopper industry.

United States Medical Rubber Stopper Market Driven by Regulatory Compliance and Advanced Elastomer Technologies

The U.S. medical rubber stopper market is heavily influenced by stringent FDA regulations, which emphasize material compatibility, sterility, and product integrity. A notable 2018 FDA alert concerning a specific rubber stopper material in Becton-Dickinson syringes highlighted the critical role of stopper formulation in maintaining drug potency, driving manufacturers to invest in R&D for safer, more stable stoppers. Technological advancements focus on innovative elastomer materials and advanced coatings that reduce extractables and leachables, ensuring the integrity of biologics and specialty pharmaceuticals. Companies are also developing specialized stoppers for pre-filled syringes, meeting the rising demand in biopharmaceutical and injectable drug sectors.

Corporate investments are robust, with firms like West Pharmaceutical Services and AptarGroup expanding production and R&D capabilities. In July 2025, AptarGroup acquired Mod3 Pharma’s manufacturing capabilities, strengthening its position in clinical trial support and drug development. Manufacturers are increasingly adopting cleanroom production and automated quality control systems, while the FDA’s Unique Device Identifier (UDI) system drives enhanced product traceability. The U.S. market demonstrates a strong emphasis on high-quality, compliant, and technologically advanced rubber stoppers to meet the growing needs of the pharmaceutical industry.

Germany Medical Rubber Stopper Market Strengthened by MDR Compliance and High-Performance Sealing Innovations

Germany’s medical rubber stopper market operates under the EU MDR 2017/745 and EMA guidelines, which stress sterility, integrity, and traceability. These regulations have led to increased adoption of sterile, high-purity rubber stoppers for pharmaceutical vials and syringes. German manufacturers are recognized for high-performance sealing solutions, developing materials that enhance drug stability and provide superior chemical resistance.

The country’s robust pharmaceutical R&D ecosystem drives demand for advanced stopper solutions. Strategic corporate investments, such as Datwyler Holding Inc.’s April 2025 launch of serial component supply for GLP-1 therapies, highlight a focus on high-value, innovative pharmaceuticals. Germany’s market leadership reflects the combination of regulatory compliance, technological innovation, and strategic investments to deliver advanced rubber stoppers meeting global pharmaceutical standards.

China Medical Rubber Stopper Market Expands with Government Support and Domestic Manufacturing Focus

China’s medical rubber stopper industry is supported by active government initiatives aimed at advancing the high-end pharmaceutical and medical device sector. Regulatory reforms by the NMPA simplify approval processes for innovative products, promoting the domestic production of high-quality stoppers that meet international standards. Technological investments in automation and AI enhance manufacturing efficiency, product quality, and compliance with safety standards.

A major trend is the domestic substitution of imported products, with local companies expanding capacity to serve China’s booming pharmaceutical and healthcare sectors. The market’s growth is fueled by demand for specialized stoppers for vaccines, biologics, and injectable drugs, highlighting China’s emergence as a hub for high-quality, compliant, and technologically advanced rubber stopper solutions.

India Medical Rubber Stopper Market Boosted by Make in India and Vaccine Production Demand

India’s medical rubber stopper market is benefitting from the Make in India initiative, which encourages domestic manufacturing and reduces reliance on imports. The country has become a leading vaccine manufacturer, fulfilling approximately 60% of global demand, driving the need for secure packaging, including rubber stoppers. Advanced technologies, such as Teflon-coated stoppers that reduce friction and minimize particulate matter, are being increasingly adopted. Companies like Bharat Rubber Works are producing stoppers in various polymers to meet diverse pharmaceutical requirements.

Corporate investments are growing, supported by medical device parks and new production facilities, fostering R&D-driven innovation. The Indian market is particularly strong in the vaccine and injectable drug sectors, reflecting the rising demand for high-quality, compliant, and technologically advanced medical rubber stoppers that support the country’s expanding healthcare infrastructure.

Japan Medical Rubber Stopper Market Focused on Precision Manufacturing and High-Performance Biopharmaceutical Solutions

Japan’s medical rubber stopper market is underpinned by its reputation for precision manufacturing and advanced material technology. Manufacturers such as Nipro Corporation and Daikyo Seiko specialize in stoppers for vials, syringes, and pre-filled syringes, emphasizing quality, reliability, and superior barrier properties. The PMDA’s May 2025 amendment to the Pharmaceuticals and Medical Devices Act strengthens supply stability, impacting both production and supply chain logistics.

The market emphasizes high-performance and value-added products, with innovation focused on stoppers for sensitive biologics and specialty drugs. In late 2024, a co-development project between a Japanese company and a European pharmaceutical giant resulted in next-generation rubber stoppers with enhanced barrier properties, addressing the demands of emerging biopharmaceutical applications. Japan’s market exemplifies precision-engineered, high-quality, and technologically advanced stopper solutions for global pharmaceutical needs.

Medical Rubber Stopper Market Report Scope

Medical Rubber Stopper Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.1 Billion

|

|

Market Size (2034)

|

$3.5 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Material (Butyl Rubber, Bromobutyl Rubber, Chlorobutyl Rubber, Natural Rubber, Silicone Rubber, Others), By Product Type (Stoppers for Vials, Stoppers for Syringes, Stoppers for Bottles, Others), By Application (Lyophilization, Freeze-dried, Blood Collection, Others), By End-User (Pharmaceutical & Biotechnology Companies, Diagnostic Laboratories, Hospitals & Clinics, Research Institutes)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

West Pharmaceutical Services, Inc., Datwyler Holding Inc., AptarGroup, Inc., Bormioli Pharma S.p.A., Nipro Corporation, Daikyo Seiko, Ltd., The Plasticoid Company, Lonstroff AG, Jiangsu Hualan Pharmaceutical New Materials Co., Ltd., Hebei Oak One Co., Ltd., Shandong Pharmaceutical Glass Co., Ltd., Sumitomo Rubber Industries, Ltd., Becton, Dickinson and Company, SteriPack Group, Jintai Industry Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Medical Rubber Stopper Market Segmentation

By Material

- Butyl Rubber

- Bromobutyl Rubber

- Chlorobutyl Rubber

- Natural Rubber

- Silicone Rubber

- Others

By Product Type

- Stoppers for Vials

- Stoppers for Syringes

- Stoppers for Bottles

- Others

By Application

- Lyophilization

- Freeze-dried

- Blood Collection

- Others

By End-User

- Pharmaceutical & Biotechnology Companies

- Diagnostic Laboratories

- Hospitals & Clinics

- Research Institutes

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Medical Rubber Stopper Market

- West Pharmaceutical Services, Inc.

- Datwyler Holding Inc.

- AptarGroup, Inc.

- Bormioli Pharma S.p.A.

- Nipro Corporation

- Daikyo Seiko, Ltd.

- The Plasticoid Company

- Lonstroff AG

- Jiangsu Hualan Pharmaceutical New Materials Co., Ltd.

- Hebei Oak One Co., Ltd.

- Shandong Pharmaceutical Glass Co., Ltd.

- Sumitomo Rubber Industries, Ltd.

- Becton, Dickinson and Company

- SteriPack Group

- Jintai Industry Co., Ltd.

* List Not Exhaustive

Methodology

The research methodology for the global Medical Rubber Stopper market combines in-depth primary and secondary research, robust data validation, and predictive market modeling to deliver actionable intelligence for industry professionals. Primary research involved discussions with pharmaceutical manufacturers, packaging engineers, quality control specialists, and regulatory authorities to capture insights on trends such as polymer-based stoppers, fluoropolymer coatings, lyophilization compatibility, and ready-to-use (RTU) solutions. Secondary research incorporated regulatory guidelines from the FDA, USP, EMA, PMDA, and ICH, alongside corporate filings, press releases, and industry journals to validate market drivers, innovations, and strategic developments. Market sizing and forecasting (2025–2034) were conducted using top-down and bottom-up approaches, considering product types, materials, applications, and end-users, while factoring in biologics growth, supply chain reshoring, and anti-counterfeiting integration. Competitive landscape analysis included company expansions, mergers, sustainability initiatives, and new technology adoption to map global market dynamics. This comprehensive methodology ensures that USDAnalytics provides precise, data-driven insights into market growth, technological innovations, and emerging opportunities in the medical rubber stopper industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.