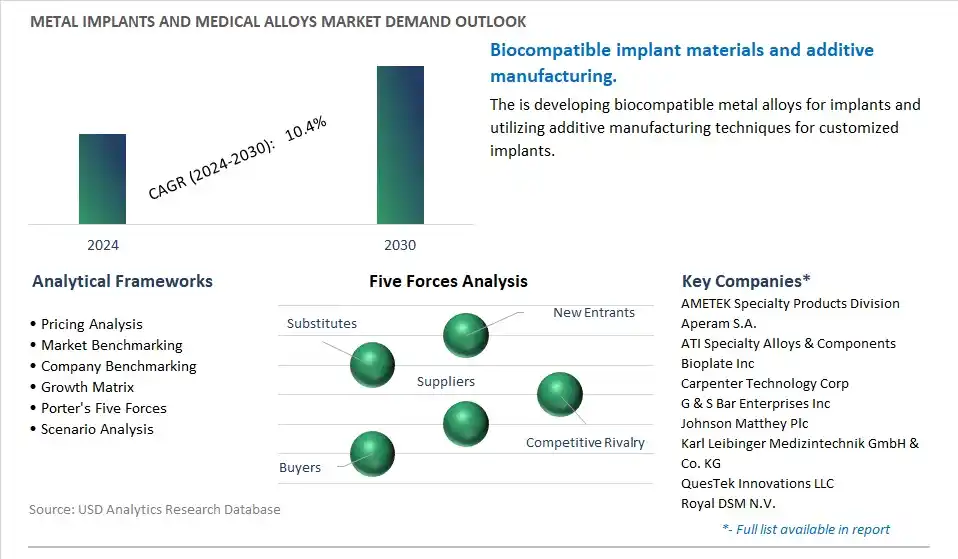

Metal Implants and Medical Alloys Market is estimated to increase at a Compounded Annual Growth Rate of 10.4% CAGR over the forecast period from 2024 to 2030

The Metal Implants and Medical Alloys Market study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments- By Type (Cobalt Chrome, Stainless Steel, Titanium, Others), By Application (Orthopedic, Dental, Spinal Fusion, Craniofacial, Stent, Others).

An Introduction to Metal Implants and Medical Alloys Market in 2024

Metal implants and medical alloys are essential components of orthopedic implants, dental prosthetics, cardiovascular devices, and surgical instruments used in medical and dental procedures. In 2024, the market for metal implants and medical alloys continues to expand, driven by the growing demand for orthopedic and dental implants, advancements in material science, and innovations in implant design and manufacturing technologies. Medical-grade alloys, such as titanium alloys, cobalt-chromium alloys, and stainless steel, offer biocompatibility, corrosion resistance, and mechanical properties tailored to specific implant applications, ensuring long-term performance and patient safety. With the aging population and increasing prevalence of musculoskeletal disorders, the demand for metal implants and medical alloys is expected to rise, fueling investments in research and development, regulatory compliance, and quality assurance measures. Moreover, advancements in additive manufacturing, surface treatments, and bioactive coatings enhance the versatility, customization, and osseointegration of metal implants, paving the way for next-generation implant materials and implantable medical devices that improve patient outcomes, restore mobility, and enhance quality of life.

Market Trend: Advancements in Biomaterials and Additive Manufacturing

A prominent trend in the metal implants and medical alloys market is the continuous advancements in biomaterials and additive manufacturing technologies. Biomaterials play a crucial role in the development of medical implants, prosthetics, and orthopedic devices, providing mechanical strength, biocompatibility, and corrosion resistance. Recent innovations in material science, metallurgy, and additive manufacturing techniques, such as 3D printing and laser sintering, have enabled the production of complex, patient-specific implants with enhanced properties and performance. Additionally, advancements in surface modification techniques, coatings, and bioactive materials are improving the integration of implants with host tissues, reducing implant rejection rates, and enhancing long-term biocompatibility. As manufacturers leverage these advancements to develop next-generation metal implants and medical alloys, the demand for customized, high-performance implants tailored to individual patient needs is expected to grow, driving market expansion and innovation in the metal implants and medical alloys sector.

Market Driver: Aging Population and Rising Incidence of Chronic Diseases

A key driver fueling the demand for metal implants and medical alloys is the aging population and the rising incidence of chronic diseases. As the global population ages, the prevalence of age-related conditions such as osteoarthritis, osteoporosis, and degenerative joint diseases is increasing, driving the need for joint replacement surgeries and orthopedic interventions. Additionally, the growing burden of chronic diseases such as cardiovascular disorders, cancer, and diabetes necessitates the use of medical implants for disease management and treatment. Metal implants and medical alloys, including titanium, stainless steel, and cobalt-chromium alloys, are widely used in orthopedic implants, cardiovascular stents, dental prosthetics, and surgical instruments due to their mechanical strength, biocompatibility, and durability. As healthcare systems strive to address the healthcare needs of an aging population and manage the growing burden of chronic diseases, the demand for metal implants and medical alloys as essential components of medical devices and implants is expected to rise, driving market growth and investment in the metal implants and medical alloys sector.

Market Opportunity: Expansion into Customized and Patient-Specific Implants

A significant opportunity for the metal implants and medical alloys market lies in the expansion into customized and patient-specific implants. With advancements in imaging technologies, computer-aided design (CAD), and additive manufacturing, there is a growing trend towards personalized medicine and customized healthcare solutions. Customized implants, tailored to individual patient anatomy and pathology, offer advantages such as improved fit, reduced risk of complications, and enhanced clinical outcomes compared to standard off-the-shelf implants. Additionally, patient-specific implants can address challenging surgical cases, complex anatomical variations, and revision surgeries, improving patient satisfaction and quality of life. By offering customized implant solutions based on patient-specific data, such as medical imaging scans and biomaterial preferences, manufacturers can differentiate their products, provide value-added services, and meet the unique needs of patients and surgeons. Collaborating with healthcare providers, academic medical centers, and medical device manufacturers to develop and commercialize customized implant solutions presents opportunities for metal implant and medical alloy companies to expand their market reach, establish partnerships, and capitalize on the growing demand for personalized healthcare solutions in orthopedics, traumatology, and reconstructive surgery. By embracing customization and patient-centric approaches, manufacturers can drive innovation, enhance competitiveness, and unlock new opportunities in the dynamic and evolving field of personalized medicine and orthopedic surgery.

Metal Implants and Medical Alloys Market Share Analysis: Titanium Implants for Orthopedic Applications is the fastest growing segment over the forecast period to 2030

Among the segments listed, titanium implants for orthopedic applications are experiencing rapid growth in the metal implants and medical alloys market. This growth is primarily driven by several factors, including the increasing prevalence of orthopedic conditions such as osteoarthritis and osteoporosis, the rising aging population, and advancements in implant materials and surgical techniques. Titanium implants offer several advantages over other materials, including excellent biocompatibility, corrosion resistance, and high strength-to-weight ratio, making them ideal for orthopedic implants such as hip and knee replacements, bone plates, and screws. Additionally, titanium implants promote osseointegration, allowing for better fixation and long-term stability within the bone. The growing demand for minimally invasive orthopedic surgeries, coupled with the expanding applications of titanium implants in trauma care, sports medicine, and joint reconstruction, further contribute to their rapid growth in the metal implants and medical alloys market. As healthcare systems worldwide prioritize improved patient outcomes, reduced implant failure rates, and enhanced quality of life for orthopedic patients, the demand for titanium implants is expected to continue growing significantly.

Metal Implants and Medical Alloys Competitive Analysis

The market research study provides in-depth insights into leading companies including the SWOT analyses, product profile, financial details, and recent developments acrossAMETEK Specialty Products Division, Aperam S.A., ATI Specialty Alloys & Components, Bioplate Inc, Carpenter Technology Corp, G & S Bar Enterprises Inc, Johnson Matthey Plc, Karl Leibinger Medizintechnik GmbH & Co. KG, QuesTek Innovations LLC, Royal DSM N.V., Stryker Medical Inc, Zimmer Biomet Holdings Inc

Metal Implants and Medical Alloys Market Segmentation

By Type

Cobalt Chrome

Stainless Steel

Titanium

Others

By Application

Orthopedic

Dental

Spinal Fusion

Craniofacial

Stent

Others

Geographical Analysis

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Metal Implants and Medical Alloys Market Companies

AMETEK Specialty Products Division

Aperam S.A.

ATI Specialty Alloys & Components

Bioplate Inc

Carpenter Technology Corp

G & S Bar Enterprises Inc

Johnson Matthey Plc

Karl Leibinger Medizintechnik GmbH & Co. KG

QuesTek Innovations LLC

Royal DSM N.V.

Stryker Medical Inc

Zimmer Biomet Holdings Inc

Reasons to Buy the Metal Implants and Medical Alloys Market Study

• Deepen your industry insights and navigate uncertainties for strategy formulation, CAPEX, and Operational decisions

• Gain access to detailed insights on the Metal Implants and Medical Alloys Market, encompassing current market size, growth trends, and forecasts till 2030.

• Access detailed competitor analysis, enabling competitive advantage through a thorough understanding of market players, strategies, and potential differentiation opportunities

• Stay ahead of the curve with insights on technological advancements, innovations, and upcoming trends

• Identify lucrative investment avenues and expansion opportunities within the Metal Implants and Medical Alloys Market industry, guided by robust, data-backed analysis.

• Understand regional and global markets through country-wise analysis, regional market potential, regulatory nuances, and dynamics

• Execute strategies with confidence and speed through information, analytics, and insights on the industry value chain

• Corporate leaders, strategists, financial experts, shareholders, asset managers, and governmental representatives can make long-term planning scenarios and build an integrated and timely understanding of market dynamics

• Benefit from tailored solutions and expert consultation based on report insights, providing personalized strategies aligned with specific business needs.

TABLE OF CONTENTS

1 Introduction to 2024 Metal Implants and Medical Alloys Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Metal Implants and Medical Alloys Market Size Outlook, $ Million, 2021 to 2030

3.2 Metal Implants and Medical Alloys Market Outlook by Type, $ Million, 2021 to 2030

3.3 Metal Implants and Medical Alloys Market Outlook by Product, $ Million, 2021 to 2030

3.4 Metal Implants and Medical Alloys Market Outlook by Application, $ Million, 2021 to 2030

3.5 Metal Implants and Medical Alloys Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Metal Implants and Medical Alloys Industry

4.2 Key Market Trends in Metal Implants and Medical Alloys Industry

4.3 Potential Opportunities in Metal Implants and Medical Alloys Industry

4.4 Key Challenges in Metal Implants and Medical Alloys Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Metal Implants and Medical Alloys Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Metal Implants and Medical Alloys Market Outlook by Segments

7.1 Metal Implants and Medical Alloys Market Outlook by Segments, $ Million, 2021- 2030

By Type

Cobalt Chrome

Stainless Steel

Titanium

Others

By Application

Orthopedic

Dental

Spinal Fusion

Craniofacial

Stent

Others

8 North America Metal Implants and Medical Alloys Market Analysis and Outlook To 2030

8.1 Introduction to North America Metal Implants and Medical Alloys Markets in 2024

8.2 North America Metal Implants and Medical Alloys Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Metal Implants and Medical Alloys Market size Outlook by Segments, 2021-2030

By Type

Cobalt Chrome

Stainless Steel

Titanium

Others

By Application

Orthopedic

Dental

Spinal Fusion

Craniofacial

Stent

Others

9 Europe Metal Implants and Medical Alloys Market Analysis and Outlook To 2030

9.1 Introduction to Europe Metal Implants and Medical Alloys Markets in 2024

9.2 Europe Metal Implants and Medical Alloys Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Metal Implants and Medical Alloys Market Size Outlook by Segments, 2021-2030

By Type

Cobalt Chrome

Stainless Steel

Titanium

Others

By Application

Orthopedic

Dental

Spinal Fusion

Craniofacial

Stent

Others

10 Asia Pacific Metal Implants and Medical Alloys Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Metal Implants and Medical Alloys Markets in 2024

10.2 Asia Pacific Metal Implants and Medical Alloys Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Metal Implants and Medical Alloys Market size Outlook by Segments, 2021-2030

By Type

Cobalt Chrome

Stainless Steel

Titanium

Others

By Application

Orthopedic

Dental

Spinal Fusion

Craniofacial

Stent

Others

11 South America Metal Implants and Medical Alloys Market Analysis and Outlook To 2030

11.1 Introduction to South America Metal Implants and Medical Alloys Markets in 2024

11.2 South America Metal Implants and Medical Alloys Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Metal Implants and Medical Alloys Market size Outlook by Segments, 2021-2030

By Type

Cobalt Chrome

Stainless Steel

Titanium

Others

By Application

Orthopedic

Dental

Spinal Fusion

Craniofacial

Stent

Others

12 Middle East and Africa Metal Implants and Medical Alloys Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Metal Implants and Medical Alloys Markets in 2024

12.2 Middle East and Africa Metal Implants and Medical Alloys Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Metal Implants and Medical Alloys Market size Outlook by Segments, 2021-2030

By Type

Cobalt Chrome

Stainless Steel

Titanium

Others

By Application

Orthopedic

Dental

Spinal Fusion

Craniofacial

Stent

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

List of Companies

AMETEK Specialty Products Division

Aperam S.A.

ATI Specialty Alloys & Components

Bioplate Inc

Carpenter Technology Corp

G & S Bar Enterprises Inc

Johnson Matthey Plc

Karl Leibinger Medizintechnik GmbH & Co. KG

QuesTek Innovations LLC

Royal DSM N.V.

Stryker Medical Inc

Zimmer Biomet Holdings Inc

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Cobalt Chrome

Stainless Steel

Titanium

Others

By Application

Orthopedic

Dental

Spinal Fusion

Craniofacial

Stent

Others

Countries Analyzed

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)