Metal Treatment Chemicals Market 2025–2034: Chrome-Free Passivation, PFAS-Free Suppressants, and EV Surface Innovation Driving $55.8 Billion Outlook at 5.6% CAGR

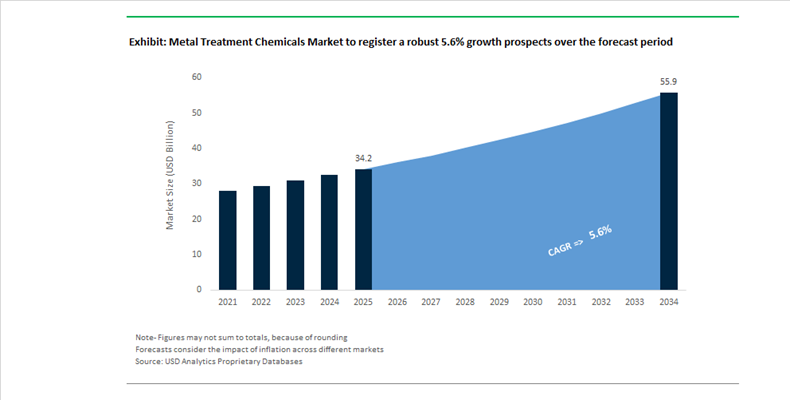

The Metal Treatment Chemicals Market is projected to expand from $34.2 billion in 2025 to $55.8 billion by 2034, registering a CAGR of 5.6%. Market growth is being driven by accelerating demand for surface pretreatment chemicals, passivation systems, conversion coatings, cleaners, sealants, and fume suppressants across automotive, EV battery manufacturing, electronics, metal packaging, and aluminum die-casting. Increasing global restrictions on hexavalent chromium, PFAS compounds, and phthalate-based plasticizers are reshaping product development pipelines. Regulatory frameworks such as the EU Battery Regulation (2023/1542), updated REACH compliance standards, and emerging EPA wastewater guidelines are compelling manufacturers to transition toward chromium-free, fluorine-free, and low-temperature curing chemistries while maintaining corrosion resistance, adhesion performance, and long-term durability.

Strategic consolidation and portfolio optimization intensified in 2024 and 2025. In November 2024, Quaker Houghton appointed Joseph Berquist as CEO and initiated a cost-optimization strategy targeting $20 million in savings to reinvest in sustainable industrial fluid technologies. In April 2025, Quaker Houghton completed the acquisition of Dipsol Chemicals, strengthening its Asia-Pacific footprint and expanding its high-value surface treatment portfolio. In June 2025, Nihon Parkerizing announced a new manufacturing plant in Chennai to serve India’s expanding automotive and electronics sectors. In August 2025, Henkel launched phthalate-free Darex COV sealants for metal packaging, enabling lower curing temperatures and improved carbon footprint metrics. In October 2025, Chemetall introduced Gardolene D, the first chromium- and fluoride-free passivation for copper foils, directly addressing EV battery pack performance and regulatory compliance. The same month, Chemetall formed a strategic partnership with Londian Wason to scale this chrome-free copper foil technology globally.

Innovation accelerated further into late 2025 and early 2026. In November 2025, SurTec and Chem-Trend introduced integrated die-casting process solutions combining advanced cleaners, passivations, and release agents for aluminum automotive components. At ISF 2026 in February, MKS’ Atotech presented Fumalock, the first fluorine-free, non-PFOS, and non-PFAS fume suppressant for hard-chrome plating, reducing hexavalent chromium emissions while aligning with EPA and REACH mandates. In early 2026, Atotech also launched Covertron 600, a Cr(VI)-free pretreatment system for plastic metallization used in decorative automotive and electronics applications. In February 2026, Henkel agreed to acquire Stahl Group for €2.1 billion, strengthening its specialty surface treatment and flexible coatings portfolio for automotive and packaging industries, signaling continued consolidation and integration across the global metal treatment chemicals value chain.

Metal Treatment Chemicals Market Trends and Opportunities

Trend: Mandatory Shift to Non-Chrome and Non-Phosphate Pretreatment Systems

The Metal Treatment Chemicals Market is undergoing a structural reset as regulators move decisively to eliminate hexavalent chromium and reduce phosphate sludge across automotive, battery, and industrial manufacturing. Tightened enforcement under the EU REACH Authorisation List, expanded again in November 2025, combined with intensified scrutiny of heavy-metal effluents by the U.S. EPA, has transformed non-compliance from a manageable risk into a production-stopping liability. As a result, OEMs and Tier 1 suppliers are accelerating the adoption of zirconium and titanium-organic hybrid pretreatments that deliver corrosion resistance and coating adhesion without hazardous residues.

A pivotal signal to the market came in October 2025 when Chemetall, part of BASF, launched Gardolene® D, the world’s first chromium- and fluoride-free passivation for copper foils used in EV batteries. This innovation aligns directly with the EU Battery Regulation 2023/1542, which mandates digital battery passports and strict hazardous substance thresholds by 2027. Environmental performance is translating into measurable outcomes. Company disclosures from BASF Coatings in May 2025 show that biomass-balanced and chrome-free surface technologies reduced CO2 emissions by roughly 8 million kilograms in 2024, with a stated target of 10 million kilograms by the end of 2025. From a performance standpoint, recent qualification trials indicate that advanced chrome-free passivation can extend EV battery service life by up to 6% after 1,000 cycles by improving surface energy and adhesion of anode materials. This combination of regulatory necessity, lifecycle sustainability, and functional gains is making non-chrome pretreatment the default specification for new platforms.

Trend: Supply Chain De-Risking and Strategic Sourcing of Thermal Salts

Geopolitical volatility and transport disruptions have exposed deep vulnerabilities in the supply of heat treatment salts such as nitrates, cyanides, and barium compounds. Aerospace, defense, and heavy engineering customers are now reengineering procurement strategies to ensure continuity of carburizing, hardening, and tempering operations. In November 2025, European Chemicals Agency recommended adding barium diboron tetraoxide to the REACH Authorisation List, triggering a wave of pre-emptive substitution across the aerospace supply base. This has accelerated R&D into alternative salt formulations and intensified qualification of secondary suppliers well ahead of potential sunset dates.

Supply chain risk has also taken on a strong ESG dimension. Data published by Achilles in 2025 highlights that disruptions linked to chokepoints such as the Red Sea and Suez Canal increased logistics costs for basic chemical precursors, while simultaneously driving a 12% rise in human rights violation alerts across chemical supply networks. In response, 67% of manufacturing executives now cite supplier diversification and real-time rate intelligence as top priorities, reflecting a shift toward anti-fragile, regionalized sourcing models. For metal treatment chemical producers, this trend is reshaping customer expectations toward guaranteed availability, transparent provenance, and resilient pricing structures rather than lowest-cost supply.

Opportunity: Specialized Chemical Passivation for Additively Manufactured Metal Parts

The transition of metal additive manufacturing from prototyping to serial production is unlocking a premium opportunity for advanced post-processing chemistries. Aerospace, medical implants, and high-performance automotive components increasingly rely on complex lattice geometries that traditional immersion treatments cannot adequately penetrate. This limitation is driving demand for ultrasonic, vapor-phase, and chemically assisted finishing solutions tailored to additively manufactured parts.

By mid-2025, REM Surface Engineering had adapted Isotropic Superfinishing and chemical polishing processes for missions involving NASA Jet Propulsion Laboratory, underscoring the criticality of advanced chemical finishing in removing loosely sintered powder and improving fatigue performance of ultralight lattice structures. Automation is rapidly becoming non-negotiable. Industry forecasts for 2025 indicate that manual post-processing cannot scale to meet the projected 21.3% increase in automotive metal 3D printing demand. Concurrently, research published in October 2025 demonstrates that tailored chemical treatments for titanium and nickel alloys significantly mitigate porosity and improve fatigue life, making specialized passivation chemistries a gatekeeper technology for regulated end-use sectors.

Opportunity: IoT-Integrated Chemical Management for Wastewater Compliance

Tightening wastewater discharge limits are pushing metal treatment operations toward digitally enabled chemical management systems. In the United States, updates to National Pollutant Discharge Elimination System permits and proposed EPA rules in October 2025 targeting toxic metals such as arsenic, cadmium, and selenium are raising compliance complexity. Parallel enforcement by India’s Central Pollution Control Board now caps hexavalent chromium at 0.1 mg/L for inland surface waters, significantly tightening allowable thresholds.

This regulatory environment is accelerating adoption of IoT-enabled dosing and monitoring solutions. Providers such as Grundfos are deploying SMART Digital Dosing systems capable of real-time flow adjustment with up to 1% accuracy, enabling precise control of pH and metal precipitation chemistry. Beyond compliance, the economics are increasingly attractive. In the Asia-Pacific region, Zero-Liquid-Discharge systems, while requiring capital expenditure four to five times higher than conventional treatment, are delivering payback periods as short as 2.8 years for 100 kiloliters per day facilities. Value is captured through recovered process water and avoidance of escalating non-compliance penalties, positioning smart chemical management not as a cost center but as a strategic efficiency and risk-mitigation investment.

Metal Treatment Chemicals Market Share and Segmentation Insights

Metal Cleaning Chemicals Lead Metal Treatment Chemicals Market Due to Critical Surface Preparation Role

Cleaning chemicals accounted for 34.80% of the Metal Treatment Chemicals Market share in 2025, making them the largest chemical category used in industrial metal surface treatment processes. Surface cleaning is the fundamental first stage in metal finishing and treatment operations, where contaminants such as oils, lubricants, machining fluids, oxide layers, and particulate residues must be removed to ensure proper adhesion of coatings, plating layers, and protective treatments. Metal cleaners are widely used across automotive manufacturing, electronics production, industrial machinery fabrication, aerospace component processing, and metal packaging facilities, supporting reliable surface preparation before downstream finishing processes. These cleaning formulations typically include alkaline cleaners, acidic cleaners, surfactant-based degreasers, and specialized metal surface conditioning agents that deliver efficient removal of contaminants while protecting the underlying metal substrate. In 2025, the industry has accelerated the shift toward aqueous metal cleaning systems, replacing solvent-based degreasers due to environmental and occupational safety regulations. This transition has encouraged the development of advanced surfactant technologies, controlled pH formulations, and optimized wastewater treatment compatibility while maintaining high cleaning efficiency for industrial metal processing operations.

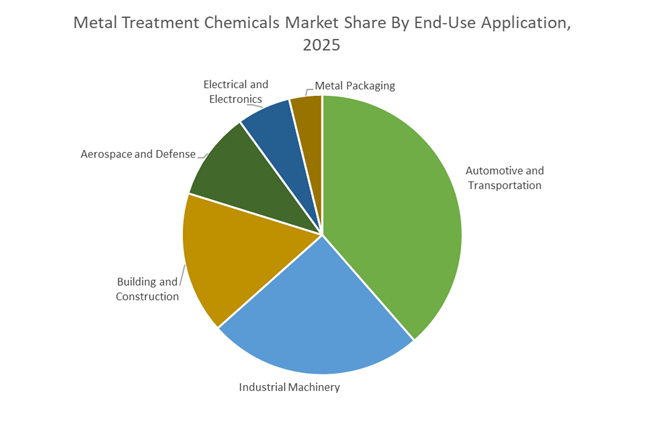

Automotive and Transportation Industry Drives the Largest Demand for Metal Treatment Chemicals

Automotive and transportation applications accounted for 38.60% of the Metal Treatment Chemicals Market share in 2025, making vehicle manufacturing the largest end-use sector for metal surface treatment technologies. Automotive production involves extensive metal processing stages including component cleaning, surface conditioning, phosphating, corrosion protection, and electrocoating preparation for body panels, structural parts, engine components, and chassis assemblies. Metal treatment chemicals are critical for ensuring strong paint adhesion, corrosion resistance, surface durability, and long-term vehicle reliability, particularly in environments exposed to road salts, moisture, and mechanical wear. The large global production volume of passenger cars, commercial vehicles, and transportation equipment continues to drive demand for metal treatment formulations. In 2025, the shift toward multi-material vehicle construction has introduced new challenges for metal treatment processes. Modern vehicle platforms increasingly combine steel, aluminum, magnesium alloys, and composite materials, requiring advanced treatment chemistries capable of delivering uniform corrosion protection and coating compatibility across mixed-metal assemblies, while maintaining consistent performance in automated automotive manufacturing lines.

Metal Treatment Chemicals Market Competitive Landscape

The metal treatment chemicals market in 2026 is driven by chromium-free, phosphorus-free, and low-temperature chemistries integrated with digital process control. AI-based bath monitoring, one-step pre-treatment systems, and energy-efficient lubricants are enabling 20–30% energy savings while meeting EV, aerospace, and sustainable packaging performance standards.

Henkel leads intelligent surface treatment with low-temperature lubricants and digital process control

Henkel AG & Co. KGaA is strengthening its leadership through digitalized metal treatment systems and low-energy chemistries. Its Bonderite E-CO platform enables real-time bath monitoring, automated dosing, and process optimization, significantly reducing chemical waste and improving line stability in high-speed can manufacturing. The company’s Bonderite L-FM 831 lubricant operates at just 43°C, delivering substantial energy and CO2 reductions compared to conventional systems. Strategic acquisition of ATP Adhesive Systems enhances its portfolio of water-based, low-VOC surface technologies for automotive and medical sectors. With strong growth in Mobility & Electronics, Henkel is advancing “Sustainability-as-a-Service” through integrated solutions that combine chemistry, data, and process efficiency.

Chemetall accelerates chromium-free passivation and integrated coating systems for EV batteries

Chemetall (BASF Surface Treatment) is leading the shift toward chromium-free and fluoride-free metal treatment chemistries with innovations like Gardolene® D, specifically designed for lithium battery copper foils. This technology enhances corrosion resistance and extends battery life by up to 6%, aligning with EU Battery Regulations. Strategic partnerships with major copper foil producers enable global deployment of advanced passivation systems. Its VIANT process integrates conversion coating and primer into a single step, reducing complexity and energy consumption. Investments in Italy and China strengthen localized support for aerospace and EV markets. Chemetall’s focus on integrated, high-performance surface engineering reinforces its leadership in sustainable metal treatment solutions.

Quaker Houghton expands EV-focused treatment solutions through strategic acquisitions and integration

Quaker Houghton is consolidating its position through a growth-by-acquisition strategy, integrating Dipsol Chemicals, Natech, and CSI into a unified metal treatment platform. The $155.2 million acquisition of Dipsol significantly enhances its capabilities in advanced plating and surface finishing across Asia-Pacific. Its “Total Process Fluid Management” approach combines metalworking fluids with surface treatment chemistries to deliver seamless solutions for automotive and aerospace OEMs. Cost optimization initiatives targeting $20 million in savings improve operational efficiency. The company is prioritizing EV battery-tray applications, offering specialized cleaners and coatings for lightweight aluminum alloys. This integrated strategy strengthens its competitive edge in high-growth, performance-driven markets.

Nihon Parkerizing strengthens Asian dominance with low-temperature phosphating and operational restructuring

Nihon Parkerizing Co., Ltd. is reinforcing its position in the Asian metal treatment market through organizational restructuring and technical innovation. The transfer of its processing business to Parker Processing Co., Ltd. enhances operational efficiency and resource allocation. Expansion in Chennai supports growing demand from South Asia’s automotive and electronics sectors. Its advancements in low-temperature phosphating reduce energy consumption while maintaining high corrosion resistance and durability. The company’s Parkerizing processes remain industry standards for structural steel treatment and anti-galling applications. With strong compliance frameworks and supply chain alignment, Nihon Parkerizing continues to lead in cost-effective, high-performance surface treatments.

AD International disrupts pretreatment with one-step systems and near-zero sludge technologies

AD International (AD Chemicals) is emerging as a disruptive player with its MM31® one-step pre-treatment system, combining cleaning, degreasing, and corrosion protection into a single process. This innovation significantly reduces process complexity, water usage, and sludge generation compared to traditional phosphating systems. Its PreCoat CPF technology enables manufacturers in appliance and HVAC sectors to eliminate energy-intensive steps while maintaining strong paint adhesion. The company is actively promoting phosphating-free solutions that align with tightening wastewater regulations. Focus on vertical powder coating lines and aluminum pre-treatment supports sustainability goals for the 2027 architectural cycle. AD Chemicals is positioning itself as a key challenger in efficient, low-carbon metal treatment technologies.

United States: PFAS Elimination and Hydrogen-Enabled Surface Processing

The United States metal treatment chemicals market is entering a decisive compliance and technology transition phase driven by environmental regulation and energy system shifts. The U.S. Environmental Protection Agency is finalizing revisions to Effluent Limitation Guidelines for metal finishing operations under 40 CFR Part 433. A Notice of Proposed Rulemaking scheduled for July 2026 targets PFAS discharges from chromium electroplating, anodizing, and chromate conversion coating processes. This regulatory trajectory is forcing plating shops and chemical suppliers to adopt PFAS-free fume suppressants and wetting agents, reshaping procurement standards across decorative and hard chrome applications. Complementing federal action, the California Air Resources Board enforced a certified list of non-PFOS wetting agents in late 2025, accelerating nationwide alignment ahead of anticipated parts-per-trillion wastewater thresholds by 2027.

Energy transition investments are influencing upstream chemistry. In November 2025, BASF and ExxonMobil signed a joint development agreement to scale methane pyrolysis, enabling low-emission hydrogen supply. This hydrogen is increasingly specified as a reducing agent in high-purity metal surface treatment and refining. In parallel, Afton Chemical launched a specialized additive suite for hydrogen-combustion heavy-duty engines in late 2025, embedding advanced metal passivators to mitigate oxidative stress and embrittlement. Downstream coatings capacity is also expanding. BASF’s Geismar, Louisiana investment, scheduled for a 2026 startup, lifts methylene diphenyl diisocyanate capacity to support polyurethane-based metal coatings and sealants that demand higher durability and chemical resistance.

China: Ultra-Low Emissions, Recycling Scale, and Integrated Verbund Production

China’s metal treatment chemicals market is being restructured by emissions mandates, recycling targets, and large-scale integrated manufacturing. Effective January 24, 2025, the Ministry of Industry and Information Technology issued Normative Conditions for the Steel Industry that mandate ultra-low emissions transformation by 2026. This includes replacing inefficient sintering and coke ovens with electric arc furnace steelmaking, which increases demand for EAF-compatible surface treatment chemicals and pickling inhibitors tailored to recycled feedstocks.

Recycling policy is a major demand driver. The Aluminium Action Plan released in March 2025 targets 15 million metric tonnes of recycled aluminum output by 2027, prioritizing Internet-enabled recycling platforms and relocation of smelting to clean-energy regions. These shifts require advanced deoxidizers, de-smutting agents, and stabilizers for variable scrap chemistries. Strategic alliances are shaping formulations. In November 2025, Nippon Paint and Allnex signed a cooperation agreement to develop bio-based sagging control resins and lower-VOC industrial coatings. Capacity investments reinforce supply. Lubrizol is finalizing a 63,000-ton-per-year expansion at Zhuhai in 2026 to supply metal deactivator-rich additive packages for the electric vehicle sector. BASF’s Zhanjiang Verbund site, a €10 billion project operating on renewable electricity, is scheduled to be operational by late 2025 and will serve as a global pilot for sustainable specialty chemicals used in metal surface treatment.

India: Incentivized Specialty Steel and ZLD-Driven Cluster Modernization

India’s metal treatment chemicals market is advancing through targeted incentives for specialty steel and accelerated adoption of water stewardship technologies. The third round of the Production Linked Incentive scheme launched in November 2025 offers incentives of 4 to 15% across 22 sub-categories, including super alloys, titanium alloys, and hybrid resin-coated steels. Disbursals beginning in FY 2026–27 are catalyzing demand for advanced pretreatments, passivators, and resin systems that meet export-grade performance and durability requirements.

Investment momentum is translating into an export-ready ecosystem. By September 2025, specialty steel initiatives had attracted ₹43,874 crore in committed investments, enabling domestic production of coated wire and tyre cord products for global automotive supply chains. Fiscal measures are reinforcing environmental upgrades. Chemical GST rationalization during 2025–2026 reduced duties on effluent treatment chemicals, accelerating Zero Liquid Discharge adoption across electroplating clusters in Maharashtra and Tamil Nadu. These clusters are transitioning to closed-loop rinsing, low-sludge pretreatments, and membrane-integrated treatment chemistries to meet tighter discharge norms while lowering operating costs.

Germany and European Union: REACH Alignment and Portfolio Agility

Germany and the wider European Union are defining compliance-led innovation in metal treatment chemicals through substance phase-outs and portfolio restructuring. In August 2025, Henkel introduced the Darex COV range of phthalate-free sealants for metal packaging, addressing tightening REACH scrutiny on endocrine disruptors while reducing curing temperatures to lower energy use. Regulatory alignment extends to formaldehyde. Germany is transitioning from national rules to EU Regulation 2023/1464, applicable from August 7, 2026, requiring reformulation of metal-treating resins and adhesives that release formaldehyde.

Corporate restructuring is reshaping market dynamics. In October 2025, BASF announced the sale of a majority stake in its coatings business to Carlyle and Qatar Investment Authority. This transaction enables the surface treatment brand Chemetall to operate with greater agility under private equity leadership from Q2 2026, accelerating response to REACH-driven reformulation and customer-specific compliance needs across automotive, packaging, and industrial coatings.

Country-Level Strategic Positioning in the Metal Treatment Chemicals Market

Metal Treatment Chemicals Market County Level Snapshot

|

Country / Region

|

Strategic Priority

|

Core Chemistry Focus

|

Policy or Regulatory Driver

|

Competitive Positioning

|

|

United States

|

PFAS phase-out and hydrogen transition

|

PFAS-free fume suppressants, metal passivators

|

EPA ELGs, CARB wetting agent rules

|

Early compliance and energy-linked innovation

|

|

China

|

Ultra-low emissions and recycling scale

|

De-smutting agents, EV-grade additives

|

MIIT steel norms, aluminum action plan

|

Integrated scale with renewable production

|

|

India

|

Specialty steel incentives and ZLD

|

Pretreatments, resin-coated systems

|

PLI scheme, GST rationalization

|

Cost-efficient modernization

|

|

Germany and EU

|

REACH compliance and portfolio agility

|

Phthalate-free sealants, low-formaldehyde resins

|

REACH updates, EU Regulation 2023/1464

|

Regulation-led reformulation leadership

|

Metal Treatment Chemicals Market Report Scope

Metal Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$34.2 Billion

|

|

Market Size (2034)

|

$55.8 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Chemical Type (Cleaners, Conversion Coatings, Plating Chemicals, Corrosion Inhibitors, Proprietary Additives), By Substrate (Iron and Steel, Aluminum and Light Alloys, Copper and Copper Alloys, Specialty Alloys), By Process Technology (Chemical and Electrochemical Treatment, Thermal and Mechanical Treatment, Vacuum Deposition Pre-treatment), By End-Use Application (Automotive and Transportation, Aerospace and Defense, Industrial Machinery, Building and Construction, Electrical and Electronics, Metal Packaging)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel, BASF, MacDermid Enthone, Dow, Nippon Paint Holdings, Quaker Houghton, Atotech, Nouryon, Oerlikon Surface Solutions, PPG Industries, Lubrizol, Nippon Parkerizing, Elementis, Grauer and Weil

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Metal Treatment Chemicals Market Segmentation

By Chemical Type

- Cleaners

- Conversion Coatings

- Plating Chemicals

- Corrosion Inhibitors

- Proprietary Additives

By Substrate

- Iron and Steel

- Aluminum and Light Alloys

- Copper and Copper Alloys

- Specialty Alloys

By Process Technology

- Chemical and Electrochemical Treatment

- Thermal and Mechanical Treatment

- Vacuum Deposition Pre-treatment

By End-Use Application

- Automotive and Transportation

- Aerospace and Defense

- Industrial Machinery

- Building and Construction

- Electrical and Electronics

- Metal Packaging

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Metal Treatment Chemicals Market

- Henkel

- BASF

- MacDermid Enthone

- Dow

- Nippon Paint Holdings

- Quaker Houghton

- Atotech

- Nouryon

- Oerlikon Surface Solutions

- PPG Industries

- Lubrizol

- Nippon Parkerizing

- Elementis

- Grauer and Weil

*- List not Exhaustive