Metallic Powder Coatings Market Size, Decorative Metal Finishes, and Energy-Efficient Coating Technologies Outlook

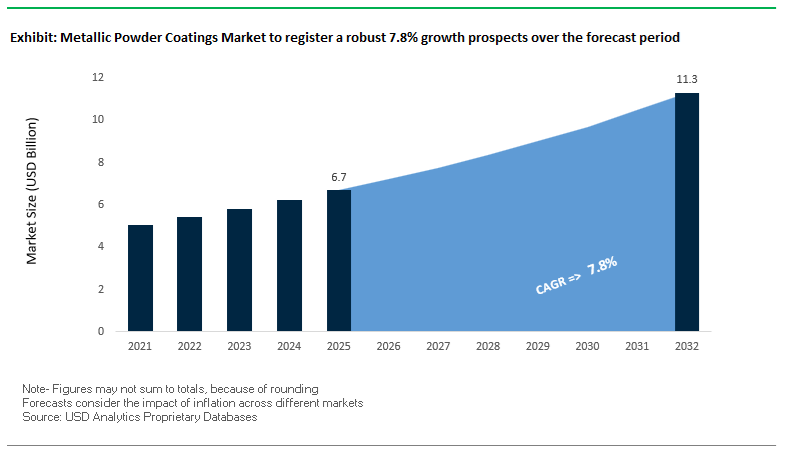

The global metallic powder coatings market was valued at $6.7 billion in 2025 and is projected to reach $11.3 billion by 2032, expanding at a strong CAGR of 7.8%. Growth is driven by rising demand for metallic powder coatings, bonded metallic pigments, architectural powder coatings, and decorative metal finishes across automotive, construction, appliances, furniture, and industrial equipment sectors. These coatings offer a combination of high durability, corrosion resistance, aesthetic appeal, and environmental compliance, making them increasingly preferred over traditional liquid coatings.

A key growth driver is the increasing adoption of premium metallic finishes in automotive exteriors, architectural facades, and consumer products, where visual differentiation and surface performance are critical. Advanced bonded metallic powder technologies are enabling consistent “flip-flop” color effects, improved recyclability, and uniform metallic dispersion, addressing historical challenges associated with metallic powder coatings. Additionally, the shift toward low-VOC, solvent-free, and energy-efficient coating systems is accelerating adoption, particularly in regions with stringent environmental regulations.

The market is also benefiting from the growing use of lightweight substrates such as aluminum, plastics, and composites, particularly in electric vehicles (EVs) and modern construction materials. Innovations in low-temperature curing, UV-curable powders, and hybrid resin systems are expanding application scope to heat-sensitive substrates, further driving market growth. Regionally, Asia-Pacific dominates due to strong construction and automotive manufacturing activity, while Europe and North America lead in advanced coating technologies and sustainability initiatives.

Market Analysis: Bonded Metallic Innovation, Sustainability Partnerships, and Capacity Expansion Driving Market Evolution

The metallic powder coatings industry is undergoing rapid transformation driven by technological innovation, strategic consolidation, and sustainability-focused initiatives. A major development occurred in February 2026, when AkzoNobel and Axalta announced a merger of equals, combining Interpon’s architectural metallic expertise with Axalta’s Alesta industrial portfolio. This consolidation is expected to significantly influence global R&D for bonded metallic pigments and advanced powder coating systems.

Product innovation continues to enhance both performance and application flexibility. In January 2026, PPG Industries launched a new series of eco-friendly metallic powder coatings featuring advanced bonding technology that ensures consistent metallic “flip-flop” effects even after multiple reclamation cycles, addressing a key limitation in powder coating reuse. Similarly, Axalta’s December 2025 advancements in UV-curable metallic powder coatings enable application on heat-sensitive substrates such as MDF and plastics, opening new opportunities in furniture and consumer goods manufacturing.

Sustainability and carbon reduction initiatives are becoming central to market development. In September 2025, a collaboration between AkzoNobel, Arkema, and BASF focused on reducing the carbon footprint of architectural powder coatings through the use of bio-based and recycled-content resins. This aligns with AkzoNobel’s May 2025 initiative to develop low-cure metallic powders, which can reduce energy consumption by up to 20% during application, supporting industrial decarbonization goals.

Capacity expansion and regional growth strategies are also shaping the market. Sherwin-Williams’ February 2026 expansion of powder coating production lines targets increasing demand for metallic and textured finishes in the North American off-highway and industrial equipment sectors. PPG Industries’ $300 million investment through 2028, including a new facility in Tennessee, further strengthens its position in advanced powder coatings for EV and industrial applications.

Innovation in aesthetics and application technology is expanding market opportunities. Jotun’s November 2025 “2026 Metallic Collection” focuses on enhanced color consistency and extreme weather resistance, targeting high-rise construction projects in demanding climates. Tiger Drylac’s July 2025 launch of 3D metallic powder coatings introduces advanced particle morphology control, enabling finishes that replicate the depth and appearance of liquid metallic paints in a single-coat powder application. Additionally, IGP Pulvertechnik’s January 2024 “Real Metal” powders provide authentic copper, brass, and steel finishes without the weight or oxidation challenges of actual metals.

Market Trend: Bonded Metallic Powder Technology Driving Color Consistency and High-Reclaim Efficiency in Architectural Extrusions

The metallic powder coatings industry is undergoing a decisive transition in architectural aluminum applications, with bonded metallic technology rapidly replacing traditional dry-blended systems. In bonded powders, metallic pigments such as aluminum flakes or mica are physically fused to resin particles, ensuring a uniform particle composition throughout application and recovery cycles. This structural integration eliminates the segregation issues that have historically plagued dry-blended powders, particularly during electrostatic spraying and overspray reclamation.

A key advantage of bonded metallic powders lies in their superior material utilization efficiency. These systems enable reclamation rates of 95% to 98% without compromising finish consistency, as the bonded pigments remain evenly distributed during recycling. In contrast, dry-blended powders experience pigment-resin separation during reclaim, leading to visible defects such as tiger striping and inconsistent metallic orientation. This efficiency gain significantly reduces material waste and enhances cost control in large-scale façade projects.

Color consistency is another critical performance parameter driving adoption. Architectural applications using bonded metallic powders report Delta E values below 0.5 across extensive curtain wall installations, ensuring near-perfect color uniformity. This represents a substantial improvement over legacy system, where variations exceeding Delta E 1.5 are common. As architectural specifications become increasingly stringent, bonded systems are emerging as the preferred solution for premium metallic finishes.

Durability requirements are also shaping material selection. More than 60% of high-end architectural metallic coatings now require compliance with AAMA 2605 standards, which mandate long-term color and gloss retention under severe weathering conditions. Bonded metallic powders are meeting these benchmarks, particularly in high-exposure environments such as coastal and subtropical regions, reinforcing their position as a high-performance solution for modern building envelopes.

Market Trend: Multi-Layer Metallic Powder Systems Enhancing Corrosion Resistance and Sustainability in Automotive Wheels

The automotive sector is driving innovation in metallic powder coatings through the adoption of multi-layer powder systems for aluminum wheels. This approach typically involves a metallic powder basecoat followed by a transparent powder clearcoat, creating a fully powder-based finishing system that replaces traditional liquid coating processes. The transition is driven by the need to meet elevated performance standards in corrosion resistance, aesthetics, and environmental sustainability, particularly in electric and luxury vehicle segments.

Corrosion resistance performance has advanced significantly with these systems. Modern metallic powder coatings for wheels are engineered to exceed 2,500 to 3,000 hours of Neutral Salt Spray testing under ASTM B117 conditions, representing a 50% improvement over the 1,000-hour benchmark that was standard five years ago. This enhanced durability is critical for vehicles operating in harsh environments, including regions with high salt exposure during winter months.

Filiform corrosion mitigation is another key performance gain. The integration of zirconium-based pretreatment technologies with metallic powder systems has reduced filiform corrosion incidence by approximately 80% on diamond-cut aluminum wheels. This improvement directly enhances the long-term aesthetic and structural integrity of exposed metallic surfaces, which are highly sensitive to corrosion-induced defects.

From a sustainability perspective, the shift to all-powder coating lines offers substantial environmental benefits. Eliminating solvent-based basecoat and clearcoat systems reduces carbon emissions by 30% to 40% per unit, primarily by removing solvent flash-off stages and the need for regenerative thermal oxidizers. This aligns with broader automotive industry goals related to decarbonization and regulatory compliance, positioning metallic powder coatings as a key enabler of sustainable vehicle manufacturing.

Market Opportunity: US GSA P100 Standards Expanding Demand for Metallic Powder Coatings in Federal Infrastructure Projects

The updated P100 Facilities Standards issued by the United States General Services Administration are creating a significant opportunity landscape for metallic powder coatings, particularly in architectural and infrastructure applications. These standards prioritize low-emission, durable finishing systems for federal buildings, aligning with national sustainability goals and green construction practices.

Powder-coated metallic finishes are increasingly specified as preferred solutions for aluminum façades, window frames, and structural components within federal projects. As inherently non-emitting materials, powder coatings contribute directly to LEED v4.1 and emerging v5 certification frameworks without requiring the extensive VOC testing associated with liquid-applied coatings. This simplifies compliance processes and enhances their attractiveness for large-scale public-sector developments.

The scale of the federal portfolio further amplifies this opportunity. With more than 370 million square feet of managed workspace, the GSA is driving a substantial retrofit and modernization cycle. Aging infrastructure coated with legacy liquid systems is being upgraded to high-performance powder-coated finishes that offer superior durability and reduced maintenance requirements. This transition is expected to generate sustained demand for metallic powder coatings, particularly in high-visibility architectural applications where aesthetics and longevity are critical.

Market Opportunity: China’s GB 30981.2-2025 Enforcement Driving Structural Shift Toward Powder-Based Metallic Coatings

China’s implementation of GB 30981.2-2025 is creating a transformative shift in the metallic coatings market by imposing strict limits on volatile organic compounds and hazardous substances. Effective from June 2026, this regulation is mandating compliance across industrial coating applications, significantly impacting the viability of traditional liquid metallic paints.

The new standard introduces stringent VOC limits that effectively disqualify many solvent-based metallic coatings from compliance. As a result, powder coating technologies are emerging as the most commercially viable alternative for achieving regulatory alignment. This shift is particularly pronounced in industrial sectors requiring metallic finishes, where performance and compliance must be balanced.

Regional enforcement mechanisms are further accelerating adoption. Under the Ministry of Ecology and Environment’s VOC Phase 3 Action Plan, key industrial regions such as the Beijing-Tianjin-Hebei cluster and the Yangtze River Delta are implementing localized bans on high-VOC liquid coatings in new industrial developments starting in 2027. These policies are creating a strong incentive for manufacturers to transition to powder-based systems ahead of enforcement timelines.

In addition to VOC restrictions, the regulation imposes strict limits on heavy metal content, including lead, cadmium, and mercury. This is driving demand for high-purity synthetic metallic pigments that meet regulatory thresholds while maintaining aesthetic performance. The convergence of environmental regulation, industrial policy, and manufacturing scale is positioning China as a critical growth market for metallic powder coatings, with global implications for technology adoption and supply chain strategies.

Metallic Powder Coatings Market Share and Segmentation Insights

Bonded Metallic Powder Coatings Capture 55.4% Share Driven by Premium Aesthetics and Process Reliability

The metallic powder coatings market by process type is dominated by bonded metallic powder coatings, accounting for 55.4% of the global market share in 2025, due to their superior finish quality and operational efficiency. In this process, metallic pigments (aluminum, bronze, pearlescent) are mechanically bonded to base powder particles, preventing separation during electrostatic spraying. This ensures consistent metallic appearance, uniform gloss, and reduced defects such as mottling and the Faraday cage effect, which are common in dry-blended systems. Additionally, bonded coatings enable up to 95% powder reclaim efficiency, significantly reducing material waste and lowering production costs. These advantages make them the preferred choice for automotive wheels, architectural aluminum, appliances, and premium furniture coatings, where high-end metallic finishes and sustainability are critical performance requirements.

Direct Sales Hold 48.9% Share Driven by OEM Demand for Precision Color Matching and Application Expertise

In the metallic powder coatings market by sales channel, direct sales lead with a 48.9% market share in 2025, reflecting the need for highly customized coating formulations and technical collaboration with end-users. Metallic powder coatings require precise control over pigment composition, particle size distribution, gloss levels, and texture effects, making direct manufacturer-to-OEM engagement essential for achieving consistent results. Large-scale industries such as automotive, construction, and consumer electronics rely on direct sourcing to ensure batch-to-batch consistency and brand-specific color standards. Furthermore, achieving optimal performance in metallic coatings requires advanced application expertise, including fine-tuning electrostatic spray parameters, gun positioning, and film thickness control. Direct sales teams provide critical on-site training, troubleshooting, and process optimization, giving them a competitive advantage over distributors and reinforcing their dominance in the global market.

Competitive Landscape in the Metallic Powder Coatings Market

AkzoNobel drives architectural and EV-focused metallic powder coating innovation

AkzoNobel, through its Interpon® and Resicoat® brands, remains a global benchmark in metallic powder coatings, particularly in architectural and mobility applications. Its 2026 merger with Axalta is expected to generate $600 million in synergies, strengthening its position across automotive and industrial sectors. The company introduced the Futura Collection 2026–2029 at PaintExpo, featuring the Interpon D2525 Anodic range that replicates anodized aluminum aesthetics with superior durability. Its collaboration with IPG Photonics has enabled laser-based curing technology, reducing energy consumption by up to 30%. Additionally, AkzoNobel is expanding its Resicoat portfolio for EV battery insulation, delivering high dielectric strength and safety performance in next-generation electric mobility systems.

PPG advances sustainable metallic powders with recycled content and instant-cure technologies

PPG Industries is strengthening its position in metallic powder coatings by integrating sustainability and advanced curing technologies. Its ENVIROLUXE™ Plus line incorporates up to 18% recycled plastic (rPET) and PFAS-free chemistry, aligning with tightening environmental regulations in 2026. The company is investing in radiation-curable coating technologies in France to develop instant-cure metallic finishes that reduce thermal stress on sensitive substrates. PPG’s acquisition of Ozark Materials enhances its infrastructure coating capabilities, integrating specialized marking and adhesion technologies. With a focus on high-edge protection and low-carbon formulations, PPG’s powders deliver 30% lower CO₂ emissions compared to conventional metallic coatings, positioning it as a leader in green coating solutions.

TIGER Coatings leads aesthetic innovation with bonded and 3D metallic powder technologies

TIGER Coatings is a specialized leader in metallic powder coatings, known for its advanced bonding processes and aesthetic surface innovations. Its proprietary 3D Metallic Powder Coatings technology creates a liquid-like depth and visual clarity in a single coat, eliminating the need for additional topcoats and reducing application costs. The company’s bonded metallic technology ensures uniform distribution of metallic flakes, preventing defects such as cloudiness or mottling. TIGER is actively promoting the transition from solvent-based coatings to recyclable powder systems, improving transfer efficiency and sustainability. Its Super Durable product line is widely used in high-end furniture and automotive aftermarket applications, offering superior resistance to UV exposure and mechanical wear.

Sherwin-Williams strengthens metallic powder coatings with durable and eco-friendly solutions

The Sherwin-Williams Company continues to dominate the North American metallic powder coatings market, leveraging its extensive distribution network and advanced product portfolio. Its Syntha Pulvin® HD range meets stringent AAMA 2604/2605 standards, ensuring long-term color retention and resistance to environmental degradation. The company is expanding its Powdura® ECO metallic line, incorporating recycled plastic resins to deliver sustainable solutions for industrial and medical device applications. Through its DesignHouse platform, Sherwin-Williams offers advanced digital color matching capabilities, enabling rapid customization for large-scale architectural projects. Strategic leadership changes in 2026 are supporting its expansion into Asia-Pacific and the integration of hybrid coating technologies.

Jotun advances smart and corrosion-resistant metallic powder coatings for energy sectors

Jotun A/S is a key player in metallic powder coatings, focusing on protective solutions for energy, infrastructure, and industrial applications. In 2026, the company launched advanced anti-corrosion systems featuring enhanced zinc-rich formulations, designed for offshore wind, oil, and gas environments. Its smart coating technologies incorporate micro-sensor capabilities that detect early-stage corrosion or surface degradation, improving maintenance planning. Jotun is also expanding its presence in energy and battery applications, supplying metallic coatings for high-temperature equipment such as boilers and furnaces. With a strong focus on ultra-low VOC epoxy-polyester hybrids, the company ensures compliance with global environmental standards while maintaining high performance and finish quality.

United States Metallic Powder Coatings Market: Sustainable Automotive Finishing and EV Supply Chain Expansion

The United States is emerging as a global epicenter for metallic powder coatings, driven by the rapid transformation of electric vehicle (EV) manufacturing, sustainable finishing technologies, and PFAS-free compliance mandates. The commercialization of next-generation thermoset metallic powder coatings is enabling superior corrosion resistance, particularly for EV battery enclosures and lightweight aluminum components, reinforcing the role of powder coatings in next-gen mobility solutions.

Strategic expansion activities, including Sherwin-Williams’ acquisition of industrial coatings divisions, are strengthening production capabilities for bonded metallic pigments across North America. Government-backed initiatives under the Inflation Reduction Act (IRA) are accelerating the shift from liquid coatings to powder-based systems to meet strict environmental standards. Innovations such as low-VOC metallic powders introduced by PPG Industries are further supporting sustainable manufacturing. Key applications are expanding into solar infrastructure, where super-durable metallic coatings protect systems from harsh environmental conditions. Regulatory enforcement of SCAQMD Rule 1113 continues to drive the adoption of near-zero emission coating technologies.

Germany Metallic Powder Coatings Market: Energy-Efficient Curing and Precision Engineering Leadership

Germany leads the metallic powder coatings market in Europe, driven by its focus on energy-efficient curing technologies, digitalization, and precision engineering. The development of ultra-low-energy (ULE) powder coatings, capable of curing at temperatures as low as 130°C, is enabling the application of metallic finishes on heat-sensitive substrates and mixed-material assemblies, expanding the application scope across industries.

The integration of digital twin technologies in coating lines is optimizing electrostatic application processes, reducing defects such as pigment nesting and improving overall coating uniformity. Significant investments in the Ruhr industrial region are modernizing coating infrastructure, transitioning from traditional liquid systems to automated powder coating solutions. Germany’s regulatory framework, including the Federal Climate Change Act, is mandating significant carbon reduction, accelerating the adoption of energy-efficient coating technologies. Additionally, companies like Carl Schlenk AG are advancing metallic pigment innovations to improve durability, shelf life, and aesthetic performance.

China Metallic Powder Coatings Market: High-Volume Production and Advanced Bonded Metallic Technologies

China dominates the global metallic powder coatings market in terms of volume, supported by large-scale manufacturing and strong environmental regulations. Policies such as the “Blue Sky Defense War” have effectively restricted new solvent-based coating installations, making powder coatings the preferred solution for industrial metal finishing.

Technological advancements include the scaling of encapsulated metallic pigment technologies, which enhance oxidation resistance and ensure consistent color effects in high-volume production. The market is witnessing strong demand in sectors such as telecommunications infrastructure, where metallic coatings are used for 5G and 6G base stations requiring high weather resistance and electromagnetic shielding properties. Investments in polyester resin production are stabilizing supply chains, while product innovations such as anti-fingerprint metallic powders are catering to premium smart appliance markets. Expansion by global players like Nippon Paint Holdings is further strengthening China’s position as a leader in advanced powder coating technologies.

India Metallic Powder Coatings Market: Infrastructure Development and Architectural Applications Driving Growth

India is witnessing rapid growth in the metallic powder coatings market, fueled by infrastructure expansion and increasing adoption in architectural applications. Government initiatives such as the National Infrastructure Pipeline and Make in India programs are driving demand for durable, high-performance coatings used in metro rail systems, airport terminals, and smart city infrastructure.

A significant technological shift from traditional dry-blending to bonding technologies is enabling domestic manufacturers to meet international standards such as Qualicoat and GSB. Foreign direct investment is boosting the establishment of specialized powder coating labs in Pune and Chennai, supporting the growing EV ecosystem. The use of metallic powder coatings on aluminum extrusions for high-rise buildings is replacing anodizing processes due to better aesthetics and environmental benefits. Additionally, government incentives under the Production Linked Incentive (PLI) scheme are accelerating demand in the white goods segment, particularly for premium appliances and consumer products.

Japan Metallic Powder Coatings Market: Advanced Functional Coatings and Precision Aesthetics

Japan’s metallic powder coatings market is defined by its focus on high-performance functional coatings, precision engineering, and advanced material innovation. The development of photocatalytic metallic powders is enabling self-cleaning surfaces that maintain their aesthetic appeal while decomposing organic pollutants under ambient light.

Technological advancements include low-film-thickness coatings, achieving full opacity at reduced thickness levels, improving material efficiency and reducing overall costs. Japan is also leading in the use of antimicrobial metallic coatings for high-end applications such as medical devices, robotics, and premium consumer electronics. Strict compliance with the Chemical Substances Control Law (CSCL) is driving the development of heavy-metal-free pigments, ensuring environmental safety and global export compliance. Investments by companies like Kansai Nerolac are further enhancing heat resistance and performance characteristics for precision engineering applications.

South Korea Metallic Powder Coatings Market: High-Performance Functional Coatings for Electronics and Shipbuilding

South Korea is emerging as a key player in the metallic powder coatings market, leveraging its expertise in electronics manufacturing, energy storage systems, and shipbuilding industries. Technological breakthroughs in high-dielectric metallic powder coatings are enabling their use in EV motor housings, providing both electrical insulation and decorative finishes.

The expansion of advanced R&D facilities, such as KCC Corporation’s Advanced Materials Center, is driving innovation in thermal management coatings for energy storage applications. Metallic powder coatings are widely used in consumer electronics, offering premium finishes for devices such as laptops and smartphones. Government initiatives under the K-Shipbuilding Strategy are promoting the adoption of anti-corrosive powder coatings in marine applications. Additionally, innovations in hybrid epoxy-polyester metallic powders are enhancing durability by combining chemical resistance with UV stability, strengthening South Korea’s position in high-performance coating technologies.

Metallic Powder Coatings Market Report Scope

Metallic Powder Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.7 Billion

|

|

Market Size (2032)

|

$11.3 Billion

|

|

Market Growth Rate

|

7.8%

|

|

Segments

|

By Process Type (Bonded Metallic Powder Coatings, Dry-Blended, Encapsulated or Stabilized Metallic Powder Coatings, Hybrid Effect Metallic Powder Coatings), By Resin Type (Polyester, Epoxy-Polyester, Epoxy, Polyurethane, Acrylic, Fluoropolymer), By Pigment Type (Aluminum Flakes, Mica and Pearlescent Pigments, Bronze and Copper Flakes, Stainless Steel and Nickel Pigments, Zinc-based Metallic Pigments), By Substrate Type (Aluminum, Steel, Galvanized Steel, Non-Metals), By End-Use Industry (Architectural, Automotive, Appliances and Consumer Goods, Furniture, Industrial Equipment, Leisure and Sports Equipment), By Functional Grade (Super Durable, Standard Durable, Anti-Corrosion, Heat-Resistant Metallic), By Sales Channel (Direct Sales, Specialty Industrial Distributors, Contract Coating Service Providers)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Akzo Nobel N.V., PPG Industries, Inc., The Sherwin-Williams Company, Axalta Coating Systems Ltd., Tiger Coatings GmbH and Co. KG, Jotun A/S, Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., IFS Coatings, TCI Powder Coatings, Prismatic Powders, Berger Paints India Limited, HMG Paints Limited, Primatek Coatings OU, Vitracoat America Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Metallic Powder Coatings Market Segmentation

By Process Type

- Bonded Metallic Powder Coatings

- Dry-Blended

- Encapsulated or Stabilized Metallic Powder Coatings

- Hybrid Effect Metallic Powder Coatings

By Resin Type

- Polyester

- Epoxy-Polyester

- Epoxy

- Polyurethane

- Acrylic

- Fluoropolymer

By Pigment Type

- Aluminum Flakes

- Mica and Pearlescent Pigments

- Bronze and Copper Flakes

- Stainless Steel and Nickel Pigments

- Zinc-based Metallic Pigments

By Substrate Type

- Aluminum

- Steel

- Galvanized Steel

- Non-Metals

By End-Use Industry

- Architectural

- Facades and Curtain Walls

- Window Frames and Door Systems

- Fencing and Railings

- Automotive

- Wheels and Rims

- Trim and Decorative Accents

- Under-the-hood Components

- Appliances and Consumer Goods

- White Goods

- Consumer Electronics

- Furniture

- Office and Corporate Furniture

- Outdoor

- Industrial Equipment

- Machinery and Tooling

- Electrical Enclosures

- Leisure and Sports Equipment

By Functional Grade

- Super Durable

- Standard Durable

- Anti-Corrosion

- Heat-Resistant Metallic

By Sales Channel

- Direct Sales

- Specialty Industrial Distributors

- Contract Coating Service Providers

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Metallic Powder Coatings Industry

- Akzo Nobel N.V.

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Axalta Coating Systems Ltd.

- Tiger Coatings GmbH & Co. KG

- Jotun A/S

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- IFS Coatings

- TCI Powder Coatings

- Prismatic Powders

- Berger Paints India Limited

- HMG Paints Limited

- Primatek Coatings OU

- Vitracoat America Inc.

*- List not Exhaustive