Micro Injection Molding Machine Market 2025–2034: AI-Driven Autonomy, EV Connector Miniaturization, and Medical Microfluidics Fueling $3.76 Trillion Outlook at 9.8% CAGR

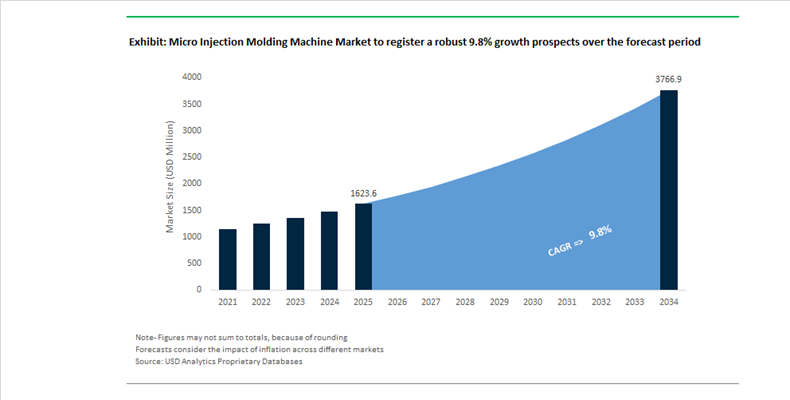

The Micro Injection Molding Machine Market is projected to expand from $1,623.6 Million in 2025 to $3,766.2 Million by 2034, registering a robust CAGR of 9.8%. Growth is being driven by precision-driven miniaturization in electronics, rapid expansion of electric vehicle (EV) sensor ecosystems, and increasing demand for high-value medical micro-components. Micro injection molding machines—engineered to process shot sizes as low as 0.01–0.1 cm³ with micron-level repeatability—are becoming essential in applications such as micro-gears, connectors, drug-delivery devices, and micro-optics. The industry is shifting from conventional parameter-based process control toward AI-defined quality targeting, reducing scrap rates and enabling high-volume micro-part manufacturing with near-zero tolerances.

In September 2025, ENGEL unveiled its “inject AI” autonomous molding cell, transitioning from “inject 4.0” digital monitoring to AI-led self-optimization. Operators input final quality parameters rather than machine settings, and the system autonomously adjusts injection pressure, speed, and cooling cycles—significantly improving consistency in micro-molding where deviations of a few microns can render parts unusable. In October 2025, Sumitomo (SHI) Demag introduced the SAM-C5 robot for ultra-compact automation, allowing complete micro-molding cells under three meters in height when paired with IntElect machines—an advantage for electronics cleanrooms with structural height constraints. At Compamed 2025, Wittmann Battenfeld demonstrated liquid silicone rubber (LSR) micro-lens production on its MicroPower 15/10 platform using a dual screw-plunger injection system to maintain thermal homogeneity for shots as small as 0.05 cm³.

Product innovation accelerated through 2025 and into 2026. In August 2025, FANUC launched the ROBOSHOT SC series, integrating AI-driven energy monitoring and enabling deeper mold compatibility without increasing footprint—addressing tooling complexity in micro-electronics and medical housings. Dr. Boy introduced the BOY XS E at Plastpol 2025, offering 100 kN clamping force on a 0.87 m² footprint, optimized for sprueless processing to minimize expensive polymer waste. Wittmann Group expanded production in China in December 2025 to localize machine supply for EV connector and sensor manufacturers. Academic-industry collaboration intensified in April 2025 when Ansbach University invested in Wittmann MicroPower systems for sustainable polymer research. By early 2026, Arburg announced global rollout of its Allrounder Trend line, while Atotech showcased complementary micro-plating solutions for 3D molded interconnect devices (MIDs), further integrating molding with electronics manufacturing. These developments underscore a decisive market shift toward AI-enabled, energy-efficient, and vertically integrated micro-manufacturing ecosystems.

Micro Injection Molding Machine Market Trends and Opportunities

Trend: Vertical Integration and Captive Micro-Molding by Medical Device OEMs

The micro injection molding machine market is being structurally reshaped by a clear shift toward vertical integration among Tier 1 medical device manufacturers. As competition intensifies in bio-absorbable implants, microneedle drug delivery, and lab-on-a-chip diagnostics, OEMs are increasingly internalizing micro-molding capabilities to protect intellectual property, compress development timelines, and eliminate reliance on capacity-constrained contract manufacturers. This transition reflects a strategic redefinition of micro-molding from a outsourced precision service into a core manufacturing competency.

Leading OEMs are prioritizing in-house production to safeguard proprietary micro-scale geometries that define competitive differentiation in ophthalmology, drug delivery, and minimally invasive devices. In August 2025, Freudenberg Medical confirmed the maturation of its silicone micro-molding platform, capable of producing ophthalmology-grade components such as sub-millimeter punctum plugs. By internalizing this capability, OEMs gain tighter control over design iterations, regulatory documentation, and process validation, which is critical under increasingly stringent FDA and MDR scrutiny.

Supply chain resilience initiatives have further accelerated this trend. Following early-2025 resilience programs announced by B. Braun Medical, many OEMs now mandate internal production of critical precision parts to reduce supplier risk and accelerate design-for-manufacturing cycles. Industry benchmarks indicate that direct integration of micro-molding into R&D and pilot production can reduce in-vitro diagnostics and consumables launch timelines by up to 30%. This has direct implications for machine demand, favoring compact, cleanroom-compatible systems such as Sumitomo (SHI) Demag’s SAM-C5 platform, which enables seamless deployment within ISO Class 7 and 8 cleanrooms without facility expansion.

Trend: AI-Native and Vision-Augmented Closed-Loop Process Control

The micro injection molding machine market is rapidly transitioning from operator-dependent parameter tuning to AI-native, self-correcting production environments. As tolerances shrink below 10 microns and part weights fall into the milligram range, manual intervention introduces unacceptable variability. Manufacturers are therefore embedding artificial intelligence, machine vision, and real-time sensor feedback directly into machine architecture to achieve autonomous process stability.

By mid-2025, inline vision inspection systems capable of 100% part verification had moved from pilot deployments to commercial scale. AI-powered inspection platforms from suppliers such as Krevera can identify up to 30 defect classes in real time, including flash, short shots, and micro-burrs. Reported results include scrap reductions of up to 30% and per-machine ROI ranging from $130,000 to $400,000 annually, driven by lower waste and reduced manual inspection labor.

Control system innovation is reinforcing this shift. At K 2025, Arburg introduced the Gestica lite control architecture on its Allrounder Trend series, enabling semi-autonomous optimization of injection pressure, clamping force, and cooling profiles. These systems lower the skills barrier for operators while ensuring repeatable part quality, a critical advantage as labor shortages intensify in advanced manufacturing. In parallel, Industry 4.0 connectivity using OPC UA protocols and embedded sensors is enabling predictive maintenance by detecting process drift within a handful of cycles, materially improving uptime in high-volume production of micro-connectors, sensors, and precision housings.

Opportunity: Multi-Material Overmolding for Implantables and Wearable Medical Devices

The convergence of digital health, implantable electronics, and biocompatible materials is opening a high-margin opportunity for two-component and multi-material micro injection molding machines. Medical device manufacturers increasingly require the ability to hermetically seal sensitive electronics within flexible, patient-safe housings while maintaining ultra-compact form factors. This has elevated demand for micro-molding platforms capable of precision overmolding with thermoplastics and elastomers in a single production cell.

Liquid Silicone Rubber overmolding has emerged as a preferred solution for encapsulating neurostimulators, biosensors, and wearable health monitors due to its flexibility, thermal stability, and biocompatibility. At K 2025, Sumitomo (SHI) Demag showcased its IntElect Multi R platform, designed specifically for micro-scale multi-material medical applications. Advanced tooling now enables feature sizes below 100 microns, supporting the rapidly expanding medical overmolding segment, which is projected to reach $1.9 billion in 2025.

This capability is particularly critical for devices that must survive repeated sterilization cycles while maintaining electrical integrity. Overmolding rigid thermoplastics onto flexible elastomers allows manufacturers to create sealed sensor housings that withstand autoclaving without compromising flexibility or signal transmission. As connected medical devices move from external wearables to partially implantable platforms, demand for precision multi-material micro injection molding machines is expected to accelerate sharply.

Opportunity: High-Mix, Low-Volume Agility for Defense and Aerospace Micro-Components

Defense and aerospace applications represent a structurally different but highly attractive growth channel for micro injection molding machine suppliers. Miniaturized guidance systems, UAV optics, and satellite subsystems increasingly rely on micro-scale components produced from high-performance polymers and advanced metals. These programs demand exceptional dimensional consistency, zero material waste, and rapid changeover between small production lots.

High-value polymers such as PEEK and LCP require precise thermal management to prevent degradation, making direct-gating and runnerless systems essential. Technologies that eliminate cold runners can reduce material waste by an order of magnitude, a critical factor when runner mass traditionally exceeds part mass by up to ten times. This near-net-shape efficiency significantly improves cost control for defense contractors operating under fixed-price programs.

Parallel growth is occurring in metal injection molding for aerospace micro-parts with internal channels and thin-wall geometries. Nickel-based superalloys and titanium powders are increasingly used to achieve weight reduction without compromising strength, supporting mission-critical performance in satellites and drones. Modular machine concepts such as Wittmann’s FlexCell architecture are gaining traction due to their minimal footprint and rapid reconfiguration capabilities. This agility enables defense manufacturers to produce high-mix, low-volume components with extreme dimensional repeatability, positioning advanced micro injection molding systems as a strategic asset in next-generation aerospace and defense manufacturing.

Micro Injection Molding Machine Market Share and Segmentation Insights

Fully Electric Machines Dominate Micro Injection Molding Machine Market Due to Precision Manufacturing Capabilities

Fully electric micro injection molding machines accounted for 58.60% of the Micro Injection Molding Machine Market share in 2025, establishing them as the preferred technology for manufacturing ultra-small, high-precision plastic components. These machines use electric servo motors and digital motion control systems to precisely regulate injection pressure, shot volume, injection speed, and clamping force, enabling accurate molding of parts with micron-level tolerances and shot weights measured in milligrams. Compared with hydraulic systems, fully electric machines deliver superior repeatability, cleaner operation, lower energy consumption, and minimal process variability, which are critical requirements in industries that demand extreme manufacturing precision. In addition, the elimination of hydraulic oil reduces contamination risks, making these machines suitable for cleanroom production environments used in medical device and electronics manufacturing. In 2025, machine manufacturers have introduced advanced digital control systems, closed-loop process monitoring, and real-time parameter adjustment capabilities, allowing operators to monitor every injection cycle and maintain consistent micro-part quality across high-volume production runs.

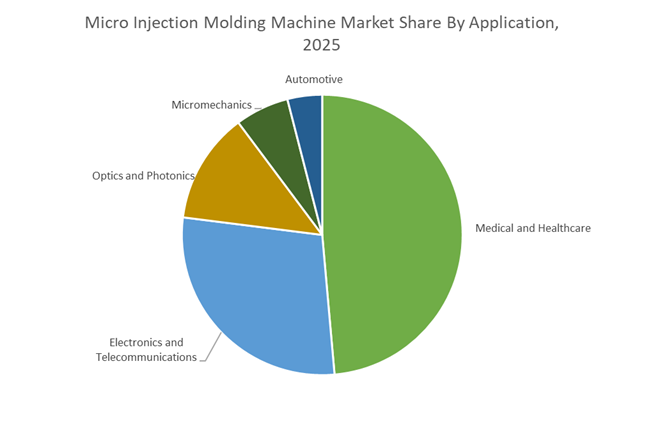

Medical and Healthcare Sector Drives the Largest Demand for Micro Injection Molding Machines

Medical and healthcare applications accounted for 48.60% of the Micro Injection Molding Machine Market share in 2025, making the sector the largest consumer of micro molding technologies. Micro injection molding is widely used to manufacture precision medical components such as microfluidic diagnostic chips, microneedles, implantable drug delivery devices, surgical instrument components, catheter parts, and minimally invasive surgical tools. These products require extremely tight tolerances, consistent material properties, and strict manufacturing reproducibility to meet medical regulatory standards. The rapid advancement of minimally invasive surgical techniques, wearable medical technologies, and point-of-care diagnostic systems continues to increase demand for miniature polymer components that can only be produced through micro molding processes. In 2025, ongoing medical device miniaturization trends have pushed the limits of molding technology, requiring micro injection molding machines capable of producing complex geometries with micro-scale features and extremely thin walls while maintaining precise dimensional accuracy and repeatability across large production volumes.

Micro Injection Molding Machine Market Competitive Landscape

The micro injection molding machine market in 2026 is driven by AI-enabled precision manufacturing, all-electric systems, and cleanroom-integrated automation. Competitive leadership is defined by sub-10 micron accuracy, Industry 4.0 connectivity, and fully autonomous molding cells for medical microcomponents, microfluidics, and high-density electronics applications.

Sumitomo (SHI) Demag accelerates ultra-fast all-electric micro molding with compact automation integration

Sumitomo (SHI) Demag is strengthening its leadership in micro injection molding through high-speed, all-electric platforms and modular automation. Its SAM-C5 robot, launched at K 2025, is optimized for six-second cycle times while maintaining a compact footprint under 3 meters. The PAC-E series demonstrates advanced thin-wall molding with 0.3 mm thickness and 2.6-second cycles across 48 cavities, highlighting unmatched throughput. The company is advancing 2K multi-component molding, enabling complex micro-part integration without secondary assembly. Its ECO vacuum technology reduces energy consumption through sensor-driven optimization, aligning with Net Zero manufacturing goals. Sumitomo’s focus on precision, speed, and energy efficiency positions it as a leader in high-volume micro medical and electronics production.

ENGEL pioneers autonomous injection molding cells with AI-driven process self-optimization

ENGEL is redefining the micro molding landscape with its inject AI framework, enabling fully autonomous manufacturing environments. The ENGEL Virtual Assistant (EVA) provides real-time troubleshooting by interfacing directly with machine documentation, reducing reliance on skilled operators. Its autonomous molding cell, unveiled at K 2025, allows users to input quality parameters while the system self-adjusts process variables in real time. The expansion into India with a fully electric 1,000 kN machine supports cost-sensitive, high-precision applications in medical and packaging sectors. Tie-bar-less e-motion machines enable larger molds within compact cleanroom footprints, improving production density. ENGEL’s AI-driven automation and digital integration position it at the forefront of Industry 4.0 micro manufacturing.

Arburg integrates intuitive control systems and sustainable materials into precision micro molding

Arburg is enhancing its competitive position through user-centric control systems and advanced material processing technologies. The Gestica lite interface simplifies machine operation, enabling efficient production even with less-skilled operators. Its Allrounder Trend series integrates RecyclatePilot software to stabilize shot weights when using post-consumer recyclates, addressing sustainability challenges. Arburg is also pioneering paper injection molding, processing fiber-rich materials to create biodegradable components. In medical applications, its cleanroom solutions deliver ISO 7-compliant syringe production with Moldlife Sense monitoring for predictive maintenance. The company’s focus on sustainability, digital control, and precision engineering strengthens its role in next-generation micro molding.

Wittmann Battenfeld delivers ultra-low waste micro molding with MicroPower platforms and rapid prototyping capabilities

Wittmann Battenfeld is a specialist in ultra-precision micro molding, with its MicroPower 15/10 system designed for near-zero material waste and high repeatability. The platform supports production of microfluidic lab-on-chip devices using 3D-printed mold inserts, enabling rapid prototyping and scalable manufacturing. Expansion of its China facility enhances local production capacity for high-precision electronics components. The EcoPrimus series offers standardized, energy-efficient solutions for cost-sensitive applications without compromising performance. Strategic collaborations with academic institutions further strengthen innovation in micro-part repeatability and process optimization. Wittmann’s focus on efficiency, precision, and R&D integration positions it strongly in niche micro manufacturing segments.

FANUC enhances micro molding efficiency with AI-driven robotics and IoT-enabled production systems

FANUC is leveraging its expertise in all-electric machinery and robotics to deliver high-efficiency micro injection molding solutions with low total cost of ownership. The ROBOSHOT SC series offers a compact design with a 40% increase in clamp speed, boosting throughput for precision components. Its AI-based plasticizing energy monitor optimizes energy consumption by analyzing thermal and shear dynamics during processing. The ROBOSHOT LINKi2 IoT platform enables real-time quality monitoring and seamless integration with digital factory systems. FANUC’s commitment to sustainability is reflected in its EcoVadis Platinum rating and use of energy-efficient technologies. Its combination of AI, robotics, and reliability makes it a key player in automated micro molding ecosystems.

Germany: Autonomous Micro-Cells and Medical-Grade Validation at Industrial Scale

Germany continues to define the technological frontier of micro injection molding through compact automation, AI-driven process control, and accelerated medical validation. At K 2025 in Düsseldorf, Sumitomo (SHI) Demag and Arburg introduced fully electric micro-cells optimized for cleanroom manufacturing. Sumitomo’s IntElect 75, integrated with SAM-C5 robotics, achieved a total system height below three meters, enabling ultra-compact ISO-class cleanroom layouts demanded by 2026 medical device programs. This form factor advantage directly addresses space-constrained European production floors where cleanroom real estate costs remain elevated.

Process autonomy is emerging as a decisive differentiator. ENGEL launched its self-regulating injection molding platform using the iQ process observer enhanced with artificial intelligence. These systems continuously detect micro-variations in melt viscosity, clamp force, and cavity pressure, enabling real-time correction to support zero-defect manufacturing for micro-optics and implantable components. Equally material is the digital validation solution co-developed by ENGEL and Hack, which automates DQ-to-PQ workflows and cuts medical certification timelines by up to 40%. Arburg’s ALLROUNDER MORE 2000 further reinforces Germany’s position by enabling high-cavity micro-molding without mold rotation, directly targeting multi-material micro-sensors and 5G connector demand scheduled for 2026 programs.

Japan: Ultra-Stable Injection Architecture and Lightweight Metal Micro-Molding

Japan’s competitive edge rests on process stability at micro-scale and the expansion of micro-molding into light metals. Sodick commercialized its m:MIM specification in 2025, leveraging the proprietary V-LINE® system that separates plasticizing from injection. This architecture ensures highly stable melt conditions, which is critical for micro metal injection molding of gears and surgical instruments where dimensional drift is unacceptable. In parallel, Japanese OEMs broadened magnesium micro-molding using the LMI450 platform, positioning micro injection molding as a viable alternative to traditional machining for aerospace and EV micro-connectors.

Export data underscores a strategic shift toward premium systems. October 2025 trade figures show Japan exported ¥9.27 billion in injection molding machinery, with micro-capable, high-precision units to the United States rising by ¥2.19 billion despite a seasonal volume dip. This reflects sustained overseas demand for Japanese reliability in ultra-precision molding as Western manufacturers prioritize yield stability over capex minimization.

Austria: Cleanroom-Integrated Micro Platforms and Rapid Microfluidic Prototyping

Austria has carved out a distinct position through highly integrated micro-molding cells optimized for medical applications. Wittmann Battenfeld demonstrated production of vascular clamps on its MicroPower 15 platform, using an injection plunger that reaches the mold parting line to virtually eliminate sprue waste. This design is economically significant for medical-grade bio-resins, where material losses materially impact unit economics.

Innovation in tooling is accelerating time-to-market. Wittmann’s collaboration with NanoVoxel showcased four-cavity micro-molding using 3D-printed nano-structured inserts, enabling rapid prototyping of lab-on-a-chip devices with micron-scale features. The fully integrated laminar flow box and consolidated peripherals within a two-square-meter footprint position Austria as a preferred supplier for plug-and-produce cleanroom cells aligned with 2026 commercialization timelines.

United States: Reshoring Momentum and Medical Device Demand Pull

The United States is experiencing demand-led expansion driven by healthcare manufacturing growth and electronics miniaturization. The U.S. Food and Drug Administration reported a 28% increase in registered medical device facilities since 2020, which is translating into higher procurement of 10 to 30 ton micro injection units for minimally invasive surgical tools planned for 2026 production. Concurrently, the U.S. Bureau of Economic Analysis recorded $89 billion in electronics manufacturing growth during 2024–2025, with roughly 40% attributed to component miniaturization that relies on micro-molded parts.

Policy-driven reshoring is reinforcing this trajectory. Infrastructure investments under the CHIPS Act are prompting domestic installation of all-electric micro-molding lines, including the IntElect series, to localize production of micro-connectors and reduce long-lead offshore dependencies. This is shifting procurement criteria toward energy efficiency, repeatability, and digital process traceability rather than lowest initial cost.

India: Trade Protection, All-Electric Exemptions, and Medical Hub Expansion

India’s market is being structurally reshaped by trade policy and targeted exemptions. In June 2025, the Ministry of Finance, India imposed definitive anti-dumping duties of up to 63% on plastic processing machines from China and Taiwan for five years. Crucially, all-electric injection molding machines were excluded, creating a strong incentive to adopt premium, all-electric micro-molding platforms from European and Japanese suppliers within India’s medical manufacturing clusters.

National production goals are amplifying demand. Preparations for Plastindia 2026 emphasize a 7% increase in domestic medical device output, driving localized procurement of micro injection molding machines capable of processing PEEK and PPS for orthopedic and implant applications. Chennai and Hyderabad are emerging as focal hubs where regulatory alignment, duty exemptions, and rising clinical manufacturing requirements converge.

Comparative Snapshot: Country-Level Positioning in the Micro Injection Molding Machine Market

Micro Injection Molding Machine Market County Level Snapshot

|

Country

|

Strategic Focus

|

Technology Lever

|

Primary End-Use Pull

|

Market Implication

|

|

Germany

|

Autonomous micro-cells and digital validation

|

AI process control, compact cleanroom systems

|

Medical, micro-optics, 5G

|

Leadership in zero-defect, certified production

|

|

Japan

|

Process stability and metal micro-molding

|

V-LINE® injection, magnesium molding

|

Aerospace, EV, surgical tools

|

Premium export growth

|

|

Austria

|

Integrated cleanroom micro platforms

|

Sprue-less injection, nano-structured tooling

|

Medical devices, microfluidics

|

Fast prototyping to scale

|

|

United States

|

Reshoring and healthcare expansion

|

All-electric micro lines

|

Medical devices, electronics

|

Domestic capacity build-out

|

|

India

|

Trade protection with electric exemption

|

All-electric micro-molding

|

Medical devices, implants

|

Accelerated adoption of high-end systems

|

Micro Injection Molding Machine Market Report Scope

Micro Injection Molding Machine Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1623.6 Million

|

|

Market Size (2034)

|

$3766.2 Million

|

|

Market Growth Rate

|

9.8%

|

|

Segments

|

By Machine Type (Fully Electric, Hydraulic, Hybrid), By Clamping Force (Up to 10 Tons, 10 to 30 Tons, 30 to 40 Tons), By Application (Medical and Healthcare, Electronics and Telecommunications, Automotive, Optics and Photonics, Micromechanics), By Material Type (Thermoplastics, Thermosets, Metal Powders, Ceramic Powders)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sumitomo Demag, Arburg, ENGEL, Wittmann Battenfeld, Sodick, FANUC, Milacron, KraussMaffei, Nissei Plastic Industrial, Shibaura Machine, BOY Machines, Babyplast, Haitian International, Toyo Machinery and Metal, Chen Hsong

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Micro Injection Molding Machine Market Segmentation

By Machine Type

- Fully Electric

- Hydraulic

- Hybrid

By Clamping Force

- Up to 10 Tons

- 10 to 30 Tons

- 30 to 40 Tons

By Application

- Medical and Healthcare

- Electronics and Telecommunications

- Automotive

- Optics and Photonics

- Micromechanics

By Material Type

- Thermoplastics

- Thermosets

- Metal Powders

- Ceramic Powders

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Micro Injection Molding Machine Market

- Sumitomo Demag

- Arburg

- ENGEL

- Wittmann Battenfeld

- Sodick

- FANUC

- Milacron

- KraussMaffei

- Nissei Plastic Industrial

- Shibaura Machine

- BOY Machines

- Babyplast

- Haitian International

- Toyo Machinery and Metal

- Chen Hsong

*- List not Exhaustive