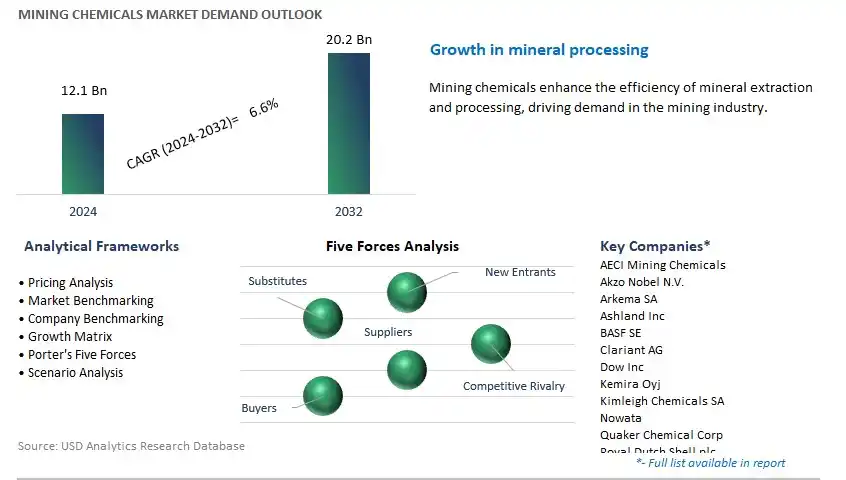

Global Mining Chemicals Market Size is valued at $12.1 Billion in 2024 and is forecast to register a growth rate (CAGR) of 6.6% to reach $20.2 Billion by 2032.

The global Mining Chemicals Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Ore (Powder Gold, Iron, Copper, Phosphate, Others), By Type (Collectors, Coatings, Flocculants, Grinding Aids, Solvent Extractants, Dust Suppressants, Defoamers, Antiscalants, Biocides, Lubricants, Frothers, Others), By Application (Mineral Processing, Explosives and Drilling, Water Treatment, Others).

An Introduction to Mining Chemicals Market in 2024

Mining chemicals are specialty chemicals used in various stages of the mining process to enhance mineral recovery, improve process efficiency, and minimize environmental impact. In 2024, the demand for mining chemicals s to be driven by the growing complexity of ore deposits, declining ore grades, and stricter environmental regulations. Mining chemicals encompass a wide range of products, including frothers, collectors, depressants, flocculants, dispersants, and grinding aids, each designed to perform specific functions in mineral processing operations. Frothers and collectors are used to facilitate the flotation of valuable minerals from ore slurries, while depressants are employed to selectively inhibit the flotation of unwanted minerals. Flocculants and dispersants are used to improve solid-liquid separation, dewatering, and tailings management, reducing water consumption and environmental footprint. Grinding aids are added to mill circuits to improve ore grindability, reduce energy consumption, and increase throughput. Further, mining chemicals are essential for mitigating environmental risks associated with acid mine drainage, metal leaching, and tailings impoundment, ensuring compliance with environmental regulations and community expectations. With advancements in chemical formulation, process optimization, and environmental stewardship, there is ongoing research into developing safer, more effective, and environmentally friendly mining chemical solutions. Additionally, the adoption of digital technologies such as process modeling, real-time monitoring, and automated dosing systems enhances the efficiency and sustainability of chemical usage in mining operations. As mining companies to invest in advanced technologies and sustainable practices, the demand for high-quality mining chemicals is expected to remain strong, driving further innovation and market growth.

Mining Chemicals Market Competitive Landscape

The market report analyses the leading companies in the industry including AECI Mining Chemicals, Akzo Nobel N.V., Arkema SA, Ashland Inc, BASF SE, Clariant AG, Dow Inc, Kemira Oyj, Kimleigh Chemicals SA, Nowata, Quaker Chemical Corp, Royal Dutch Shell plc, Sasol Ltd, Solenis LLc, Solvay SA, and others.

Mining Chemicals Market Dynamics

Market Trend: Shift towards Sustainable and Environmentally Friendly Solutions

A prominent market trend for mining chemicals is the industry's shift towards sustainable and environmentally friendly solutions. With increasing awareness of environmental impacts and regulatory pressures, there's a growing demand for mining chemicals that minimize environmental harm and promote sustainable mining practices. This trend is driving the development and adoption of eco-friendly alternatives to traditional chemicals, such as biodegradable reagents, water-based solutions, and green extraction technologies. Mining companies are seeking chemical suppliers that offer products with reduced toxicity, lower environmental footprint, and improved safety profiles, aligning with their sustainability objectives and corporate social responsibility initiatives.

Market Driver: Technological Advancements and Mining Process Optimization

A key market driver for mining chemicals is the continuous technological advancements and the drive for process optimization in mining operations. As mining companies aim to improve efficiency, productivity, and cost-effectiveness, there's a growing demand for specialty chemicals that enhance mineral recovery, ore beneficiation, and metal extraction processes. Advanced chemical formulations, innovative additives, and novel extraction techniques are being developed to address the challenges associated with complex ore bodies, declining ore grades, and increasing operational costs. The adoption of mining chemicals is driven by the need to maximize mineral resource utilization, optimize production yields, and maintain competitiveness in the global mining market.

Market Opportunity: Tailored Solutions for Specific Mining Challenges

A potential opportunity for mining chemical suppliers lies in offering tailored solutions for specific mining challenges and operational requirements. Opportunities exist for developing customized chemical formulations and services that address the unique needs of different mining operations, including gold, copper, iron ore, and rare earth mineral extraction. By collaborating closely with mining companies, chemical suppliers can gain insights into their specific processing challenges, metallurgical characteristics, and environmental considerations, enabling the development of targeted solutions to improve process efficiency, reduce chemical consumption, and mitigate environmental impacts. This approach allows chemical suppliers to differentiate themselves in the market, establish long-term partnerships with mining clients, and capture opportunities in niche segments and emerging mining regions.

Mining Chemicals Market Share Analysis: Copper segment generated the highest revenue in 2024

Among the options provided, the largest segment in the Mining Chemicals Market is the "Copper" ore segment. Copper is one of the most extensively mined metals globally due to its wide range of industrial applications, particularly in electrical wiring, plumbing, electronics, and construction. Mining copper ore involves complex extraction processes that require the use of various chemicals for ore processing, including flotation agents, solvent extractants, and leaching agents. Additionally, copper mining operations often involve large-scale processing facilities and high-volume production, further driving the demand for mining chemicals. The extensive use of chemicals in copper ore processing, coupled with the significant global demand for copper, makes the "Copper" ore segment the largest in the Mining Chemicals Market.

Mining Chemicals Market Share Analysis: Grinding Aids Type is poised to register the fastest CAGR over the forecast period

The Grinding Aids Type segment is the fastest-growing segment in the Mining Chemicals Market. Grinding aids are additives used during the grinding and milling processes in mining operations to improve the efficiency of ore liberation and reduce energy consumption. These chemicals facilitate the comminution of ore particles, resulting in finer particle size distribution and increased surface area, which enhances the efficiency of downstream processes such as flotation and leaching. With the increasing complexity of ore deposits and declining ore grades, mining companies are facing challenges in achieving optimal mineral recovery while minimizing operating costs. Grinding aids address these challenges by improving the grinding efficiency and reducing the energy consumption of grinding mills, leading to higher throughput and lower operating expenses. Moreover, advancements in grinding aid formulations, such as polymer-based additives and surfactant technologies, further enhance their effectiveness in achieving finer particle sizes and improving mineral liberation. Additionally, the growing focus on sustainable mining practices and environmental stewardship drives the adoption of grinding aids that reduce water and energy consumption, contributing to the segment's growth in the Mining Chemicals Market. With the continual demand for efficient and sustainable mineral processing solutions, the Grinding Aids Type segment presents significant growth opportunities for manufacturers and suppliers to innovate and meet the evolving needs of the mining industry.

Mining Chemicals Market Share Analysis: Mineral Processing segment generated the highest revenue in 2024

The Mineral Processing Application segment is the largest segment in the Mining Chemicals Market contributing to its prominence. Mineral processing is a fundamental stage in the mining value chain, where various chemicals are extensively utilized to extract, separate, and concentrate valuable minerals from ore deposits. These chemicals, including collectors, frothers, flocculants, and solvent extractants, play crucial roles in flotation, leaching, gravity separation, and other mineral processing techniques. Collectors and frothers aid in selectively attaching mineral particles to air bubbles during flotation, while flocculants enhance the settling and dewatering of mineral concentrates. Additionally, solvent extractants facilitate the extraction of metals from aqueous solutions, contributing to the recovery of valuable metals such as copper, gold, and uranium. The widespread use of mining chemicals in mineral processing operations to optimize mineral recovery, improve process efficiency, and meet quality specifications makes the Mineral Processing Application segment the largest in the Mining Chemicals Market. With the continuous demand for efficient and sustainable mineral processing solutions to address declining ore grades and increasing environmental regulations, the Mineral Processing Application segment presents significant growth opportunities for manufacturers and suppliers to innovate and provide value-added solutions to the mining industry.

Mining Chemicals Market

By Ore

Powder Gold

Iron

Copper

Phosphate

Others

By Type

Collectors

Coatings

Flocculants

Grinding Aids

Solvent Extractants

Dust Suppressants

Defoamers

Antiscalants

Biocides

Lubricants

Frothers

Others

By Application

Mineral Processing

Explosives and Drilling

Water Treatment

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Mining Chemicals Companies Profiled in the Study

AECI Mining Chemicals

Akzo Nobel N.V.

Arkema SA

Ashland Inc

BASF SE

Clariant AG

Dow Inc

Kemira Oyj

Kimleigh Chemicals SA

Nowata

Quaker Chemical Corp

Royal Dutch Shell plc

Sasol Ltd

Solenis LLc

Solvay SA

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Mining Chemicals Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Mining Chemicals Market Size Outlook, $ Million, 2021 to 2032

3.2 Mining Chemicals Market Outlook by Type, $ Million, 2021 to 2032

3.3 Mining Chemicals Market Outlook by Product, $ Million, 2021 to 2032

3.4 Mining Chemicals Market Outlook by Application, $ Million, 2021 to 2032

3.5 Mining Chemicals Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Mining Chemicals Industry

4.2 Key Market Trends in Mining Chemicals Industry

4.3 Potential Opportunities in Mining Chemicals Industry

4.4 Key Challenges in Mining Chemicals Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Mining Chemicals Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Mining Chemicals Market Outlook by Segments

7.1 Mining Chemicals Market Outlook by Segments, $ Million, 2021- 2032

By Ore

Powder Gold

Iron

Copper

Phosphate

Others

By Type

Collectors

Coatings

Flocculants

Grinding Aids

Solvent Extractants

Dust Suppressants

Defoamers

Antiscalants

Biocides

Lubricants

Frothers

Others

By Application

Mineral Processing

Explosives and Drilling

Water Treatment

Others

8 North America Mining Chemicals Market Analysis and Outlook To 2032

8.1 Introduction to North America Mining Chemicals Markets in 2024

8.2 North America Mining Chemicals Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Mining Chemicals Market size Outlook by Segments, 2021-2032

By Ore

Powder Gold

Iron

Copper

Phosphate

Others

By Type

Collectors

Coatings

Flocculants

Grinding Aids

Solvent Extractants

Dust Suppressants

Defoamers

Antiscalants

Biocides

Lubricants

Frothers

Others

By Application

Mineral Processing

Explosives and Drilling

Water Treatment

Others

9 Europe Mining Chemicals Market Analysis and Outlook To 2032

9.1 Introduction to Europe Mining Chemicals Markets in 2024

9.2 Europe Mining Chemicals Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Mining Chemicals Market Size Outlook by Segments, 2021-2032

By Ore

Powder Gold

Iron

Copper

Phosphate

Others

By Type

Collectors

Coatings

Flocculants

Grinding Aids

Solvent Extractants

Dust Suppressants

Defoamers

Antiscalants

Biocides

Lubricants

Frothers

Others

By Application

Mineral Processing

Explosives and Drilling

Water Treatment

Others

10 Asia Pacific Mining Chemicals Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Mining Chemicals Markets in 2024

10.2 Asia Pacific Mining Chemicals Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Mining Chemicals Market size Outlook by Segments, 2021-2032

By Ore

Powder Gold

Iron

Copper

Phosphate

Others

By Type

Collectors

Coatings

Flocculants

Grinding Aids

Solvent Extractants

Dust Suppressants

Defoamers

Antiscalants

Biocides

Lubricants

Frothers

Others

By Application

Mineral Processing

Explosives and Drilling

Water Treatment

Others

11 South America Mining Chemicals Market Analysis and Outlook To 2032

11.1 Introduction to South America Mining Chemicals Markets in 2024

11.2 South America Mining Chemicals Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Mining Chemicals Market size Outlook by Segments, 2021-2032

By Ore

Powder Gold

Iron

Copper

Phosphate

Others

By Type

Collectors

Coatings

Flocculants

Grinding Aids

Solvent Extractants

Dust Suppressants

Defoamers

Antiscalants

Biocides

Lubricants

Frothers

Others

By Application

Mineral Processing

Explosives and Drilling

Water Treatment

Others

12 Middle East and Africa Mining Chemicals Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Mining Chemicals Markets in 2024

12.2 Middle East and Africa Mining Chemicals Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Mining Chemicals Market size Outlook by Segments, 2021-2032

By Ore

Powder Gold

Iron

Copper

Phosphate

Others

By Type

Collectors

Coatings

Flocculants

Grinding Aids

Solvent Extractants

Dust Suppressants

Defoamers

Antiscalants

Biocides

Lubricants

Frothers

Others

By Application

Mineral Processing

Explosives and Drilling

Water Treatment

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

AECI Mining Chemicals

Akzo Nobel N.V.

Arkema SA

Ashland Inc

BASF SE

Clariant AG

Dow Inc

Kemira Oyj

Kimleigh Chemicals SA

Nowata

Quaker Chemical Corp

Royal Dutch Shell plc

Sasol Ltd

Solenis LLc

Solvay SA

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Ore

Powder Gold

Iron

Copper

Phosphate

Others

By Type

Collectors

Coatings

Flocculants

Grinding Aids

Solvent Extractants

Dust Suppressants

Defoamers

Antiscalants

Biocides

Lubricants

Frothers

Others

By Application

Mineral Processing

Explosives and Drilling

Water Treatment

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)