Mining Wastewater Treatment Equipment Market Overview: Growth Outlook to 2034

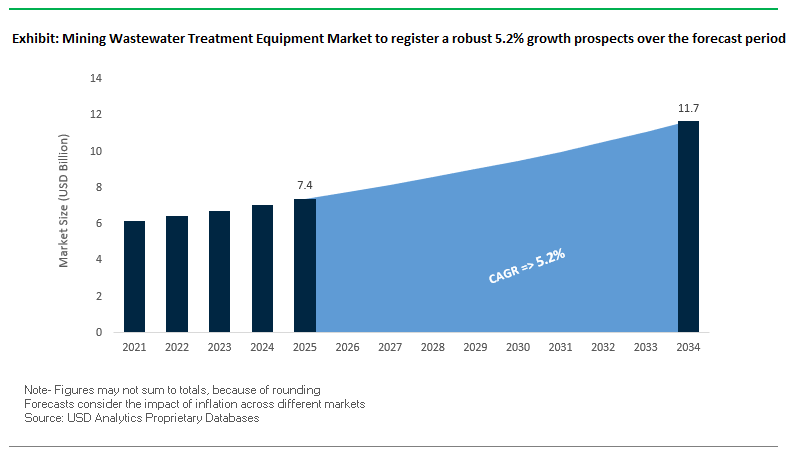

The global mining wastewater treatment equipment market is projected to grow from USD 7.4 billion in 2025 to USD 11.7 billion by 2034, registering a CAGR of 5.2%. This growth is fueled by rising environmental concerns, increasing water scarcity, and stricter government regulations that require mining companies to treat and reuse contaminated water before discharge. Mining wastewater often contains acid mine drainage (AMD), heavy metals, suspended solids, and chemical residues, making advanced treatment technologies indispensable for operational sustainability.

Industry Stakeholders are increasingly investing in advanced membrane technologies, zero liquid discharge (ZLD) systems, and microbial fuel cell innovations to reduce water-related risks and ensure compliance with environmental standards. The global push for responsible mining practices, ESG integration, and sustainable resource management will continue to boost demand for advanced wastewater treatment equipment.

Key Insights for Industry Stakeholders

- Water Stress in Mining Regions: Over 16% of global critical mineral mines are located in water-stressed regions, creating demand for high-efficiency treatment systems.

- Stagnant Recycling Rates: Top mining companies reported 58.4% average water recycling rates in 2023, unchanged since 2021, signaling untapped opportunities for technology adoption.

- Lithium Extraction Challenge: Extracting 1 ton of lithium from brine water requires up to 500,000 gallons of water, with operations in Chile’s Salar de Atacama consuming 65%+ of local water supply.

- Sustainability Leadership: 24% of mining companies have achieved 80%+ wastewater recycling rates, demonstrating the potential of advanced wastewater treatment solutions.

Mining Wastewater Treatment Equipment Market Analysis: Recent Developments and Strategic Shifts

The mining wastewater treatment equipment market is evolving rapidly due to technological advancements, M&A activity, and sustainability-driven regulations. Companies are investing in zero liquid discharge (ZLD), membrane filtration, advanced oxidation processes, and microbial fuel cells to enhance efficiency, reduce environmental footprints, and improve water recovery rates in mining operations.

In August 2025, DuPont Water Solutions was recognized at the BIG Sustainability Awards for innovations in minimal liquid discharge (MLD) systems, a critical technology for treating high-salinity mining wastewater. The same month, German innovators Niklas Ruf and Jana Spiller won the Stockholm Junior Water Prize for their flood warning system, showcasing potential applications in mine water management. Earlier, in July 2025, Veolia Water Technologies was awarded France’s largest treated wastewater reuse project in Argelès-sur-Mer, proving its expertise in scaling water reuse for industrial sectors like mining.

Strategic acquisitions are reshaping the industry. In May 2025, Veolia acquired full ownership of its Water Technologies and Solutions subsidiary, accelerating its integrated offerings for mining. Meanwhile, H2O America, also in July 2025, completed a USD 540 million acquisition of Quadvest, announcing infrastructure modernization plans worth USD 500 million over five years. On the innovation front, Kurita Water Industries (April 2025) demonstrated the use of microbial fuel cells to generate electricity from wastewater a breakthrough with strong potential for energy-positive mining treatment plants.

Global infrastructure projects are also influencing adoption. In October 2024, an MLD wastewater treatment plant treating 160,000 m³/day became operational in Foshan, China, for textile manufacturing an approach increasingly mirrored in mining. Additionally, Xylem’s July 2025 earnings report showed USD 2.3 billion in quarterly revenue, up 6%, highlighting growing demand for industrial water and mining wastewater solutions worldwide.

Key Market Trends Driving Growth of Mining Wastewater Treatment Equipment Industry

Policy and Financial Incentives Encouraging Water Stewardship

Government regulations and sustainability mandates are primary drivers in the mining wastewater sector. The U.S. Environmental Protection Agency (EPA) continues to enforce stringent effluent standards, as highlighted in Preliminary Plan #16 (2024), targeting improved compliance with NPDES permits. Simultaneously, corporate initiatives led by the International Council on Mining and Metals (ICMM) and Global Reporting Initiative (GRI) frameworks are pushing mining companies to disclose water usage and implement sustainable practices. PwC’s 2024 report, “Mine 2024: Preparing for Impact,” indicates that leading mining companies are increasingly embedding water management in their ESG strategies, driving adoption of advanced wastewater treatment equipment.

Advanced and Hybrid Treatment Technologies for Complex Effluents

Hybrid and advanced treatment solutions are transforming wastewater management in the mining industry. A 2024 MDPI study on a high-altitude copper mine demonstrated that combining ion exchange, nanofiltration, and cyclone electrodeposition achieved 95.1% copper recovery with 99.997% purity. Additionally, a 2025 RSC Publishing review emphasizes the integration of smart monitoring and automated systems with technologies such as advanced oxidation and membrane bioreactors. These innovations enhance treatment efficiency, enable precise chemical dosing, and reduce labor intensity, making them crucial for managing variable and high-strength mining wastewater streams.

Resource Recovery and Circular Economy Integration

The mining industry is increasingly viewing wastewater as a source of recoverable value. Case studies highlight investments exceeding $20 million in treatment facilities designed to recover metals like zinc and copper from acidic effluents, creating new revenue streams while reducing environmental impact. Companies like Adionics are pioneering lithium extraction from brine and mine-related waters, demonstrating how resource recovery technologies align with circular economy principles. This trend reinforces the market’s focus on sustainability and profitability through innovative wastewater treatment solutions.

Mining Wastewater Treatment Equipment Market Share Insights

By Equipment Type: Physical Treatment Leads, Advanced Treatment Growing Rapidly

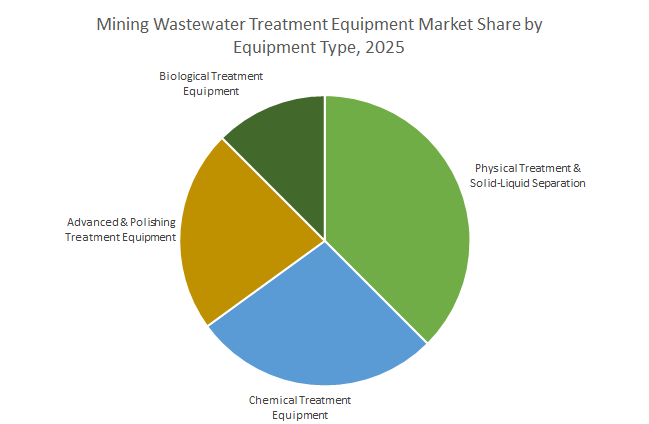

Physical Treatment & Solid-Liquid Separation (38%) dominates due to its critical role in handling massive slurry volumes and suspended solids. Chemical Treatment Equipment (26.9%) ensures pH adjustment, coagulation/flocculation, and heavy metal precipitation. Advanced & Polishing Treatment (24.6%) is the fastest-growing segment, driven by water reuse and ZLD adoption, incorporating membranes, ion exchange, and electrochemical processes. Biological Treatment is niche, primarily for passive treatment of acid mine drainage, but remains important for long-term sustainability. The market reflects a balance between foundational treatment, regulatory compliance, and innovative recovery-driven solutions.

By Water Source: Process Water and AMD Dominate

Process Water & Mill Effluent (32.8%) represents high-volume, operationally critical streams from mineral processing containing suspended solids, metals, and chemicals. Acid Mine Drainage (AMD) (26.9%) is highly hazardous and requires continuous chemical management, representing a substantial portion of CAPEX and OPEX. Tailings Pond Return Water (24.6%) highlights the shift toward circular water systems, while Pit Lake Water & Heap Leachate demand specialized treatment for process chemicals and long-term environmental management. These segments underline the dual focus on operational efficiency and sustainability in mining wastewater management.

By Phase of Mining: Active Treatment Dominates, ZLD Emerging

Active Water Treatment (67.4%) leads due to high effluent volumes during operational mining, requiring continuous high-capacity systems. Closure & Post-Closure Treatment (24.6%) is increasingly important for long-term management of AMD and pit lakes, often relying on passive or semi-passive biological systems. Zero Liquid Discharge (ZLD) represents a premium, high-investment segment driven by water scarcity and stringent regulatory requirements. ZLD adoption is gradually moving from niche to mainstream, signaling the future direction of sustainable mining water management.

Australia: Advanced Water Management and Virtual Curtain Technology for Sustainable Mining

Australia’s mining wastewater treatment equipment market is shaped by stringent environmental regulations and technological innovation. State environment protection policies, such as the SEPP Waters of Victoria, provide frameworks to maintain environmental quality and protect beneficial water uses. The Commonwealth Scientific and Industrial Research Organisation (CSIRO) developed the "Virtual Curtain" technology, which utilizes hydrotalcites to remove metal contaminants from wastewater, producing significantly less sludge than conventional lime-based methods. Government initiatives promote responsible mining practices, including wastewater reuse and recycling, reinforcing environmental stewardship. The market’s key applications focus on Australia’s extensive mining sector, particularly iron ore, coal, and precious metals, with emphasis on perpetual water treatment solutions for mine closure and long-term sustainability.

United States: PFAS Regulations and RO Systems Driving Equipment Innovation

In the United States, mining wastewater treatment is heavily influenced by government funding, environmental regulations, and corporate innovation. The EPA is addressing environmental challenges such as acid mine drainage, while ongoing efforts to regulate per- and polyfluoroalkyl substances (PFAS) are driving demand for advanced filtration and treatment technologies. Companies like Xylem Inc. provide a wide range of solutions, including reverse osmosis (RO) systems to remove heavy metals and salinity, and containerized ozone systems for cyanide destruction in gold processing. Key applications focus on sustainable mining practices, with technologies enabling reuse of tailings pond water for ore processing, drilling, and cooling, aligning with regulatory compliance and resource optimization goals.

Canada: Modular Solutions and Clean Technology Investments Support Market Growth

Canada’s mining wastewater treatment equipment market benefits from strong government support and technological innovation. Programs such as Natural Resources Canada’s Clean Growth Program invest in R&D for clean technology in mining. In 2020, a $4.5 million investment supported E2Metrix Inc. in developing its ECOTHOR system for contaminant removal in mining wastewater. Canadian companies, including H2O Innovation, offer technical solutions such as nanofiltration (NF), reverse osmosis (RO), and membrane bioreactors (MBRs) to treat biodegradable and chemical-laden wastewater. The market is driven by the need for rapid deployment, modular systems, and solutions suited for remote mining sites, addressing pollutants such as heavy metals and ammonia.

China: Green Mining Regulations and Integrated Wastewater Technologies Expand Market

China’s mining wastewater treatment market is strongly influenced by regulatory oversight and government investments. The Ministry of Ecology and Environment (MEE) enforces strict mining wastewater discharge regulations, with a national focus on green mining and controlling groundwater contamination. The government plans to invest $50 billion in wastewater treatment by 2025, including projects in coal and metal mining. Technological advancements encompass coagulation, precipitation, microbial treatment, adsorption, and integrated membrane systems. The market is driven by the complexity of mining effluent, which often contains a mixture of fine debris, chemicals, and water, requiring advanced treatment solutions to ensure compliance and environmental protection.

India: ZLD Policies and Government Missions Foster Advanced Mining Wastewater Solutions

India’s mining wastewater treatment equipment market is shaped by regulatory mandates, technological support, and infrastructure programs. The Central Pollution Control Board (CPCB) and State Pollution Control Boards (SPCBs) require Zero Liquid Discharge (ZLD) for mining operations in water-scarce regions. While recent DST-supported technologies focus on textile wastewater using biosurfactants and membrane systems, these methods are adaptable for mining effluent treatment. Government initiatives such as the "Jal Jeevan Mission" and "Namami Gange Mission" drive water and wastewater treatment adoption for industrial sectors, including mining, supporting sustainable operations and compliance with environmental standards.

Germany: Advanced Modular Plants and Digital Twins for Mining Wastewater Optimization

Germany’s mining wastewater treatment market is influenced by EU directives, technological innovation, and corporate expertise. The revised Urban Wastewater Treatment Directive (January 2025) requires a "4th purification stage" to remove micropollutants, driving the adoption of advanced decentralized systems. German companies like EnviroChemie recently commissioned a modular treatment plant for the Ellatzite-Med mining complex in Bulgaria, employing mechanical and chemical treatment with multiple precipitation reagents for heavy metal and solids removal. Technological trends in Germany include advanced monitoring systems, AI-driven digital twins, and climate-adaptive water management solutions, positioning German expertise at the forefront of sustainable mining wastewater treatment.

Competitive Landscape: Leading Players in Mining Wastewater Treatment Equipment

The competitive landscape is defined by global water technology leaders, integrated solution providers, and innovative specialists that focus on mining wastewater treatment challenges. Companies compete on advanced technologies, regional expansion, ESG alignment, and ability to deliver ZLD and high-efficiency recycling systems.

DuPont Water Solutions – Membrane Innovation for Mining Wastewater

DuPont is a pioneer in high-performance membranes such as FilmTec™ RO and NF systems, which play a critical role in acid mine drainage treatment and ZLD applications. In 2025, it won an R&D 100 Award for its FilmTec™ Fortilife™ XC160 Membrane, designed for high-salinity mining wastewater. With ultrafiltration (IntegraTec™) and ion exchange resins, DuPont offers complete solutions for mining companies seeking sustainability, water reuse, and lower OPEX.

Veolia Water Technologies – Full-Spectrum Mining Wastewater Solutions

Veolia stands out for its end-to-end solutions, ranging from biological treatment to thermal evaporators and crystallizers for mining ZLD systems. In May 2025, Veolia strengthened its portfolio by acquiring full ownership of its Water Technologies and Solutions subsidiary, enhancing efficiency and integration. Its GreenUp plan emphasizes decarbonization, depollution, and water reuse, making it a trusted partner for global mining companies.

SUEZ Water Technologies & Solutions – Digital and Customized Mining Wastewater Treatment

SUEZ provides customized wastewater treatment equipment tailored to harsh industrial and mining environments. Recent contracts in Asia (2024–2025) highlight its role in achieving 100% wastewater recycling and ZLD. SUEZ integrates predictive analytics and digital monitoring platforms to optimize chemical usage and reduce fouling, which lowers operating costs for mining operators.

Xylem Inc. – End-to-End Mining Water Solutions with IoT Integration

Xylem delivers comprehensive water cycle solutions, including mine dewatering systems, advanced oxidation, and MBRs. Its 2023 acquisition of Evoqua created a powerful combined platform for mining wastewater treatment. Xylem’s focus on IoT-based monitoring and predictive maintenance ensures regulatory compliance, operational safety, and efficient recycling in mining regions facing severe water stress.

Evoqua Water Technologies LLC – North American Leader in Mission-Critical Treatment

Evoqua, now part of Xylem (2023), has a strong North American footprint, serving 38,000+ customers with 200,000 installations worldwide. Its offerings include filtration, industrial process water treatment, and emerging contaminant removal (PFAS). With its Sustainability and Innovation Hub in Pittsburgh, Evoqua is advancing research on climate resilience and contaminant management for industries such as mining.

Kurita Water Industries Ltd. – Chemical and Biological Innovation for Mining Effluent

Kurita is a specialist in chemical-based water treatment and innovative microbial technologies. In June 2024, it expanded operations in India through Kurita AquaChemie India Private Limited (KAIL) to tap into the region’s mining sector. Its solutions include odor/nutrient control, chemical membrane cleaning, and microbial fuel cells for energy generation. Kurita’s approach focuses on minimizing discharges and maximizing water reuse, aligning with global ESG targets.

Mining Wastewater Treatment Equipment Market Report Scope

Mining Wastewater Treatment Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.4 Billion

|

|

Market Size (2034)

|

$11.7 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Type (Physical Treatment & Solid-Liquid Separation Equipment, Chemical Treatment Equipment, Biological Treatment Equipment, Advanced & Polishing Treatment Equipment), By Water Source (Acid Mine Drainage, Process Water & Mill Effluent, Tailings Pond Return Water, Pit Lake Water, Heap Leachate), By Phase of Mining (Active Water Treatment, Closure & Post-Closure Water Treatment, Zero Liquid Discharge), By Mining Commodity (Coal Mining, Gold Mining, Base & Precious Metals, Uranium Mining), By Contaminant Treated (Heavy Metals, Acid Mine Drainage, Suspended Solids & Tailings, Cyanide & Reagents, Oil & Grease, Salinity & Brine)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., Evoqua Water Technologies, DuPont de Nemours, Inc., Alfa Laval, Toray Industries, Inc., Aquatech International, Kubota Corporation, The Dow Chemical Company, V.A. TECH WABAG Ltd., Mitsubishi Chemical Corporation, Kurita Water Industries Ltd., H2O GmbH, Thermax Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Mining Wastewater Treatment Equipment Market Segmentation

By Type

- Physical Treatment & Solid-Liquid Separation Equipment

- Chemical Treatment Equipment

- Biological Treatment Equipment

- Advanced & Polishing Treatment Equipment

By Water Source

- Acid Mine Drainage

- Process Water & Mill Effluent

- Tailings Pond Return Water

- Pit Lake Water

- Heap Leachate

By Phase of Mining

- Active Water Treatment

- Closure & Post-Closure Water Treatment

- Zero Liquid Discharge

By Mining Commodity

- Coal Mining

- Gold Mining

- Base & Precious Metals

- Uranium Mining

By Contaminant Treated

- Heavy Metals

- Acid Mine Drainage

- Suspended Solids & Tailings

- Cyanide & Reagents

- Oil & Grease

- Salinity & Brine

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Mining Wastewater Treatment Equipment Industry include-

- Veolia

- SUEZ

- Xylem Inc.

- Evoqua Water Technologies

- DuPont de Nemours, Inc.

- Alfa Laval

- Toray Industries, Inc.

- Aquatech International

- Kubota Corporation

- The Dow Chemical Company

- V.A. TECH WABAG Ltd.

- Mitsubishi Chemical Corporation

- Kurita Water Industries Ltd.

- H2O GmbH

- Thermax Limited

*- List not Exhaustive

Research Coverage

This report investigates the Mining Wastewater Treatment Equipment Market and delivers analysis reviews that benchmark removal performance, lifecycle costs, and retrofit pathways across mine phases and water sources; it highlights technology breakthroughs in membranes, ion exchange, AOPs, electrochemical polishing, and ZLD/MLD hybrids while mapping adoption under tightening permits and ESG disclosure. Developed by USDAnalytics, the study quantifies capacity additions, evaluates vendor strengths, and distills procurement playbooks for tailings, AMD, brines, and mill effluents translating engineering metrics into bankable business cases for reuse and resource recovery. With scenario-tested forecasting and competitive diagnostics, this report is an essential resource for mine owners, EPC/M, OEMs, investors, and EHS leaders planning resilient, compliance-ready water strategies through 2034. Scope Includes-

- Segmentation

- By Type: Physical Treatment & Solid-Liquid Separation Equipment; Chemical Treatment Equipment; Biological Treatment Equipment; Advanced & Polishing Treatment Equipment

- By Water Source: Acid Mine Drainage; Process Water & Mill Effluent; Tailings Pond Return Water; Pit Lake Water; Heap Leachate

- By Phase of Mining: Active Water Treatment; Closure & Post-Closure Water Treatment; Zero Liquid Discharge

- By Mining Commodity: Coal Mining; Gold Mining; Base & Precious Metals; Uranium Mining

- By Contaminant Treated: Heavy Metals; Acid Mine Drainage; Suspended Solids & Tailings; Cyanide & Reagents; Oil & Grease; Salinity & Brine

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data 2021–2024; Forecasts 2025–2034.

- Companies (15+ profiles/analysis): Veolia; SUEZ; Xylem Inc.; Evoqua Water Technologies; DuPont de Nemours, Inc.; Alfa Laval; Toray Industries, Inc.; Aquatech International; Kubota Corporation; The Dow Chemical Company; V.A. TECH WABAG Ltd.; Mitsubishi Chemical Corporation; Kurita Water Industries Ltd.; H2O GmbH; Thermax Limited.

Methodology

USDAnalytics applies a triangulated approach combining: (1) bottom-up equipment tracking by mine site, water source, and train configuration (clarification, DAF, filters, IX, UF/NF/RO, AOP, electrocoagulation, evaporators/crystallizers); (2) top-down calibration to commodity output, water balances, and permit limits (pH, metals, sulfate, TDS, cyanide, turbidity); and (3) 90+ expert interviews across miners, OEMs/EPCs, and regulators. Performance datasets normalize kWh·m⁻³, reagent dose, recovery %, brine ratio, metal recovery yield, sludge index, and O&M staffing. Scenario models stress-test pricing, energy trajectories, ZLD mandates, and water-stress indices to 2034, producing defensible market sizes, share estimates, and cost curves for greenfield, brownfield, and closure portfolios.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Mining Wastewater Treatment Equipment Market

1. Executive Summary

1.1. Market Highlights and Key Projections

1.2. Key Insights: Water Stress, Untapped Recycling Opportunities, and Sustainability

1.3. Global Market Snapshot

1.3.1. Current Market Valuation (2025): $7.4 Billion

1.3.2. Projected Market Valuation (2034): $11.7 Billion

1.3.3. Compound Annual Growth Rate (CAGR): 5.2%

2. Market Outlook (2025–2034)

2.1. Introduction: Growth, Drivers, and Key Challenges

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Key Trends Driving Market Growth

2.3.1. Policy and Financial Incentives Encouraging Water Stewardship

2.3.2. Advanced and Hybrid Treatment Technologies for Complex Effluents

2.3.3. Resource Recovery and Circular Economy Integration

3. Innovations and Strategic Developments Redefining the Market

3.1. Market Analysis: Recent Developments and Strategic Shifts

3.1.1. DuPont Water Solutions Recognized for MLD Innovations (August 2025)

3.1.2. Veolia Strengthens Portfolio with Strategic Acquisition and New Contracts (2025)

3.1.3. H2O America's Expansions and Infrastructure Modernization (July-August 2025)

3.1.4. Kurita's Breakthrough in Microbial Fuel Cells (April 2025)

3.1.5. Xylem's Strong Performance Reflecting Growing Industrial Demand (July 2025)

3.1.6. Adoption of New AI and IoT-driven Technologies for Optimization

4. Competitive Landscape: Leading Players

4.1. Market Overview: Global Leaders and Innovative Specialists

4.2. Strategic Profiles of Key Companies

4.2.1. DuPont Water Solutions: Membrane Innovation for Mining Wastewater

4.2.2. Veolia Water Technologies: Full-Spectrum Mining Wastewater Solutions

4.2.3. SUEZ Water Technologies & Solutions: Digital and Customized Treatment

4.2.4. Xylem Inc.: End-to-End Mining Water Solutions with IoT Integration

4.2.5. Evoqua Water Technologies LLC: North American Leader in Mission-Critical Treatment

4.2.6. Kurita Water Industries Ltd.: Chemical and Biological Innovation

5. Market Segmentation Insights

5.1. By Equipment Type

5.1.1. Physical Treatment & Solid-Liquid Separation (38% Market Share)

5.1.2. Chemical Treatment Equipment (26.9% Market Share)

5.1.3. Advanced & Polishing Treatment (24.6% Market Share)

5.1.4. Biological Treatment Equipment

5.2. By Water Source

5.2.1. Process Water & Mill Effluent (32.8% Market Share)

5.2.2. Acid Mine Drainage (AMD) (26.9% Market Share)

5.2.3. Tailings Pond Return Water (24.6% Market Share)

5.2.4. Pit Lake Water & Heap Leachate

5.3. By Phase of Mining

5.3.1. Active Water Treatment (67.4% Market Share)

5.3.2. Closure & Post-Closure Water Treatment (24.6% Market Share)

5.3.3. Zero Liquid Discharge (ZLD)

5.4. By Mining Commodity

5.4.1. Coal Mining

5.4.2. Gold Mining

5.4.3. Base & Precious Metals

5.4.4. Uranium Mining

5.5. By Contaminant Treated

5.5.1. Heavy Metals

5.5.2. Acid Mine Drainage

5.5.3. Suspended Solids & Tailings

5.5.4. Cyanide & Reagents

5.5.5. Oil & Grease

5.5.6. Salinity & Brine

6. Country Analysis and Outlook

6.1. Australia: Advanced Water Management and Virtual Curtain Technology

6.2. United States: PFAS Regulations and RO Systems

6.3. Canada: Modular Solutions and Clean Technology Investments

6.4. China: Green Mining Regulations and Integrated Wastewater Technologies

6.5. India: ZLD Policies and Government Missions

6.6. Germany: Advanced Modular Plants and Digital Twins

6.7. Other Countries Analyzed

6.7.1. North America (Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (Japan, South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Market Size Outlook by Region (2025-2034)

7.1. North America Mining Wastewater Treatment Equipment Market Size Outlook to 2034

7.1.1. By Equipment Type

7.1.2. By Water Source

7.1.3. By Phase of Mining

7.2. Europe Mining Wastewater Treatment Equipment Market Size Outlook to 2034

7.2.1. By Equipment Type

7.2.2. By Water Source

7.2.3. By Phase of Mining

7.3. Asia Pacific Mining Wastewater Treatment Equipment Market Size Outlook to 2034

7.3.1. By Equipment Type

7.3.2. By Water Source

7.3.3. By Phase of Mining

7.4. South America Mining Wastewater Treatment Equipment Market Size Outlook to 2034

7.4.1. By Equipment Type

7.4.2. By Water Source

7.4.3. By Phase of Mining

7.5. Middle East and Africa Mining Wastewater Treatment Equipment Market Size Outlook to 2034

7.5.1. By Equipment Type

7.5.2. By Water Source

7.5.3. By Phase of Mining

8. Company Profiles: Leading Players in Mining Wastewater Treatment Equipment Market

8.1. Veolia

8.2. SUEZ

8.3. Xylem Inc.

8.4. Evoqua Water Technologies

8.5. DuPont de Nemours, Inc.

8.6. Alfa Laval

8.7. Toray Industries, Inc.

8.8. Aquatech International

8.9. Kubota Corporation

8.10. The Dow Chemical Company

8.11. V.A. TECH WABAG Ltd.

8.12. Mitsubishi Chemical Corporation

8.13. Kurita Water Industries Ltd.

8.14. H2O GmbH

8.15. Thermax Limited

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures