Market Overview: Nafion Demand Accelerates As Ultra-Thin PFSA Membranes Power PEM Fuel Cells, Electrolyzers & Chlor-Alkali Systems

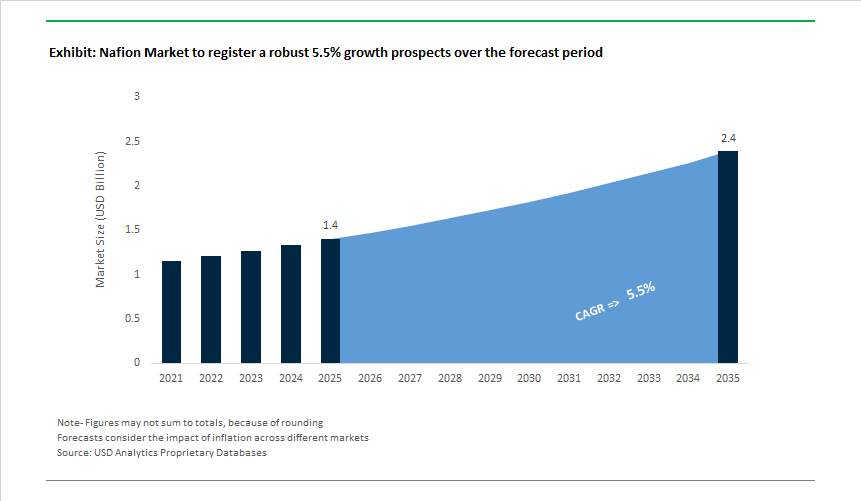

The Nafion Market, valued at USD 1.4 billion in 2025, is projected to grow at a 5.5% CAGR to reach USD 2.4 billion by 2035, driven by rising global adoption of high-performance PFSA membranes across fuel cells, water electrolyzers, and industrial electrochemical processes.

The Nafion Market is entering a new growth phase as global expansion of PEM fuel cells, PEM water electrolyzers, and Chlor-Alkali systems places unprecedented emphasis on proton conductivity, ultra-thin PFSA architectures, and long-term chemical stability. Nafion’s PFSA ionomer, built on a chemically robust perfluorinated backbone with side-chain sulfonic acid groups, remains unmatched in durability and proton transport, enabling conductivity near 100 mS/cm at 80°C/100% RH and maintaining structural integrity under aggressive redox, acidic, and humidified environments. As manufacturers race to increase stack efficiency and reduce system cost, the industry is shifting toward 8-25 μm membranes, optimized dispersion-cast layers for high-power-density MEAs, and reinforced PFSA constructions that suppress membrane creep, thinning failure, and peroxide-driven degradation.

Major PFSA producers-including Chemours (Nafion), AGC (FORBLUE membranes), and Asahi Kasei-are now scaling digital membrane casting, dispersion uniformity control, and ultra-low-defect film production to meet the reliability expectations of automotive fuel cells (>60,000 hours), stationary systems (>80,000 hours), and industrial electrolyzers (>90% system efficiency targets). Clean hydrogen mandates in the U.S., EU, Japan, and Korea are intensifying the need for regionalized PFSA supply chains, MEA-grade ionomer availability, and membrane platforms engineered for elevated pressure differentials in next-generation water electrolyzers. By 2035, the Nafion market landscape will be defined by reinforced PFSA composites (ePTFE/Nafion laminates), catalytic durability stabilizers, and specialized grades for redox-flow batteries (RFBs) and zero-gap electrochemical CO₂ conversion-applications that rely on Nafion’s selectivity, proton mobility, and unparalleled chemical resistance

Market Analysis: Nafion Capacity Expansions, Hydrogen Programs & Electrochemical Innovation

The Nafion market is witnessing strong momentum driven by capacity investments, strategic supply chain expansions, and rising electrochemical demand across hydrogen, transportation, and Chlor-Alkali applications. In January 2025, The Chemours Company confirmed it is on track to complete its USD 200 million Nafion capacity expansion at the Villers-Saint-Paul site, directly addressing the growing need for PFSA membranes in PEM electrolyzers used for clean hydrogen production. The increasing focus on domestic and regional supply security was further reflected in August 2025, where Chemours signed a strategic agreement with SRF Limited to strengthen its distribution and technical support footprint in India - a major future hydrogen economy and one of the fastest-growing electrolyzer markets.

Strong demand continued through November 2025, when Chemours' earnings report highlighted robust performance across energy and transportation sectors, driven by sustained uptake of Nafion in PEM stacks and advanced membranes for heavy-duty vehicles. In parallel, competition in the PFSA category intensified: March 2025 saw W. L. Gore begin a long-term collaboration with a global automotive OEM to optimize GORE-SELECT® (a PFSA-ePTFE reinforced Nafion derivative) for heavy-duty fuel cell stacks, aiming for efficiency gains and cost parity with diesel engines. Additional momentum in hydrogen electrolysis came from September 2025, when U.S. DOE funding programs elevated high-performance fluorinated membranes as a critical component of the national clean hydrogen strategy.

Innovation in adjacent electrochemical technologies also shaped market direction. As early as December 2024, researchers at Imperial College London introduced a next-generation ion-exchange membrane for Redox Flow Batteries (RFBs), signaling potential competition to Nafion in grid-scale storage. On the other hand, global adoption trends showed diversification: in July 2024, JAXA validated AGC’s FORBLUE S-Series membrane for spacecraft oxygen generation - positioning fluorinated membranes as reliable under extreme conditions. The combination of capacity expansions, new partnerships, and ongoing membrane innovation underscores a dynamic competitive environment for PFSA producers through 2035.

Nafion Market: Trends and Opportunities

Strategic Capacity Expansion Positions Nafion™ as a Hydrogen-Critical Material

The Nafion™ market is entering a structurally different phase as governments and utilities move from pilot electrolyzers to gigawatt-scale hydrogen hubs, exposing membrane supply as a potential bottleneck. In response, leading fluoropolymer producers are pivoting from batch processing to continuous-roll, high-throughput membrane manufacturing, a shift that prioritizes thickness control, mechanical uniformity, and yield at scale. Between 2024 and 2025, Chemours completed a $200 million expansion at its Villers-Saint-Paul site in France, purpose-built to increase Nafion™ ionomer and membrane output for PEM electrolysis. The strategic logic is surface-area intensity: higher-current stacks demand tighter tolerances and far more membrane area per MW, making continuous production essential.

Supply-chain security is becoming equally decisive. In the United States, Chemours is leveraging incentives under the Inflation Reduction Act to reinforce domestic fluoropolymer capacity, positioning Advanced Performance Materials as an enabling layer for both hydrogen and semiconductors. Manufacturing innovation is underpinning cost-down trajectories: by 2025, slot-die coating and high-speed extrusion reduced sheet thickness variability to ±2 microns, improving current distribution and durability in high-pressure stacks. As electrolyzer OEMs standardize designs for utility-scale deployment, procurement criteria are shifting toward lifetime uniformity and mechanical robustness, favoring suppliers with proven continuous manufacturing and reinforcement know-how.

Composite and Nanostructured PFSA Membranes Extend Lifetime Under Dynamic Loads

As renewable-powered electrolysis introduces frequent start–stop cycles and load variability, standard PFSA membranes face fatigue, crack propagation, and gas crossover risks. R&D focus has therefore moved to composite architectures that decouple proton transport from mechanical stress. A notable advance emerged from collaborative research by Incheon National University and Harvard University, which introduced an interpenetrating network combining Nafion with perfluoropolyether (PFPE). Updated 2024–2025 validation showed a 175% increase in fatigue threshold, extending operational life from 242 to 410 hours in heavy-duty duty cycles—directly addressing expansion–contraction damage.

Nanocomposite strategies are closing performance gaps in harsh environments. 2025 studies demonstrated that embedding sulfonated siliceous layered materials into Nafion matrices doubled power density at 120°C and 20% relative humidity, enabling operation in hot, dry conditions that typically dehydrate PFSA membranes. Chemical stability is also improving: titania-based radical scavengers integrated into new-generation Nafion™ reduced voltage decay rates by ~3.5× in open-circuit tests, lowering fluoride emission—an accepted proxy for polymer backbone degradation. Collectively, these advances reposition Nafion from a static material choice to a tunable platform optimized for variable renewable energy inputs.

Enabling Gigawatt-Scale Electrolyzer Rollouts Through Policy-Led Demand

National hydrogen mandates are translating into guaranteed, multi-year procurement for PEM-compatible membranes, elevating Nafion from specialty polymer to infrastructure material. In Europe, the Clean Hydrogen Partnership launched a 2025 call totaling €184.5 million, including €80 million from REPowerEU to double Hydrogen Valleys—each representing clustered demand for large electrolyzer fleets. This policy design favors standardized PEM stacks, reinforcing membrane volume requirements with predictable offtake.

In the U.S., deployment is accelerating through regional hubs. The U.S. Department of Energy advanced Phase 1 awards for seven hydrogen hubs (including ARCH2, MACH2, PNWH2), backed by $7 billion in federal funding. These hubs are planned to collectively deliver millions of tons of clean hydrogen annually by the end of the decade, implying sustained, high-volume Nafion™ procurement. Economics are aligning as well: Section 45V tax credits of up to $3/kg are compressing green hydrogen costs, making PEM electrolysis competitive with SMR and shifting focus from capex pilots to bankable scale projects—a dynamic that structurally benefits membrane suppliers with proven reliability.

Nafion™ Expands Its Role in Long-Duration Flow Battery Systems

Beyond hydrogen, Nafion remains a reference membrane for vanadium redox flow batteries (VRFBs), where long cycle life and chemical stability outweigh first-cost considerations. As grids seek 6-hour-plus long-duration energy storage, VRFB deployments are rising in applications where lithium-ion economics deteriorate. While Nafion’s ionic domains (3–5 nm) can permit vanadium crossover, 2025 reviews highlighted supramolecular modifications—such as fluoroalkyl-grafted nanoclusters—that delivered ~100% improvements in proton/vanadium selectivity without sacrificing conductivity.

Utility-scale validation is reinforcing confidence. Case studies from Sumitomo Electric (2024–2025) document VRFB installations in Japan and the U.S. Pacific Northwest achieving 20,000+ cycle lifetimes, relying on Nafion’s oxidative stability to sustain performance over decades. A parallel opportunity is emerging in lifecycle optimization: research programs are developing methods to recover and recondition Nafion membranes from decommissioned stacks, targeting 15–20% reductions in total system lifecycle cost. As LDES becomes a grid necessity rather than an option, Nafion’s dual role in hydrogen and flow batteries positions it as a cross-sector cornerstone material in the energy transition.

Nafion Market Share Analysis

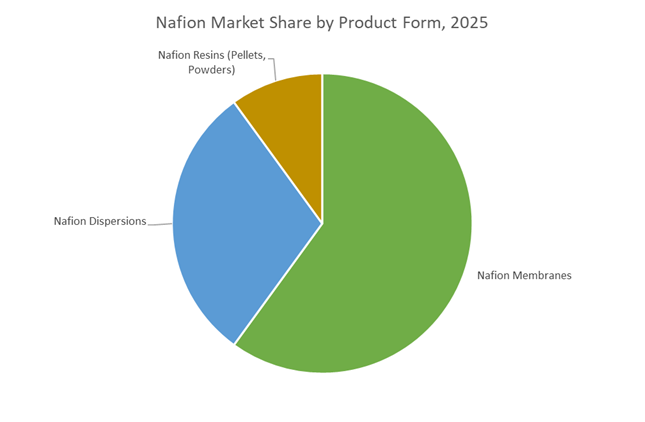

Market Share by Product Form: Nafion Membranes Anchor the Market’s Functional Core

Nafion membranes account for approximately 60% of total demand in the global Nafion Market, reflecting their role as the essential functional architecture in proton exchange and electrochemical separation systems. This dominance is driven by Nafion membranes’ ability to combine high proton conductivity, long operational lifespan, and chemical stability in environments where alternative polymer electrolytes fail. With engineered lifetimes exceeding 60,000 operating hours, Nafion membranes provide the predictability and durability required by fleet operators and utilities deploying fuel cells and electrolyzers as long-term infrastructure assets. Market share is further reinforced by Nafion’s industry-leading proton conductivity, which minimizes electrical losses during operation and directly improves system efficiency in energy conversion and storage applications. Thickness versatility also strengthens adoption, as different membrane grades allow buyers to optimize performance trade-offs between power density and structural robustness depending on end-use requirements. Advanced membrane variants capable of operating at elevated temperatures enable simplified thermal management, reducing system complexity, weight, and cost—an increasingly important advantage as hydrogen technologies scale toward commercial deployment. Collectively, these performance and lifecycle benefits position Nafion membranes as the default material platform for high-value electrochemical systems, securing their leading share within the market.

Market Share by Application: Energy and Power Drive Nafion Demand Through Hydrogen and Storage Economics

The energy and power segment represents approximately 45% of total Nafion consumption, making it the largest application area and the primary growth engine for the market. This leadership is anchored in the rapid expansion of green hydrogen production, where Nafion membranes serve as the critical separator in proton exchange membrane (PEM) electrolyzers and fuel cells. By enabling high current density operation without corrosive liquid electrolytes, Nafion-based systems achieve higher hydrogen output per unit of installed capacity, improving capital efficiency for producers. In transportation, Nafion-enabled fuel cells deliver substantially higher energy conversion efficiency than internal combustion engines, offering a compelling economic case for logistics and heavy-duty fleets seeking to reduce fuel costs and emissions simultaneously. The segment’s market share is further reinforced by the role of Nafion membranes in long-duration energy storage, particularly in redox flow batteries that stabilize electricity grids with high renewable penetration. As governments and utilities accelerate investments in hydrogen infrastructure and grid-scale storage to meet net-zero targets, the energy and power sector remains the structural anchor of global Nafion demand, sustaining its dominant share in the market.

Competitive Landscape: Global PFSA Leaders Shaping the Future Of PEM Technology

The competitive landscape of the Nafion Market is shaped by global PFSA membrane suppliers, reinforced composite membrane innovators, and advanced materials firms expanding into hydrogen and electrochemical markets. Producers differentiate through proton conductivity performance, thin-film PFSA engineering, ePTFE reinforcement, and long-term durability under high-power PEM operating conditions. As clean hydrogen, FCEVs, and electrolysis capacity increase globally, partnerships, regional supply expansion, and advanced membrane designs are emerging as critical competitive levers.

The Chemours Company - Exclusive Nafion Producer Leading Global Pfsa Supply

Chemours remains the exclusive global producer of Nafion™ PFSA materials, setting the benchmark for PEM fuel cells, water electrolyzers, and Chlor-Alkali electrolysis systems. With a USD 200 million capacity expansion underway in France (announced Jan 2025), the company is strategically positioned to supply the accelerating hydrogen market. Nafion is integral to high-purity NaOH and Cl₂ production due to its exceptionally high ion selectivity, and it continues to dominate proton exchange applications requiring high electrochemical stability. Chemours’ strategic focus centers on anchoring Nafion across the full hydrogen value chain - from FCEV stacks to PEM electrolyzers and redox-flow storage technologies.

W. L. Gore & Associates - Reinforced Gore-Select® Membranes For High-Durability Pem Stacks

W. L. Gore develops GORE-SELECT® membranes, combining PFSA chemistry with ePTFE reinforcement to deliver exceptional mechanical stability and ultra-thin (<12 μm) architectures. This allows manufacturers to achieve higher power density, reduced stack costs, and longer operating lifetimes. With membranes deployed in over 80,000 FCEVs across 100+ models, Gore is a significant player in commercial fuel-cell mobility. Its March 2025 collaboration with a major automotive OEM demonstrates strategic commitment to advancing PEM stack durability for heavy-duty vehicles - a critical step in replacing diesel-based transport.

Agc Inc. (Asahi Glass) - Forblue S-Series Membranes Targeting Pem Electrolysis Leadership

AGC manufactures the FORBLUE™ S-Series fluorinated ion-exchange membranes engineered for world-class voltage performance and gas-barrier characteristics, making them highly competitive in PEM water electrolysis. AGC’s membrane technology was validated by JAXA in July 2024, confirming durability and efficiency under extreme aerospace conditions. With plans to commission a dedicated production facility in Kitakyushu by 2026, AGC is scaling its presence in the green hydrogen market. Proprietary fluorochemical engineering enables minimized electrical resistance and high structural uniformity, strengthening its position as a direct competitor to Nafion in electrolyzer applications.

The United States represents the most policy-driven growth engine for the Nafion market, with demand structurally anchored to clean hydrogen economics and supply chain security. The restoration of the Section 45V Hydrogen Production Tax Credit in 2025 has materially altered project bankability for PEM electrolyzers, directly increasing offtake visibility for high-durability Nafion™ membranes used in large-scale hydrogen hubs. This fiscal signal has accelerated domestic membrane electrode assembly (MEA) deployment across industrial clusters pursuing the DOE’s Hydrogen Shot target. Parallel to energy policy, the strategic integration of Nafion™ into rare earth and critical mineral recovery reflects a broader federal objective to de-risk downstream processing. Through alliances involving The Chemours Company, Nafion is increasingly positioned as a dual-use strategic material-supporting both clean energy and mineral independence. Federal R&D funding further reinforces this trajectory by prioritizing MEA cost reduction, durability under high current density, and lifetime extension under cyclic operation.

France as Europe’s Manufacturing Anchor for PFSA Membranes

France has emerged as the central manufacturing hub for PFSA-based ionomers in Europe, translating hydrogen policy ambition into physical production capacity. Large-scale capital deployment into Nafion™ membrane manufacturing has strengthened Europe’s ability to localize electrolyzer supply chains amid rising gigawatt-scale installations. The expansion of fluoropolymer capacity supports not only water electrolysis but also adjacent applications such as redox flow batteries and hydrogen-compatible industrial processes. France’s advantage lies in its tight coupling of membrane production with downstream hydrogen and green steel initiatives, particularly in coastal industrial zones. These projects require membranes capable of maintaining ionic conductivity and mechanical stability under high-pressure, high-throughput electrolysis, reinforcing sustained demand for premium-grade Nafion dispersions and reinforced films.

Germany’s Dual-Track Strategy: PEM Continuity and AEM Disruption

Germany’s Nafion market dynamics are defined by a deliberate dual-track membrane strategy. While PFSA membranes remain foundational for near-term PEM electrolyzer deployments aligned with national hydrogen targets, Germany is simultaneously investing in anion exchange membrane alternatives to reduce long-term system costs. This competitive landscape does not diminish Nafion’s relevance; rather, it elevates performance benchmarks around durability, reinforcement, and pressure tolerance. The build-out of Germany’s hydrogen core grid provides structural demand certainty for high-modulus ion exchange films across industrial electrolysis, mobility, and power balancing applications. German policy emphasis on system efficiency and infrastructure coupling ensures that Nafion-type membranes continue to serve as reference materials for high-performance electrochemical systems, even as cost-driven alternatives mature.

China’s Commercial Fuel Cell Scale and Localization Imperative

China represents the largest real-world deployment environment for Nafion-type membranes, driven by commercial fuel cell electric vehicle (FCEV) fleets rather than pilot-scale projects. National plans positioning hydrogen as an emerging pillar industry have translated into aggressive fleet expansion targets, particularly for heavy-duty logistics. This scale of deployment places stringent demands on membrane durability, chemical stability, and resistance to contamination over extended duty cycles. China’s strategy emphasizes localization of the entire PEM stack supply chain, including bipolar plates and balance-of-plant components, to support high-volume FCEV manufacturing. Nafion remains a benchmark membrane chemistry within this ecosystem, especially for applications requiring proven lifetime performance under variable load conditions.

South Korea’s Regulatory Consolidation and Hydrogen Market Confidence

South Korea’s Nafion market outlook is shaped by regulatory consolidation and long-term hydrogen planning under the “K-Hydrogen” framework. The creation of a centralized climate and energy ministry has reduced policy fragmentation, accelerating approvals for hydrogen mobility and power generation projects that depend on PEM technology. Legal clarity introduced through hydrogen-specific legislation has increased investor confidence in domestic MEA production lines, where Nafion-type membranes remain essential for performance-critical applications. In parallel, South Korea’s semiconductor and ultrapure water infrastructure creates ancillary demand for high-quality ion exchange membranes, reinforcing Nafion’s strategic relevance beyond energy alone.

Japan’s Digital Optimization of Legacy and Modern Membrane Applications

Japan’s Nafion market is characterized less by volume expansion and more by lifecycle optimization and digital integration. The country continues to lead in the chlor-alkali sector, where membrane longevity and energy efficiency are critical economic variables. Digital service platforms integrating IoT and data analytics are extending the operational life of ion exchange membranes while reducing power consumption across global plants. This approach sustains stable, replacement-driven demand for high-performance membranes and reinforces Japan’s role as a technology reference point for membrane process optimization. At the same time, Japan’s commitment to mercury-free and environmentally compliant production ensures continued modernization of membrane-based electrochemical systems.

National Strategic Development Matrix: Nafion Market (2025)

Nafion Market Development Matrix by Country

|

Country / Region

|

Primary Strategic Driver

|

2025 Policy or Investment Catalyst

|

Core Nafion Application Focus

|

|

United States

|

Hydrogen economics & reshoring

|

45V tax credit restoration, DOE Hydrogen Shot

|

PEM electrolyzers, critical mineral recovery

|

|

France

|

European manufacturing localization

|

PFSA capacity expansion for electrolyzers

|

PEM water electrolysis, flow batteries

|

|

Germany

|

Hydrogen infrastructure & cost competition

|

Hydrogen core grid, AEM pilot plants

|

High-pressure PEM systems, industrial H₂

|

|

China

|

Commercial FCEV scale

|

15th Five-Year Plan hydrogen designation

|

Fuel cell trucks, logistics fleets

|

|

South Korea

|

Regulatory reform & hydrogen mobility

|

K-Hydrogen legislation and ministry reform

|

PEM stacks, MEA localization

|

|

Japan

|

Digital optimization & compliance

|

IoT-enabled chlor-alkali modernization

|

Chlor-alkali membranes, lifecycle services

|

Nafion Market Report Scope

Nafion Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.4 Billion

|

|

Market Size (2035)

|

$2.4 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Product Form (Membranes, Dispersions, Resins), By Application (Energy & Power, Chemical Processing, Industrial, Analytical & Instrumentation, Semiconductor Manufacturing, Emerging Applications), By Equivalent Weight (Low Equivalent Weight, High Equivalent Weight), By Structure (Reinforced Membranes, Non-Reinforced Membranes)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Chemours Company, W. L. Gore & Associates Inc., Asahi Kasei Corporation, AGC Inc., Dongyue Group Ltd., Solvay S.A., 3M Company, Ballard Power Systems Inc., Plug Power Inc., Cummins Inc., Fumatech BWT GmbH, Freudenberg Sealing Technologies GmbH & Co. KG, VFlowTech Pte Ltd., Toshiba Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Nafion Market Segmentation

By Product Form

- Nafion Membranes

- Nafion Dispersions

- Nafion Resins

By Application

- Energy and Power

- Chemical Processing

- Industrial

- Analytical and Instrumentation

- Semiconductor Manufacturing

- Emerging Applications

By Equivalent Weight

- Low Equivalent Weight

- High Equivalent Weight

By Structure

- Reinforced Membranes

- Non-Reinforced Membranes

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Nafion Market

- The Chemours Company

- W. L. Gore & Associates, Inc.

- Asahi Kasei Corporation

- AGC Inc.

- Dongyue Group Ltd.

- Solvay S.A.

- 3M Company

- Ballard Power Systems Inc.

- Plug Power Inc.

- Cummins Inc.

- Fumatech BWT GmbH

- Freudenberg Sealing Technologies GmbH & Co. KG

- VFlowTech Pte Ltd.

- Toshiba Corporation

*- List not Exhaustive