Nano Paints and Coatings Market Size, Smart Nanomaterials, and High-Performance Functional Coatings Outlook

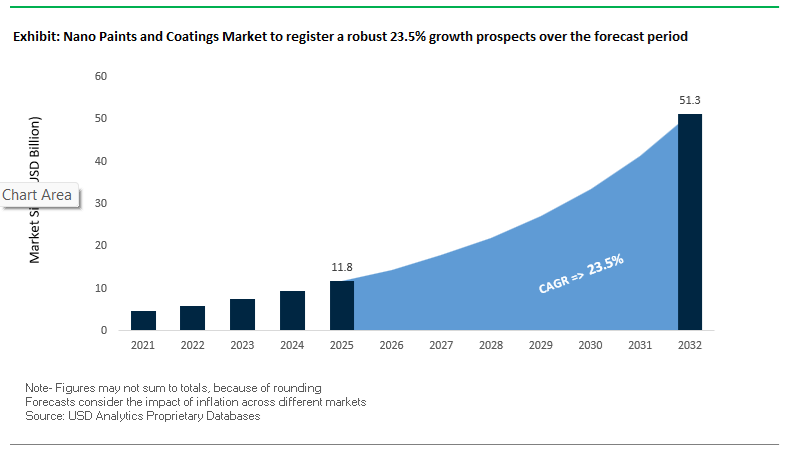

The global nano paints and coatings market was valued at $11.8 billion in 2025 and is projected to surge to $51.7 billion by 2032, expanding at an exceptional CAGR of 23.5%. This rapid growth is driven by increasing demand for nanocoatings, self-healing coatings, antimicrobial coatings, graphene-based coatings, and nano-enabled functional paints across automotive, construction, healthcare, electronics, and energy sectors. These coatings leverage nano-scale materials such as nanoparticles, carbon nanotubes (CNTs), and graphene to deliver enhanced durability, corrosion resistance, UV protection, and multifunctionality beyond conventional coatings.

A key growth driver is the rising adoption of smart coatings with advanced functionalities, including self-healing, anti-microbial, anti-corrosion, and energy-efficient properties. In sectors such as electric vehicles (EVs), aerospace, and infrastructure, nano coatings enable longer asset life, reduced maintenance, and improved performance under extreme conditions. Additionally, the integration of energy-harvesting and carbon-capturing capabilities is expanding the role of coatings from passive protection layers to active functional materials.

The market is also benefiting from advancements in material science, nanotechnology, and precision coating processes, which allow for ultra-thin, uniform, and highly efficient coatings. Regulatory pressure to reduce environmental impact is accelerating the adoption of low-VOC, bio-based, and sustainable nano-coatings. Regionally, North America and Europe lead in innovation and R&D, while Asia-Pacific is witnessing rapid adoption due to expanding industrial manufacturing and infrastructure development.

Market Analysis: Self-Healing Nanocoatings, Energy-Harvesting Surfaces, and Advanced Material Innovation Driving Market Evolution

The nano coatings industry is undergoing a transformative shift driven by breakthrough material innovations, strategic collaborations, and expanding industrial applications. In March 2026, Arkema expanded its portfolio of self-healing nanomaterials, designed for automotive and structural applications, with demonstrated micro-damage recovery efficiencies exceeding 80%. This technology significantly reduces maintenance requirements by enabling coatings to autonomously repair surface defects, enhancing long-term durability.

Product innovation is also advancing healthcare applications. In January 2026, Benjamin Moore introduced an antimicrobial coating utilizing silver-based nanotechnology, providing continuous pathogen resistance in high-traffic hospital environments. This reflects the growing importance of nano-enabled antimicrobial surfaces in infection control.

Strategic collaborations are accelerating the development of sustainable nano-coatings. The September 2025 R&D partnership between AkzoNobel, Arkema, and BASF focuses on developing low-carbon architectural coatings using nano-scale bio-based resins, aiming to reduce the environmental footprint of high-volume coating applications without compromising performance.

Energy-efficient and functional coating systems are gaining traction. In October 2025, AkzoNobel entered a strategic agreement to supply coatings for solar-absorbing wall technology, where nano-scale pigments enable building exteriors to capture and retain thermal energy, effectively transforming coatings into energy-harvesting surfaces. Similarly, Graphenstone’s May 2025 project in the Middle East utilizes graphene-infused coatings that act as a carbon sink, absorbing CO₂ while providing enhanced structural performance.

Advancements in nanomaterials are expanding applications in electronics and EVs. Nanocyl’s July 2025 investment in CNT-based materials supports the development of coatings that provide electrical conductivity and electromagnetic interference (EMI) shielding for EV battery systems and sensors. Additionally, Nano-X GmbH’s August 2025 facility expansion strengthens production of easy-to-clean and anti-corrosion nanocoatings, addressing demand in automotive and appliance sectors.

Technology integration is also improving coating performance and application efficiency. Sherwin-Williams’ October 2025 integration of nanotechnology additives enhances scratch resistance and UV durability, extending coating lifespan by up to 20%. AkzoNobel’s November 2024 introduction of nano-clearcoats with hydrogen-powered spray systems further supports low-energy curing and sustainable application processes in automotive refinishing.

Emerging coating processes are redefining precision and performance. Forge Nano’s January 2024 expansion of Atomic Layer Deposition (ALD) technology enables the creation of ultra-thin, pinhole-free barrier coatings for aerospace components, offering superior protection in critical high-performance environments.

Market Trend: Waterborne PFAS-Free Nano-Ceramic Coatings Redefining Non-Stick Cookware Performance and Compliance

The nano paints and coatings industry is undergoing a rapid transition toward waterborne PFAS-free ceramic coatings in the global cookware segment, driven by tightening regulatory frameworks and increasing scrutiny on fluorinated chemistries. Manufacturers are replacing traditional solvent-borne PTFE coatings with silica-based sol-gel nano coatings that deliver superior mechanical performance while aligning with evolving compliance requirements related to PFAS restrictions.

Nano-ceramic coatings are demonstrating a significant leap in hardness and thermal stability compared to legacy fluoropolymer systems. With pencil hardness reaching 9H, these coatings offer enhanced scratch resistance and durability, far exceeding the 2H to 3H range typically associated with PTFE coatings. Thermal resistance is another critical advantage, with ceramic nano coatings maintaining structural integrity at temperatures exceeding 450°C, compared to PTFE degradation thresholds around 260°C, where toxic emissions become a concern. This performance profile is positioning PFAS-free nano coatings as a safer and more durable alternative in high-temperature cookware applications.

Adoption rates are accelerating rapidly across developed markets. As of early 2026, more than 40% of new non-stick cookware product launches in Europe and North America feature ceramic nano coatings, reflecting a strategic shift by brands to comply with upcoming PFAS regulatory sunset clauses expected in 2026 and 2027. Manufacturing efficiency is also improving with waterborne systems. Modern nano-ceramic coating lines reduce curing energy consumption by up to 15% compared to PTFE-based processes, which require higher sintering temperatures and solvent recovery infrastructure. This combination of regulatory compliance, performance enhancement, and energy efficiency is driving large-scale adoption of nano-ceramic coatings in the cookware industry.

Market Trend: Diamond-Like Carbon Nano Coatings Advancing Wear Resistance and Clean Processing in Food Manufacturing Equipment

The industrial food processing segment is emerging as a high-growth application area for advanced nano coatings, particularly through the adoption of Diamond-Like Carbon coatings. These coatings are replacing conventional chrome plating and electroless nickel systems in high-speed and high-temperature processing environments such as extrusion equipment and chocolate molding systems.

DLC nano coatings deliver exceptional tribological performance, with coefficients of friction ranging between 0.05 and 0.1. This ultra-low friction significantly reduces mechanical energy loss and enhances process efficiency in continuous production systems. In high-pressure extrusion environments, DLC-coated components demonstrate up to 70% reduction in abrasive wear compared to hardened stainless steel, extending equipment lifespan and reducing maintenance frequency. These properties are critical in large-scale food processing operations where downtime directly impacts productivity.

Thermal stability further enhances the suitability of DLC coatings for food-grade applications. Advanced hydrogenated DLC variants maintain structural integrity at temperatures between 300°C and 350°C, enabling compatibility with clean-in-place systems without coating degradation or contamination risks. The coatings also exhibit micro-hardness levels between 20 and 30 GPa, approaching the hardness of industrial diamond while maintaining biocompatibility for direct food contact. These combined attributes are positioning DLC nano coatings as a high-performance solution for next-generation food processing equipment.

Market Opportunity: FDA PFAS Guidance Accelerating Reformulation Demand for Nano-Silica and Hybrid Food Contact Coatings

The regulatory landscape in the United States is creating substantial opportunities for nano coatings in food contact applications following the FDA’s updated guidance on PFAS substances. The agency’s determination that several legacy PFAS-based approvals are no longer valid has triggered a widespread reformulation cycle across the non-stick and grease-resistant coatings market.

This regulatory shift is driving a surge in Food Contact Notifications for PFAS-free alternatives, particularly nano-silica and bio-based hybrid coatings. Manufacturers with pre-validated PFAS-free formulations and comprehensive toxicological data are gaining a significant competitive advantage, achieving adoption cycles that are approximately 25% faster within the U.S. supply chain. This acceleration is particularly relevant for cookware and food packaging applications where regulatory approval timelines directly influence market entry.

Testing requirements under the updated guidance are also more stringent, with mandatory evaluation of sub-visible particulate release and strict migration limits. Nano-hybrid coatings that utilize cross-linked structures are demonstrating strong compliance, with zero detectable migration at thresholds as low as 10 parts per billion. This level of performance is reinforcing the transition toward advanced nano coatings that combine safety, durability, and regulatory readiness, creating a high-value opportunity segment for innovation-driven suppliers.

Market Opportunity: China GB 4806.7-2025 Standard Driving Large-Scale Transition to PFAS-Free Nano Coatings in Cookware Manufacturing

China’s implementation of the revised GB 4806.7-2025 food safety standard is creating a transformative opportunity for nano coatings, particularly in the global cookware manufacturing ecosystem. The standard introduces strict limits on perfluorinated compounds and persistent organic pollutants, effectively mandating the transition to PFAS-free coating technologies across one of the world’s largest production bases.

The regulation establishes a Total Fluorine limit of less than 50 mg/kg, with enforcement beginning in late 2025 and early 2026. This requirement is forcing widespread reformulation among manufacturers, particularly in major production hubs such as Guangdong and Zhejiang. The scale of this transition is substantial, with approximately 1.2 billion units of annual cookware production expected to shift from traditional fluoropolymer coatings to nano-ceramic and DLC-based alternatives.

This regulatory-driven market pivot is creating significant demand for advanced nano coating technologies that can meet both performance and compliance requirements. Suppliers offering PFAS-free formulations with proven durability, thermal resistance, and food safety credentials are well positioned to capture market share in this rapidly evolving landscape. The convergence of regulatory enforcement, manufacturing scale, and material innovation is positioning China as a central growth engine for the nano paints and coatings industry.

Nano Coatings Market Share and Segmentation Insights

Anti-Corrosion Nano Coatings Capture 22.6% Share Driven by Superior Durability and Thin-Film Performance

The nano paints and coatings market by type is led by anti-corrosion nano coatings, accounting for 22.6% of the global market share in 2025, driven by their advanced material science and superior protective capabilities. These coatings incorporate nanoparticles such as nano-silica, nano-zinc oxide, and nano-clay, which effectively fill microscopic pores within the coating matrix, significantly reducing electrolyte penetration and corrosion initiation. This results in 2–5x longer protection lifespan compared to conventional coatings, making them highly attractive for industrial, marine, and infrastructure applications. Additionally, nano-engineered coatings deliver equivalent corrosion resistance at 50–70% lower film thickness, reducing material consumption, application time, and overall lifecycle costs. As industries prioritize high-performance anti-corrosion coatings, durability, and cost efficiency, this segment continues to dominate the global nano coatings market.

Building & Construction Holds 32.5% Share Fueled by Self-Cleaning Facades and Antimicrobial Surface Demand

In the nano paints and coatings market by end-use industry, building and construction leads with a 32.5% market share in 2025, supported by increasing demand for smart, sustainable, and functional coatings in modern infrastructure. A key growth driver is the adoption of nano-TiO₂ self-cleaning coatings, which use photocatalytic reactions to break down organic dirt and harmful pollutants (NOx/SOx), aligning with global green building certifications such as LEED and BREEAM. Additionally, the post-pandemic environment has accelerated the use of nano-silver and nano-copper antimicrobial coatings on high-touch surfaces in hospitals, schools, commercial buildings, and public transport hubs. These coatings enhance hygiene and reduce pathogen transmission, making them critical for public safety. The convergence of energy-efficient building materials, environmental compliance, and health-focused coatings positions the construction sector as the largest consumer in the global nano coatings market.

Competitive Landscape of the Nano Paints and Coatings Market

AkzoNobel Leads with Sustainable Nano-Coating Innovations and Energy-Efficient Technologies

AkzoNobel N.V. has established itself as a global leader in sustainable nano paints and coatings, particularly in architectural and mobility applications. In 2026, the company partnered with IPG Photonics to introduce laser-based curing technology for its Interpon and Resicoat nano-powder coatings, reducing energy consumption by up to 30%. Its Futura Collection 2026–2029 leverages nano-SiO₂ technology to deliver ultra-matte, high-luminescence finishes for large-scale infrastructure. Additionally, AkzoNobel has expanded its Resicoat portfolio to support electric vehicle battery insulation, enhancing safety and thermal management. With a 47% reduction in carbon footprint since 2018, the company dominates the low-VOC and chromate-free nano-coatings segment.

PPG Industries Drives Growth Through Advanced Nano Barrier Coatings and Industrial Applications

PPG Industries, Inc. continues to strengthen its position in the industrial nano coatings market through extensive R&D capabilities and high-performance solutions. Its SIGMASHIELD™ product line, incorporating nanoparticle barrier technology, addresses corrosion under insulation (CUI) in oil and gas industries, contributing to strong financial performance in 2026. The company has also invested in a cutting-edge facility in France to scale UV-curable nanocomposite coatings for electronics, enabling instant-cure protection. PPG’s innovation in PVC-NI nano-coatings for food packaging ensures BPA-free compliance, while its strategic focus on hyperscale data centers highlights its role in thermal management and anti-corrosion nano solutions.

Henkel Expands Nano-Ink and Smart Coating Leadership Through Strategic Acquisition

Henkel AG & Co. KGaA is a pioneer in conductive nano-inks and printed electronics, integrating nanotechnology with IoT applications. The company’s $2.5 billion acquisition of Stahl Holdings in 2026 significantly enhances its capabilities in nano-surface treatments for automotive and luxury materials. At LOPEC 2026, Henkel introduced silver plated-copper nano-ink technology, reducing material costs by 40% while maintaining high conductivity. Its dominance in PTC nano-coatings supports thermal management in batteries and wearable devices. Through the Inspiration Center Düsseldorf, Henkel collaborates across 800+ industries, reinforcing its leadership in customized nano-adhesive and coating solutions.

Nanovere Technologies Advances High-Performance 3D Nano-Coatings for Durability and Marine Efficiency

Nanovere Technologies, LLC is a leading innovator in 3D-structured nano-coatings, specializing in extreme durability and hydrophobic performance. Its proprietary Zyvere® technology achieves 9H hardness with high flexibility, making it ideal for demanding industrial applications. In 2026, the company expanded into the marine sector, offering biofouling-resistant coatings that reduce hydrodynamic drag without toxic chemicals. Its Nano-Clear® coatings provide over 10 years of UV resistance, targeting asset refurbishment and fleet protection markets. Furthermore, its scalable single-component moisture-cure nano-coatings enable field applications with factory-level durability, strengthening its position in the high-performance nano coatings market.

Nippon Paint Dominates Photocatalytic and Self-Cleaning Nano Coatings in Asia

Nippon Paint Holdings is a dominant force in the photocatalytic nano coatings market, particularly across Asia-Pacific infrastructure sectors. Its NANO Clean Clear Coat technology creates hydrophilic surfaces that enable self-cleaning through rainwater, addressing facade maintenance challenges. The company is investing heavily—¥4 trillion—in smart functional coatings to eliminate harmful chemicals like PFAS and MCCPs. Its innovation in hydrogel-based nano-antifouling marine coatings reduces fuel consumption by up to 8%, enhancing operational efficiency. With a leading presence in Japan and China, Nippon Paint leverages nanoscale particle distribution to achieve high-quality finishes while reducing material usage.

P2i Ltd Specializes in Ultra-Thin Liquid-Repellent Nano-Coatings for Electronics and Automotive Sensors

P2i Ltd is a global leader in liquid-repellent nano coatings, particularly for consumer electronics and advanced hardware. Its Pulse™ and Ion-Mask™ technologies utilize plasma deposition nano-coating processes, creating ultra-thin protective layers significantly thinner than human hair while delivering IPX8 waterproofing. The company has introduced halogen-free nano coatings for PCBs, supporting sustainable and repairable electronics manufacturing. P2i is a preferred partner for major smartphone OEMs, protecting over 1 billion devices globally. In 2026, it expanded into automotive applications, providing nano-coatings for ADAS and LiDAR systems, enhancing performance in autonomous driving environments.

United States Nano Paints and Coatings Market: Smart Functional Surfaces and Defense-Grade Innovation

The United States leads the nano paints and coatings market, driven by high-value innovation across aerospace, defense, healthcare, and semiconductor industries. The commercialization of 3D-structured nano-coatings is enabling superior scratch resistance and optical clarity, particularly for automotive glazing and aerospace windows. Government backing through the National Nanotechnology Initiative (NNI) is accelerating the development of carbon-capturing nano-coatings, where surfaces actively absorb CO₂, aligning with sustainability goals.

Regulatory oversight under EPA TSCA guidelines is pushing manufacturers toward “Safe-by-Design” nano-coating formulations, particularly for antimicrobial consumer applications. The market is also benefiting from strong demand for nano-hydrophobic coatings in electronics and semiconductor manufacturing, ensuring resistance to moisture and oxidation. Investments in laser-based powder curing technologies are reducing energy consumption while enhancing nanoscale deposition precision. Innovations such as nano-silver and TiO₂-based air-purifying paints are gaining traction in architectural applications, offering continuous antimicrobial protection and improved indoor air quality.

China Nano Paints and Coatings Market: Industrial Scale Production and Green Manufacturing Transition

China dominates the global nano coatings market in volume, driven by rapid industrialization and government mandates promoting green manufacturing and low-VOC technologies. Policies such as the “Blue Sky Defense War” are incentivizing the adoption of nano-enhanced waterborne coatings, accelerating the transition away from solvent-based systems.

Technological advancements include the scaling of graphene-reinforced nano coatings, which significantly enhance corrosion resistance and extend the lifecycle of infrastructure such as coastal power pylons. The deployment of photocatalytic “lotus-effect” coatings on high-speed rail networks is reducing maintenance requirements through self-cleaning surfaces. China’s strong presence in the EV battery sector is also driving demand for nano-ceramic thermal barrier coatings, preventing thermal runaway in lithium-ion batteries. Expansion of production facilities for nano-SiO₂ and carbon nanotube dispersions is further strengthening China’s position as a global supplier of advanced nano-coating materials.

Germany Nano Paints and Coatings Market: Circular Economy and Precision Engineering Leadership

Germany is a European leader in nano paints and coatings, focusing on precision engineering, sustainability, and circular economy integration. The development of biocide-free nano-structured coatings is enabling environmentally safe solutions for marine and industrial applications, relying on physical surface properties rather than chemical leaching.

Major players such as Evonik and Henkel are advancing bio-based nano-emulsions using cellulose nanocrystals, replacing traditional petroleum-based resins. Regulatory alignment with the EU Eco-Label (2026) is pushing manufacturers toward zero-SVOC nano coatings, ensuring minimal environmental impact. Investments in digital twin coating lines are enabling real-time monitoring of nanoscale deposition, enhancing quality and consistency. Germany’s leadership in anti-reflective nano coatings for semiconductor lithography and medical optics further highlights its dominance in high-precision applications.

India Nano Paints and Coatings Market: Renewable Energy and Infrastructure Expansion Driving Growth

India is emerging as a high-growth market for nano paints and coatings, supported by large-scale infrastructure investments and renewable energy expansion. The National Infrastructure Pipeline is driving demand for nano-SiO₂ reinforced coatings, which significantly enhance the durability of bridges, tunnels, and public infrastructure.

The country is witnessing strong adoption of anti-reflective and anti-soiling nano coatings for solar panels, improving energy output in high-dust regions. The establishment of dedicated nano-coating manufacturing facilities, such as the Chakan plant, is strengthening domestic production capabilities. Government initiatives under the PLI scheme are expected to boost the specialty nano-chemicals segment, reducing reliance on imports. Innovations such as nano-TiO₂ cool roof paints are addressing urban heat challenges, while the growing demand for nano-silver antimicrobial coatings is expanding applications in healthcare and public infrastructure.

Japan Nano Paints and Coatings Market: Advanced Material Science and High-Performance Applications

Japan’s nano coatings market is defined by high-performance materials, precision engineering, and advanced R&D investments, particularly in electronics and transportation sectors. Continuous investment exceeding $2.1 billion annually is driving innovation in nano-carbon interfaces and hybrid coatings.

Technological advancements include inorganic-organic hybrid nano coatings, combining ceramic hardness with polymer flexibility for next-generation flexible displays. The market also benefits from applications in high-speed rail systems, where heat-shielding nano coatings protect components from friction-induced stress. Government initiatives are supporting the development of advanced materials hubs, while regulatory compliance under CSCL updates ensures environmental safety in nanomaterial usage. Innovations such as anti-fog nano coatings are further enhancing performance in robotics and surveillance systems.

South Korea Nano Paints and Coatings Market: Electronics and Energy Storage Innovation Hub

South Korea is emerging as a key player in the nano paints and coatings market, driven by its dominance in electronics manufacturing and energy storage systems. Breakthroughs in high-dielectric nano coatings are enabling improved insulation and thermal management in EV motor housings, supporting compact and efficient designs.

The country is also leading in the development of ultra-durable nano coatings for foldable OLED displays, capable of withstanding extensive mechanical stress without degradation. Government support through initiatives such as the K-Battery Strategy is driving the adoption of solvent-free nano-coating technologies. Investments in advanced R&D facilities, including KCC Corporation’s Surface Engineering Excellence Center, are accelerating innovation in nano-silicone hybrid coatings. Additionally, the integration of bio-renewable nano-cellulose sealants in packaging applications highlights South Korea’s commitment to sustainable material solutions.

Nano Paints and Coatings Market Report Scope

Nano Paints and Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.8 Billion

|

|

Market Size (2032)

|

$51.7 Billion

|

|

Market Growth Rate

|

23.5%

|

|

Segments

|

By Type (Anti-Microbial, Self-Cleaning, Anti-Corrosion, Anti-Fingerprint, Thermal Insulation, Conductive and Anti-Static, UV-Resistant, Specialty), By Nanomaterial (Graphene and Carbon Nanotubes, Nano-Silicon Dioxide, Nano-Titanium Dioxide, Nano-Silver, Nano-Zinc Oxide, Nano-Clays, Nano-Zirconia), By Technology (Water-borne, Solvent-borne, Powder Coatings, Radiation-Cured), By Substrate (Metal, Glass, Plastic, Ceramics, Textiles and Wood), By End-Use Industry (Building and Construction, Automotive and Transportation, Electronics, Healthcare and Medical, Aerospace and Defense, Marine, Food and Beverage Packaging)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., Akzo Nobel N.V., The Sherwin-Williams Company, BASF SE, Axalta Coating Systems Ltd., P2i Ltd., Nanogate SE, HZO, Inc., Tesla NanoCoatings, Inc., Nanophase Technologies Corporation, Bio-Gate AG, Nanovere Technologies, LLC, NEI Corporation, Aculon, Inc., ACTnano, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Nano Paints and Coatings Market Segmentation

By Type

- Anti-Microbial

- Self-Cleaning

- Anti-Corrosion

- Anti-Fingerprint

- Thermal Insulation

- Conductive and Anti-Static

- UV-Resistant

- Specialty

By Nanomaterial

- Graphene and Carbon Nanotubes

- Nano-Silicon Dioxide

- Nano-Titanium Dioxide

- Nano-Silver

- Nano-Zinc Oxide

- Nano-Clays

- Nano-Zirconia

By Technology

- Water-borne

- Solvent-borne

- Powder Coatings

- Radiation-Cured

By Substrate

- Metal

- Glass

- Plastic

- Ceramics

- Textiles and Wood

By End-Use Industry

- Building and Construction

- Automotive and Transportation

- Electronics

- Healthcare and Medical

- Aerospace and Defense

- Marine

- Food and Beverage Packaging

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Nano Paints and Coatings Industry

- PPG Industries, Inc.

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- BASF SE

- Axalta Coating Systems Ltd.

- P2i Ltd.

- Nanogate SE

- HZO, Inc.

- Tesla NanoCoatings, Inc.

- Nanophase Technologies Corporation

- Bio-Gate AG

- Nanovere Technologies, LLC

- NEI Corporation

- Aculon, Inc.

- ACTnano, Inc.

*- List not Exhaustive