Natural Phosphates Market Growth Driven by Phosphoric Acid Output Gains, Mining Expansion, and Rising Battery-Grade Phosphate Demand (2025–2034)

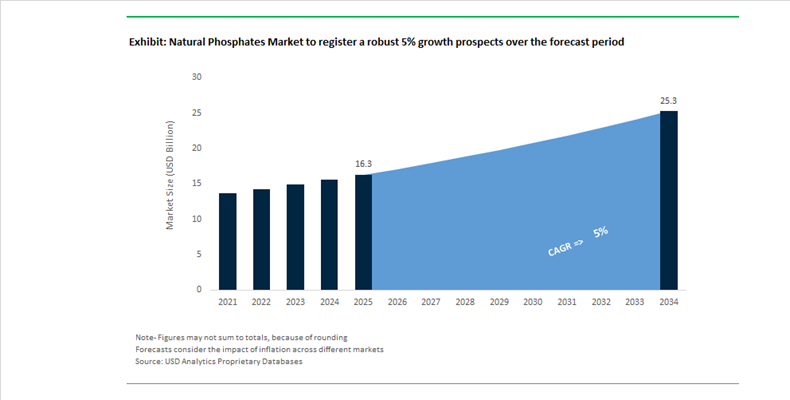

The Natural Phosphates Market is projected to expand from USD 16.3 billion in 2025 to USD 25.3 billion by 2034, registering a CAGR of 5%, driven by intensifying demand across phosphatic fertilizers, industrial applications, and emerging battery-grade phosphate materials. For industry professionals and institutional buyers, the market is currently defined by production efficiency gains, supply chain stabilization strategies, and evolving end-use competition. As of early 2026, leading producers are achieving 21% year-over-year increases in phosphoric acid output through advanced beneficiation technologies, directly addressing post-2025 supply volatility. Simultaneously, global refining hubs are operating at or above 80% capacity utilization, signaling tight supply-demand balance ahead of seasonal agricultural demand peaks exceeding 7 million tonnes of phosphate products in North America alone. Strategic mine expansions, such as the addition of ~1,966 acres to extend production life and secure 6 million tons per annum output, reinforce long-term supply security. However, the market is undergoing structural transformation, with LFP battery demand competing for phosphate feedstock and premium phosphate products delivering 10–15% yield improvements, while European sustainability mandates requiring 20% phosphorus recovery are redefining sourcing models and accelerating circular economy integration.

The global natural phosphates industry is undergoing a period of strategic consolidation, capital restructuring, and operational optimization, with major players actively reinforcing vertically integrated value chains. In March 2026, PhosAgro strengthened its financial position through the issuance of CNY 1.5 billion in bonds, enabling accelerated execution of its 2025–2030 development strategy focused on integrated phosphate fertilizer production and logistics expansion. This aligns with broader industry trends emphasizing cost control, supply chain resilience, and downstream value capture. In February 2026, The Mosaic Company reported $150 million in value capture during 2025, with an additional $100 million cost optimization initiative launched for 2026, underscoring a continued shift toward operational efficiency amid margin pressures.

Capacity expansion and geopolitical positioning remain central to competitive dynamics. In January 2026, the Saudi Arabian Mining Company (Ma’aden) secured feedstock allocation approval for its “Phosphate 4” project, set to increase total production capacity to nearly 12 million tonnes per annum, reinforcing Saudi Arabia’s emergence as a dominant global phosphate exporter. However, the same month also highlighted input cost volatility risks, as Mosaic extended production curtailments in Brazil due to rising sulfur prices, illustrating the sector’s sensitivity to upstream raw material fluctuations. Earlier, in December 2025, Ma’aden completed the acquisition of Mosaic’s stake in the Wa’ad Al Shamal Phosphate Company, a move aligned with its long-term objective of tripling phosphate output by 2030 within a broader $110 billion mining expansion framework.

Policy interventions and sustainability-driven investments are further reshaping market fundamentals. In November 2025, India launched the National Critical Mineral Mission (NCMM), streamlining regulatory approvals and reducing dependency on imports by accelerating domestic phosphate mining projects. Complementing this, August 2025 saw amendments to India’s MMDR Act, allowing up to 10% mining lease area expansion, unlocking previously inaccessible deep phosphate reserves. Meanwhile, sustainability initiatives are gaining capital priority, exemplified by OCP Group’s October 2025 investment of over $910 million into renewable energy and desalination infrastructure at its Jorf Lasfar hub. These developments collectively indicate a transition toward sustainable phosphate mining, regulatory acceleration, and resource security, while simultaneously redefining competitive benchmarks across the global natural phosphates market.

Natural Phosphates Market Trends and Opportunities

Trend: Geopolitical Reshoring and Critical Mineral Reclassification

Natural phosphates have decisively moved from being treated as a commoditized fertilizer input to a geopolitically sensitive critical mineral. This structural shift is reshaping investment flows, trade routes, and long-term procurement strategies across agriculture, energy, and industrial supply chains. In November 2025, the U.S. Department of the Interior formally added phosphate to its Critical Minerals List, a move that unlocks expedited permitting, federal financing mechanisms, and infrastructure incentives for domestic mining and beneficiation. The policy objective is clear: reduce exposure to the 3.5 million tonnes of phosphate imports recorded in 2024 and insulate food and energy systems from external shocks.

In parallel, Western buyers are actively engineering alternative supply corridors to counterbalance China’s dominance, which still accounts for nearly 98% of Asia-Pacific phosphate rock output under increasingly strict domestic-first export controls. The resulting supply tightness has already translated into price volatility, with DAP spot prices in Western Europe reaching USD 750 to 760 per tonne in late 2025. Strategic equity investments are accelerating along the Senegal-Canada-Norway axis, which is emerging as a politically aligned phosphate belt. A notable example is Coromandel International, which increased its ownership in Senegal’s Baobab Mining project to secure long-term rock supply for India, where urea and phosphate sales reached a record six million tonnes in December 2025. These moves signal that natural phosphates are now being sourced through long-horizon, security-driven strategies rather than spot-market optimization.

Trend: Premiumization of Reactive Phosphate Rock for Organic Soil Health

Alongside geopolitical realignment, the market is undergoing a qualitative shift toward Reactive Phosphate Rock as agribusinesses reframe soil fertility through a regenerative lens. Large-scale food producers aligned with Science Based Targets initiatives are actively encouraging the replacement of acid-treated superphosphates with minimally processed natural phosphates that can be applied directly to soil. This transition eliminates the energy-intensive sulfuric acid stage, reducing the Scope 3 carbon footprint of crop production by an estimated 30 to 40% while improving long-term soil biology.

The momentum is reinforced by policy tailwinds. Government frameworks such as India’s BioE3 Policy and the EU Green Deal are favoring mineral-based organic inputs, propelling the global organic fertilizer market toward a projected USD 10 billion valuation in 2025. Precision agriculture technologies deployed at scale in 2025 are further improving the economics of RPR by enabling targeted placement and optimized particle sizing. These advances are reported to increase phosphate use efficiency by up to 20%, particularly in alkaline soil regions where water-soluble phosphates underperform. As a result, RPR is no longer viewed as a niche organic input but as a scalable, premium solution aligned with both productivity and decarbonization goals.

Opportunity: High-Purity Refinement for the LFP Battery Boom

The electrification of transport represents the most powerful non-agricultural demand catalyst for natural phosphates. Lithium iron phosphate battery chemistry has overtaken nickel-based systems as the dominant global platform, with LFP cell production expected to exceed 1,100 GWh in 2025, accounting for roughly 63% of total battery output. Each gigawatt-hour of LFP capacity consumes substantial volumes of high-purity phosphorus, placing unprecedented strain on existing phosphoric acid supply chains.

This demand surge has already triggered a price response. In late 2025, prices for 85% high-purity phosphoric acid rose sharply from 6,400 to 7,000 yuan per tonne, tracking record phosphate ore production levels. In response, new projects in Canada and Norway are being designed as vertically integrated ore-to-cathode hubs. These facilities bypass traditional fertilizer markets entirely, focusing instead on converting igneous phosphate rock directly into purified phosphoric acid tailored for battery-grade specifications. For natural phosphate producers, this represents a structural upgrade from volume-driven fertilizer margins to technology-linked energy transition economics.

Opportunity: Non-Toxic Flame Retardant Fillers for Green Construction

A second high-margin opportunity is emerging at the intersection of construction safety and environmental regulation. As halogenated flame retardants are phased out under EU REACH and comparable frameworks, phosphorus-based mineral fillers derived from natural phosphate are gaining traction as safer alternatives. Apatite-based fillers and phosphate-reactive systems are being incorporated into building materials, technical textiles, and polymer composites to meet increasingly strict fire safety codes without compromising recyclability.

Advances in Calcium Magnesium Phosphate Cement technology reported in 2025 demonstrate that phosphate-based systems can protect steel structures at temperatures up to 500–600°C while offering superior adhesion compared with gypsum coatings. Beyond infrastructure, electronics manufacturers are also integrating finely ground natural phosphates into polymers for smartphones and laptops to meet low-toxicity and circularity certifications. This convergence of fire safety, sustainability, and regulatory compliance positions natural phosphates as a critical functional material well beyond their traditional fertilizer role.

Natural Phosphates Market Share and Segmentation Insights

Phosphate Rock Dominates Natural Phosphates Market as the Primary Feedstock for Fertilizer Production

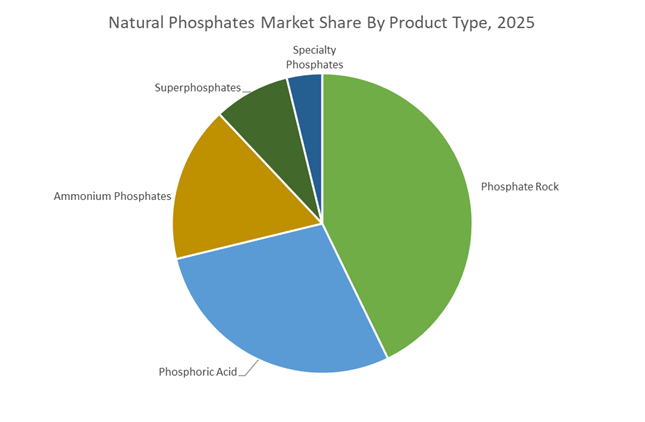

Phosphate rock accounted for 42.80% of the Natural Phosphates Market share in 2025, making it the most important raw material within the global phosphate value chain. Phosphate rock is the fundamental mineral resource used to produce phosphoric acid, ammonium phosphates, superphosphate fertilizers, and other phosphate derivatives that support agricultural productivity and industrial chemical applications. Global phosphate rock production exceeds 200 million tons annually, with the majority processed into fertilizer-grade phosphates used in crop nutrient formulations. The market is highly influenced by the geographic distribution of phosphate reserves, which are concentrated in a limited number of countries including Morocco, China, the United States, and Russia, creating strategic supply considerations for fertilizer producers and agricultural economies. In 2025, growing awareness of phosphate resource security has driven investment in new mining operations, beneficiation technologies, and improved resource recovery techniques. Producers are also exploring methods to optimize ore utilization and recover phosphate from industrial byproducts and waste streams, supporting long-term supply stability in a resource-constrained global market.

Agriculture Sector Drives the Largest Demand for Natural Phosphates

Agriculture accounted for 74.80% of the Natural Phosphates Market share in 2025, making crop nutrient production the overwhelmingly dominant application for phosphate-based materials. Phosphorus is one of the three primary macronutrients required for plant growth, playing a critical role in root development, energy transfer within plants, photosynthesis, and crop yield formation. Phosphate fertilizers derived from natural phosphates are widely used across major agricultural crops including corn, wheat, rice, soybeans, and oilseeds, which collectively support global food supply chains. As the global population continues to grow and dietary patterns shift toward higher protein consumption, agricultural systems require increased fertilizer inputs to maintain productivity and soil fertility. In 2025, agricultural producers are increasingly adopting circular phosphorus management strategies due to concerns about long-term phosphate resource availability. Technologies such as struvite recovery from wastewater treatment plants, nutrient recycling from livestock manure, and phosphorus recovery from food processing waste streams are gaining attention as supplemental phosphorus sources that can complement mined phosphate resources and support more sustainable fertilizer supply systems.

Natural Phosphates Market Competitive Landscape

The natural phosphates market in 2026 is shaped by resource control, decarbonized fertilizer production, and low-impurity phosphate sourcing. Competitive leadership hinges on access to high-grade reserves, cadmium compliance, green ammonia integration, and tailored nutrient solutions that enhance crop yield, soil health, and fertilizer efficiency.

OCP Group scales green ammonia integration and customized phosphate solutions for global agriculture

OCP Group dominates the natural phosphates market by leveraging over 70% of global reserves and transitioning toward customized plant nutrition solutions. The company reported US$11.4 billion revenue in 2025, driven by strong demand from India and Brazil. Its tailored nutrient portfolio now accounts for 30% of total sales, reflecting a 55% year-over-year increase. OCP is investing heavily in its Green Investment Program, including renewable-powered ammonia production and desalinated water usage. With over US$910 million in Q4 2025 capex, it is expanding capacity for sustainable DAP and MAP fertilizers. This integrated, low-carbon phosphate strategy positions OCP as a global leader in decarbonized fertilizer production.

Ma’aden accelerates phosphate mega-project expansion with integrated logistics and long-term supply contracts

Ma’aden is rapidly expanding its phosphate production capacity through its Phosphate 3 and upcoming Phosphate 4 projects, targeting 12 million t/a output. The company reported a 73% increase in net profit (SAR 3.47 billion) in H1 2025, supported by strong DAP production and favorable pricing. A five-year agreement to supply 3.1 million MT annually to India secures long-term demand visibility. Its fully integrated logistics chain, from Wa’ad Al Shamal to Ras Al Khair, minimizes supply disruptions and costs. The addition of 2.5 million t/a capacity reinforces its position as a future top global exporter. Ma’aden’s scale, integration, and export strategy underpin its competitive strength.

PhosAgro leverages ultra-low impurity igneous phosphate to capture premium regulated markets

PhosAgro differentiates itself through high-purity igneous phosphate rock with low cadmium content, enabling premium positioning in regulated markets. The company achieved 3.11 million tonnes production in Q1 2025, with phosphate fertilizers increasing by 5%. Its Balakovo plant expansion is set to add nearly 1 million tonnes annually by 2026. Strong vertical integration ensures self-sufficiency in sulfuric and phosphoric acid production, supporting a 33% EBITDA margin. Exports to Africa grew by 16.1%, reflecting expansion into high-growth agricultural regions. Its eco-efficient production and compliance advantage make it a preferred supplier for specialty fertilizers and animal feed.

Mosaic integrates biological solutions and resource optimization to stabilize North American phosphate supply

The Mosaic Company is focusing on biological-enhanced fertilizers and mine life extensions to sustain its leadership in North America. Production curtailments in Brazil highlight its margin-first strategy amid volatile sulfur prices. The South Fort Meade expansion aims to secure 6 million tons per year of phosphate rock, extending operational life by four years. Mosaic Biosciences is advancing nutrient use efficiency (NUE) technologies, improving fertilizer performance and reducing application intensity. The company anticipates a balanced-to-tight phosphate market in 2026, driven by soil nutrient replenishment needs. Its integration of biologicals and resource management strengthens long-term competitiveness.

ICL pivots toward specialty phosphates and high-margin nutrition segments with focused portfolio optimization

ICL Group is repositioning its phosphate business toward specialty mineral applications and high-margin segments. Its Phosphate Solutions division generated US$605 million in Q3 2025, supported by increased specialty phosphate volumes and improved pricing. The company has exited capital-intensive LFP battery projects to focus on core strengths in food-grade and specialty crop nutrition. R&D initiatives, including collaboration with Hebrew University, target improved phosphorus mobility to address soil fixation challenges. ICL’s strategy emphasizes value-added phosphate derivatives and innovation-driven growth. This focused portfolio transformation enhances profitability and market differentiation.

Morocco: Vertical Integration, Green Ammonia, and Specialty Phosphate Leadership

Morocco continues to anchor the global natural phosphates ecosystem through scale, integration, and accelerated decarbonization. OCP Group’s multi-year green investment strategy, spanning 2023 to 2027, is structurally reshaping phosphate mining and downstream fertilizer production. The $13 billion program targets an increase in fertilizer capacity from 12 million tons to 20 million tons by 2027, supported by the commissioning of the Meskala mine and a dedicated chemical complex at Mzinda. These assets strengthen Morocco’s position across phosphate rock beneficiation, phosphoric acid conversion, and finished fertilizer manufacturing, while improving ore logistics and product flexibility.

Decarbonization is now embedded into Morocco’s phosphate cost curve. In April 2025, OCP finalized a $1.75 billion bond issuance to fund its 2030 roadmap, with green ammonia production as a central pillar. By reducing exposure to fossil-fuel-based nitrogen imports, OCP is structurally lowering emissions intensity while securing long-term input availability. This transition is reinforced by renewable power and water security investments. By late 2025, three solar plants totaling 202 MWp were activated, with LFP battery energy storage scheduled for summer 2026. These systems power reverse-osmosis desalination units, enabling full reliance on non-conventional water for mining and processing. Parallel acquisitions, including the expansion to a 75% stake in GlobalFeed, are shifting Morocco further into specialty animal nutrition phosphates and water-soluble fertilizer formulations, supported by green financing agreements with SACE and AFD concluded in mid-2025.

Saudi Arabia: Capacity Expansion and Long-Term Offtake Security

Saudi Arabia is positioning phosphate mining as a strategic pillar of industrial diversification under Vision 2030. In 2025, Ma’aden secured Ministry of Energy approval for feedstock allocation for its fourth phosphate expansion project. The Phosphate 4 initiative is designed to add 2.5 million tons of phosphate and specialty fertilizer capacity, pushing total annual output toward 12 million tons. This expansion reinforces Saudi Arabia’s role as a large-scale, integrated supplier to global fertilizer markets.

Demand visibility is being locked in through long-term bilateral agreements. In July 2025, Ma’aden signed a five-year supply agreement with India covering 3.1 million tonnes of phosphate fertilizers annually. Early execution was evident by October 2025, when a 180,000-tonne DAP shipment was delivered at $728 per tonne CFR. Alongside offtake security, Saudi Arabia is accelerating upstream exploration and processing integration through the Ma’aden Hancock partnership. Investments in mining wastewater recovery technologies deployed in late 2025 are also improving operational sustainability and water efficiency across phosphate assets.

United States: Strategic Mineral Reframing and Technology-Driven Recovery

The United States natural phosphates market is undergoing a strategic redefinition driven by national security and resource efficiency priorities. In November 2025, phosphate and potash were formally added to the U.S. Critical Minerals List. This designation is expected to streamline federal permitting, unlock funding pathways, and prioritize domestic phosphate assets as essential to food security and defense resilience.

Technology upgrades are reinforcing competitiveness at the mine level. In July 2025, The Mosaic Company commissioned the Hydrofloat system at Esterhazy, adding 400,000 tonnes of annual capacity by recovering fine-grained minerals previously lost in tailings. This materially improves resource utilization while lowering unit cash costs. In parallel, Mosaic is advancing research into extracting rare earth elements from phosphogypsum byproducts. By positioning phosphate mining as a secondary source of REEs relevant to electric vehicles and defense technologies, U.S. producers are broadening the strategic relevance of domestic phosphate operations ahead of 2026.

Russia: Process Self-Sufficiency and Resource Longevity

Russia’s natural phosphates industry is focused on internal resilience and long-term ore security. In 2025, PhosAgro invested approximately RUB 70 billion to modernize its Balakovo complex, commissioning new sulphuric acid process lines in June that added 750,000 tonnes per year of capacity. This upgrade enhances self-sufficiency in critical inputs for phosphate rock processing, insulating operations from external supply volatility.

Production flexibility is also improving. Pilot systems introduced in mid-2025 allow dynamic switching between MAP, DAP, NPK, and NPS fertilizers, targeting nearly one million tonnes of incremental output versus 2024. On the resource side, underground mining at the Rasvumchorr Plateau commenced in October 2025, with a design capacity of 6 million tonnes of apatite-nepheline ore annually. This development underpins long-term feedstock availability for Russia’s phosphate value chain.

Egypt: Export-Oriented Expansion and Downstream Integration

Egypt is accelerating its transition from phosphate rock exporter to downstream processor. The government announced a $573 million investment in a new phosphoric acid plant at Abu Tartour, with construction scheduled to begin in 2026 and initial output targeted at 250,000 tons annually. This facility is expected to anchor value addition in the New Valley region.

At the mining level, Misr Phosphate is expanding run-of-mine capacity to 7 million tonnes per year by end-2025. The company is targeting European buyers with de-dusted, higher-grade phosphate rock, aiming to export 1 million tonnes annually by late 2026. Further downstream integration is planned through negotiations for a DAP, MAP, and NPK complex at Ain Sokhna, expected to conclude by early 2026 with a proposed DAP capacity of 600,000 tonnes per year.

Jordan: Market Access and Sustainability Credentials

Jordan’s phosphate sector is consolidating its position through export strength and sustainability recognition. By December 2025, Jordan Phosphate Mines Company reported exports to India valued at 1.6 billion dinars annually, supported by newly secured mining rights that enhance supply continuity to South Asia.

Sustainability is emerging as a competitive differentiator. In 2025, JPMC received a four-star Recognition of Excellence rating from the European Foundation for Quality Management, becoming the first Jordanian mining company to achieve this milestone. The certification reflects progress in responsible extraction, logistics efficiency, and environmental stewardship, strengthening Jordan’s positioning with international buyers.

Comparative Summary: Natural Phosphates Market by Country

Natural Phosphates Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Developments

|

Structural Impact

|

|

Morocco

|

Decarbonized vertical integration

|

Green ammonia, renewables, desalination

|

Lowest-carbon, specialty-led phosphate supply

|

|

Saudi Arabia

|

Capacity and offtake security

|

Phosphate 4, India supply deal

|

Stable long-term export growth

|

|

United States

|

Critical minerals and recovery tech

|

Hydrofloat, REE extraction

|

Enhanced resource efficiency and security

|

|

Russia

|

Process self-sufficiency

|

Balakovo upgrades, Rasvumchorr mine

|

Long-term production resilience

|

|

Egypt

|

Downstream value addition

|

Abu Tartour acid plant, export upgrades

|

Shift from rock exporter to processor

|

|

Jordan

|

Export competitiveness and ESG

|

India exports, EFQM recognition

|

Premium access through sustainability

|

Natural Phosphates Market Report Scope

Natural Phosphates Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$16.3 Billion

|

|

Market Size (2034)

|

$25.3 Billion

|

|

Market Growth Rate

|

5%

|

|

Segments

|

By Product Type (Phosphate Rock, Phosphoric Acid, Ammonium Phosphates, Superphosphates, Specialty Phosphates), By Resource Source (Marine Deposits, Igneous Deposits, Biogenic Deposits), By Application (Fertilizers, Animal Feed, Industrial Chemicals, Food and Beverage Ingredients, Energy Materials), By End-User Industry (Agriculture, Animal Husbandry, Food Processing, Electronics and Batteries, Water Treatment)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

OCP Group, The Mosaic Company, PhosAgro, Ma’aden, Nutrien, ICL Group, Jordan Phosphate Mines Company, EuroChem Group, Groupe Chimique Tunisien, Misr Phosphate, Wengfu Group, Yunnan Phosphate Haikou, Yara International, Vale, Hubei Xingfa Chemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Natural Phosphates Market Segmentation

By Product Type

- Phosphate Rock

- Phosphoric Acid

- Ammonium Phosphates

- Superphosphates

- Specialty Phosphates

By Resource Source

- Marine Deposits

- Igneous Deposits

- Biogenic Deposits

By Application

- Fertilizers

- Animal Feed

- Industrial Chemicals

- Food and Beverage Ingredients

- Energy Materials

By End-User Industry

- Agriculture

- Animal Husbandry

- Food Processing

- Electronics and Batteries

- Water Treatment

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Natural Phosphates Market

- OCP Group

- The Mosaic Company

- PhosAgro

- Ma’aden

- Nutrien

- ICL Group

- Jordan Phosphate Mines Company

- EuroChem Group

- Groupe Chimique Tunisien

- Misr Phosphate

- Wengfu Group

- Yunnan Phosphate Haikou

- Yara International

- Vale

- Hubei Xingfa Chemicals

*- List not Exhaustive