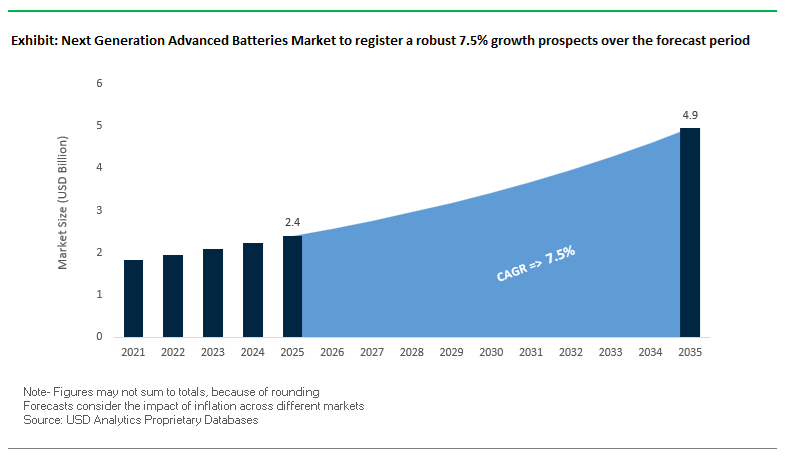

The Next Generation Advanced Batteries Market, valued at USD 2.4 billion in 2025 and projected to reach USD 4.9 billion by 2035 at a CAGR of 7.5% (2025–2035), is being reshaped by breakthroughs in solid-state, semi-solid, sodium-ion and lithium-metal batteries.

From 2024 through late 2025, the global next generation advanced batteries market has shifted decisively from concept to industrialization, supported by large-scale investments, OEM collaborations and commercialization milestones. In November 2025, CATL brought online the world’s first 5 GWh all-solid-state battery production line in Hefei, positioning China at the center of solid-state manufacturing scale-up. The followed CATL’s October 2025 launch of the “Naxtra” sodium-ion battery, delivering 175 Wh/kg with strong −40°C performance, clearly targeted at cold-climate EVs and cost-sensitive segments. In May 2025, CATL’s 500 Wh/kg semi-solid-state battery entered mass production and began equipping Li Auto’s MEGA flagship EV, providing a real-world validation of ultra-high energy density cells in commercial vehicles rather than just demonstration packs. In parallel, SVOLT’s July 2025 announcement that its 300 Wh/kg semi-solid-state batteries will power future BMW Mini models from 2027 signals that European OEMs are also committing to semi-solid platforms as part of their electrification roadmap.

The ecosystem for solid-state and lithium-metal batteries is likewise consolidating. In October 2025, QuantumScape began shipping B1 QSE-5 anode-less lithium-metal cell samples to major automotive OEMs, including the VW Group and Ducati, marking a critical transition from lab-scale prototypes to OEM testing programs. That same month, Solid Power announced a Joint Evaluation Agreement with Samsung SDI and BMW, expanding its sulfide-based solid-state collaboration network beyond its early Ford ties and emphasizing compatibility with existing Li-ion production lines. In December 2024, QuantumScape launched “Cobra” heat-treatment equipment, designed to cut ceramic separator processing times by an order of magnitude, directly tackling the GWh-scale manufacturability bottleneck. On the strategic investment side, ProLogium secured environmental and construction permits in January 2025 for its €5.2 billion 48 GWh solid-state gigafactory in Dunkirk, France (production from 2027), underscoring Europe’s push to localize high-value battery IPCEI projects.

Beyond solid-state and sodium-ion, the next generation advanced batteries market is also shaped by extreme-fast-charging lithium-ion innovations and capital market developments. In December 2025, StoreDot agreed to a business combination at a USD 882 million pro-forma enterprise value, aimed at accelerating commercialization of its Extreme Fast Charging (XFC) silicon-anode batteries, engineered to deliver “100 miles in 3 minutes” charging targets. Meanwhile, SVOLT is preparing a 2.3 GWh semi-solid production line with volume deliveries from 2026, alongside a roadmap to 400 Wh/kg semi-solid and all-solid cells for eVTOL applications, underlining the market’s extension into aerospace and low-altitude aviation. Collectively, these developments indicate that from 2025–2027, the landscape will be defined by multi-chemistry portfolios (semi-solid, sodium-ion, all-solid, XFC Li-ion), with OEMs hedging technology risk and suppliers racing to demonstrate bankable performance, scale and cost trajectories.

For OEMs and cell manufacturers, the key question is no longer “if” these chemistries will scale, but which technology delivers bankable energy density, fast charging, cycle life and USD/kWh targets for EVs and grid storage. Semi-solid cells already demonstrate 500 Wh/kg, enabling >1,000 km premium EV range, while sodium-ion batteries at 175 Wh/kg with 10,000 cycles are redefining cost and resource risk for ESS and entry-level EV platforms. Further, industry roadmaps are converging on USD 70/kWh all-solid-state cell cost as the inflection point for parity with mature liquid Li-ion, supported by 43.65 GWh of pilot solid-state capacity in China alone. Decision-makers are therefore evaluating next-generation batteries not as lab curiosities, but as near-commercial solutions that can de-risk lithium supply, unlock extreme fast charging and support diversified EV portfolios.

- Ultra-high energy density: Semi-solid-state batteries achieving 500 Wh/kg are enabling >1,000 km EV range, positioning them as a premium upgrade path beyond current NCM/LFP chemistries.

- Fast-charge capability: New solid-state lithium-metal cells showing 80% SoC in under 15 minutes at 5C directly address OEM range and charging anxiety and support high-throughput charging infrastructure strategies.

- Sodium-ion viability: 175 Wh/kg sodium-ion with 10,000-cycle life provides a compelling alternative to LFP for ESS and low-cost EVs, reducing reliance on critical lithium and nickel.

- Cost roadmaps: Manufacturers are targeting USD 70/kWh for all-solid-state cells, widely recognized as the critical cost-parity threshold versus mainstream liquid Li-ion for mass-market EV adoption.

- Industrialization scale: An aggregate 43.65 GWh of operational pilot solid-state capacity in China (2025) confirms that next-generation chemistries are transitioning rapidly from R&D to GWh-scale industrial manufacturing.

Trends & Opportunities: Silicon-Dominant Anodes, Sodium-Ion Scaling, Localized LFP Supply Chains, and Aviation-Certified Battery Platforms Reshape the Next Generation Advanced Batteries Market

Trend 1: Accelerated Transition to Silicon-Dominant Anodes to Break the Energy Density Ceiling in EV Batteries

Silicon-dominant anodes are emerging as the most strategically important technology for next-generation EV batteries, offering a dramatic uplift in energy density and high-rate charging performance compared to conventional graphite anodes. Global automotive and materials manufacturers are moving rapidly toward commercial-scale deployment.

Core developments underscoring this shift include:

- Gigawatt-scale silicon anode production is now underway, with Sila commissioning its new Moses Lake, Washington facility designed to deliver 2–5 GWh initially, with planned expansion to 250 GWh within five years, ensuring a domestic supply chain for premium EV batteries.

- Material-level capacity advantage, as silicon stores up to 10× more lithium than graphite, enabling commercially available Si-dominant anodes to deliver ~20% higher energy density than state-of-the-art graphite cells, directly increasing EV driving range.

- Strategic joint ventures, such as HS HYOSUNG Group’s €120 million investment with Umicore, signal industry-wide anticipation of 40% annual growth in silicon-based anode demand.

- Ultra-fast charging capabilities, with Si/C composite anodes demonstrating outstanding high-rate performance and stable cycling at 3000 mA g⁻¹, validating their readiness for EV fast-charging architectures.

The trend strongly indicates that silicon-dominant anodes will anchor the next performance leap in automotive lithium-ion batteries, unlocking higher range and shorter charging times.

Trend 2: Large-Scale Industrialization of Sodium-Ion Batteries as a Low-Cost, Safe Alternative for Energy Storage Systems

Sodium-Ion (Na-ion) batteries are rapidly emerging as a high-volume commercial technology for stationary energy storage systems (ESS), driven by cost advantages, supply security, and thermal safety improvements over lithium-ion.

Key growth drivers include:

- Massive GWh-scale capacity buildouts, such as BYD’s 30 GWh/year sodium-ion plant and Guangde Qingna Technology’s 20 GWh Na-ion project backed by CNY 6 billion, accelerating global availability of Na-ion ESS solutions.

- Safety and thermal stability superiority, as sodium-based cathodes and electrolytes exhibit inherently lower fire risk-an essential requirement for residential, commercial, and grid-scale deployments.

- Lower raw material exposure, since sodium is abundant in seawater and mineral deposits, ensuring predictable cost structures and mitigating lithium price volatility.

- Manufacturing line compatibility, as Na-ion production can be integrated into existing lithium-ion gigafactories with minimal modification, significantly reducing capex and enabling rapid commercialization.

This trend positions sodium-ion batteries as a cost-efficient, resource-secure platform for next-decade grid storage and indoor ESS installations.

Opportunity 1: Localized LFP Cathode Active Material (CAM) Production in the U.S. and Europe to Capture IRA and EU Incentives

A global race is underway to localize production of Lithium Iron Phosphate (LFP) Cathode Active Material (CAM)-one of the highest-growth segments in the battery supply chain. U.S. IRA incentives and EU industrial policies are catalyzing unprecedented investment into domestic cathode manufacturing.

Key opportunity drivers include:

- IRA’s Advanced Manufacturing Production Tax Credit (AMPTC) offering a 10% production credit for electrode active materials, cutting the cost curve by ~$45/kWh for U.S.-produced LFP CAM.

- European upstream capacity expansion, led by Northvolt, which has secured ≈$8 billion in investment since 2017 to strengthen Europe’s cathode material and battery cell manufacturing footprint, including the Northvolt Fem LFP facility.

- Severe supply chain imbalance, with Europe producing only ~3% of global cathode material and North America producing <1%, despite 1.2 TWh of planned U.S. gigafactory capacity under development.

- DOE funding of $3.5 billion earmarked specifically for U.S. battery manufacturing and materials processing, boosting incentives for new LFP CAM plants.

Given skyrocketing demand for IRA-compliant EV batteries and EU domestic supply chain autonomy, localized LFP CAM production represents one of the most financially attractive and strategically urgent opportunities in the battery ecosystem.

Opportunity 2: Aviation-Certified Battery Supply Chains for eVTOL and Next-Generation Electric Aircraft

Electric Vertical Take-Off and Landing (eVTOL) aircraft are approaching commercial certification, creating a high-margin, safety-critical vertical for advanced battery suppliers capable of meeting stringent aviation requirements.

Key technical and commercial drivers include:

- High specific energy baseline, with eVTOL developers requiring ≥230 Wh/kg to achieve ~100-mile operational range, while next-generation aviation battery programs target up to 500 Wh/kg at the cell level.

- High-rate discharge capability, with eVTOL propulsion demanding up to 5C or greater power bursts during takeoff, climb, and landing, placing extreme stress on battery chemistry and thermal management.

- Stringent aviation safety testing, including compliance with UN 38.3 thermal runaway, vibration, altitude, and impact tests, drastically limiting the pool of qualified battery suppliers.

- Exclusive OEM partnerships, such as CATL’s collaboration with AutoFlight to develop a next-generation eVTOL battery system engineered for the industry's longest continuous flight duration.

This opportunity creates a new premium supply chain segment where qualified battery partners can gain long-term locked-in contracts with aviation manufacturers-similar to the early days of EV battery supplier agreements.

Next Generation Advanced Batteries Market Share Analysis

Market Share by Material Type: Silicon Anodes Lead Through Unmatched Storage Capacity, High Energy Density Gains, and Manufacturing Compatibility

Silicon anodes command the leading 45% share of the Next Generation Advanced Batteries Market because they represent the fastest, most commercially viable pathway to unlocking higher energy density, the single most important performance metric for modern battery technologies. Unlike emerging chemistries that require entirely new production ecosystems, silicon—especially in silicon-carbon composite forms—offers a dramatic leap in lithium storage capacity while maintaining compatibility with today’s lithium-ion manufacturing processes. Silicon’s theoretical capacity of ~3,600 mAh/g, nearly 10× higher than graphite, directly translates into next-generation lithium-ion and solid-state batteries capable of 20%–50% higher energy density, enabling longer EV driving range and extended device runtime without increasing pack size or weight. These characteristics align perfectly with market drivers centered on maximizing energy output per kilogram and per liter. Moreover, silicon’s manufacturability advantage is a critical share accelerator; engineered composites successfully mitigate volumetric expansion issues, allowing seamless integration into existing electrode coating, calendaring, and cell assembly lines. This minimizes retooling costs and shortens the commercialization timeline, giving silicon anodes a decisive lead over alternative high-capacity materials such as lithium–sulfur or metal–air systems. As OEMs prioritize rapid scaling, cost reduction, and incremental performance gains with minimal disruption, silicon anode technology remains the dominant material segment shaping the next-generation battery roadmap.

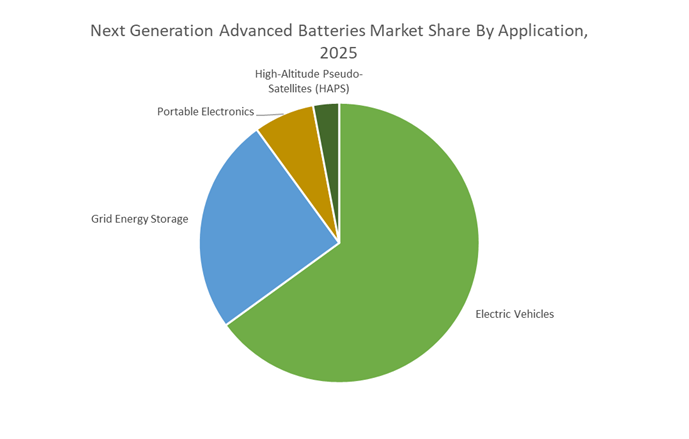

Market Share by Application: Electric Vehicles Dominate as Next-Generation Batteries Enable Range Extension, Fast Charging, and Multi-TWh Demand Growth

The Electric Vehicles (EV) segment holds the highest 65% share of the Next Generation Advanced Batteries Market because EV platforms exert the most intense pressure on the industry to deliver higher energy density, faster charging capability, and lower cost-per-mile—all areas where silicon-enhanced and next-generation battery architectures deliver transformative advantages. As EV adoption accelerates globally, OEMs require batteries that extend range without increasing pack size; silicon-rich anodes directly support this need by enabling 10%–20% range increases, meaning a 300-mile EV could gain an extra 30–60 miles without any change in pack footprint. This performance uplift directly addresses consumer concerns around range anxiety, making silicon-enabled batteries a strategic differentiator for automakers. The scale of EV adoption also drives unmatched volume demand: global EV battery installations surpassed 900 GWh in 2024, with projections exceeding 3 TWh by 2030, making EVs the largest and fastest-growing consumption base for all advanced battery materials.

Next-generation batteries are also indispensable for achieving extreme fast charging (XFC), a core requirement for mass EV adoption. Silicon-based chemistries can accommodate higher charging currents with reduced lithium plating risk, enabling targets such as 80% charge in 15 minutes or less—a benchmark critical for replicating the convenience of conventional refueling. Automakers and cell manufacturers are aggressively pursuing silicon integration to meet these performance goals while simultaneously reducing pack cost via higher energy density. As fast-charging infrastructure scales globally and regulatory pressure increases to phase out combustion engines, EV manufacturers continue to prioritize next-generation battery technologies, solidifying EVs as the dominant application driving market share and long-term commercialization momentum.

Country Analysis: Global Advanced Battery Innovation and Manufacturing Hubs

China – Sodium-Ion Commercialization Leadership and Accelerated Solid-State Battery Pilot Scale-Up

China dominates the Next Generation Advanced Batteries Market, spearheading global industrialization of Sodium-Ion (Na-ion) batteries and rapidly scaling pilot production for Solid-State Batteries (SSBs). The country’s leadership is fueled by strong state-backed financing, vertically integrated supply chains, and unmatched deployment speed across EV and grid-scale applications. CATL’s breakthrough Naxtra sodium-ion battery—with an energy density of 175 Wh/kg, comparable to LFP—marks a pivotal milestone by enabling over 500 km EV range, validating Na-ion as a competitive, low-cost chemistry for mainstream mobility. Simultaneously, BYD’s construction of a 30 GWh/year Sodium-Ion Gigafactory in Xuzhou demonstrates aggressive industrial scaling, aligning with national strategies to diversify battery chemistries beyond lithium.

China is also pioneering large-scale Na-ion deployment. HiNa Battery supplied the world’s largest 100 MWh sodium-ion energy storage plant in Nanning (July 2024), signaling commercial readiness for high-cycle, stationary grid storage. China’s parallel investment in solid-state battery technologies is equally transformative. GAC Group commissioned a pilot line in 2025 targeting >400 Wh/kg solid-state cells, while MIIT initiated a mid-term review of its 6 billion yuan national SSB development initiative, accelerating technology transfer toward mass production. Infrastructure integration is progressing rapidly, highlighted by the successful grid connection of a 200 MW/800 MWh semi-solid-state energy storage station in Wuhai, achieving a cycle life of 12,000 cycles and setting new global benchmarks for long-duration ESS reliability.

United States – Solid-State Lithium-Metal Battery Commercial Milestones and Deep Federal R&D Support

The United States is shaping the global Solid-State Lithium-Metal Battery (SSB) landscape through a combination of venture-backed innovation, national laboratory R&D, and strategic OEM collaboration. QuantumScape’s shipment of B1 QSE-5 solid-state sample cells in October 2025 marks one of the sector’s most significant commercial milestones. The technology’s 844 Wh/L volumetric energy density positions it as a next-generation solution for long-range EVs and high-performance mobility applications. Concurrently, QuantumScape’s highly automated Eagle Line pilot production facility in San Jose is a crucial step toward scaling to gigawatt-hour production, introducing advanced separator manufacturing processes aimed at lowering cost and improving yield.

Durability validation remains a major U.S. advantage. Early 2024 testing of the QuantumScape–Volkswagen prototype cell demonstrated >1,000 cycles with only ~5% capacity fade, confirming suitability for 300,000–500,000 km EV lifespans. U.S. collaboration continues to deepen: Solid Power’s Joint Evaluation Agreement with BMW and Samsung SDI positions its sulfide-based solid electrolyte as a key material candidate for next-generation EV batteries. Federal support is extensive, with multi-year funding through DOE and national labs emphasizing separator stability, lithium-metal interface engineering, and manufacturability—solidifying the United States as a foundational hub for SSB commercialization.

Europe (Germany/France) – Automotive-Driven Solid-State Integration and Sodium-Ion Pilot Line Expansion

Europe’s strategic ambition to localize advanced battery manufacturing under the EU Green Deal and Net Zero Industrial Act (NZIA) is reshaping the region’s position within the global battery supply chain. Germany’s automotive sector continues to lead integration efforts, exemplified by BMW’s deployment of a Solid Power–based solid-state battery prototype in an i7 test vehicle (Q2 2025). This milestone transitions Europe from laboratory-scale demonstrations to automotive-grade field validation, a critical requirement for establishing a competitive European SSB ecosystem.

Europe is also positioning itself as a significant innovation hub for alternative chemistries, including Lithium-Sulfur (Li-S) batteries, where the Fraunhofer IWS plays a central role in developing high-energy cathode architectures and sulfur stabilization techniques. Sodium-ion momentum is accelerating as well, with new Na-ion pilot plant investments across Germany and France, focusing on cost-sensitive stationary storage markets where sodium’s abundance and low price offer a structural advantage. These initiatives collectively strengthen Europe’s long-term energy sovereignty, reduce dependency on imported lithium, and support competitive European manufacturing of advanced battery technologies.

Japan – Miniaturized All-Solid-State Production and Ultra-Fast Charging Breakthroughs

Japan remains a global stronghold in materials science and precision battery engineering, focusing particularly on miniaturized all-solid-state batteries (ASSBs) for electronics, drones, robotics, and eventually electric vehicles. Panasonic’s roadmap to commercialize small-format all-solid-state batteries between 2025 and 2029 represents one of the industry’s most ambitious manufacturing commitments. Target performance metrics—including 80% charging in 3 minutes and cycle life exceeding 30,000 cycles—position Japan at the forefront of ultra-fast-charging innovation. These attributes are essential for drone logistics, autonomous systems, and high-end consumer electronics, where power density and rapid charging dramatically improve functionality.

Japan’s automotive sector is pursuing parallel advancements. Toyota’s SSB prototype, undergoing road testing in 2025, aims for 1,200 km driving range on a single rapid charge, redefining EV performance benchmarks. Toyota’s approach combines high-capacity cathode development, proprietary solid electrolyte engineering, and improved lithium-metal interface stability—advancing Japan’s long-term goal of mass-market SSB commercialization. As Japanese firms continue leveraging global partnerships and strong domestic R&D ecosystems, the country strengthens its position as a high-precision hub for emerging battery technologies.

Competitive Landscape: Strategic Positioning of Leading Next-Gen Battery Players

The Next Generation Advanced Batteries Market is dominated by a mix of Asian cell majors and Western solid-state specialists, each leveraging differentiated chemistries and business models. Competitive advantage is increasingly determined by vertical integration, multi-chemistry roadmaps, access to automotive platforms, and the ability to industrialize novel materials at GWh scale. While Chinese leaders like CATL and SVOLT are already mass-producing semi-solid and sodium-ion cells, U.S. and European players including QuantumScape, Solid Power and ProLogium are focused on high-energy all-solid-state architectures and licensing-driven expansion. Further, StoreDot is carving out a niche around Extreme Fast Charging (XFC) solutions compatible with existing Li-ion production assets, allowing OEMs to upgrade performance without rebuilding gigafactory infrastructure.

CATL remains the central force in next generation advanced batteries, combining 500 Wh/kg semi-solid-state, all-solid-state pilot lines, and sodium-ion Naxtra cells in a unified portfolio. Its 500 Wh/kg semi-solid batteries, in mass production since May 2025, already power the Li Auto MEGA, demonstrating commercial feasibility at pack scale. In October 2025, the company launched Naxtra sodium-ion, achieving 175 Wh/kg with superior low-temperature performance for northern-region EVs and ESS. By November 2025, CATL commissioned the world’s first 5 GWh all-solid-state production line in Hefei, consolidating its position as a frontrunner in solid-state industrialization. CATL’s strategic roadmap is clearly multi-chemistry, targeting USD 70/kWh cost levels across solid-state platforms and leveraging its integration with automotive OEMs to deploy fast-charge-ready packs.

QuantumScape’s competitive strength lies in its anode-less lithium-metal solid-state cell design and proprietary ceramic electrolyte separator, engineered for high energy density and robust fast-charge performance. In December 2024, the company introduced Cobra, a next-gen heat-treatment system to scale production of its ceramic separator, reducing processing time by roughly an order of magnitude and addressing a key manufacturing bottleneck. By October 2025, QuantumScape began shipping B1 QSE-5 prototype cells to major OEM partners, including the VW Group and Ducati, marking a shift from lab validation to real vehicle testing. Its cells are aimed at premium and performance EVs that require high voltage, high power and durable 5C charge/discharge operation. QuantumScape’s strategy centers on proving cycle life, safety and manufacturability at GWh scale, paving the way toward A-sample and eventual series production.

Solid Power differentiates itself with a sulfide-based all-solid-state electrolyte designed to be compatible with conventional Li-ion roll-to-roll equipment, enabling an easier transition for existing gigafactories. Its strategic model emphasizes licensing and joint development rather than only owning large-scale cell manufacturing assets. In October 2025, Solid Power signed a Joint Evaluation Agreement with Samsung SDI and BMW, expanding its network of automotive partners beyond Ford and validating the global interest in its electrolyte technology. The company is moving toward commissioning a continuous electrolyte production pilot line by 2026, a crucial upstream milestone for stable supply. With a disciplined cash investment plan of USD 85–95 million in 2025, Solid Power is focused on capital-efficient scaling to A-sample qualification, positioning its sulfide electrolyte as a drop-in enabler for multiple OEM cell formats.

ProLogium has emerged as a leading lithium-ceramic solid-state battery player, emphasizing fully inorganic electrolytes and high energy density. At CES 2025, it unveiled its fourth-generation Lithium-Ceramic Battery (LCB) with an energy density around 380 Wh/kg, targeting high-range EVs and premium mobility applications. The company already operates a GWh-scale demonstration plant in Taiwan (since 2024) and has shipped over 500,000 cells to customers, demonstrating repeatable mass producibility. In January 2025, ProLogium secured environmental and construction permits for a €5.2 billion, 48 GWh solid-state gigafactory in Dunkirk, France, backed by around €1.5 billion in government support, anchoring the EU’s solid-state industrial ambitions. Its strategy combines regional diversification (Asia + Europe) with direct engagement with major OEMs, leveraging a robust IP portfolio around ceramic electrolytes and stacking technologies.

StoreDot is positioning itself as the XFC (Extreme Fast Charging) specialist in the next-generation battery landscape, focusing on silicon-dominant anode chemistries that can deliver “100 miles of range in 3 minutes” targets. Its technology is explicitly designed as a drop-in solution for existing Li-ion gigafactories, enabling partners to upgrade performance without fully retooling plants—an attractive proposition for OEMs under capex pressure. In December 2025, StoreDot finalized a business combination valued at USD 882 million, providing the capital needed to ramp commercialization and global partnerships. The company is working toward mass production of XFC cells from 2025 onward, with an emphasis on meeting OEM criteria for cycle life, safety and fast-charge durability. StoreDot’s core strategic focus is eliminating range and charging anxiety to support widespread EV adoption, especially in high-utilization fleets and premium segments.

SVOLT Energy Technology is emerging as a significant semi-solid-state and next-gen Li-ion manufacturer with strong ties to global OEMs. Its first-generation semi-solid-state cells, delivering around 270–300 Wh/kg, have already secured a Tier-1 supply deal to power future BMW Mini models, with mass supply planned from 2027. By July 2025, SVOLT confirmed the BMW partnership, underscoring European OEM trust in its technology. The company operates a dedicated 2.3 GWh semi-solid production line, with commercial deliveries targeted for 2026, and is developing second-generation semi-solid cells targeting 400 Wh/kg. Beyond automotive, SVOLT’s roadmap includes all-solid-state batteries tailored for low-altitude aviation and eVTOL platforms, reflecting a broader strategy to serve high-energy, high-safety aerospace applications.

Next Generation Advanced Batteries Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.4 Billion

|

|

Market Size (2035)

|

$4.9 Billion

|

|

Market Growth Rate

|

7.5%

|

|

Segments

|

By Chemistry (Solid-State Batteries, Sodium-Ion Batteries, Lithium-Sulfur Batteries, Lithium-Air Batteries, Anode-Free Lithium-Metal Batteries), By Electrolyte State (All-Solid-State, Semi-Solid-State, Solid-State Polymer Electrolytes, Aqueous Batteries), By Material Type (Solid Electrolytes, Hard Carbon, Silicon Anodes, Sulfur Cathodes), By Application (Electric Vehicles, Grid Energy Storage, High-Altitude Pseudo-Satellites, Portable Electronics & Wearables)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

CATL, QuantumScape Corporation, Toyota Motor Corporation, BYD Company Ltd., Solid Power Inc., GAC Group, Farasis Energy, HiNa Battery Technology Co. Ltd., StoreDot, Sion Power Corporation, LG Energy Solution, SK On Co. Ltd., Panasonic Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Next Generation Advanced Batteries Market Segmentation

By Chemistry

- Solid-State Batteries (SSB)

- Sodium-Ion (Na-ion) Batteries (SIB)

- Lithium-Sulfur (Li-S) Batteries

- Lithium-Air (Li-Air) Batteries

- Anode-Free Lithium-Metal Batteries

By Electrolyte State

- All-Solid-State (Ceramic/Polymer/Sulfide)

- Semi-Solid-State (Hybrid Electrolyte)

- Solid-State Polymer Electrolytes

- Aqueous Batteries

By Material Type

- Solid Electrolytes (Garnet, Sulfide, Oxide)

- Hard Carbon (Na-ion Anode)

- Silicon Anodes (Next-Gen Li-ion/SSB)

- Sulfur Cathodes (Li-S)

By Application

- Electric Vehicles (EV)

- Grid Energy Storage

- High-Altitude Pseudo-Satellites (HAPS)

- Portable Electronics/Wearables

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: Key Next Generation Advanced Batteries Developers

- Contemporary Amperex Technology Co. Limited (CATL)

- QuantumScape Corporation

- Toyota Motor Corporation

- BYD Company Ltd.

- Solid Power, Inc.

- GAC Group (Guangzhou Automobile Group)

- Farasis Energy

- HiNa Battery Technology Co., Ltd.

- StoreDot

- Sion Power Corporation

- LG Energy Solution (LGES)

- SK On Co., Ltd.

- Panasonic Corporation

*- List not Exhaustive