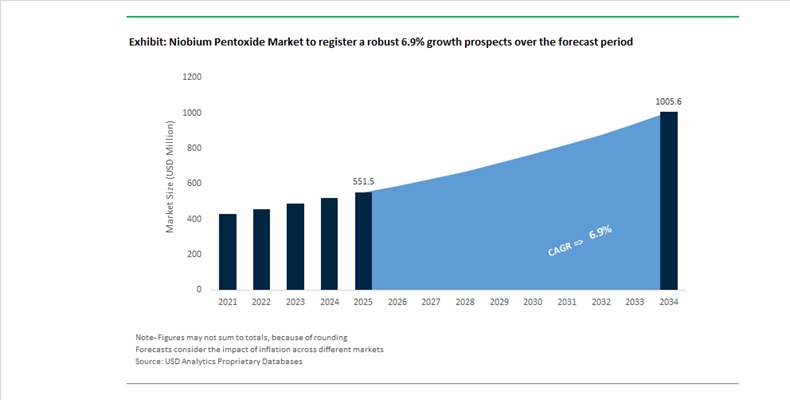

Niobium Pentoxide Market Valued at $551.5 Million in 2025 to Surpass $1,005.4 Million by 2034 at 6.9% CAGR

The Niobium Pentoxide (Nb₂O₅) Market is valued at $551.5 Million in 2025 and is projected to reach $1,005.4 Million by 2034, expanding at a robust CAGR of 6.9%. Market growth is being redefined by battery-grade niobium oxide demand, strategic defense integration, and accelerated upstream resource development. Traditionally dominated by ferroniobium for high-strength low-alloy (HSLA) steels, the value chain is now shifting toward high-purity Nb₂O₅ for lithium-ion battery anodes, advanced ceramics, optical coatings, and aerospace superalloys.

In June 2025, Toshiba Corporation began sample shipments of its SCiB™Nb rechargeable lithium-ion battery, the first commercial cell utilizing a Niobium Titanium Oxide anode. Developed in partnership with CBMM and Sojitz Corporation, the battery achieves 80% charge in 10 minutes and exceeds 15,000 charge cycles. This milestone establishes Nb₂O₅-derived materials as credible alternatives to graphite and LTO in heavy-duty commercial EVs, automated guided vehicles, and industrial robotics. The deployment validates years of pilot-scale oxide optimization and signals a structural increase in battery-grade niobium consumption.

Supply-side expansion accelerated in 2024. In Q2 2024, CBMM announced a 15% capacity expansion at its Brazilian facilities to address rising demand for high-purity niobium oxide in electronics and battery applications. In November 2024, Echion Technologies inaugurated a 2,000-tonne-per-year XNO® mixed niobium oxide production facility within CBMM’s Araxá complex. Earlier in June 2024, Echion raised £29 million in Series B funding led by Volta Energy Technologies to commercialize XNO® globally. In September 2024, Leclanché SA launched the first commercial lithium-ion cell integrating XNO® technology, targeting marine propulsion and rail electrification. These developments establish multi-thousand-ton annual output for battery-grade Nb₂O₅, transitioning the market from laboratory-scale to industrial-scale deployment.

Geopolitical resource diversification intensified in 2025. In June 2025, Kazakhstan announced the discovery of the Kuirektikol deposit in Karagandy Oblast, estimated at over 20 million metric tons of rare metal resources including niobium. If confirmed, Kazakhstan could emerge as the third-largest global reserve holder after Brazil and China. In the United States, NioCorp Developments Ltd. reported a record $307 million consolidated cash balance in 2025, advancing the Elk Creek Project in Nebraska toward an Independent Technical Review by EXIM Bank. In 2025, NioCorp also acquired scandium alloy manufacturing assets from FEA Materials to support domestic aluminum-scandium-niobium master alloy production for aerospace and defense. Parallel to this, Globe Metals secured non-binding offtake agreements in early 2025 covering 82% of Phase 1 Nb₂O₅ output from its Kanyika Project in Malawi, with binding agreements expected by September 2025 and deliveries scheduled for May 2026.

Defense and high-temperature applications remain structurally important. In 2024, the U.S. Department of Defense confirmed integration of niobium-based superalloys into hypersonic flight platforms capable of Mach-5+ environments. Nb₂O₅-derived alloys are prioritized for thermal stability and oxidation resistance under extreme aerodynamic stress, reinforcing niobium’s classification as a strategic material. This dual demand from battery electrification and defense superalloys strengthens pricing power and secures long-term offtake contracts.

In 2025, circular economy initiatives entered early validation phases. A collaboration between iCAST and Echion Technologies demonstrated chemical recycling pathways capable of recovering high-purity niobium oxide from spent battery anodes. The process converts end-of-life materials into refined niobium salts, creating a technically viable loop for battery-grade Nb₂O₅ regeneration. As giga-factory deployments scale globally, recycling integration is expected to become a key cost-control and sustainability lever across the niobium pentoxide supply chain.

Niobium Pentoxide (Nb₂O₅) Market Trends and Opportunities

Trend: Strategic Expansion and Geographic De-risking of Global Niobium Supply Chains

The niobium pentoxide market is entering a decisive phase of geographic diversification as governments and industrial consumers respond to long-standing concentration risks in global niobium supply. With niobium formally classified as a Critical Mineral across G7 economies, downstream users in aerospace, automotive, and advanced manufacturing are actively supporting upstream projects outside Brazil to secure long-term access to Nb₂O₅. Canada has emerged as a strategic anchor in this transition. In October 2025, the Canadian government announced a CAD 6.4 billion critical minerals investment framework, including conditional funding of up to CAD 36.3 million for refining and processing facilities in Ontario. These initiatives are designed to establish domestic niobium oxide conversion capacity, reducing reliance on imported intermediates while supporting battery-grade and aerospace specifications.

Africa represents the second major axis of diversification. The Kanyika Niobium Project in Malawi, being advanced by Globe Metals & Mining, is positioned as Africa’s first industrial-scale niobium operation. With an estimated capital commitment of USD 250 million and an engineered output of approximately 73,250 tonnes of niobium pentoxide over a 23-year mine life, Kanyika is expected to serve as a critical alternative supply source for European and Asian offtakers by 2028. Parallel to these developments, the world’s dominant producer is pivoting downstream. CBMM’s announced USD 1.7 billion investment program, targeting a doubling of sales volume by 2030, places strong emphasis on niobium oxide derivatives rather than solely ferroniobium. This strategic shift signals that Nb₂O₅ is transitioning from a niche chemical into a cornerstone material for next-generation energy, alloy, and electronics applications.

Trend: Accelerated Qualification of High-Purity Nb₂O₅ for Advanced Battery Architectures

Niobium pentoxide is rapidly gaining strategic relevance in the battery materials ecosystem, driven by its role in stabilizing high-energy-density cathodes and enabling next-generation solid-state batteries. High-purity Nb₂O₅ is increasingly being qualified as a surface coating and dopant for nickel-rich cathode chemistries, where interfacial instability has historically limited cycle life. Peer-reviewed research published in December 2025 demonstrates that niobium-modified NMC 9055 cathodes achieve 99.7% capacity retention after 200 cycles, compared to 75.3% for uncoated materials. This performance differential is material for automotive OEMs targeting battery lifetimes exceeding 1,000 cycles under fast-charging conditions.

Industrialization efforts are accelerating in parallel. CBMM’s NBXCELER™ program is scaling dedicated production assets for battery-grade niobium oxide, with multiple new plants scheduled to be operational by the end of 2025. The stated objective is to exceed 20 kilotonnes of Nb₂O₅ capacity by 2030, explicitly aligned with ultra-fast charging requirements, including six-minute charge targets for heavy-duty electric vehicles. Beyond conventional lithium-ion systems, Nb₂O₅ is being evaluated as a functional dopant in sulfide-based solid electrolytes. Recent laboratory and pilot-scale results indicate that niobate-phosphate hybrid coatings can sustain near-100% capacity retention over 1,000 cycles at ambient temperatures, positioning niobium pentoxide as a critical enabler for Gen-3 solid-state battery commercialization.

Opportunity: Niobium-Based Materials for Hydrogen Transport, Storage, and Purification

The global scale-up of hydrogen infrastructure presents a structurally attractive opportunity for niobium pentoxide and niobium-alloyed materials. Hydrogen embrittlement remains one of the most significant technical barriers to safe, high-pressure hydrogen transport, particularly in repurposed natural gas pipelines. High-Strength Low-Alloy steels containing up to 0.10% niobium are increasingly specified for API X80 and higher-grade pipelines, as they offer an optimal balance between mechanical strength and resistance to hydrogen-induced cracking. Industrial validation data confirms that niobium microalloying enables larger-diameter pipelines capable of handling hydrogen blending without compromising fracture toughness.

In parallel, Nb₂O₅ is emerging as a high-performance barrier coating material. Physical Vapor Deposition-based niobium oxide coatings act as dense, ceramic-like diffusion barriers that significantly reduce hydrogen permeation into steel substrates. These coatings are being evaluated for storage tanks, compressors, and transport vessels, where extended service life and reduced inspection frequency translate directly into lower total cost of ownership. A third, high-value avenue is hydrogen purification. Niobium-based permeable membranes, developed using magnetron sputtering and solid-solution engineering, are demonstrating competitive hydrogen flux and corrosion resistance at operating temperatures approaching 550°C. Compared with palladium-based membranes, niobium solutions offer a materially lower cost structure, making them attractive for large-scale hydrogen separation and refining systems.

Opportunity: High-Refractive-Index Optical Materials for AR/VR and LIDAR Systems

Niobium pentoxide occupies a strategically important position in advanced optics, particularly as demand accelerates for compact, high-performance components in AR, VR, and autonomous vehicle sensing systems. With a refractive index of approximately 2.4 at 550 nm and low chromatic dispersion, Nb₂O₅ enables the design of thinner, lighter optical elements without sacrificing image quality. This characteristic directly addresses one of the primary adoption barriers in consumer AR and VR devices, where headset weight and form factor remain critical constraints.

In automotive applications, Nb₂O₅ thin films are increasingly incorporated into diffractive optical elements used in LIDAR modules. These films enhance diffraction efficiency and signal clarity, supporting long-range detection accuracy required for Level 3 and Level 4 autonomous driving systems. Optical research published in 2025 highlights niobium pentoxide as a preferred platform for achieving high-efficiency diffractive optics under harsh thermal and environmental conditions. Beyond LIDAR, demand is rising for high-purity Nb₂O₅ in lanthanum borate glasses used for antireflection coatings and electrochromic devices. Its optical transparency across the UV–visible spectrum, combined with superior environmental stability, is driving substitution away from titanium dioxide in premium optical glass manufacturing, reinforcing niobium pentoxide’s role as a critical material in next-generation photonics and sensing technologies.

Niobium Pentoxide Market Share and Segmentation Insights

Industrial Grade Niobium Pentoxide Leads Market Through Alloy Production and Steel Microalloying Demand

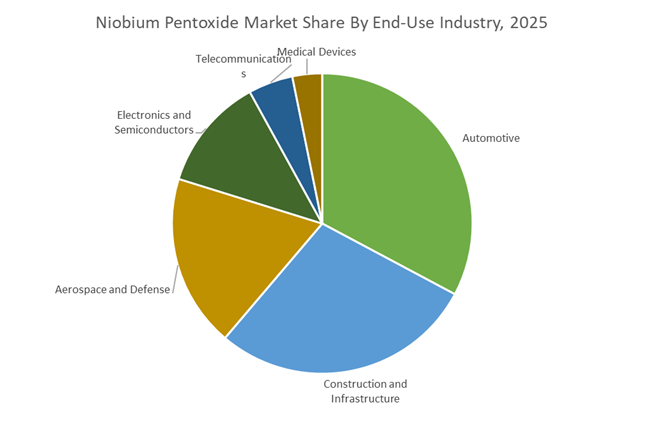

Industrial grade niobium pentoxide accounted for 58.60% of the Niobium Pentoxide Market share in 2025, making it the most widely consumed grade within the global niobium materials industry. Industrial grade niobium pentoxide is primarily used in the production of ferroniobium alloys, which are critical alloying additives in high-strength low-alloy (HSLA) steels and superalloys. These advanced steels are widely utilized in automotive structures, construction materials, pipelines, and heavy industrial equipment, where niobium enhances mechanical strength, weldability, and corrosion resistance while enabling thinner and lighter steel components. Because ferroniobium production requires large quantities of niobium pentoxide but does not demand ultra-high purity, industrial grade material offers the most cost-effective feedstock for large-scale metallurgical processes. In 2025, while industrial grade continues to dominate overall consumption, high-purity niobium pentoxide is emerging as a rapidly expanding segment, driven by applications in optical lenses, electronic components, piezoelectric devices, and advanced energy storage materials, where higher purity levels significantly influence product performance and value.

Automotive Industry Drives the Largest Demand for Niobium Pentoxide

Automotive accounted for 32.80% of the Niobium Pentoxide Market share in 2025, making vehicle manufacturing the largest end-use sector for niobium-based materials. Niobium plays a crucial role in producing high-strength low-alloy (HSLA) steels used in vehicle chassis, body structures, suspension components, and safety reinforcement systems. By adding small amounts of niobium to steel, manufacturers can significantly improve strength-to-weight ratio, fatigue resistance, and formability, enabling the production of lighter vehicle structures without compromising safety performance. Automotive manufacturers increasingly adopt these advanced steels as part of broader vehicle lightweighting strategies aimed at improving fuel efficiency and extending electric vehicle driving range. In 2025, the transition toward electric vehicle (EV) platforms is also expanding the range of niobium-based applications within the automotive sector. Emerging technologies include niobium-enhanced battery anodes for fast-charging lithium-ion batteries, niobium oxide coatings used in sensors and electronic components, and lightweight niobium alloys for specialized automotive parts, creating new demand channels beyond traditional steel microalloying applications.

Niobium Pentoxide Market Competitive Landscape

The niobium pentoxide market in 2026 is driven by fast-charging battery anode commercialization, high-purity oxide demand, and critical mineral supply diversification. Competitive advantage centers on vertical integration, battery-grade Nb₂O₅ production, and geopolitical positioning to support EV, aerospace, and energy transition applications.

CBMM leads battery-grade niobium oxide scale-up and non-steel revenue diversification

CBMM remains the dominant force in the niobium pentoxide market, leveraging its Araxá reserves and full value chain integration. The company commissioned a 2,000-tonne/year battery-grade oxide facility, supporting ~1 GWh of EV battery production. Its NBXCELER™ portfolio is driving adoption in fast-charging anodes and cathode doping applications. CBMM is targeting 30% revenue from non-steel applications by 2030, reflecting a strategic pivot toward energy storage. With three industrial plants operational in 2026 and validated performance in electric mobility, it is scaling global offtake agreements. Its cost leadership and R&D partnerships underpin its market dominance.

CMOC strengthens high-purity niobium oxide output through multi-metal integration strategy

CMOC Group is expanding its niobium pentoxide footprint through its “Multi-Metal Synergies” model, integrating niobium with molybdenum and cobalt operations. Its Brazilian assets are undergoing upgrades to improve recovery rates and increase output of high-purity 3N (99.9%) Nb₂O₅, which accounted for over 67% of global demand in 2025. The company’s diversified portfolio enables bundled supply solutions for aerospace, electronics, and defense sectors. Strong ESG-aligned operations, including water recycling and tailings management, support sustainable production. Record 2025 output highlights operational resilience across its global mining network. CMOC’s scale and integration strengthen its position in specialty oxide markets.

NioCorp advances U.S. niobium supply chain with Elk Creek project and defense-grade alloy development

NioCorp Developments is a key catalyst for North American niobium supply chain localization through its Elk Creek Project in Nebraska. The company initiated a US$44.6 million construction phase in 2026, supported by approximately US$500 million in funding, including U.S. Department of Defense backing. Its designation under critical mineral programs accelerates development and financing pathways. NioCorp is collaborating with Lockheed Martin to develop niobium-enhanced and aluminum-scandium alloys for aerospace applications. This positions the company at the intersection of defense, lightweight materials, and energy transition supply chains. Its focus on domestic production strengthens geopolitical resilience in niobium supply.

AMG builds circular niobium recovery and high-purity processing capabilities for aerospace applications

AMG Critical Materials is redefining its role through circular economy integration and high-purity oxide processing. Its acquisition of AURA Technologie enables recovery of niobium and molybdenum from spent catalysts, creating a closed-loop supply chain. The company reported US$235 million EBITDA in 2025, reflecting strong growth in specialty materials. Its new U.S. facility, launching in 2026, will focus on high-purity oxides for aerospace and superalloy applications. AMG’s capital-light strategy emphasizes high-return projects and proprietary refining technologies. This approach positions it as a key supplier in sustainable and onshored critical material ecosystems.

Ioneer expands U.S. critical mineral production with high-efficiency extraction and battery supply integration

Ioneer Ltd. is emerging as a strategic supplier within the North American battery materials ecosystem through its Rhyolite Ridge project. Backed by a US$996 million DOE loan, the project entered commercial production in 2026, emphasizing sustainable extraction. Process optimization has reduced leach time by 50%, increasing output capacity by 28%. Its integrated production of boric acid complements niobium applications in optical glass and advanced ceramics. Ioneer is securing long-term offtake agreements to anchor its position in the U.S. “Battery Belt.” Its multi-mineral strategy enhances supply chain resilience for energy transition materials.

Brazil: From Mineral Dominance to Battery-Grade Niobium Industrialization

Brazil sits at the strategic core of the global niobium pentoxide market, driven by its unmatched resource base and the deliberate downstream expansion led by CBMM. The commissioning of the world’s first industrial-scale niobium oxide refining facility in Araxá during late 2024 marked a structural inflection point for the market. With a dedicated capacity of 3,000 tonnes per annum of battery-grade Nb₂O₅, the facility positions Brazil not merely as a raw material exporter but as a critical processor of advanced energy materials. This shift directly supports lithium-ion battery cathode and anode value chains, where purity, consistency, and scalability are decisive procurement criteria.

Brazil’s battery strategy accelerated further with the November 2024 inauguration of the XNO™ anode production facility, developed jointly with Echion Technologies. With an annual output of 2,000 tonnes, equivalent to roughly 1 GWh of lithium-ion cell capacity, this plant demonstrates the commercial viability of niobium-based fast-charge battery chemistries. CBMM’s deployment of mixed niobium-titanium oxide batteries in electric buses, capable of ultra-fast 10-minute charging, reinforces the relevance of niobium pentoxide in high-duty urban transit systems. Financially, CBMM’s 2025 outlook confirms a decisive revenue rebalancing, with battery-related niobium products projected to rise to 25% of total revenues by 2030. This transition is underpinned by a dedicated R256 million capital allocation in 2025 for mixed oxide plants, signaling Brazil’s move from pilot-scale innovation to mass-market supply leadership.

United States: Supply Chain Security and Ultra-High Purity Positioning

The United States niobium pentoxide market is defined by strategic vulnerability and policy-driven localization. The September 2024 Department of Defense award of $26.4 million to establish the first domestic high-purity niobium oxide facility in Pennsylvania reflects growing concern over aerospace and defense supply chain resilience. This initiative directly addresses reliance on imported oxides for mission-critical applications, including turbine blades, hypersonic systems, and rocket propulsion components that require 4N and 5N purity grades.

Federal urgency intensified in 2025 when the USGS reaffirmed niobium’s critical mineral status, even as domestic consumption declined by 8% in 2024. This paradox has sharpened focus on structural supply risk rather than short-term demand cycles. The Elk Creek Project in Nebraska stands at the center of this response. By November 2025, NioCorp Developments had secured all major permits and contracted 75% of its planned long-term production, pending final financing. Concurrently, the aerospace sector, which accounts for over one-fifth of U.S. niobium consumption, is actively pushing tighter purity specifications to support next-generation thermal and mechanical performance requirements. As a result, the U.S. market is evolving toward smaller-volume, ultra-high-purity niobium pentoxide streams with defense-grade traceability rather than bulk oxide consumption.

Canada: Strategic Balancing Through Resource Optionality

Canada plays a stabilizing role in the global niobium pentoxide market by offering geopolitical and geological diversification. The Niobec mine in Quebec remains the only significant producing niobium asset in North America, continuing to supply ferro-niobium and specialty oxides for defense and advanced manufacturing applications in 2025. Its operational continuity provides a critical counterbalance to Brazil’s dominance, particularly for Western buyers seeking supply redundancy.

Exploration and recovery initiatives are expanding Canada’s strategic optionality. Vital Metals’ March 2025 Tardiff Niobium Recovery strategy outlined a resource base containing 578,000 tonnes of niobium pentoxide, with an emphasis on advanced hydrometallurgical processing to handle complex ore bodies. Complementing this, Apex Critical Metals’ December 2025 discovery at the Cap Project in British Columbia identified a 1.8-kilometer niobium trend with high-grade intercepts exceeding 1 percent Nb₂O₅. These developments do not immediately alter supply volumes but materially strengthen Canada’s medium-term positioning as a secure source of refined niobium pentoxide for defense-aligned and clean-energy applications.

China: Volume Leadership Under Export Constraint Dynamics

China remains the single largest consumer of niobium pentoxide, accounting for roughly 36% of global volume, driven primarily by infrastructure, steel, and electronics manufacturing. In 2025, the government’s Green Steel initiative accelerated adoption of niobium-microalloyed high-strength low-alloy steels, enabling material efficiency gains and carbon intensity reduction across large-scale construction projects. This structural demand anchors consistent consumption of technical-grade niobium pentoxide in steelmaking.

Beyond steel, China’s electronics sector is emerging as a high-growth outlet for refined oxides. In 2025, usage of 3N and 4N grade Nb₂O₅ in multilayer ceramic capacitors increased by double digits, fueled by rapid expansion of 5G base stations and miniaturized IoT devices. However, export licensing controls introduced between late 2024 and 2025 have tightened access to high-purity oxides for international buyers. These dual-use restrictions have effectively favored domestic refineries, creating a supply-side squeeze that reinforces China’s internal value capture while reshaping global trade flows for battery and electronics-grade niobium pentoxide.

United Kingdom: Innovation-Led Demand Creation

The United Kingdom occupies a technology-driven niche in the niobium pentoxide market, with demand rooted in energy transition applications rather than raw material production. Nybolt’s $30 million funding round in April 2025 highlights growing confidence in niobium-enhanced fast-charging battery systems, particularly for autonomous logistics, warehouse robotics, and heavy-duty electric vehicles where rapid charge-discharge cycles are mission-critical.

Parallel advances in materials science are expanding niobium pentoxide’s relevance beyond batteries. In 2025, U.K. research institutions demonstrated measurable efficiency gains in electrolyzers using niobium-graphene composite catalysts. These findings position niobium pentoxide derivatives as enabling materials within the U.K.’s hydrogen economy roadmap, especially for high-efficiency electrolysis systems. While volumes remain modest, the U.K. market exerts disproportionate influence on future application development and downstream specification standards.

Summary Table: Niobium Pentoxide Market – Country-Level Strategic Positioning

Niobium Pentoxide Market County Level Snapshot

|

Country

|

Strategic Focus Area

|

Key Developments

|

Market Implication

|

|

Brazil

|

Battery-grade oxide industrialization

|

Industrial Nb₂O₅ refining, XNO anodes, mixed oxide transit

|

Global supply anchor for energy storage

|

|

United States

|

Supply security and ultra-high purity

|

DoD funding, Elk Creek project, aerospace demand

|

Defense-driven, high-purity niche growth

|

|

Canada

|

Resource diversification and recovery

|

Niobec stability, Tardiff and Cap projects

|

Geopolitical and supply risk mitigation

|

|

China

|

Volume consumption and internalization

|

Green steel, MLCC growth, export controls

|

Domestic value capture and trade tightening

|

|

United Kingdom

|

Innovation-led application expansion

|

Fast-charge batteries, hydrogen catalysts

|

Technology-driven demand creation

|

Niobium Pentoxide Market Report Scope

Niobium Pentoxide Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$551.5 Million

|

|

Market Size (2034)

|

$1005.4 Million

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Grade (Industrial Grade, High-Purity Grade), By Application (Metal and Alloy Production, Optical Materials, Energy Storage, Electronics, Catalysis), By End-Use Industry (Aerospace and Defense, Automotive, Electronics and Semiconductors, Construction and Infrastructure, Telecommunications, Medical Devices)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

CBMM, Anglo American, Niobec, Mitsui Mining and Smelting, JX Nippon Mining and Metals, AMG Advanced Metallurgical Group, PhosAgro, NioCorp Developments, Tantalum-Niobium International Study Center, Jiujiang Tanbre, King-Tan Tantalum and Niobium, Guangdong Zhiyuan New Material, F&X Electro-Materials, Solar Applied Materials Technology, Admat

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Niobium Pentoxide Market Segmentation

By Grade

- Industrial Grade

- High-Purity Grade

By Application

- Metal and Alloy Production

- Optical Materials

- Energy Storage

- Electronics

- Catalysis

By End-Use Industry

- Aerospace and Defense

- Automotive

- Electronics and Semiconductors

- Construction and Infrastructure

- Telecommunications

- Medical Devices

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Niobium Pentoxide Market

- CBMM

- Anglo American

- Niobec

- Mitsui Mining and Smelting

- JX Nippon Mining and Metals

- AMG Advanced Metallurgical Group

- PhosAgro

- NioCorp Developments

- Tantalum-Niobium International Study Center

- Jiujiang Tanbre

- King-Tan Tantalum and Niobium

- Guangdong Zhiyuan New Material

- F&X Electro-Materials

- Solar Applied Materials Technology

- Admat

*- List not Exhaustive