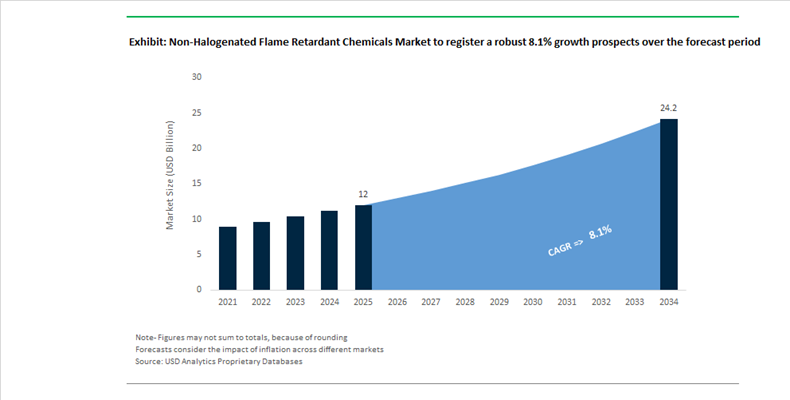

Non-Halogenated Flame Retardant Chemicals Market Valued at $12 Billion in 2025, Set to Reach $24.2 Billion by 2034 at 8.1% CAGR

The Non-Halogenated Flame Retardant Chemicals Market is valued at $12 billion in 2025 and is projected to reach $24.2 billion by 2034, expanding at a strong CAGR of 8.1%. Growth is being driven by stringent fire safety regulations, rapid electrification of mobility, and the global phase-out of halogenated flame retardants in electronics, construction materials, and automotive components. Increasing restrictions under EU REACH, TSCA, and global green building codes are accelerating the transition toward phosphorus-based, mineral-based, polymeric, and reactive flame retardant systems that minimize toxic gas release, smoke density, and corrosive byproducts during combustion.

In February 2024, the European Chemicals Agency classified Triphenyl Phosphate (TPP) as a Substance of Very High Concern due to endocrine-disrupting properties. This regulatory action reshaped formulation strategies across consumer electronics and printed circuit boards, prompting rapid adoption of safer organophosphorus alternatives. In May 2024, Ascend Performance Materials launched EV-specific non-halogenated flame retardant grades for battery housings and busbars, engineered to maintain color stability under high thermal stress while meeting UL94 V-0 standards. The electrification trend intensified in June 2025 when BASF SE introduced Ultramid® Advanced N3U42G6, a polyamide 9T grade incorporating non-halogenated chemistry to prevent electro-corrosion in 800V and 1000V EV systems. In November 2025, BASF localized Ultradur® PBT flame-retardant production in India, strengthening regional supply chains for automotive and electronics OEMs.

Strategic consolidation and capacity expansion accelerated through 2025. In May 2025, J.M. Huber Corporation acquired The R.J. Marshall Company’s alumina trihydrate and antimony-free flame retardant assets, integrating them into Huber Advanced Materials to reinforce North American dominance in mineral-based non-halogenated systems. In November 2025, Clariant AG formed a joint venture with FUHUA in Leshan, China, to develop next-generation phosphorus-based flame retardants for construction and automotive sectors. During the same month, Clariant inaugurated a second Exolit™ OP halogen-free production line at its Daya Bay site, lifting total site investment to CHF 100 million and strengthening supply for e-mobility and 5G infrastructure. In early 2026, Clariant advanced a titanium-based catalyst technology positioned as a non-antimony alternative for polyester systems, addressing volatility in the antimony trioxide market.

Innovation in reactive and circular-compatible chemistries is defining competitive positioning. At K 2025, Lanxess AG showcased Levagard® 2100, a reactive phosphorus-based flame retardant chemically bonded into polyurethane matrices, reducing migration and VOC emissions. Throughout 2025 and early 2026, ICL Group advanced polymeric flame retardant systems engineered for recyclability, aligning with circular economy mandates. In January 2026, Huber Advanced Materials implemented global price adjustments in response to U.S. tariffs on aluminum hydroxide feedstock, underscoring the geopolitical sensitivity of mineral-based flame retardant supply chains.

The market structure is evolving toward high-performance, low-smoke, non-corrosive flame retardant technologies tailored for EV battery packs, high-frequency 5G components, lightweight construction panels, and advanced engineering plastics. Phosphorus-based additives, metal hydroxides, reactive polymeric systems, and halogen-free catalysts are replacing brominated and chlorinated compounds across high-growth applications, reinforcing sustained momentum in the global non-halogenated flame retardant chemicals industry.

Non-Halogenated Flame Retardant (NHFR) Chemicals Market Trends and Opportunities

Trend: Mandatory Phase-In of NHFRs in Consumer Electronics Under Converging EU and US Regulations

The global non-halogenated flame retardant chemicals market is entering a regulatory-driven acceleration phase as brominated and chlorinated systems rapidly lose legal and commercial viability. In the European Union, the European Commission initiated a decisive regulatory reset in February 2025 through its consultation under the POP Regulation, proposing ultra-low unintentional trace contaminant limits of ≤10 mg/kg for PBDEs in mixtures and finished articles. With final enforcement deadlines set for December 30, 2025, particularly for child-centric and childcare products, electronics OEMs are facing non-negotiable timelines for reformulation. This effectively eliminates tolerance-based compliance strategies and forces full material substitution toward halogen-free flame retardant systems.

A parallel regulatory tightening is unfolding in the United States. The U.S. Environmental Protection Agency finalized TSCA Section 6 risk management rules for DecaBDE and PIP (3:1), effective January 21, 2025. These rules prohibit processing and distribution of these substances in most commercial applications, including wire insulation, internal connectors, and plastic housings. The result is a synchronized transatlantic compliance landscape that leaves electronics manufacturers with little optionality outside NHFR adoption. OEMs are therefore standardizing around UL94 V-0 rated halogen-free polymers, prioritizing materials that meet flame retardancy at reduced wall thicknesses without compromising dielectric performance. Suppliers such as Asahi Kasei are capitalizing on this shift by commercializing modified PPE resins capable of achieving V-0 ratings at 0.75 mm, aligning with miniaturization trends in 5G and consumer electronics.

Trend: Phosphorus-Based NHFRs Becoming Core Safety Materials in EV Battery Platforms

The electrification of mobility is structurally reshaping demand patterns within the NHFR chemicals market, with phosphorus-based systems emerging as the dominant solution for EV battery safety. High-voltage architectures exceeding 800 V, combined with the thermal runaway risks inherent in lithium-ion cells, have rendered traditional halogenated flame retardants unsuitable due to their corrosive and toxic gas emissions under fire conditions. As a result, battery manufacturers are specifying non-corrosive NHFR chemistries that maintain electrical integrity during and after thermal events.

This demand shift is catalyzing large-scale capacity investments in Asia, where EV manufacturing is most concentrated. In October 2025, Clariant completed a CHF 100 million expansion at its Daya Bay facility to scale Exolit® OP phosphinate production dedicated to e-mobility applications. The strategic rationale extends beyond compliance. Extreme volatility in antimony trioxide pricing, which surged over 400 percent year-on-year to exceed USD 51,500 per ton in early 2025, has exposed the fragility of halogen-antimony systems. Phosphorus-based NHFRs such as aluminum diethylphosphinate allow OEMs to decouple flame retardancy from antimony supply risk while achieving UL94 V-0 certification. New specialty grades introduced in 2025 also deliver CTI ratings of 600 V, ensuring long-term electrical safety in moisture- and heat-intensive battery environments, a critical benchmark for next-generation fast-charging platforms.

Opportunity: NHFR-Enabled High-Frequency Plastics for 5G and Advanced Connectivity

The global rollout of 5G infrastructure and massive MIMO antenna systems is opening a specialized, high-margin opportunity for NHFR formulations engineered for radio-frequency transparency. Traditional mineral-filled flame retardants introduce dielectric losses that are unacceptable at millimeter-wave frequencies. As a result, OEMs are increasingly specifying organic phosphorus and nano-hybrid NHFR systems that preserve low dielectric constants and dissipation factors while maintaining stringent fire safety ratings.

Advanced PPE-based foams and enclosures used in 5G radomes must operate at dielectric constants of approximately 2.6–2.8 and dissipation factors below 0.004 at 28 GHz. NHFR additives are being optimized to deliver UL94 V-0 performance without altering these parameters, directly protecting signal efficiency and network reliability. Additionally, dense urban deployment of small cells is intensifying thermal loads within compact housings. This is driving R&D into NHFR systems that simultaneously enhance flame resistance and thermal conductivity, positioning non-halogenated solutions as multifunctional enablers rather than single-attribute compliance additives.

Opportunity: Transparent Intumescent NHFR Coatings for Mass Timber Construction

The rapid adoption of mass timber construction is creating a structurally new demand segment for non-halogenated flame retardant coatings that preserve visual aesthetics while meeting stringent fire codes. Updates to the 2024 International Building Code and the National Design Specification for Wood Construction have legitimized cross-laminated timber for mid- and high-rise buildings, provided that 1-hour and 2-hour fire resistance ratings can be demonstrated. This has accelerated the specification of transparent intumescent NHFR coatings that expand into insulating char layers under heat exposure.

Water-based, halogen-free intumescent systems are now achieving ASTM E84 Class A ratings while remaining optically clear, enabling architects to retain exposed timber surfaces in commercial and residential projects. In 2025, formulation priorities shifted toward long-term shelf-life stability and application robustness under variable site conditions, with ammonium polyphosphate-based systems such as Exolit AP 435 setting performance benchmarks. Regulatory momentum is reinforcing this opportunity. As cities including Paris and Vancouver mandate low-carbon construction materials, transparent NHFR coatings are becoming a critical enabler for substituting steel with timber while maintaining compliance with NFPA 285 and UL 263 fire safety standards.

Non-Halogenated Flame Retardant Chemicals Market Share and Segmentation Insights

Phosphorus-Based Flame Retardants Dominate Non-Halogenated Flame Retardant Chemicals Market Through High Efficiency in Engineering Plastics

Phosphorus-based flame retardants accounted for 42.80% of the Non Halogenated Flame Retardant Chemicals Market share in 2025, making them the most widely used product category across polymers, engineering plastics, coatings, and electronic materials. These flame retardants are highly valued for their dual flame inhibition mechanisms, functioning in both the gas phase and condensed phase to suppress combustion, reduce heat release, and promote protective char formation during fire exposure. The category includes organophosphates, phosphinates, and red phosphorus compounds, which are widely incorporated into polyamides, polyesters, epoxy resins, polyurethanes, and thermoplastic composites used in electronics, automotive components, and industrial equipment. Their strong performance across diverse polymer systems has accelerated adoption as industries shift away from brominated flame retardants due to environmental and regulatory pressure. In 2025, aluminum diethylphosphinate has gained particular prominence in high-temperature engineering plastics used in electronic connectors, circuit protection devices, and miniature components, offering thermal stability above 350°C and maintaining flame retardancy during high-temperature processing conditions typical of advanced electronics manufacturing.

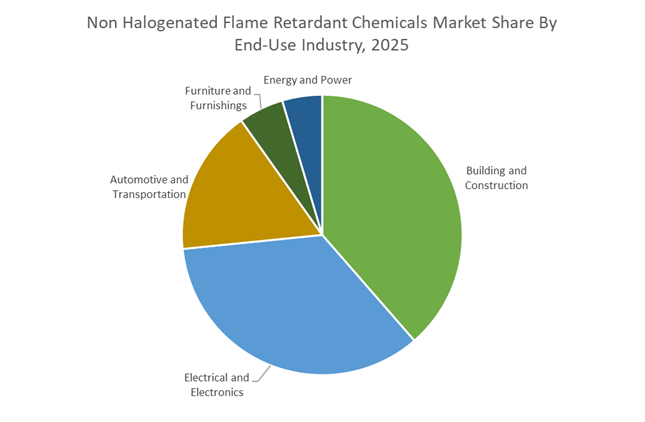

Building and Construction Industry Drives the Largest Consumption of Non-Halogenated Flame Retardant Chemicals

Building and construction accounted for 38.60% of the Non Halogenated Flame Retardant Chemicals Market share in 2025, representing the largest end-use sector for halogen-free flame retardant materials. Modern construction materials require flame protection to comply with stringent fire safety regulations and building codes governing insulation, cables, structural plastics, coatings, and interior finishes. Non-halogenated flame retardant chemicals are widely incorporated into polymeric insulation foams, electrical wiring compounds, composite panels, and protective coatings to reduce fire propagation and smoke generation while maintaining material durability. The large scale of global construction activity across residential buildings, commercial complexes, infrastructure projects, and energy facilities continues to generate strong demand for halogen-free fire protection materials. In 2025, the expansion of green building certification systems such as LEED and BREEAM has become a significant market driver, as developers increasingly specify low-toxicity, environmentally compliant flame retardant solutions to achieve sustainability credits. This shift has accelerated the replacement of halogenated flame retardants with phosphorus-based, mineral-based, and intumescent systems in insulation materials, wire and cable coatings, and construction polymers used in modern fire-safe buildings.

Non-Halogenated Flame Retardant Chemicals Market Competitive Landscape

The non-halogenated flame retardant chemicals market in 2026 is driven by EV electrification, halogen-free regulatory mandates, and antimony-free formulations. Competitive differentiation centers on phosphorus-based additives, mineral hydrates, and localized production, enabling high CTI performance, dielectric stability, and sustainable fire safety solutions for electronics and automotive applications.

Clariant scales phosphorus flame retardants with EV-grade CTI performance and Asia-Pacific capacity expansion

Clariant is strengthening its leadership through advanced phosphorus-based flame retardants and strategic Asian manufacturing expansion. Its CHF 100 million Daya Bay Phase II investment adds a second Exolit® OP production line, improving supply agility for e-mobility and electronics sectors. The launch of Exolit® OP 1266 enables stable CTI 600 V performance, critical for EV busbars and connectors. Its partnership with FUHUA enhances next-generation halogen-free additive development under tightening regulations. Clariant’s Exolit® OP Terra line integrates renewable feedstocks with ≥50% Renewable Carbon Index, supporting carbon-neutral manufacturing. This combination of innovation, sustainability, and regional capacity reinforces its competitive edge.

BASF integrates high-performance polymers and localized production for EV and cable flame retardant applications

BASF leverages its Verbund integration and polymer expertise to deliver high-performance non-halogenated flame retardant solutions. Its Shanghai TPU production for Elastollan® FR grades supports EV charging infrastructure and robotic cable applications with localized supply efficiency. Ultramid® T6000 and Advanced N3U42G6 materials provide superior thermal shock resistance and electro-corrosion protection in high-voltage systems. BASF’s collaboration with THOR enhances additive development for halogen-free compliance and material sustainability. With strong positioning in automotive and electrical applications, BASF offers integrated solutions that combine flame retardancy with mechanical durability. This approach strengthens its role in next-generation mobility and electronics.

ICL drives sustainable flame retardant innovation with integrated mineral supply and SAFR evaluation framework

ICL Group is advancing non-halogenated flame retardant technologies through its SAFR® sustainability framework and vertically integrated mineral supply chain. The company offers over 50 tailored solutions for EV powertrains, battery casings, and charging infrastructure. Its polymeric and reactive flame retardants provide non-leaching performance, addressing environmental persistence concerns. Integration from Dead Sea resources ensures reliable supply of phosphorus and magnesium-based materials. ICL’s focus on eco-friendly additives aligns with EU Green Deal requirements and global OEM sustainability targets. This positions the company as a key supplier of high-performance, environmentally compliant flame retardants.

Huber strengthens mineral-based flame retardant portfolio with ATH/MDH integration and synergistic additive technologies

Huber Advanced Materials leads in halogen-free mineral flame retardants through its expanded ATH and MDH portfolio following MAGNIFIN integration. The company’s Safire® technology enhances efficiency by combining nitrogen-phosphate chemistry with mineral systems, reducing required loading levels. Its Kemgard® range provides effective smoke suppression and serves as a replacement for antimony trioxide in PVC applications. A 2026 price adjustment reflects cost pressures from tariffs and logistics, reinforcing margin protection strategies. Huber’s focus on technical synergy and high-temperature performance supports automotive and construction applications. This positions it as a dominant supplier in mineral-based flame retardant systems.

LANXESS accelerates phosphorus-based additive growth with high-purity halogen-free solutions for electronics and coatings

LANXESS is expanding its polymer additives business by focusing on organo-phosphorus flame retardants as sustainable alternatives to halogenated systems. Its Disflamoll® and Levagard® product lines are optimized for polyurethane foams and flexible coatings, delivering efficient flame retardancy without compromising material properties. The company emphasizes compliance with REACH and RoHS, targeting high-purity formulations for electronics and aerospace sectors. Dual-action flame retardancy mechanisms enhance both gas-phase and condensed-phase performance. LANXESS leverages its deep phosphorus chemistry expertise to support OEM transitions to halogen-free materials. This strategy strengthens its position in high-growth, regulation-driven markets.

China: Phosphorus-Centric Scale-Up Aligned with EV and Electronics Policy

China has emerged as the most aggressive adopter of non-halogenated flame retardant chemicals, driven by electric mobility, electronics miniaturization, and regulatory substitution of brominated systems. A central inflection point was the November 2025 completion of Clariant’s CHF 100 million expansion at Daya Bay, adding a second Exolit™ OP phosphorus-based production line. The facility now functions as Clariant’s Asia-Pacific supply anchor for halogen-free flame retardants used in EV battery housings, power electronics, and high-voltage connectors. This capacity build is structurally aligned with China’s rapid EV charging rollout, which is projected to exceed 12 million charging points by 2026 and requires engineering plastics capable of withstanding 800V architectures.

The strategic momentum accelerated further in Q4 2025 through Clariant’s joint venture with FUHUA in Leshan, Sichuan, targeting next-generation phosphorus NHFRs for domestic compliance. This aligns with the MIIT 2026 Green Manufacturing mandate, which explicitly prioritizes halogen-free engineering plastics in 5G infrastructure and consumer electronics, aiming to cut DecaBDE usage by more than 40%. Product innovation has kept pace, with the October 2025 launch of Exolit OP 1266 (TP), delivering a CTI of 600V, a critical benchmark for long-term insulation safety in EV battery packs.

Germany: Reactive and Polymeric NHFRs Anchoring EU Sustainability Standards

Germany’s NHFR market evolution is defined by chemistry-level innovation rather than capacity expansion, reflecting the EU’s stringent sustainability and Ecodesign frameworks. At K 2025, LANXESS introduced Levagard 2100, a reactive phosphorus flame retardant that chemically integrates into PUR and PIR matrices. This migration-resistant profile materially reduces VOC emissions and positions reactive NHFRs as the preferred solution for sustainable building insulation across Europe.

LANXESS also scaled Emerald Innovation 5000 during 2025, a polymeric NHFR engineered as a direct replacement for halogenated additives in engineering plastics, enabling OEMs to meet updated Ecodesign and recyclability criteria without redesigning components. In parallel, German R&D programs are pivoting toward phosphorus-nitrogen synergistic systems to protect hydrogen fuel cell components, with pilot deployments in North Rhine-Westphalia targeting 2026 commercialization. Complementing this, BASF optimized its Melapur™ 200 production, refining particle size distribution to improve dispersion in thin-walled nylon parts used in automotive electronics and power modules.

United States: Defense Supply Security and Infrastructure-Driven Demand

In the United States, the NHFR market is being reshaped by defense localization, PFAS elimination, and infrastructure-led consumption. During 2024–2025, the Department of Defense issued targeted grants to onshore production of high-purity organophosphorus intermediates, reducing strategic dependence on imported halogen-free chemistries for aerospace composites. This move aligns NHFR development with national security priorities rather than solely commercial regulation.

Commercial momentum has been reinforced by private-sector innovation. J.M. Huber Corporation received Gold Standard recognition in May 2025, underscoring its leadership in ATH and magnesium hydroxide flame retardants, which remain critical for wire and cable and construction applications. In November 2025, Zentek launched a graphite-gel-based NHFR in the U.S., targeting lithium-ion battery fire mitigation. Concurrently, Trinseo advanced PFAS-free Emerge™ polycarbonate resins in response to state-level legislation. Federal Infrastructure Investment and Jobs Act spending in 2025–2026 has further increased demand for NHFR-based intumescent coatings mandated for bridges, tunnels, and high-occupancy steel structures.

India: Import Substitution and Rail-Led Fire Safety Compliance

India’s NHFR market is transitioning from import dependence toward localized production, driven by rail infrastructure and electronics recycling policy. In 2025, VKP HFFR Pvt. Ltd. emerged as a notable domestic supplier, securing funding to manufacture halogen-free flame retardants for automotive engineering plastics and technical textiles. This development directly addresses cost and lead-time disadvantages associated with European imports.

Regulatory momentum is reinforcing this shift. Updated E-waste Management Rules for 2025–2026 incentivize the use of NHFR-compatible recyclable plastics in consumer electronics to simplify shredding and material recovery. At the same time, large-scale deployment of Vande Bharat high-speed rail projects has driven demand for NHFR-compliant interior panels and upholstery meeting EN 45545 fire standards, anchoring rail as a structurally important end-use segment for halogen-free systems in India.

Israel: Circular Phosphorus Innovation for Flexible Applications

Israel’s contribution to the NHFR market is centered on high-performance phosphorus chemistry optimized for circularity. In 2025, ICL Group announced a $40 million capital expenditure to expand its next-generation phosphorus-based NHFR portfolio. These formulations are engineered to retain recyclability of plastic components after first use, aligning with circular economy objectives across Europe and North America.

ICL also optimized its Fyrol™ HF-series in 2025, particularly HF-10, enhancing fire resistance in flexible polyurethane foams without compromising mechanical properties. This positions Israel as a niche innovation hub for NHFRs in foams, furniture, and transportation interiors where performance trade-offs have historically limited halogen-free adoption.

Summary Table: Non-Halogenated Flame Retardant Chemicals – Country-Level Strategic Positioning

Non-Halogenated Flame Retardant Chemicals Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Developments

|

Market Implication

|

|

China

|

EV and electronics-driven phosphorus NHFR scale

|

Daya Bay expansion, MIIT substitution mandate

|

Rapid volume growth and high-voltage specialization

|

|

Germany

|

Reactive and polymeric NHFR innovation

|

Levagard 2100, Emerald Innovation 5000

|

EU-compliant, low-VOC premium solutions

|

|

United States

|

Defense security and infrastructure demand

|

DoD onshoring, PFAS-free resins, IIJA

|

Stable industrial and construction-led consumption

|

|

India

|

Import substitution and rail safety

|

Domestic start-ups, EN 45545 compliance

|

Localization and cost-driven adoption

|

|

Israel

|

Circular phosphorus chemistry

|

ICL capex, Fyrol™ HF optimization

|

High-value recyclable NHFR niches

|

Non-Halogenated Flame Retardant Chemicals Market Report Scope

Non-Halogenated Flame Retardant Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12 Billion

|

|

Market Size (2034)

|

$24.2 Billion

|

|

Market Growth Rate

|

8.1%

|

|

Segments

|

By Product Type (Mineral-Based Flame Retardants, Phosphorus-Based Flame Retardants, Nitrogen-Based Flame Retardants, Intumescent Flame Retardant Systems), By Polymer Type (Polyolefins, Engineering Thermoplastics, Thermoset Resins, Polyurethanes, Styrenics), By Application (Wires and Cables, Insulation Materials, Electronic Components and Enclosures, Automotive Components, Textiles and Protective Materials), By End-Use Industry (Electrical and Electronics, Building and Construction, Automotive and Transportation, Furniture and Furnishings, Energy and Power)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Clariant, LANXESS, J.M. Huber, ICL Group, BASF, Albemarle, Italmatch Chemicals, Nabaltec, Budenheim, ADEKA, Wengfu Group, Songwon Industrial, Shandong Brother Sci & Tech, Thor Group, Rio Tinto

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Non Halogenated Flame Retardant Chemicals Market Segmentation

By Product Type

- Mineral-Based Flame Retardants

- Phosphorus-Based Flame Retardants

- Nitrogen-Based Flame Retardants

- Intumescent Flame Retardant Systems

By Polymer Type

- Polyolefins

- Engineering Thermoplastics

- Thermoset Resins

- Polyurethanes

- Styrenics

By Application

- Wires and Cables

- Insulation Materials

- Electronic Components and Enclosures

- Automotive Components

- Textiles and Protective Materials

By End-Use Industry

- Electrical and Electronics

- Building and Construction

- Automotive and Transportation

- Furniture and Furnishings

- Energy and Power

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Non Halogenated Flame Retardant Chemicals Market

- Clariant

- LANXESS

- J.M. Huber

- ICL Group

- BASF

- Albemarle

- Italmatch Chemicals

- Nabaltec

- Budenheim

- ADEKA

- Wengfu Group

- Songwon Industrial

- Shandong Brother Sci & Tech

- Thor Group

- Rio Tinto

*- List not Exhaustive