North America Biocides & Disinfectants Market: Industry Growth Analysis and Value Forecast to 2034

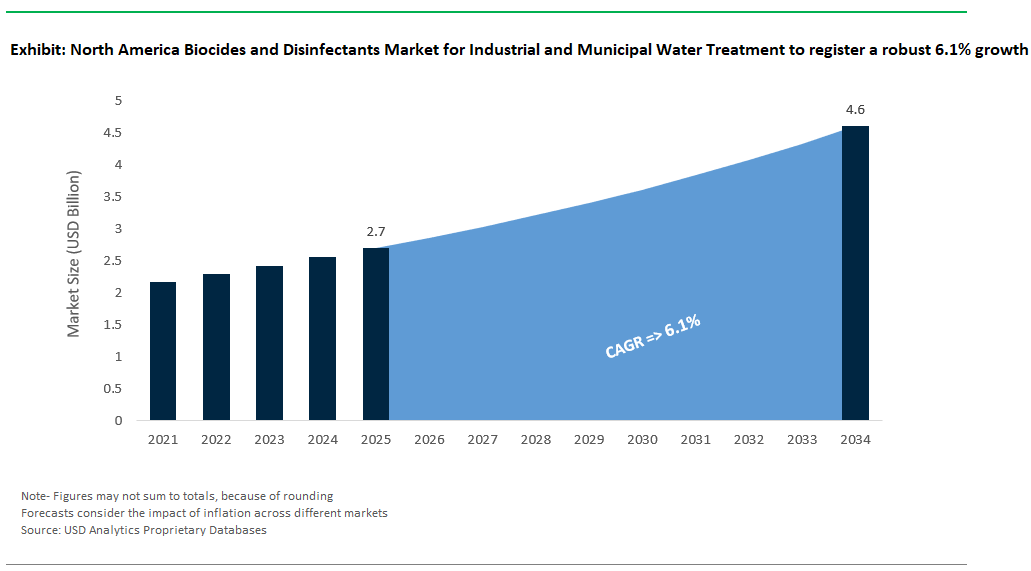

North America Biocides and Disinfectants Market for Industrial and Municipal Water Treatment Size is estimated at $2.7 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 6.1% to reach $4.6 Billion by 2034.

The North American biocides and disinfectants market is defined by high regulatory oversight and application-specific performance standards, particularly in industrial and municipal water treatment. In industrial cooling water applications, oxidizing biocides remain a cornerstone, with chlorine dioxide (ClO₂) commonly dosed between 0.1–0.5 ppm for microbial control, especially targeting Legionella pneumophila. This aligns with ASHRAE Standard 188 and CDC guidance, which recommend maintaining effective CT (concentration × time) values for disinfection without exceeding corrosive thresholds. BCDMH (1-bromo-3-chloro-5,5-dimethylhydantoin) continues to be favored due to its stability and consistent biocidal performance under varying pH and temperature conditions, as acknowledged by the Cooling Technology Institute (CTI).

Non-oxidizing biocides such as DBNPA and THPS are widely used where oxidative damage or material compatibility is a concern. DBNPA’s rapid breakdown into non-toxic byproducts usually within 24 hours has earned it widespread approval under the U.S. EPA’s FIFRA framework. THPS, typically dosed between 50–100 ppm, has shown effective biofilm control in monthly applications and meets corrosion-resistance standards outlined in NACE TM0212 protocols.

In the municipal sector, drinking water treatment continues to evolve under regulatory directives such as the U.S. EPA Stage 2 Disinfection Byproduct Rule. Water utilities frequently maintain chloramine residuals to limit trihalomethane (THM) and haloacetic acid (HAA) formation while ensuring microbial control. Advanced disinfection systems, particularly ultraviolet advanced oxidation processes (UV-AOP), are gaining traction. For example, systems utilizing 40 mJ/cm² UV with 0.5 mg/L hydrogen peroxide have demonstrated >99.9% inactivation rates of Cryptosporidium, compliant with NSF/ANSI Standard 55 Class A certification.

However, evolving toxicological findings and environmental discharge regulations are reshaping the biocide landscape. Compounds like glutaraldehyde are subject to effluent restrictions often below 50 parts per billion (ppb) in permitted discharges and face challenges for reauthorization under Canada’s Pest Control Products Act and the EU’s Biocidal Products Regulation (BPR). Formaldehyde usage is increasingly constrained due to its OSHA PEL (permissible exposure limit) of 0.75 ppm and its classification as a Group 1 carcinogen by IARC. As a result, chemical manufacturers are investing in biodegradable, precision-targeted biocides that align with sustainability objectives and worker safety standards.

Market Trend: Transition Toward PFAS-Free and Smart Disinfection Technologies

A notable trend in North America’s biocides and disinfectants market is the accelerated shift away from per- and polyfluoroalkyl substances (PFAS) and quaternary ammonium compounds (QACs), driven by U.S. and Canadian regulatory actions. The U.S. EPA finalized its National Primary Drinking Water Regulation for PFAS in 2024, setting enforceable limits for six PFAS compounds, while Canada has proposed stringent environmental screening assessments for QACs due to bioaccumulation concerns.

This shift is prompting the adoption of alternative disinfection technologies such as enzymatic biocides, electrolyzed oxidizing water (EOW), peracetic acid (PAA), and UV-AOP systems. These solutions are gaining preference for their minimal residuals and efficacy against chlorine-resistant pathogens like Cryptosporidium and Legionella. Additionally, AI-enabled systems are being integrated to optimize dosage and performance. For instance, Evoqua’s SmartGuard™ monitors water chemistry in real time, allowing precise dosing adjustments that reduce chlorine use by up to 25% while maintaining 4-log reduction targets required by EPA guidelines.

In sectors with elevated hygiene standards such as healthcare, hospitality, and data centers technologies like copper-silver ionization and UV-ozone are being deployed to address both microbial control and disinfection by-product concerns. These approaches offer improved Legionella mitigation and comply with CDC Toolkit recommendations for healthcare water systems.

Market Opportunity: Over $1.2 Billion Growth in Industrial Water Reuse and Legionella Prevention

A major opportunity in the North American biocides and disinfectants market lies in the intersection of industrial water reuse and Legionella control, collectively representing a market expansion of over $1.2 billion. Industrial facilities, particularly those with significant cooling and HVAC infrastructure, are adopting water reuse systems that reduce chemical discharge and align with sustainability targets set under ESG frameworks.

Cooling towers account for a substantial portion of biocide use, and major installations such as those operated by Dow and Duke Energy are exploring alternatives to halogenated chemistries. Innovations in non-oxidizing biocides, along with copper-silver ionization systems, are enabling >90% water reuse while minimizing scaling and corrosion. These practices support compliance with Clean Water Act discharge permits and reduce operational downtime.

In municipal reuse, utilities like Phoenix’s 91st Avenue Wastewater Treatment Plant are piloting combined PAA and UV treatments that meet potable reuse standards without forming regulated DBPs. This is increasingly critical under revised Safe Drinking Water Act proposals expected to tighten controls on THMs, HAAs, and emerging contaminants.

The commercial sector is also responding to heightened awareness of Legionella risks. Healthcare institutions such as Mayo Clinic are adopting monochloramine-based protocols endorsed by CDC’s Legionella control toolkit to reduce outbreaks. Meanwhile, technology companies such as Microsoft are incorporating biocide selection into their green data center procurement criteria, with a preference for systems that exclude PFAS and demonstrate digital control capabilities.

Regulatory incentives including carbon credits for UV or ozone-based systems and PFAS-free procurement preferences are creating a competitive advantage for suppliers offering validated, high-performance, and environmentally compatible disinfection solutions tailored to North American regulatory and operational realities.

Competitive Analysis North America Biocides and Disinfectants Market for Water Treatment

The North American market for biocides and disinfectants in industrial and municipal water treatment is highly competitive and follows a three-tier structure with global leaders, regional specialists, and emerging disruptors. The top-tier players, Ecolab, Lonza, BASF, Solvay, and Dow, hold about 60% of the market. They achieve this by using their extensive B2B supply chains, strong compliance with regulations (especially in EPA-regulated applications), and improved digital dosing capabilities. Their recent developments in chlorine-free chemistries, such as peracetic acid (PAA), and hydrogen peroxide-based solutions, show a move toward low-toxicity, environmentally friendly products amid growing sustainability demands. These companies are adding intelligence to disinfection processes, using platforms like Ecolab’s 3D TRASAR and Solvay’s SmartDoseto optimize chemical use and improve traceability. These factors are crucial for large-scale industrial and municipal contracts.

The mid-tier includes companies like Kemira, Buckman, Albemarle, and Bio-Lab, which make up about 30% of the market. These firms have established strong positions through regional strength, cost innovation, and specialization. For example, Bio-Lab’s dominance in sodium hypochlorite supply in the Southeast U.S. and Buckman’s use of enzymes for biofilm control illustrate how technical customization and location matter. Kemira’s chloramine blends for pulp and paper and Albemarle’s bromine-based biocides also serve important sectors like energy, marine, and heavy industry.

The final tier features fast-growing disruptors like Evoqua, Enviro Tech, and BioSafe Systems, who are influencing the market’s future. Currently, they hold only 10% of the market share, but they are expanding quickly by focusing on chlorine-free, residue-minimizing, and LEED-compliant disinfection systems. Evoqua’s combination of UV and electrochemical technologies is gaining popularity in municipal systems that want to move away from traditional chlorine methods. Meanwhile, Enviro Tech and BioSafe Systems target food and agriculture facilities with EPA-compliant, non-toxic blends that satisfy both safety and sustainability needs.

Overall, the competitive landscape is increasingly influenced not just by volume or brand reputation, but by the ability to deliver performance while meeting regulatory requirements, environmental standards, and digital traceability. As chlorine- and glutaraldehyde-based chemicals face regulatory scrutiny and ESG concerns, companies in all tiers are racing to adjust their portfolios to meet changing standards. They are doing this through patented biocide chemistries, smart delivery systems, and vertically integrated manufacturing processes.

North America Biocides & Disinfectants Market for Industrial & Municipal Water Treatment– Segmentation Insights (2025–2034)

By Type of Biocide: Oxidizing Biocides Dominate, Non-Oxidizing Solutions Gain Ground

In North America's water treatment sector, oxidizing biocides are expected to command the largest market share at 62.9% in 2025, cementing their position as the go-to solution for large-scale disinfection needs. Chlorine, chlorine dioxide, and bromine remain the most extensively used oxidizing agents, valued for their broad-spectrum efficacy and cost-effectiveness in neutralizing bacteria, viruses, and algae across municipal drinking water systems and industrial process waters. The continued reliance on chlorination technologies in legacy infrastructure especially in municipal water treatment sustains the dominant use of oxidizing agents.

Conversely, non-oxidizing biocides are projected to grow at the fastest CAGR of 8.7% through 2034, owing to their increasing adoption in high-value industrial settings where biofilm formation is a critical operational concern. Compounds such as isothiazolinones, glutaraldehyde, and quaternary ammonium salts are being increasingly employed in cooling towers, paper mills, and oilfield water systems due to their selective biocidal action, lower corrosivity, and compatibility with complex chemistries. Their growth is particularly pronounced in systems requiring precise microbial control without introducing residual oxidants, especially in food and beverage, electronics, and pharmaceutical facilities.

.png)

By Application: Industrial Water Treatment Leads, Municipal Sector Holds Steady

Industrial water treatment is anticipated to account for 57.4% of the North American biocides market in 2025, driven by sectors such as power generation, oil and gas, chemicals, and manufacturing. These industries rely heavily on biocides and disinfectants to prevent microbial growth, biofouling, and corrosion in cooling systems, boilers, and closed-loop water networks. The persistent expansion of industrial cooling infrastructure across the United States and Canada along with the rise in water reuse practices further fuels biocide demand in complex process environments where downtime and contamination must be strictly controlled.

Meanwhile, the municipal water treatment segment is forecast to grow steadily at a CAGR of 7.1% during the same period, supported by regulatory mandates and public health standards. Chloramine and chlorine continue to dominate municipal disinfection practices due to their proven reliability, safety, and residual protection throughout the distribution system. As municipalities modernize treatment plants and adopt dual disinfection strategies, the segment remains critical to ensuring safe potable water supply for growing urban populations across North America.

North America Biocides and Disinfectants Market for Industrial and Municipal Water Treatment Report Scope

North America Biocides and Disinfectants Market for Industrial and Municipal Water Treatment

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.7 Billion

|

|

Market Size (2034)

|

$4.6 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Type of Biocide/Disinfectant (Oxidizing Biocides, Non-Oxidizing Biocides, Other Biocide Types), By Application (Industrial Water Treatment, Municipal Water Treatment), By Form (Liquid, Solid (Powder, Granules, Tablets), Gas), By End-User Industry (Municipal Utilities (Water and Wastewater), Industrial

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Solenis LLC (U.S.), Kemira Oyj (Finland), SNF Holding Company (U.S. - SNF Floerger), BASF SE (Germany), The Dow Chemical Company (U.S.), Veolia Water Technologies (France), ChemTreat, Inc. (U.S.), Nouryon (The Netherlands), Brenntag North America, Inc. (Germany), ChemREADY (U.S.), Chardon Laboratories, Inc. (U.S.), E and C Chemicals Inc. (U.S.), Arxada (Switzerland), LANXESS AG (Germany),

|

|

Countries

|

US, Canada, Mexico

|

North America Biocides and Disinfectants Market for Industrial and Municipal Water Treatment Market Segmentation

By Type of Biocide/Disinfectant

- Oxidizing Biocides

- Chlorine and Hypochlorites

- Bromine Compounds

- Chlorine Dioxide

- Ozone (O3)

- Peracetic Acid (PAA)

- Hydrogen Peroxide

- Non-Oxidizing Biocides

- Glutaraldehyde

- Isothiazolinones

- Quaternary Ammonium Compounds (Quats)

- DBNPA (2,2-Dibromo-3-nitrilopropionamide)

- THPS (Tetrakis Hydroxymethyl Phosphonium Sulfate)

- Carbamates

- Phenolics

- Metallic Compounds

- Other Biocide Types

By Application

- Industrial Water Treatment

- Cooling Water Systems

- Boiler Water Treatment

- Process Water Treatment

- Industrial Wastewater Treatment

- Oil and Gas

- Pulp and Paper

- Power Plants

- Mining and Mineral Processing

- Food and Beverage

- Chemical Manufacturing

- Electronics and Semiconductors

- Other Industrial Manufacturing

- Municipal Water Treatment

- Drinking Water Disinfection

- Municipal Wastewater Disinfection

By Form

- Liquid

- Solid (Powder, Granules, Tablets)

- Gas

By End-User Industry

- Municipal Utilities (Water and Wastewater)

- Industrial

- Power Generation

- Oil and Gas

- Chemical Manufacturing

- Food and Beverage

- Pulp and Paper

- Mining and Mineral Processing

- Pharmaceutical

- Electronics and Semiconductors

- Other Industrial Sectors

By Country

- United States

- Canada

- Mexico

Top Companies in North America Biocides and Disinfectants Market for Industrial and Municipal Water Treatment

- Ecolab Inc. (U.S.)

- Solenis LLC (U.S.)

- Kemira Oyj (Finland)

- SNF Holding Company (U.S. - SNF Floerger)

- BASF SE (Germany)

- The Dow Chemical Company (U.S.)

- Veolia Water Technologies (France)

- ChemTreat, Inc. (U.S.)

- Nouryon (The Netherlands)

- Brenntag North America, Inc. (Germany)

- ChemREADY (U.S.)

- Chardon Laboratories, Inc. (U.S.)

- E and C Chemicals Inc. (U.S.)

- Arxada (Switzerland)

- LANXESS AG (Germany)

* List Not Exhaustive

Research Coverage

The North America Biocides and Disinfectants Market Report provides a comprehensive analysis of the region’s evolving disinfection landscape across industrial and municipal water treatment applications. The report examines how regulatory frameworks (EPA, ASHRAE, CDC), advanced digital dosing technologies, and sustainability mandates are transforming biocide demand in critical sectors such as power generation, food processing, pharmaceuticals, and municipal utilities.

Scope Includes:

- Segmentation

- By Type of Biocide/Disinfectant: Oxidizing Biocides (Chlorine, Chlorine Dioxide, Bromine, Ozone, Peracetic Acid, Hydrogen Peroxide) and Non-Oxidizing Biocides (Glutaraldehyde, Isothiazolinones, Quaternary Ammonium Compounds, DBNPA, THPS, Carbamates, Phenolics, Metallic Compounds).

- By Application: Industrial Water Treatment (Cooling, Boiler, Process, Oil & Gas, Mining), Municipal Water Treatment (Drinking and Wastewater Disinfection).

- By Form: Liquid, Solid (Powder/Granules/Tablets), Gas.

- By End-User: Municipal Utilities, Industrial (Power, Chemical, Food & Beverage, Pharmaceutical, Electronics, Oil & Gas).

- By Country: U.S., Canada, Mexico.

- Key Trends: Transition toward PFAS-free chemistries, enzymatic biocides, UV-AOP systems, and digital monitoring platforms like Evoqua’s SmartGuard™ for real-time dosing optimization.

- Leading Players: Ecolab, Solenis, BASF, Kemira, SNF Holding, Dow, Veolia, Nouryon, and emerging disruptors like BioSafe Systems and Evoqua.

- Study Period: Historic: 2021–2024; Forecast: 2025–2034

Methodology

The report adopts a hybrid methodology combining primary interviews, regulatory insights, and predictive analytics:

- Primary Research: Structured interviews with water treatment engineers, procurement managers, and regulatory experts across sectors such as municipal utilities, power generation, healthcare, and data centers. Contributions from OEMs specializing in cooling tower operations and PFAS-free disinfection technologies were incorporated for accuracy.

- Secondary Research: Analysis of EPA Safe Drinking Water Act updates, ASHRAE Standard 188, NSF/ANSI certifications, CDC Legionella guidelines, and public filings from top-tier suppliers (Ecolab, Dow, BASF). Sourcing of market data from NAICS-coded industry databases, financial disclosures, and trade journals (Cooling Technology Institute, WQA reports).

- Modeling & Forecasting: Market estimates developed using bottom-up segmentation modeling, validated against capital expenditure in water reuse, PFAS regulation compliance costs, and ESG-aligned procurement incentives. Advanced econometric models adjusted for inflationary trends, supply chain variability, and technological adoption rates across North America.

- Validation: Benchmarking against case studies such as Phoenix Wastewater Plant’s UV-PAA reuse project, Mayo Clinic’s Legionella control systems, and Microsoft’s PFAS-free procurement program. All forecasts were stress-tested using scenario-based simulations for regulatory and technological disruptions.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements