North America Organic Coagulants for Municipal Wastewater Market: Growth Analysis, Value Projections, and Industry Forecast

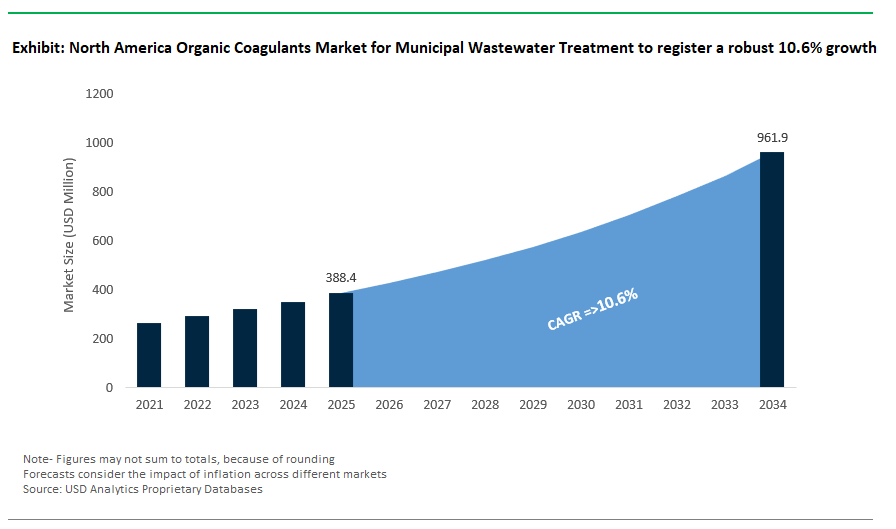

North America Organic Coagulants Market for Municipal Wastewater Treatment Size is estimated at $388.4 Million in 2025 and is forecast to register an annual growth rate (CAGR) of 10.6% to reach $961.8 Million by 2034.

The North American market for organic coagulants in municipal wastewater treatment is growing steadily, driven by performance optimization needs, biosolids regulations, and a gradual shift toward biodegradable, low-toxicity formulations. Synthetic cationic polymers such as polyDADMAC and polyamines are widely used during primary clarification, typically dosed at 2–10 mg/L to achieve >85% total suspended solids (TSS) and 70–80% biochemical oxygen demand (BOD) reductions. These polymers also play a vital role in sludge conditioning, where formulations with charge densities between 40–80% optimize dewatering in centrifuges, yielding 25–35% dry solids (DS) cakes, according to EPA 832-F-00-073.

Complementing synthetic options, bio-based coagulants are emerging as viable alternatives chitosan, derived from crustacean shells, demonstrates excellent turbidity removal (80–90%) at 5–20 mg/L and meets OECD 301F biodegradability thresholds (>90% within 28 days). Tannin-based derivatives, dosed at 30–60 mg/L, are NSF/ANSI 60 certified and offer a notable 40% reduction in metal-laden sludge compared to traditional alum, making them ideal for plants prioritizing sustainability.

Regulatory pressure under 40 CFR Part 503 on residual acrylamide content (<0.05%) in synthetic polymers is nudging utilities toward safer, natural coagulants that sidestep these constraints entirely. While synthetic polymers remain more cost-efficient, bio-polymers, though priced higher, offer downstream savings by cutting sludge disposal expenses by 20–30%, as demonstrated in NYC DEP operations. As utilities aim to balance compliance, cost, and environmental impact, the market is shifting toward hybrid strategies that leverage both synthetic performance and bio-based sustainability.

Market Trend: Bio-Based Coagulants and AI-Driven Dosing Transform North American Municipal Wastewater Treatment

The North American municipal wastewater treatment sector is rapidly shifting toward bio-based organic coagulants and smart dosing technologies, driven by environmental regulations, sludge disposal costs, and growing PFAS scrutiny. With the EPA’s 2024 alum discharge rule restricting landfilling of metal-laden sludge, utilities are embracing plant-derived polymers like Kemira’s Superfloc® BIO-100, which slashes sludge by 30% while maintaining 90% turbidity removal already operational at Los Angeles’ Hyperion Plant. Similarly, Canada’s Green Municipal Fund is financing the deployment of chitosan-based coagulants at Toronto’s Ashbridges Bay WWTP, resulting in a 40% cut in ferric chloride usage. Digital transformation further enhances performance and cost-efficiency; Evoqua’s SmartChem™ system, for instance, uses machine learning to dynamically optimize bio-coagulant dosing at Chicago’s Stickney Plant, achieving 15–20% chemical cost savings. These shifts not only align with USDA BioPreferred® product incentives but also support carbon reduction goals, as bio-coagulants lower lifecycle GHG emissions and unlock $50–100/ton in sludge handling cost reductions. As regulators continue tightening nutrient, sludge, and contaminant discharge limits, and as BIL funding prioritizes PFAS and biosolids reduction, the competitive advantage lies with suppliers offering sustainable chemistry integrated with smart dosing platforms.

Growth Opportunity: Modified Organic Coagulants for PFAS and Microplastic Removal

The emergence of PFAS and microplastics as priority contaminants in North American municipal wastewater has created a lucrative opportunity for modified organic coagulants, particularly those designed to enhance solid-liquid separation while targeting emerging pollutants. Technologies like Calgon’s PFAS-Select™ OCF, a chitosan-lignin hybrid coagulant, have demonstrated up to 95% PFAS removal from biosolids, enabling utilities to comply with the EPA’s stringent 4 ppt discharge limit a key concern for over 6,000 municipal plants. In parallel, BASF’s Zetag™ MP offers a next-gen solution for microplastic agglomeration, tested in San Francisco’s Oceanside Plant, and increasingly relevant due to Canada’s national single-use plastics ban and mounting pressure from consumer safety groups. Beyond contaminant capture, these organics also support nutrient recovery integration; for example, Ostara’s Pearl® system uses bio-coagulant-pretreated wastewater to enhance struvite crystallization, generating up to $500K annually in fertilizer revenue for medium-scale plants. As $10B in EPA BIL grants funnel into sludge and PFAS mitigation projects, utilities are actively seeking integrated, non-toxic, and circular water treatment solutions. Chemical manufacturers that bundle biopolymer technology with digital control platforms and collaborate with agri-tech innovators (e.g., Kemira + Cargill on corn-derived coagulants) are well-positioned to dominate this evolving segment.

North America Organic Coagulants Market for Municipal Wastewater Treatment – Competitive Analysis

The North America organic coagulants market for municipal wastewater treatment faces tough competition due to regulatory changes, climate demands, and digital upgrades. The competitive landscape features major specialty chemical leaders, including Solenis, Kemira, BASF, and SNF, who together hold over 65% of the market. These companies set themselves apart with unique formulations designed for municipal needs, such as Solenis’ coagulants for rain events and Kemira’s polymers for biosolid recovery. Their competitive edge is boosted by significant investments in smart treatment infrastructure. For instance, BASF uses AI-based dosage prevention, while SNF’s new plant in Georgia supports localized supply chains, which are important in today’s procurement environment.

Tier 2 companies are finding their niche by focusing on sustainable innovations. Firms like BioWater Tech and Accepta offer biodegradable or enzyme-enhanced solutions. Their products appeal to regulatory-compliant, low-carbon applications, which are perfect for decentralized and smaller plants, including systems used by tribal and coastal communities. Although these firms may not have the same scale, they make up for it through certification (NSF/OMRI), local biomass sourcing (such as shellfish and seaweed), and "Buy America" credentials, enabling them to qualify for federal infrastructure grants.

Meanwhile, Tier 3 is made up of over 15 regional commodity players that primarily serve rural municipalities and seasonal lagoon systems. They prioritize cost, providing products priced 30% lower than premium brands. Though they may not focus on innovation, their regional presence and pricing strategy help them secure bulk contracts, especially where regulatory standards are less strict or enforcement is weak.

Throughout the market, product types are becoming increasingly important. Synthetic PolyDADMAC still holds a significant 40% share, but marine-based chitosan and starch-based coagulants are rising in popularity due to carbon footprint regulations and the growing interest in bio-based procurement. Companies like BASF and SNF are introducing synthetic hybrids, indicating a shift towards PFAS-free options that maintain polymer effectiveness. New application areas, such as nutrient recovery, direct potable reuse, and resilience against wet weather, are also pushing the demand for tailored organic blends.

Strategically, leading companies are focusing on innovation that meets regulatory requirements and building resilient supply chains. For example, Solenis was the first to receive EPA verification for a PFAS-free coagulant. At the same time, Kemira uses carbon labeling and rail delivery to respond to climate risks. New municipal contracting models, like performance-based pricing, biosolid monetization, and co-financing for pilot programs, are becoming important for long-term partnerships and customer loyalty.

Looking towards 2025–2030, the market is expected to shift further. Bio-based coagulants are anticipated to reach a 35% market share, driven by climate policy and carbon accounting expectations. Automated dosing is predicted to achieve 60% market penetration through the use of sensors, digital twins, and blockchain-enabled traceability tools. Nutrient recovery, especially phosphorus harvesting, will provide additional value, allowing suppliers to charge 20% more through performance-based contracts. Overall, success in this market will depend on verified regulatory compliance, localized and climate-resilient supply strategies, and digital ecosystems that enhance chemical performance while driving operational savings.

North America Organic Coagulants Market for Municipal Wastewater Treatment– Segmentation Insights (2025–2034)

By Type of Organic Coagulant: Polyamines Dominate, Bio-Based Coagulants Accelerate Fastest

In the North American municipal wastewater treatment market, polyamines are expected to maintain dominance with a 2025 market share of approximately 39.2%, owing to their high cationic charge density and effectiveness in destabilizing colloidal particles. These coagulants are essential for reducing turbidity and enhancing sludge dewatering during primary and secondary clarification processes. Their widespread adoption in both large municipal treatment plants and decentralized systems makes them a cornerstone of chemically-assisted wastewater treatment.

Meanwhile, natural or bio-based coagulants are projected to be the fastest-growing segment with a robust CAGR of 11.2% through 2034, driven by growing municipal mandates focused on sustainability and green chemistry. Derived from plant extracts, chitosan, or starch-based polymers, these eco-friendly alternatives are gaining traction for being biodegradable and producing less chemical sludge. Adoption is notably increasing in progressive states like California and Washington, where utilities are integrating bio-based solutions into pilot projects and full-scale phosphorus removal programs to meet nutrient discharge regulations. Their use aligns with both environmental stewardship goals and circular economy principles.

.png)

By Application in Municipal Wastewater Treatment: Primary Treatment Leads, Tertiary Treatment Expands Rapidly

Primary treatment is set to remain the leading application area for organic coagulants, accounting for around 44.1% of the market in 2025. This segment benefits from high demand for coagulants in the removal of total suspended solids (TSS), biochemical oxygen demand (BOD), and floatable materials during the initial phase of municipal sewage processing. Organic coagulants like polyamines and polyDADMAC are preferred due to their ability to enhance sedimentation, reduce sludge volume, and minimize downstream load on secondary treatment systems.

On the growth side, tertiary treatment is forecast to expand at the fastest CAGR of 10.9%, fueled by the rising need for advanced nutrient removal, phosphorus polishing, and membrane filtration system support. Coagulants are increasingly used as pre-treatment chemicals before membrane filtration (e.g., MBR, RO) and in chemical phosphorus precipitation processes especially in plants targeting ultra-low nutrient discharge limits. This trend is reinforced by tightening effluent regulations under the Clean Water Act and state-level water quality targets in regions with sensitive receiving water bodies. As utilities seek to future-proof their infrastructure, chemical support for tertiary processes is gaining strategic priority.

North America Organic Coagulants Market for Municipal Wastewater Treatment Report Scope

North America Organic Coagulants Market for Municipal Wastewater Treatment

|

Parameter

|

Details

|

|

Market Size (2025)

|

$388.4 Million

|

|

Market Size (2034)

|

$961.8 Million

|

|

Market Growth Rate

|

10.6%

|

|

Segments

|

By Type of Organic Coagulant (Polyamines, PolyDADMAC, EPI-POLYAMINES, DICY Polymer, Natural/Bio-based Coagulants, Other Specialty Organic Coagulants), By Application in Municipal Wastewater Treatment (Primary Treatment, Secondary/Biological Treatment Support, Tertiary Treatment), By Form of Chemical (Liquid, Powder/Solid

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SNF Holding Company (U.S.), Ecolab Inc. (U.S.), Kemira Oyj (Finland), Solenis LLC (U.S.), BASF SE (Germany), Veolia Water Technologies (France), Kurita Water Industries Ltd. (Japan), Buckman (U.S.), USALCO (U.S.),

|

|

Countries

|

US, Canada, Mexico

|

North America Organic Coagulants Market for Municipal Wastewater Treatment Market Segmentation

By Type of Organic Coagulant

- Polyamines

- PolyDADMAC

- EPI-POLYAMINES

- DICY Polymer

- Natural/Bio-based Coagulants

- Other Specialty Organic Coagulants

By Application in Municipal Wastewater Treatment

- Primary Treatment

- Secondary/Biological Treatment Support

- Tertiary Treatment

By Form of Chemical

By Country

- United States

- Canada

- Mexico

Top Companies in North America Organic Coagulants Market for Municipal Wastewater Treatment

- SNF Holding Company (U.S.)

- Ecolab Inc. (U.S.)

- Kemira Oyj (Finland)

- Solenis LLC (U.S.)

- BASF SE (Germany)

- Veolia Water Technologies (France)

- Kurita Water Industries Ltd. (Japan)

- Buckman (U.S.)

- USALC(U.S.)

* List Not Exhaustive

Research Coverage

This report investigates the North America Organic Coagulants Market for Municipal Wastewater Treatment, delivering comprehensive analysis reviews on market dynamics, emerging regulations, and breakthrough technologies such as bio-based polymers and AI-driven dosing systems. It highlights innovation in PFAS and microplastic removal, sustainable coagulant formulations, and nutrient recovery strategies, making this report an essential resource for utilities, chemical manufacturers, and municipal planners. USDAnalytics provides detailed insights into competitive structures, pricing models, and the future role of smart and sustainable chemistry in wastewater treatment, ensuring professionals gain actionable intelligence for strategic decisions.

Key Research Details:

- Segmentation:

- By Type of Organic Coagulant: Polyamines, PolyDADMAC, EPI-POLYAMINES, DICY Polymer, Natural/Bio-based Coagulants, Other Specialty Organic Coagulants.

- By Application: Primary Treatment, Secondary/Biological Treatment Support, Tertiary Treatment.

- By Form: Liquid, Powder/Solid.

- Geographic Scope: United States, Canada, Mexico.

- Study Period: Historic data (2021–2024) and forecast data (2025–2034).

- Companies covered: SNF Holding Company (U.S.), Ecolab Inc. (U.S.), Kemira Oyj (Finland), Solenis LLC (U.S.), BASF SE (Germany), Veolia Water Technologies (France), Kurita Water Industries Ltd. (Japan), Buckman (U.S.), USALC (U.S.).

Methodology

USDAnalytics employs a hybrid research methodology combining primary interviews with municipal utility operators, wastewater engineers, and chemical suppliers, alongside secondary research from EPA, NACWA, and ASTM standards. Market size projections utilize a bottom-up approach, factoring in municipal wastewater flow rates, polymer usage intensity, and infrastructure upgrade cycles under the Bipartisan Infrastructure Law (BIL). Forecast models integrate econometric analysis with scenario-based assumptions, reflecting shifts toward bio-based chemistry, digital dosing systems, and PFAS compliance mandates. Rigorous data triangulation, leveraging procurement data, utility pilot case studies, and supplier financial reports, ensures the accuracy and reliability of our projections.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements