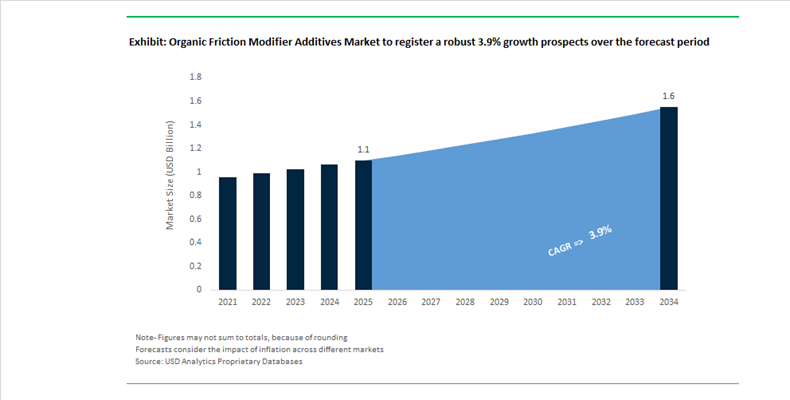

Organic Friction Modifier Additives Market Valued at $1.1 Billion in 2025 Projected to Reach $1.6 Billion by 2034 at 3.9% CAGR Driven by Fuel Economy Standards and Advanced Engine Lubrication

The Organic Friction Modifier Additives Market is valued at $1.1 billion in 2025 and is projected to reach $1.6 billion by 2034, expanding at a CAGR of 3.9%. Growth is closely linked to tightening global fuel economy regulations, evolution of engine hardware toward downsized turbocharged architectures, and the increasing complexity of transmission systems. Organic friction modifiers (OFMs) play a critical role in boundary lubrication regimes by forming adsorbed molecular films that reduce metal-to-metal contact, lower coefficient of friction, and enhance fuel efficiency. Demand is particularly strong in passenger car motor oils (PCMO), automatic transmission fluids (ATF), and heavy-duty lubricants engineered for extended drain intervals.

Regulatory milestones reshaped formulation strategies beginning in 2024. In July 2024, Lubrizol Corporation introduced Lubrizol® PV1710, designed to meet the new ILSAC GF-7 specification ahead of the March 31, 2025 licensing date. The technology integrates advanced organic friction modifiers to deliver improved chain-wear protection and measurable fuel economy gains in gasoline direct injection engines. In August 2025, Afton Chemical Corporation launched HiTEC® 65522, one of the first gasoline performance additive packages approved under the revised TOP TIER+™ Revision G standard. The formulation incorporates OFMs to optimize internal efficiency while controlling injector deposits in high-pressure systems.

A significant technological shift emerged in September 2025 when Afton Chemical introduced HiTEC® 12582, the first dedicated additive package for hydrogen-powered heavy-duty internal combustion engines. Hydrogen combustion introduces elevated water formation and altered lubricity conditions, requiring specialized organic friction modifier systems to maintain film integrity under diluted lubrication environments. In May 2025, Lubrizol expanded its transmission portfolio with AT9311, a multi-vehicle ATF additive leveraging robust OFM chemistry to ensure anti-shudder durability and consistent shift quality across diverse global transmission platforms. These innovations indicate that OFMs are evolving beyond conventional gasoline and diesel applications into alternative fuel architectures.

Research intensity within the sector intensified through 2025. Infineum International Limited advanced molecular-level research on OFMs, with Professor Pete Dowding receiving the ISIS Impact Award in 2025 for work utilizing neutron scattering and digital simulation to understand adsorption mechanisms. This research supports in-silico additive design, reducing experimental development cycles and enabling lower-carbon formulations. In November 2025, Infineum signed a strategic supply agreement with Rianlon Corporation to strengthen Asia-Pacific manufacturing resilience for friction modifiers and antioxidants. The company’s July 2025 Sustainability Report further highlighted the shift toward renewable feedstocks and circular raw materials for OFM production.

Corporate expansion and digital integration are reinforcing competitive positioning. In December 2025, Lubrizol opened a new office in São Paulo to support localized additive development for Latin American markets, where biofuel blends require adaptive friction chemistry. In early 2026, BASF SE inaugurated a global Digital Hub in Hyderabad, leveraging AI and analytics to optimize specialty organic additive synthesis. BASF disclosed in 2025 that over 15% of its 2024 sales originated from products launched within five years, underscoring rapid innovation cycles in additive chemistry. Late 2025 also saw Lubrizol introduce a zinc-free hydraulic additive incorporating modern organic friction control technologies, reflecting regulatory pressure to minimize metallic additives in environmentally sensitive applications such as marine and agricultural systems.

Organic Friction Modifier (OFM) Additives Market Trends and Opportunities

Trend: Adoption of OFMs in Ultra-Low Viscosity (0W-8 and 0W-12) Engine Oils

The transition toward ultra-low viscosity engine oils is reshaping additive demand dynamics across the global lubricants value chain. Driven by the final Corporate Average Fuel Economy standards issued by the National Highway Traffic Safety Administration for model years 2024–2031, OEMs are increasingly specifying 0W-8 and emerging 0W-12 formulations to reduce parasitic losses and meet a 50.4 mpg fleet-wide fuel economy target by 2031. While viscosity reduction delivers a measurable 2% to 3% improvement in fuel efficiency compared with conventional 0W-20 oils, it also pushes engine operation closer to boundary lubrication conditions. This has elevated organic friction modifiers from optional performance enhancers to structurally essential formulation components.

Testing programs conducted during 2024–2025 show that ultra-low viscosity oils require higher OFM treat rates, typically between 0.1% and 1.0%, to compensate for reduced hydrodynamic film thickness in valvetrain and piston ring contacts. The introduction of the JASO GLV-1 standard in early 2025 further reinforces this shift by mandating fuel economy improvements exceeding 1.1% under firing conditions versus 0W-16 reference oils. To achieve these benchmarks without compromising emission system durability, formulators are prioritizing ash-free organic molybdenum complexes, fatty acid amides, and high-polarity ester-based OFMs. Independent engine studies at SwRI during this period confirm that these chemistries effectively close the “friction gap” created by viscosity thinning, making OFMs a central lever for OEM compliance strategies rather than a secondary additive choice.

Trend: Shift Toward Ashless and Metal-Free OFMs for EV Drivetrain Fluids

Electrification is redefining the functional requirements of friction modifiers, particularly in electric and hybrid drivetrains where lubricant formulations must balance tribological performance with electrical insulation. High-speed electric motors operating above 20,000 rpm place stringent demands on dielectric strength and thermal stability, rendering traditional sulfurized or metal-containing friction modifiers unsuitable. Patent disclosures in 2025 from additive developers including Lubrizol and Afton Chemical illustrate a clear pivot toward ashless, metal-free organic esters and nitrogen-functional OFMs that reduce friction while preserving low electrical conductivity.

Copper compatibility has emerged as a decisive qualification criterion, as EV motors and integrated e-axles contain extensive copper windings. New OFM chemistries introduced in late 2024 are engineered to achieve a “1A” copper strip corrosion rating, addressing one of the most critical failure risks in e-fluid applications. Market structure further reinforces this trend, as hybrids and plug-in hybrids accounted for roughly three-quarters of EV fluid demand in 2024. These platforms require multifunctional OFMs capable of handling frequent cold starts, intermittent engine operation, and continuous protection of electric drive components. As a result, branched diester OFMs and polymer-assisted organic systems are gaining share, positioning ashless OFMs as the default friction control solution for next-generation driveline fluids.

Opportunity: Bio-Derived OFMs for Environmentally Acceptable Lubricants

Regulatory mandates are transforming bio-derived friction modifiers from niche sustainability options into core compliance tools. The U.S. EPA Vessel General Permit requires the use of Environmentally Acceptable Lubricants in all oil-to-water interfaces on commercial vessels exceeding 79 feet, effectively guaranteeing baseline demand for biodegradable OFMs in marine applications. Vegetable oil esters and synthetic bio-esters are increasingly specified as friction modifiers in stern tubes, thrusters, and deck machinery, where leakage risk is unavoidable and environmental liability is high.

Performance benchmarking of bio-based OFM systems demonstrates that modern formulations can exceed 95% biodegradability under OECD 301B testing, well above the regulatory threshold for ready biodegradability. Products such as those marketed by FUCHS illustrate that high lubricity and friction reduction can be achieved without sacrificing environmental performance. Beyond maritime uses, forestry and agricultural equipment operators are adopting natural oil-based OFMs to mitigate soil contamination risks and reduce long-term remediation exposure. This regulatory and liability-driven demand is creating a durable premium segment for bio-derived OFMs, particularly among operators seeking to strengthen ESG reporting credentials.

Opportunity: High-Temperature Stable OFMs for Aerospace and Performance Racing

Rising power densities in aerospace and motorsport applications are opening a high-margin niche for OFMs capable of surviving extreme thermal and shear conditions. Advanced aircraft engines and racing powertrains expose lubricants to intermittent temperatures far beyond the stability limits of conventional organic additives. While surface engineering solutions such as ceramic coatings protect metal substrates, friction modifiers must maintain adsorption strength and avoid carbonization under transient high-heat exposure.

Research programs at institutions including Imperial College London are using laser-induced fluorescence and infrared thermography to characterize OFM film behavior at shear rates exceeding 10⁷ s⁻¹, providing critical insights into molecular design requirements for next-generation additives. Parallel work documented by NASA Glenn Research Center highlights growing interest in solid-organic hybrid lubrication systems, where OFMs are embedded within polymer composites to deliver self-lubricating performance at temperatures up to 350°C. These developments position thermally robust OFMs as enabling materials for aerospace transmissions, high-speed bearings, and elite motorsport engines, where reliability under extreme conditions carries disproportionate economic and safety value.

Organic Friction Modifier Additives Market Share and Segmentation Insights

Organic Molybdenum Compounds Lead Friction Modifier Additive Demand in Advanced Lubricant Formulations

Organic molybdenum compounds accounted for 34.80% of the Organic Friction Modifier Additives Market by type in 2025, making them the most widely used friction reduction additives in modern lubricant systems. Compounds such as molybdenum dithiocarbamate and trinuclear molybdenum deliver superior friction reduction and wear protection by forming low-friction boundary films on metal surfaces under high-load conditions. These additives are critical in automotive lubricants designed to improve fuel efficiency and engine durability. In 2025, lubricant formulators are increasingly focusing on low-viscosity engine oil optimization, where ultra-low viscosity grades such as 0W-16 and 0W-20 require advanced organic molybdenum additives with enhanced solubility, thermal stability, and compatibility with high-performance synthetic base oils.

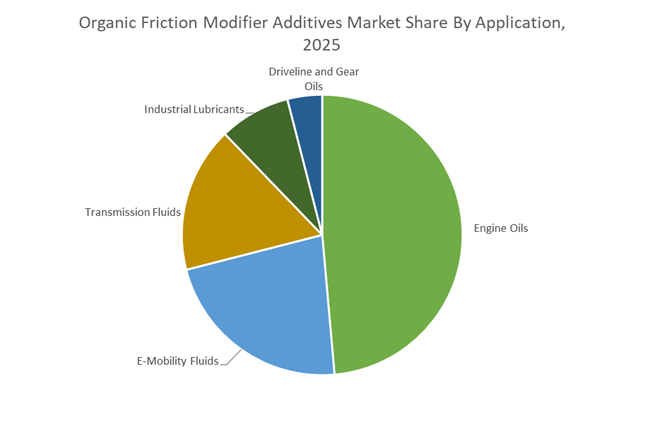

Engine Oils Segment Dominates Organic Friction Modifier Consumption in Automotive Lubricants

Engine oils represented 48.60% of the Organic Friction Modifier Additives Market by application in 2025, reflecting the extensive use of friction modifiers in passenger vehicles and heavy-duty transportation fleets. These additives reduce internal engine friction, improve mechanical efficiency, and help automotive manufacturers meet stringent fuel economy regulations such as CAFE and WLTP standards. The global scale of automotive lubricant consumption continues to drive demand for high-performance friction modifier additives. A significant 2025 market trend is the emergence of e-mobility lubricant applications, where organic friction modifiers are incorporated into electric drive unit fluids to support wet clutch compatibility, gear protection, and electrical property control in electric vehicle transmission systems.

Organic Friction Modifier Additives Market Competitive Landscape

The organic friction modifier additives market in 2026 is driven by ultra-low viscosity engine oils, electrified drivetrain fluids, and bio-sourced additive chemistries. Competitive advantage lies in advanced tribofilm engineering, dielectric-compatible OFMs, and mass-balance certified polymers that enhance fuel economy, wear protection, and OEM compliance.

Lubrizol accelerates GF-7 compliant additive innovation with EV-focused friction modifier platforms

Lubrizol is strengthening its leadership in organic friction modifier additives through API SQ and ILSAC GF-7 compliant solutions tailored for modern hybrid and electrified powertrains. The launch of Lubrizol® PV1710 delivers advanced OFM chemistry for enhanced boundary lubrication and engine protection under ultra-low viscosity conditions. Its Oléane™ GTL friction modifier addresses EV drivetrain requirements, combining low friction with high thermal stability for e-axle cooling fluids. Expansion of its Bangkok innovation center enhances regional R&D and application development in Asia-Pacific. The introduction of biodegradable Carbopol® BioSense Polymer highlights its shift toward sustainable, eucalyptus-derived materials. This integrated innovation strategy positions Lubrizol at the forefront of next-generation friction modifier technologies.

Infineum advances tribofilm science to enable ultra-low viscosity lubricant performance and durability

Infineum is leading in boundary lubrication science through its ultra-low viscosity (ULV) technology platform, designed to maintain wear protection in low HTHS oil formulations. Its research on mixed acylglycerols demonstrates improved tribofilm thickness and durability across temperature ranges, enhancing engine efficiency. The company is actively driving development of PC-12 heavy-duty engine oil standards, requiring high-performance organic additives for extended drain intervals. Its solutions also address marine fuel stability, reducing sludge formation and improving operational efficiency. Infineum’s deep R&D focus on tribochemistry and additive synergy strengthens its position in advanced lubricant formulations. This scientific leadership enables high-performance OFMs for future mobility systems.

Afton Chemical enhances hybrid engine efficiency through rapid film-forming organic friction modifiers

Afton Chemical is focusing on high-efficiency OFMs designed for modern gasoline and hybrid engines, leveraging over two decades of OEM-aligned testing expertise. Its friction modifiers are engineered to provide rapid boundary film formation, addressing cold-start wear challenges in hybrid powertrains. The company reports 5–8% efficiency gains through optimized additive packages, supporting fuel economy targets. Its biodiesel-focused solutions mitigate injector deposits and filtration issues in renewable fuel systems. Afton’s GPA portfolio expansion reinforces its presence in high-performance fuel and lubricant additives. This performance-driven strategy positions Afton as a key player in next-generation engine lubrication.

BASF integrates Verbund scale and polyether innovation to deliver low-carbon high-efficiency friction modifiers

BASF is leveraging its Verbund infrastructure and chemical integration to develop high-performance organic friction modifiers aligned with future mobility requirements. Its Energy Efficiency Booster (EEB) technology utilizes polyether-based structures to exceed traditional PAO performance in reducing friction. The Zhanjiang Verbund site ensures localized supply of advanced lubricant additives across Asia-Pacific. With a projected EBITDA of €6.2–€7.0 billion in 2026, BASF continues to invest in high-margin specialty additives. Its Scopeblue label highlights products with significantly reduced carbon footprints, supporting sustainability mandates. This combination of innovation, scale, and carbon transparency strengthens BASF’s competitive position.

Croda leads bio-based friction modifier innovation with high-performance polymeric additives and NPP growth

Croda is advancing organic friction modifier technology through its naturally derived polymer platforms, particularly the Perfad™ series. Products like Perfad FM 3336 deliver up to 2.6% fuel economy improvement and outperform traditional GMO additives by 30% in thermal stability. Its polymeric additives provide superior performance across wider temperature ranges, making them ideal for ultra-low viscosity formulations. Croda is also targeting regulatory-driven markets with bio-based alternatives to chlorinated paraffins, such as Perfad 8100 for metalworking fluids. With a 10% increase in NPP sales, the company is focusing on patented, high-margin innovations. This strategy positions Croda as a leader in sustainable, high-performance friction modifier additives.

United States – Regulatory Pull and Advanced Powertrain Optimization

The United States organic friction modifier additives industry is being reshaped by regulatory upgrades and rapid powertrain evolution. Effective March 2025, the introduction of the API SQ category has materially raised performance thresholds for engine oils, requiring measurable fuel efficiency gains in the range of 5 to 8% for 2026 vehicle platforms. This has directly increased treat rates of organic friction modifier additives in passenger car motor oils, particularly for ultra-low-viscosity grades designed to minimize hydrodynamic losses. Product innovation has accelerated accordingly. The Lubrizol Corporation launched Lubrizol® PV1710 in late 2025, a formulation aligned with ILSAC GF-7 requirements that simultaneously mitigates low-speed pre-ignition in gasoline direct injection engines while sustaining high friction-reduction efficiency under boundary lubrication regimes.

Infrastructure and compliance investments reinforce this shift. Afton Chemical completed a major upgrade to its mechanical testing laboratory in 2025, enabling simulation of extreme shock-load conditions relevant to dual-clutch transmission applications where organic polymeric friction modifiers are increasingly critical. Parallel Environmental Protection Agency guidelines for 2025–2026 emphasizing industrial efficiency and PFAS-free formulations are accelerating the transition toward biodegradable ester-based organic modifiers in open gear and industrial lubricant systems. Looking ahead, U.S. formulators are prioritizing specialized OFMAs for e-axle fluids, where friction reduction must be balanced with dielectric strength and material compatibility in electrified drivetrains.

China – Localized Capacity and Ultra-Low-Viscosity Migration

China has emerged as the most strategically important growth market for organic friction modifier additives due to its dominance in electrified vehicle production and rapid migration to advanced transmission architectures. In 2024–2025, BASF SE established a high-capacity fuel performance additives facility in Shanghai, localizing the production of organic friction modifiers to serve domestic OEMs and lubricant blenders at scale. This investment aligns with China’s vehicle mix, where dual-clutch and continuously variable transmissions accounted for roughly two-thirds of light-vehicle production in 2024. Government and OEM priorities are increasingly focused on fluids with narrow frictional windows to prevent clutch shudder and torque interruption, elevating the role of precisely engineered OFMAs.

Regulatory pressure further amplifies demand. Implementation of China VI-b emission standards for 2025–2026 has driven a market-wide shift toward 0W-16 and 0W-12 engine oils, where maintaining protective films under ultra-thin lubrication conditions is not feasible without high-performance organic friction modifiers. Capacity expansion by Chevron Oronite at its Ningbo site in 2025 added dedicated production lines for dispersant-inhibitor packages integrating advanced OFMAs, underscoring China’s role as both a consumption and production hub for next-generation friction-reducing chemistries.

United Kingdom and Europe – Molecular Insight and Carbon Reduction Imperatives

The United Kingdom and broader European market is distinguished by fundamental research leadership and regulatory-driven formulation change. In March 2025, Infineum, in collaboration with the University of Cambridge, unveiled an advanced beamline tribometer capable of visualizing organic friction modifier adsorption at the molecular level under real engine pressures. This capability represents a step change in understanding boundary lubrication behavior and is accelerating the design of OFMAs with higher surface affinity and durability.

Climate policy reinforces this research focus. UK-based studies published in 2025 highlighted that incremental improvements in OFMA efficiency could translate into global carbon dioxide reductions of approximately 50 million metric tons annually, elevating friction modifiers from a formulation detail to a systemic decarbonization lever. Infineum’s work on biofuel compatibility further demonstrated that optimized OFMA packages in B20 and B30 fuel systems can deliver meaningful fuel efficiency gains over mineral-based baselines. Enactment of Euro 7 particulate limits in 2025 is indirectly pushing European formulators toward OFMA-rich low-SAPS lubricants to protect exhaust gas recirculation and gasoline particulate filter systems without compromising frictional performance.

Singapore – ASEAN Innovation and Marine Lubrication Transition

Singapore is consolidating its role as the ASEAN innovation and supply hub for organic friction modifier additives, with a dual focus on automotive and marine applications. In late 2025, The Lubrizol Corporation opened its Southeast Asia Innovation Center in Jurong, dedicated to localized coatings and specialty organic solutions engineered for high-humidity, high-temperature operating environments typical of the Asia Pacific region. This facility strengthens regional development of OFMAs tailored to local fuel qualities and duty cycles.

Marine lubrication is an additional growth vector. Singapore’s maritime authority introduced Green Port incentives in 2025, favoring vessels that deploy bio-based organic friction modifiers in cylinder lubricants to reduce frictional drag and fuel consumption. Supply chain capacity is expanding in parallel. Infineum increased production capacity at its Singapore facility during 2024–2025 to serve growing demand from Indian and ASEAN vehicle fleets, positioning the city-state as a critical node for friction-reducing additive distribution.

Brazil – Bio-Based Polymers and Natural-Origin Mandates

Brazil’s organic friction modifier additives market is being driven by sustainability policy and abundant bio-based feedstocks. In March 2025, The Lubrizol Corporation partnered with Suzano to introduce the Carbopol® BioSense platform, a biodegradable organic polymer derived from eucalyptus designed for diverse friction-modifying applications. This collaboration exemplifies Brazil’s ability to translate forestry and biomass advantages into high-performance additive chemistries.

Policy alignment is reinforcing adoption. Brazil’s environmental framework for 2025–2026 prioritizes industrial chemicals with up to 98% natural-origin content, accelerating substitution away from molybdenum-based inorganic modifiers toward organic fatty acids and bio-polymers. These mandates are influencing lubricant formulation across automotive, industrial, and agricultural machinery segments, positioning Brazil as a testbed for large-scale deployment of renewable organic friction modifier technologies.

Strategic Country Comparison – Organic Friction Modifier Additives

Organic Friction Modifier Additives Market County Level Snapshot

|

Country / Region

|

Primary Driver

|

Technology Emphasis

|

Strategic Position

|

|

United States

|

API SQ and GF-7 compliance

|

LSPI-safe OFMAs, e-axle fluids

|

Regulatory-led innovation hub

|

|

China

|

China VI-b and EV scale

|

Ultra-low-viscosity OFMAs

|

Largest consumption and production base

|

|

UK and Europe

|

Euro 7 and CO2 reduction

|

Molecularly optimized OFMAs

|

Research-driven formulation leader

|

|

Singapore

|

ASEAN growth and marine policy

|

Bio-based friction modifiers

|

Regional innovation and supply hub

|

|

Brazil

|

Natural-origin mandates

|

Bio-polymers and fatty acids

|

Sustainability-led adoption market

|

Organic Friction Modifier Additives Market Report Scope

Organic Friction Modifier Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.1 Billion

|

|

Market Size (2034)

|

$1.6 Billion

|

|

Market Growth Rate

|

3.9%

|

|

Segments

|

By Type (Organic Fatty Acids, Fatty Nitrogen Compounds, Ester-Based Friction Modifiers, Organic Polymer Friction Modifiers, Organic Molybdenum Compounds), By Form (Liquid, Solid), By Application (Engine Oils, Transmission Fluids, Driveline and Gear Oils, E-Mobility Fluids, Industrial Lubricants), By End-User Industry (Automotive, Aerospace, Marine, Manufacturing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Lubrizol, Infineum, Afton Chemical, Chevron Oronite, BASF, Evonik Industries, Croda International, Vanderbilt Chemicals, Dover Chemical, King Industries, Italmatch Chemicals, LANXESS, ADEKA, Sanyo Chemical Industries, Clariant

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Organic Friction Modifier Additives Market Segmentation

By Type

- Organic Fatty Acids

- Fatty Nitrogen Compounds

- Ester-Based Friction Modifiers

- Organic Polymer Friction Modifiers

- Organic Molybdenum Compounds

By Form

By Application

- Engine Oils

- Transmission Fluids

- Driveline and Gear Oils

- E-Mobility Fluids

- Industrial Lubricants

By End-User Industry

- Automotive

- Aerospace

- Marine

- Manufacturing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Organic Friction Modifier Additives Industry

- Lubrizol

- Infineum

- Afton Chemical

- Chevron Oronite

- BASF

- Evonik Industries

- Croda International

- Vanderbilt Chemicals

- Dover Chemical

- King Industries

- Italmatch Chemicals

- LANXESS

- ADEKA

- Sanyo Chemical Industries

- Clariant

*- List not Exhaustive