Ortho Phthalaldehyde Market Driven by Healthcare Sterilization Modernization and Safety-Centric Reformulation

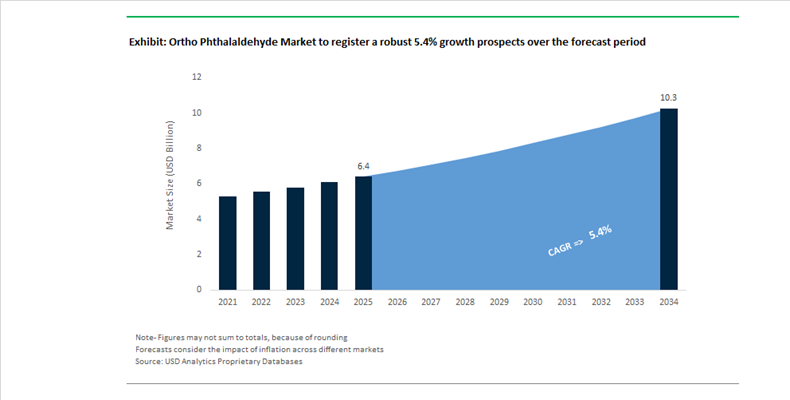

The Ortho Phthalaldehyde (OPA) Market Valued at $6.4 Billion in 2025 Projected to Reach $10.3 Billion by 2034 at 5.4% CAGR is structurally anchored in high-level disinfection (HLD), analytical chemistry, and specialty aldehyde synthesis. OPA functions as a potent biocidal aldehyde for cold sterilization of heat-sensitive medical devices—particularly flexible endoscopes—and as a derivatization reagent in amino acid analysis. Between 2024 and 2026, the market has been shaped by hospital automation, regulatory scrutiny of aldehyde exposure, and expansion of pharmaceutical-grade production capacity in Asia-Pacific and North America.

In January 2025, Sigma-Aldrich introduced a high-purity OPA reagent portfolio targeting clinical diagnostics and pharmaceutical R&D. Ultra-low impurity thresholds are increasingly required in chromatography and fluorescence-based assays, particularly in biologics manufacturing and peptide quantification. Simultaneously, Advanced Sterilization Products expanded its production capacity for Cidex® OPA to address growing global demand as hospitals phase out high-temperature sterilization for delicate optical and polymer-based surgical instruments. OPA remains a preferred high-level disinfectant because it achieves broad-spectrum antimicrobial efficacy without the corrosiveness associated with glutaraldehyde.

Worker safety and regulatory oversight are redefining product engineering. The National Institute for Occupational Safety and Health initiated a multi-year occupational exposure study through 2025 to evaluate respiratory and dermal risks linked to OPA vapor exposure in clinical settings. This research is accelerating the deployment of closed-loop delivery systems and automated reprocessors to minimize direct handling. By early 2026, companies such as STERIS and Metrex Research integrated OPA-compatible automated HLD (AHLD) systems into their latest platforms, significantly reducing operator exposure while ensuring cycle reproducibility in high-throughput hospitals. These automated systems are becoming standard in tertiary care facilities across North America, Europe, and the Gulf region.

Regulatory dynamics are influencing regional demand patterns. In 2026, Oman reported strong compliance with Ministerial Decision 184/2020 on infection control, accelerating OPA adoption in Muscat and Salalah healthcare systems. Meanwhile, the European Chemicals Agency postponed its decision on certain ethanol-based biocides in late 2025. This delay indirectly sustains aldehyde-based disinfectants’ market share across the European Union, as hospitals maintain validated OPA workflows pending further regulatory clarity. In the United States, Washington State’s 2025 restrictions on formaldehyde releasers reinforce a broader aldehyde-safety discourse, positioning OPA as a comparatively lower-volatility alternative in industrial microbial control applications.

Supply-side strengthening is underway in Asia. BASF commenced core production at its Zhanjiang Verbund site in late 2025, providing aromatic intermediates critical for localized OPA synthesis. In early 2026, MP Biomedicals and ACTO GmbH confirmed expanded pharma-grade OPA output in Asia-Pacific to support modernization of hospital infrastructure in developing markets.

Ortho Phthalaldehyde (OPA) Market Trends and Opportunities: Regulatory Substitution Momentum and Smart Reprocessing Ecosystems

Regulatory Crackdown on Glutaraldehyde Accelerating OPA Adoption in High-Level Disinfection

The Ortho Phthalaldehyde (OPA) market is experiencing accelerated adoption driven by intensifying global regulatory scrutiny on glutaraldehyde-based disinfectants, particularly concerning occupational exposure and respiratory sensitization risks. Regulatory bodies are shifting toward frameworks that prioritize acute sensory irritation and immediate health impacts, positioning OPA as a safer, next-generation aldehyde disinfectant with a superior toxicological profile.

The December 2025 update from the U.S. Environmental Protection Agency (EPA) marked a pivotal regulatory inflection point, reinforcing the transition toward low-vapor-pressure, activation-free disinfectants. Unlike glutaraldehyde, OPA does not require complex activation protocols or vapor containment systems, significantly reducing compliance burdens in hospital sterilization units. This regulatory realignment is directly influencing procurement strategies, particularly in high-throughput healthcare environments.

From an operational standpoint, OPA has emerged as the benchmark for irritant-minimized disinfection environments, supported by its chemical stability across a broad pH range (pH 3–9). This eliminates the frequent neutralization failures associated with glutaraldehyde in alkaline conditions, enhancing process reliability. Adoption data underscores this trend, with over 60% of Tier-1 hospitals in emerging markets transitioning to OPA-based reprocessing systems by 2025, achieving up to 30% reduction in chemical waste while improving workforce safety metrics. This positions OPA as a core component in sustainable hospital disinfection protocols and regulatory-compliant sterilization workflows.

Supply Chain Concentration and Cost Pressures Driving Nearshoring Strategies in OPA Production

The global OPA supply chain is characterized by high geographic concentration in the Asia-Pacific region, creating systemic vulnerabilities for medical-grade disinfectant supply continuity. As of 2025, approximately 45.8% of global OPA production is concentrated in Asia-Pacific, with China and India serving as key suppliers of ≥99% purity OPA required for high-level disinfection applications. This concentration introduces a single-point-of-failure risk, particularly in the context of geopolitical shifts and trade policy realignments.

Recent trade developments in 2026, including tariffs on critical chemical intermediates, have increased input cost structures, contributing approximately 0.5 percentage points to inflation for downstream medical chemical manufacturers. This has triggered a strategic pivot toward nearshoring and domestic production incentives, particularly across North America and Europe, as companies seek to de-risk supply chains and ensure uninterrupted access to critical sterilization chemicals.

Cost dynamics further complicate the landscape, with average production costs for high-purity OPA reaching $3,000 per ton. To maintain competitiveness, approximately 20% of manufacturers are adopting advanced manufacturing technologies, including automated flow reactors and physical AI-driven process optimization, to enhance yield efficiency and reduce labor dependency. These advancements are reshaping the competitive dynamics of the OPA market, where supply resilience and production efficiency are becoming key differentiators.

Growth of OPA-Integrated Automated Endoscope Reprocessors and Smart Sterilization Systems

A major opportunity in the OPA market lies in the integration of OPA chemistry with advanced automated reprocessing systems, particularly for heat-sensitive and complex medical devices such as flexible endoscopes. The increasing procedural volume in minimally invasive diagnostics is driving demand for Automated Endoscope Reprocessors (AERs) that can deliver consistent, validated high-level disinfection using OPA.

Recent hardware innovations are accelerating this transition. In June 2025, STERIS introduced dual-basin AER systems, enabling parallel or independent disinfection cycles optimized for OPA contact time and distribution across intricate device geometries. These systems are designed to ensure uniform chemical exposure within narrow lumens, addressing a critical challenge in endoscope reprocessing.

Parallel to hardware advancements, digital traceability and smart sterilization ecosystems are gaining traction. Leading players such as Advanced Sterilization Products (ASP) are expanding capabilities in real-time monitoring of Minimum Effective Concentration (MEC), enabling automated validation of OPA efficacy during each disinfection cycle. This aligns with increasing regulatory requirements for data-logged compliance and audit-ready sterilization records.

Clinical evidence further reinforces this shift. Studies indicate that automation in reprocessing can reduce human error by up to 80%, prompting healthcare facilities to integrate OPA-based systems directly with hospital information management systems (HIMS). This convergence of chemical disinfection, automation, and digital compliance is creating a high-growth segment within the OPA market, centered on smart, connected sterilization infrastructure.

Next-Generation OPA Formulations: Faster Acting, Low-Concentration, and Sustainable Disinfection Solutions

Innovation in formulation chemistry is unlocking new growth pathways through the development of next-generation OPA disinfectants that offer faster cycle times, enhanced stability, and reduced environmental impact. These advancements are addressing key procurement priorities in healthcare systems, including efficiency, cost optimization, and sustainability compliance.

In January 2025, Sigma-Aldrich (under Merck KGaA) launched high-stability OPA formulations engineered to reduce odor intensity while maintaining rapid disinfection cycles of 10–12 minutes, a substantial improvement over traditional 45-minute glutaraldehyde protocols. This reduction in turnaround time significantly enhances instrument utilization rates and operational throughput in busy clinical settings.

Stability improvements are equally transformative. Modern OPA solutions can now be reused for up to 14 days, provided MEC validation is maintained using standardized test strips. Advanced formulation techniques, including Design of Experiments (DoE)-driven optimization, ensure sustained antimicrobial efficacy against resistant organisms such as Bacillus subtilis and mycobacteria, even after repeated use cycles.

Sustainability considerations are further driving innovation in packaging and dosing systems. The introduction of pre-measured, single-use OPA formulations tailored for AER systems minimizes overuse, reduces chemical waste, and aligns with hospital procurement policies focused on environmental footprint reduction. These developments position next-generation OPA solutions as a high-performance, eco-efficient alternative, supporting the broader transition toward green healthcare infrastructure and circular chemical usage models.

Ortho Phthalaldehyde Market Share and Segmentation Insights

Liquid OPA Formulations Dominate Market Demand in Medical Instrument Disinfection Systems

Liquid formulations accounted for 72.80% of the Ortho Phthalaldehyde Market by form in 2025, reflecting their widespread use in healthcare disinfection procedures. Ortho phthalaldehyde is commonly supplied as ready-to-use or concentrated liquid solutions that enable precise dilution and direct application in high-level disinfection workflows. Liquid OPA formulations are compatible with automated endoscope reprocessors and manual immersion systems used in hospitals and ambulatory surgery centers for processing heat-sensitive medical devices. In 2025, the industry has focused on stabilized liquid OPA formulations, incorporating optimized pH buffers and stabilizing agents that extend shelf life, maintain antimicrobial activity over repeated use cycles, and improve operational cost efficiency for high-volume medical instrument sterilization programs.

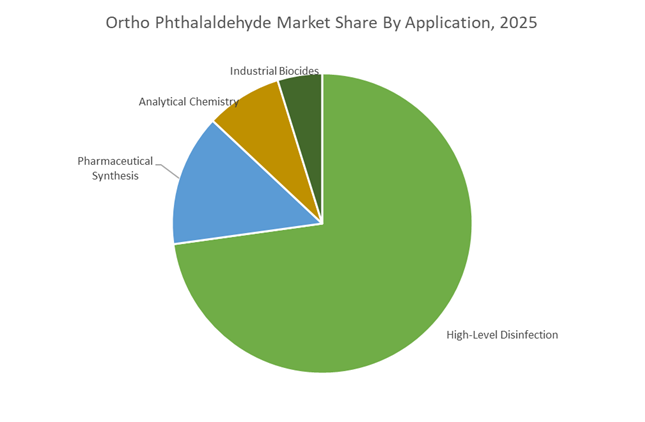

High-Level Disinfection Segment Drives OPA Consumption in Endoscope Reprocessing and Medical Equipment Sterilization

High-level disinfection represented 72.80% of the Ortho Phthalaldehyde Market by application in 2025, making it the primary use case across healthcare facilities and diagnostic laboratories. OPA has become a preferred disinfectant for reprocessing flexible endoscopes and other heat-sensitive medical instruments due to its strong mycobactericidal activity, rapid microbial kill performance, and compatibility with delicate medical device materials. The large number of endoscopic procedures performed globally continues to sustain strong demand for high-performance disinfectants. A major 2025 industry development is the integration of automated endoscope reprocessing systems, where OPA formulations are optimized for compatibility with automated cycles that deliver consistent disinfection while reducing operator exposure and improving workplace safety in clinical environments.

Ortho-Phthalaldehyde Market Competitive Landscape

The Ortho-Phthalaldehyde (OPA) Market is defined by integrated disinfection ecosystems, high-purity analytical reagents, and automated delivery systems. Leading players are focusing on closed-loop reprocessing technologies, proteomics-grade OPA chemicals, and healthcare safety compliance to address rising demand across medical device sterilization and biochemical analysis.

ASP leads automated OPA disinfection ecosystems with CIDEX and AER integration

Advanced Sterilization Products (ASP) dominates the OPA market through its integrated high-level disinfection (HLD) ecosystem centered around the CIDEX™ OPA Solution. The product remains an industry benchmark with validated 12-minute manual and 5-minute automated reprocessing cycles, widely adopted in endoscope sterilization. ASP’s expansion of OPA and hydrogen peroxide production capacity supports rising demand across Asia-Pacific and Latin America. Its AEROFLEX™ automated endoscope reprocessor enhances digital traceability and sterility assurance, reducing human error in clinical workflows. A key differentiator is ASP’s extensive device compatibility database, ensuring safe interaction with sensitive fiber-optic medical equipment. This combination of chemistry, automation, and validation infrastructure solidifies ASP’s leadership in healthcare disinfection systems.

Nanosonics scales closed-loop OPA disinfection systems with recurring consumables growth

Nanosonics Limited is disrupting the OPA market by integrating chemical disinfection into automated hardware platforms, particularly in ultrasound probe reprocessing. The company reported $198.6 million in FY25 revenue, with 17% growth driven by a 20% increase in recurring consumables, including OPA-based disinfectants. Its trophon®3 and trophon®2 Plus systems deliver 40% faster cycle times and advanced DICOM integration for seamless hospital data traceability. The “Protection by Design” approach ensures closed-loop disinfection, minimizing healthcare worker exposure to OPA vapors and converting waste into safer byproducts. With over 37,000 installed units globally and strong North American adoption, Nanosonics is building a scalable, device-integrated disinfection ecosystem. This recurring revenue model enhances long-term market penetration.

Merck delivers proteomics-grade OPA reagents for high-precision biochemical analysis

Merck KGaA is a key player in the analytical-grade OPA segment, supplying ultra-high-purity reagents for proteomics, pharmaceutical R&D, and biochemical testing. Through Sigma-Aldrich, the company introduced ≥99% purity OPA reagents optimized for HPLC and amino acid quantification, addressing demand for precision in protein analysis workflows. Its expertise in fluorometric detection enables highly sensitive reactions with primary amines, critical for modern drug development. Following its 2026 restructuring, Merck streamlined its OPA portfolio under the Science & Lab Solutions unit to improve global supply chain efficiency. Strict control over physicochemical specifications ensures consistency in automated laboratory systems. This focus on high-purity, research-grade organics positions Merck strongly in life sciences applications.

Metrex leverages GPO partnerships to expand high-volume OPA disinfection in hospitals

Metrex Research, LLC is strengthening its position in healthcare disinfection through large-scale institutional partnerships and high-efficiency OPA formulations. Its MetriCide™ OPA Plus solution is optimized for high-volume hospital settings, offering a 30-day reuse life and rapid 12-minute disinfection cycle, improving operational efficiency. Strategic alignment with Premier Inc. provides access to approximately 4,100 hospitals and 200,000 healthcare providers, ensuring strong market penetration in the U.S. Recognition as Infection Prevention Solutions Company of the Year underscores its focus on domestic manufacturing and infection control innovation. Ongoing collaboration with Solvay supports material compatibility testing for next-generation medical devices. This combination of distribution strength and product efficiency enhances Metrex’s competitive advantage.

Evonik targets industrial OPA applications through specialty intermediates and custom synthesis

Evonik Industries AG competes in the industrial-grade OPA segment by focusing on specialty intermediates and custom synthesis for advanced materials applications. Its Advanced Technologies segment, generating €5.97 billion in 2025, supports demand for OPA in polymerization, photoresists, and specialty coatings. The company operates as a B2B technical partner, supplying bulk OPA for semiconductor and industrial manufacturing processes. Through its “Evonik Tailor Made” program, it is optimizing its production network and prioritizing expansion in high-growth markets such as China and India. Strong free cash flow of €695 million in 2025 provides financial flexibility for investment in sustainable production technologies. Its emphasis on green chemistry and low-waste catalytic processes positions Evonik for long-term competitiveness in specialty chemicals.

China – Capacity Control, Vertical Integration, and Medical-Grade Expansion

China’s ortho phthalaldehyde industry is characterized by scale, upstream integration, and rapid alignment with medical-grade demand. As of 2025, leading domestic producers such as Richap Chem and Wanxiang Chemical collectively account for more than one-third of global OPA production capacity, underpinned by China’s cost-efficient chemical manufacturing ecosystem. Temporary suspension of select export control measures by Ministry of Commerce of the People's Republic of China between late 2025 and late 2026 has improved the flow of OPA intermediates into international markets, reinforcing China’s role as a supply stabilizer during a period of energy and logistics volatility.

Operationally, Chinese producers are deepening vertical integration into o-xylene precursors to manage margin exposure amid fluctuating utility and feedstock costs. Environmental enforcement is simultaneously reshaping production. New 2026 regulations in Yangtze River Delta chemical parks mandate advanced VOC capture in aldehyde synthesis, accelerating investments in closed-reactor systems. On the demand side, newly commissioned high-purity liquid OPA lines in Ningbo and Gaoyou are specifically targeting medical-grade applications, while the expansion of specialized endoscopy centers under national healthcare reforms is lifting domestic consumption of OPA-based high-level disinfectants through 2026.

United States – Distribution Centralization and Faster Disinfection Cycles

The United States OPA market is anchored in healthcare procurement efficiency, regulatory clarity, and product-cycle innovation. A pivotal development occurred in October 2025 when Advanced Sterilization Products entered a comprehensive distribution agreement with Premier Inc., centralizing access to Cidex OPA solutions across thousands of hospitals and ambulatory care sites. This consolidation is streamlining purchasing decisions for high-level disinfectants amid rising procedure volumes.

From a regulatory standpoint, the U.S. Food and Drug Administration continues to recognize OPA as a substantial equivalent to legacy glutaraldehyde-free formulations under 880.6885, while tightening 2025 monitoring requirements around minimum effective concentration thresholds. Innovation is focused on workflow efficiency. Metrex integrated its MetriCide OPA Plus with next-generation automated endoscope reprocessors in late 2025, enabling rapid five-minute cycles at ambient temperatures. Complementary advances include longer-shelf-life OPA test strips and education partnerships with Association for Professionals in Infection Control and Epidemiology, reinforcing compliance and infection prevention outcomes.

Germany – Regulatory Rigor, Centralized Procurement, and Exposure Mitigation

Germany represents Europe’s most mature OPA market, supported by a large medtech manufacturing base and stringent biocidal oversight. OPA-based disinfectants are regulated under EU Regulation 528/2012, with 2025–2026 approvals overseen by Federal Institute for Occupational Health and Safety. Compliance requirements are shaping portfolio strategies, particularly for suppliers serving hospital instrument reprocessing and surface disinfection.

Market structure is evolving in parallel with healthcare reform. The 2025–2026 consolidation of surgical services into high-volume Level 3 centers is driving bulk procurement contracts for OPA disinfectants, favoring suppliers with reliable logistics and validated exposure controls. German manufacturers are investing heavily in R&D to lower toxicity profiles and develop bio-based aldehyde alternatives, while operational upgrades focus on closed-loop reprocessing systems to minimize worker exposure to OPA vapors. These measures align with forthcoming workplace safety initiatives and reinforce Germany’s benchmark status for regulated disinfectant use.

Japan – High-Purity Reagents and Aging-Demographic Demand

Japan’s OPA industry is defined by precision chemistry, regulatory scrutiny, and steady healthcare demand driven by demographic trends. In November 2025, Ministry of Economy, Trade and Industry issued the 2026 schedule for low-volume new chemical substance notifications, influencing the introduction of specialized OPA-derived reagents. Concurrently, amendments to the Chemical Substances Control Law enforcement order have tightened impurity monitoring for analytical-grade OPA used in HPLC derivatization.

Demand fundamentals remain stable. Rising diagnostic procedures associated with Japan’s aging population are sustaining consistent consumption of rapid-acting OPA sterilants for endoscopy. Japanese chemical firms maintain a competitive edge in ultra-high-purity OPA production, typically exceeding 99.5%, supplying global diagnostic laboratories that require reproducible amino acid analysis and stringent quality assurance.

India – Pharmaceutical Utilization and Cost-Competitive Exports

India’s OPA market is expanding through pharmaceutical synthesis, healthcare access programs, and export-oriented manufacturing. Chemical clusters in Gujarat and Telangana are increasing the use of OPA as a functional reagent and intermediate for drug development, benefiting from proximity to active pharmaceutical ingredient producers. On the healthcare side, expansion of the Ayushman Bharat scheme in 2025–2026 is increasing surgical volumes in Tier 2 cities, creating incremental demand for affordable high-level disinfectants compatible with existing endoscopy infrastructure.

Indian producers are also strengthening their export posture. Generic OPA formulations are increasingly directed toward Southeast Asian and Middle Eastern markets, where price sensitivity favors competitively sourced intermediates. This strategy positions India as a complementary supplier to China, particularly in markets seeking diversified sourcing without compromising baseline quality standards.

Comparative Country Snapshot – Ortho Phthalaldehyde Industry

Ortho Phthalaldehyde Market County Level Snapshot

|

Country

|

Primary Market Driver

|

Regulatory Emphasis

|

Strategic Position

|

|

China

|

Scale and medical-grade capacity

|

VOC control and park compliance

|

Global supply anchor with vertical integration

|

|

United States

|

Centralized healthcare procurement

|

MEC monitoring under FDA

|

Workflow efficiency and rapid-cycle adoption

|

|

Germany

|

Hospital consolidation

|

EU Biocidal Regulation

|

Compliance-led, bulk procurement market

|

|

Japan

|

Diagnostics and aging population

|

CSCL impurity controls

|

High-purity reagent specialist

|

|

India

|

Pharma synthesis and public healthcare

|

Export standards alignment

|

Cost-competitive regional supplier

|

Ortho Phthalaldehyde Market Report Scope

Ortho Phthalaldehyde Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.4 Billion

|

|

Market Size (2034)

|

$10.3 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Form (Liquid, Solid), By Grade (Medical and Disinfectant Grade, Reagent and Analytical Grade, Technical Grade), By Application (High-Level Disinfection, Analytical Chemistry, Pharmaceutical Synthesis, Industrial Biocides), By End-User (Hospitals and Ambulatory Surgery Centers, Diagnostic Laboratories and Research Institutes, Pharmaceutical and Biotechnology Companies, Food and Beverage Processing Facilities)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Advanced Sterilization Products, Metrex Research, Richap Chemical, Wanxiang Chemical, Jinan Finer Chemical, Shodhana Laboratories, Capot Chemical, Chemodex, Merck, Thermo Fisher Scientific, Evonik Industries, Crosstex International, Schülke & Mayr, Laboratories Anios, Gaoyou Gaoyuan Auxiliary

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ortho Phthalaldehyde Market Segmentation

By Form

By Grade

- Medical and Disinfectant Grade

- Reagent and Analytical Grade

- Technical Grade

By Application

- High-Level Disinfection

- Analytical Chemistry

- Pharmaceutical Synthesis

- Industrial Biocides

By End-User

- Hospitals and Ambulatory Surgery Centers

- Diagnostic Laboratories and Research Institutes

- Pharmaceutical and Biotechnology Companies

- Food and Beverage Processing Facilities

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ortho Phthalaldehyde Industry

- Advanced Sterilization Products

- Metrex Research

- Richap Chemical

- Wanxiang Chemical

- Jinan Finer Chemical

- Shodhana Laboratories

- Capot Chemical

- Chemodex

- Merck

- Thermo Fisher Scientific

- Evonik Industries

- Crosstex International

- Schülke & Mayr

- Laboratories Anios

- Gaoyou Gaoyuan Auxiliary

*- List not Exhaustive