PACVD-Based Coatings Market Size, Advanced Deposition Demand, and High-Precision Manufacturing Expansion

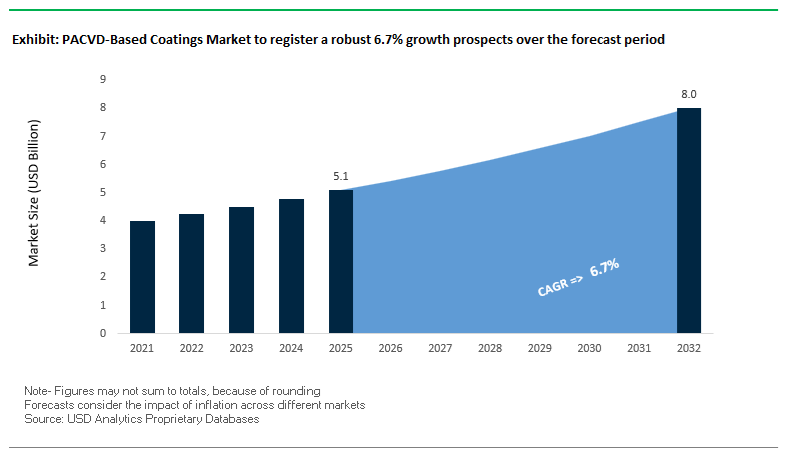

The global PACVD (Plasma-Assisted Chemical Vapor Deposition) Based Coatings Market reached $5.1 billion in 2025 and is projected to grow at a CAGR of 6.7% through 2032, achieving $8 billion by 2032. This expansion reflects the accelerating adoption of thin-film coating technologies in semiconductor fabrication, precision tooling, automotive engineering, and high-performance industrial components.

PACVD technologies are increasingly positioned as critical enablers of next-generation manufacturing, particularly where atomic-scale precision, uniform coating thickness, and enhanced surface functionality are required. The transition toward sub-3nm semiconductor nodes, electric vehicle power electronics, and advanced tribological systems is intensifying demand for PACVD coatings such as diamond-like carbon (DLC), silicon nitride, and silicon oxide layers. These coatings provide superior hardness, corrosion resistance, thermal stability, and low friction, making them indispensable in high-stress and high-temperature environments.

A major structural driver is the shift away from environmentally hazardous coating methods, including electroplating and hard chrome processes, toward vacuum-based plasma-assisted technologies that comply with evolving environmental regulations such as REACH. This transition is particularly evident in automotive components, hydraulic systems, and tooling applications, where PACVD coatings deliver both performance enhancement and regulatory compliance.

Furthermore, the market is benefiting from rapid industrialization in Asia-Pacific, especially in semiconductor manufacturing hubs and advanced machining ecosystems. Increasing investments in SiC and GaN semiconductor devices, 800V EV architectures, and high-efficiency power electronics are further expanding the addressable market for PACVD coatings. Simultaneously, innovation in bio-based precursors and sustainable plasma chemistries is reshaping the environmental footprint of deposition processes, positioning PACVD as a key technology within the broader green manufacturing transition.

Market Analysis: Semiconductor Scaling Breakthroughs, Strategic Industry Realignment, and Green PACVD Innovation

Recent developments in the PACVD-based coatings market highlight a strong convergence of semiconductor innovation, sustainability imperatives, and strategic industry restructuring. In April 2026, Applied Materials introduced its Precision Selective Nitride PECVD system, engineered for 2nm logic nodes and Gate-All-Around (GAA) transistor architectures. This system leverages a bottom-up selective deposition approach, addressing scaling limitations of conventional deposition techniques and reinforcing PACVD’s central role in next-generation chip fabrication.

Industry consolidation and specialization are also shaping competitive dynamics. In February 2026, Oerlikon completed its transformation into a pure-play surface technology company following the divestment of its Barmag business. This strategic pivot enables focused investment in PACVD, PVD, and thermal spray technologies, targeting high-growth sectors such as aerospace, energy, and semiconductors.

On the application front, innovation is diversifying beyond industrial uses into high-value decorative and consumer applications. In January 2026, Hauzer Techno Coating launched its “Brown Luxury” PACVD series, delivering superior hardness and color consistency for premium electronics and architectural hardware. This reflects a growing niche where PACVD combines aesthetic precision with extreme wear resistance.

Tooling and manufacturing efficiency remain key focus areas. Ionbond’s CVD 29 Ultra launch in December 2025 was accompanied by advancements in PACVD layer integration, enhancing tool life and reducing downtime in semiconductor and precision molding operations. Meanwhile, Evatec’s May 2025 expansion of PECVD capabilities for SiC and GaN wafers directly supports the transition toward high-voltage EV powertrains, reinforcing PACVD’s importance in power semiconductor ecosystems.

Sustainability is emerging as a defining innovation axis. The October 2025 industrialization of bio-based PACVD precursors, led by a consortium including BASF, signals a shift toward reducing reliance on fossil-derived silanes and hydrocarbons. Additionally, Hauzer’s “Beyond Hard Chrome” initiative (April 2025) underscores the regulatory-driven replacement of legacy coating technologies with PACVD-based DLC and duplex systems, particularly in automotive and hydraulic applications.

Market Trend: PACVD DLC Coatings Enabling Ultra-High-Pressure Fuel Injection Systems in Automotive Applications

The PACVD-based coatings industry is experiencing strong momentum in automotive fuel systems as engine platforms transition toward ultra-high-pressure injection architectures exceeding 3,000 bar. These operating conditions demand advanced surface engineering solutions capable of maintaining dimensional stability, minimizing friction losses, and ensuring long-term wear resistance under extreme mechanical stress. Plasma Assisted Chemical Vapor Deposition DLC coatings have emerged as the industry standard for critical reciprocating components such as plungers, tappets, and pump cylinders.

PACVD DLC coatings deliver ultra-low coefficients of friction in the range of 0.05 to 0.1, significantly reducing parasitic energy losses within high-pressure fuel pumps. At injection pressures approaching 3,000 bar, these coatings enable torque loss reductions of approximately 15% to 20% compared to untreated metallic surfaces. This performance improvement directly contributes to enhanced fuel efficiency and supports compliance with stringent emission standards such as Euro VII and China VI-b.

Wear resistance is a defining advantage of PACVD DLC coatings. Endurance testing under simulated high-pressure conditions demonstrates a 70% reduction in abrasive wear over extended operational cycles of 5,000 hours, preserving the tight tolerances required for precise fuel metering. Additionally, the non-line-of-sight deposition capability of PACVD provides uniform coating thickness across complex internal geometries, achieving consistency within ±5% even in small-bore components. This capability differentiates PACVD from conventional PVD processes and enables scalable application across advanced fuel system architectures.

Market Trend: PACVD SiOx Barrier Coatings Advancing Recyclable High-Barrier Flexible Packaging Solutions

The flexible packaging sector is rapidly adopting PACVD silicon oxide coatings as manufacturers shift toward mono-material, recyclable packaging structures. These coatings provide glass-like barrier properties on polymer substrates such as PET and polypropylene while maintaining transparency, flexibility, and compatibility with circular economy requirements.

PACVD SiOx coatings achieve high-performance oxygen barrier levels, with oxygen transmission rates below 0.5 cm³/m²/day. This performance is comparable to aluminum foil laminates while offering significant weight reduction and improved recyclability. The ability to replace multi-layer foil structures with single-material solutions is a key driver in sustainable packaging innovation, particularly in food and beverage applications.

Moisture barrier performance is equally critical, with water vapor transmission rates maintained below 0.3 g/m²/day. Plasma-assisted deposition enhances film density and structural integrity, delivering approximately 30% greater crack resistance compared to evaporated SiOx coatings. This improved mechanical robustness is essential for high-speed packaging operations, where films undergo significant stress during forming, filling, and sealing processes.

An additional advantage is microwave compatibility. Unlike metallic barrier layers, SiOx coatings are non-conductive, enabling the development of microwave-safe high-barrier packaging formats. This capability is supporting growth in ready-to-eat meal packaging, a segment expanding at an estimated annual rate of around 12%. These combined attributes position PACVD SiOx coatings as a cornerstone technology in next-generation sustainable packaging systems.

Market Opportunity: Hydrogen Economy Investments Driving Demand for PACVD Barrier Coatings in High-Pressure Compression Systems

The emergence of the hydrogen economy is creating a significant opportunity for PACVD-based coatings, particularly in high-pressure hydrogen compression and storage infrastructure. The U.S. Department of Energy, through its advanced manufacturing and decarbonization initiatives, is actively supporting the development of surface engineering solutions that enhance material durability and safety in hydrogen environments.

Hydrogen embrittlement presents a major challenge for metallic components exposed to high-pressure hydrogen gas. PACVD coatings, including amorphous carbon and silicon carbide variants, are being developed as effective diffusion barriers capable of reducing hydrogen permeation into steel substrates by more than 90%. This protection is critical for preventing brittle fracture in compressor valves, seals, and pipelines operating at pressures up to 700 bar.

Funding support is accelerating innovation in this area. Under the 2025 to 2026 industrial decarbonization roadmap, over $50 million has been allocated for research and development of advanced coating technologies that enable hydrogen infrastructure scalability. This includes coatings compatible with high-pressure refueling systems and long-duration storage applications. As hydrogen adoption expands across transportation and industrial sectors, PACVD coatings are positioned to play a central role in ensuring reliability and safety.

Market Opportunity: China NMPA Standards Driving Adoption of PACVD DLC Coatings in Orthopedic Implants

China’s evolving medical device regulatory framework is creating a high-value opportunity for PACVD coatings in the healthcare sector, particularly in orthopedic implants. Updates to the Medical Device Classification Catalogue and the introduction of new industry standards are emphasizing the importance of wear-resistant and biocompatible surface modifications in implantable devices.

PACVD DLC coatings are increasingly being specified for joint replacement systems and metal bone plates due to their ability to significantly reduce wear and ion release. Clinical and laboratory data indicate that DLC-coated implants can reduce metal ion leaching by up to 99%, addressing concerns related to long-term biocompatibility and implant safety. This performance is particularly important in load-bearing applications such as hip and knee prostheses, where material degradation can impact patient outcomes.

Regulatory incentives are further accelerating adoption. The updated approval framework includes fast-track pathways for innovative medical devices that demonstrate improved durability and reduced corrosion. PACVD DLC-coated implants showing at least a 30% increase in service life during fatigue testing are eligible for reduced clinical trial timelines, potentially shortening approval cycles by up to six months.

The combination of regulatory support, clinical performance advantages, and increasing healthcare demand is positioning PACVD coatings as a critical technology in the next generation of orthopedic devices within the Chinese medical market.

PACVD Market Share and Segmentation Insights

RF PACVD Holds 45.6% Share Driven by Multi-Substrate Compatibility and Complex Geometry Coating

The PACVD-based coatings market by plasma activation technology is led by RF PACVD (Radio Frequency Plasma-Enhanced Chemical Vapor Deposition), accounting for 45.6% of the global market share in 2025, due to its exceptional versatility and coating precision. RF PACVD systems are capable of processing both insulating and conductive substrates, including ceramics, polymers, glass, and metals, making them the preferred technology for advanced coatings such as diamond-like carbon (DLC) coatings and SiOx barrier coatings. A major advantage is their ability to deliver uniform coating thickness on complex 3D geometries, including medical devices, internal tube surfaces, and precision-engineered components, where line-of-sight technologies fall short. This combination of broad material compatibility, high-performance thin-film coatings, and precision deposition reinforces RF PACVD’s leadership in the global advanced coatings market.

Contract Coating Services Capture 55.3% Share Driven by High Equipment Costs and Batch Processing Advantages

In the PACVD-based coatings market by service model, contract coating services dominate with a 55.3% market share in 2025, reflecting the high capital and technical barriers associated with PACVD systems. These systems typically require investments ranging from $250,000 to $2 million, along with specialized expertise in vacuum technology, plasma physics, and cleanroom operations, making outsourcing the preferred option for many manufacturers. Contract coating providers serve industries such as medical devices, automotive components, cutting tools, and industrial molds, offering DLC and functional thin-film coatings without requiring customers to invest in infrastructure. Additionally, these providers optimize batch processing, combining parts from multiple clients into single deposition cycles, significantly reducing per-part costs and turnaround times. This efficiency and accessibility position contract services as the dominant model in the global PACVD coatings market.

Competitive Landscape of the PACVD-Based Coatings Market

Oerlikon Balzers Leads PACVD Innovation with High-Performance DLC Coatings

Oerlikon Balzers, part of Oerlikon’s Surface Solutions Division, is a global leader in PACVD coatings, particularly in the DLC segment for automotive and precision components. In 2026, the company showcased its BALINIT® DYLYN portfolio featuring metal-free carbon coatings with surface hardness up to 30 GPa and exceptional lubricity. Its expansion of the PrimeSurface network into Vietnam and India strengthens its presence in the growing Southeast Asian manufacturing hub. Oerlikon’s PACVD services are witnessing strong demand in aerospace and medical sectors due to biocompatibility and low-temperature deposition advantages. With over 110 coating centers worldwide, it delivers integrated end-to-end surface engineering solutions.

Ionbond Advances Hybrid PACVD Technologies for Semiconductor and EV Applications

IHI Ionbond AG is a leader in hybrid PVD/PACVD coating technologies, targeting high-growth sectors such as semiconductor machinery and electric vehicle components. In 2026, the company introduced advanced DLC coatings at SVC TechCon, designed to withstand extreme thermal cycling in EV power electronics. Its Diamondblack™ ADLC coatings enhance durability in aggressive plasma environments, extending component lifespan. Ionbond’s Decobond™ coatings combine functional wear resistance with aesthetic finishes, meeting FDA standards for food-contact applications. Additionally, its sustainability initiatives demonstrate that low-friction PACVD coatings can reduce fuel consumption by up to 3.5%, reinforcing its leadership in energy-efficient coating technologies.

CemeCon Strengthens Precision Coating Leadership with Advanced Diamond Deposition Systems

CemeCon AG is a key innovator in the PACVD coatings market, particularly for cutting tools and mold applications. The company leads in diamond coating technology, utilizing proprietary PACVD processes to deposit crystalline diamond layers on complex 3D geometries. In 2026, it expanded its U.S. operations to support aerospace and defense supply chains. Its advanced control systems enable real-time process optimization, ensuring consistent coating quality across batches. The CC800®/9 platform integrates PVD and PACVD processes within a single cycle, reducing turntimes by 20%. CemeCon’s focus on high-precision, high-durability coatings strengthens its position in industrial and tooling applications.

Richter Precision Enhances Industrial Applications with Ultra-Hard PACVD Coating Solutions

Richter Precision Inc. is a dominant provider of PACVD coating services in North America, offering advanced Titankote™ solutions for industrial and medical applications. Its Titankote™ C10 coating achieves extreme hardness levels of 9000 HV, making it ideal for surgical tools and precision components. The company specializes in low-temperature PACVD processes, enabling coating of heat-sensitive materials such as specialty steels and elastomers. Richter is also a preferred partner for plastic injection molding, where its coatings improve mold release and reduce cycle times. In 2026, it launched an aerospace MRO program, extending component life by up to 200% through high-performance DLC coating solutions.

Hauck Heat Treatment Expands PACVD Applications in Automotive and Green Energy Sectors

Hauck Heat Treatment, part of Aalberts Surface Technologies, is a major player in industrial PACVD coatings, focusing on automotive and heavy machinery applications. Leveraging Aalberts’ global network, the company offers integrated heat treatment and PACVD coating solutions in a continuous production chain. In 2026, Hauck introduced silicon-doped DLC coatings with enhanced thermal stability up to 500°C and improved adhesion on challenging substrates. The company is targeting the green energy sector, providing coatings for wind turbine components to reduce surface fatigue and wear. With the capacity to process over 50 million automotive parts annually, Hauck leads in high-volume PACVD coating production.

Germany PACVD-Based Coatings Market: DLC Innovation and Green Manufacturing Transformation

Germany stands as the European hub for PACVD-based coatings, driven by its leadership in precision engineering, automotive manufacturing, and sustainable surface technologies. At the K 2025 trade fair, German companies highlighted a major transition toward PACVD thin-film coatings as PFAS-free alternatives in plastic injection molding, particularly for demolding applications. This shift aligns with EU REACH regulations targeting the elimination of hazardous materials such as hard chrome plating.

The country is witnessing strong innovation in diamond-like carbon (DLC) coatings, particularly for industrial tooling and additive manufacturing. The integration of PACVD wear-resistant coatings in 3D-printed metal tools is reducing cycle times in high-volume production processes such as bottle cap manufacturing. Additionally, Germany is investing heavily in hydrogen economy infrastructure, where PACVD-coated bipolar plates are critical for fuel cell performance. Regional clusters in Saxony and Baden-Württemberg are expanding coating service centers, reinforcing Germany’s leadership in high-value, sustainable coating solutions.

China PACVD-Based Coatings Market: Semiconductor Expansion and High-Volume Deposition Leadership

China’s PACVD coatings market is characterized by large-scale capacity expansion and rapid integration into semiconductor manufacturing, positioning the country as a global leader in plasma-enhanced thin-film deposition technologies. Government mandates promoting industrial growth are driving investments in high-throughput PACVD chambers for advanced semiconductor architectures such as 3D NAND and FinFET, where precise thin-film deposition is essential.

China’s regulatory and industrial frameworks are also encouraging the adoption of PACVD barrier coatings in food packaging, supported by expanded material approvals under GB 4806.10-2025 standards. The country holds a significant share in vacuum coating equipment demand, with new facilities in the Pearl River Delta specializing in anti-reflective coatings for solar photovoltaic applications. Additionally, tightening VOC emission regulations are accelerating the transition from traditional liquid coatings to closed-system PACVD processes, enhancing sustainability and efficiency.

Japan PACVD-Based Coatings Market: Advanced Material Science and EV Thermal Management Innovation

Japan leads in innovation-intensive PACVD coating applications, particularly in electric vehicles, electronics, and advanced materials engineering. Collaborative developments, such as the joint venture between Nippon Paint and Uchihamakasei, are pioneering in-mold PACVD coating technologies for EV exteriors, significantly reducing carbon emissions during production.

The country’s strong R&D ecosystem is driving advancements in electrostatic discharge-resistant coatings for EV battery sensors and high-precision electronics. PACVD technology is also being applied in smart packaging solutions, where oxygen-scavenging coatings extend the shelf life of ready-to-eat food products. Additionally, Japan is advancing ultra-high-pressure PACVD processes for optical fiber coatings, supporting next-generation 6G infrastructure. Strict regulatory frameworks, including the Positive List System for food-contact materials, are further encouraging the adoption of low-migration plasma-deposited barrier coatings.

United States PACVD-Based Coatings Market: Aerospace Applications and Nearshoring-Driven Growth

The United States PACVD coatings market is being reshaped by aerospace innovation, PFAS-free regulatory transitions, and nearshoring trends. The adoption of PACVD-based diamond-like carbon coatings is accelerating as a replacement for PFAS-containing lubricants, particularly in medical devices and high-performance industrial applications.

Technological breakthroughs include the development of environmental barrier coatings (EBCs) for aerospace turbine blades, capable of withstanding temperatures above 1,200°C using plasma-assisted deposition. Infrastructure investments and nearshoring initiatives are driving demand for PACVD coatings in logistics and industrial automation systems, particularly in the U.S. Sun Belt region. The market is also expanding in pharmaceutical packaging, where PACVD moisture barrier coatings ensure sterile integrity in blister packs. Additionally, defense sector investments under the CHIPS Act are boosting demand for plasma-resistant coatings in semiconductor manufacturing equipment.

South Korea PACVD-Based Coatings Market: Semiconductor Clusters and Advanced Display Technologies

South Korea is a global leader in PACVD coatings for semiconductor and display applications, driven by its strong presence in electronics manufacturing. The country holds a high concentration of patents in plasma technologies, reflecting its dominance in advanced deposition processes and materials innovation.

Recent advancements include low-voltage PACVD processes (<160V), which significantly reduce thermal stress, enabling coating applications for flexible electronics and foldable OLED displays. South Korea is also advancing halogen-resistant coatings for semiconductor etch chambers, ensuring durability under extreme processing conditions. In the medical sector, PACVD-based coatings are being explored for biocompatible implants, particularly using plasma electrolytic oxidation on titanium materials. Additionally, the demand for thin-film encapsulation (TFE) in display manufacturing is driving large-scale adoption of PACVD technologies.

Switzerland PACVD-Based Coatings Market: Luxury Coatings and High-Precision Medical Applications

Switzerland remains a global benchmark for high-performance PACVD coatings, particularly in luxury goods, precision tooling, and medical applications. Innovations such as Oerlikon Balzers’ INSPIRA carbon platform are enhancing productivity and quality in advanced carbon coatings, including DLC finishes.

The country is a leader in diamond coatings for machining applications, improving efficiency in aerospace and dental manufacturing. PACVD coatings are widely used in the Swiss watch industry, providing durable, high-hardness finishes with premium aesthetics. Additionally, the adoption of organosilane-based plasma coatings is enabling PFAS-free solutions in textile and polymer applications. Switzerland’s early adoption of low-VOC and solvent-free deposition technologies aligns with EU sustainability goals, reinforcing its leadership in high-value coating markets.

India PACVD-Based Coatings Market: Infrastructure Growth and Local Manufacturing Expansion

India is emerging as a fast-growing market for PACVD-based coatings, supported by infrastructure development and government initiatives such as the National Infrastructure Pipeline and PLI schemes. The establishment of advanced facilities like Oerlikon’s Smart Integrated Surface Solutions Centre in Tumakuru is strengthening domestic capabilities in plasma coating technologies.

The market is witnessing increasing adoption of PACVD DLC coatings in automotive components, helping manufacturers meet stringent BS-VI emission standards by reducing friction and improving efficiency. Growth in pharmaceutical manufacturing hubs is driving demand for high-purity, low-friction coatings for production and packaging tools. Additionally, India’s rapid expansion in solar energy is boosting the use of PACVD coatings in thin-film solar cells, supporting the country’s renewable energy targets. The rise of e-commerce is also creating demand for moisture-resistant plasma coatings in logistics and warehouse applications, further accelerating market growth.

PACVD-Based Coatings Market Report Scope

PACVD-Based Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.1 Billion

|

|

Market Size (2032)

|

$8 Billion

|

|

Market Growth Rate

|

6.7%

|

|

Segments

|

By Coating Material (Metal-based Coatings, Ceramic-based Coatings, Carbon-based Coatings, Polymer and Composite Coatings), By Plasma Activation Technology (RF, DC, Microwave PACVD, Inductively Coupled Plasma), By Substrate Material (Metals and Alloys, Semiconductors, Polymers and Plastics, Glass and Ceramics), By End-Use Industry (Microelectronics and Semiconductors, Transportation, Cutting Tools and Machining, Medical Devices and Healthcare, Energy, Optics and Consumer Electronics), By Equipment Configuration (Batch Coaters, In-line Coaters, Cluster Tools), By Functional Property (Wear and Friction Resistance, Corrosion and Chemical Protection, Biocompatibility, Electrical Conductivity, Optical Transparency and Haze Control), By Service Model (Coating Equipment Sales, Contract Coating Services)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Oerlikon Balzers, IHI Ionbond AG, Applied Materials, Inc., ASM International N.V., Bühler Group, Jusung Engineering Co., Ltd., Lam Research Corporation, Veeco Instruments Inc., Entegris, Inc., KLA Corporation, ULVAC, Inc., RÜBIG GmbH and Co KG, Kurt J. Lesker Company, Plasma-Therm LLC, AGC Plasma Technology Solutions

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

PACVD Based Coatings Market Segmentation

By Coating Material

- Metal-based Coatings

- Ceramic-based Coatings

- Carbon-based Coatings

- Polymer and Composite Coatings

By Plasma Activation Technology

- RF

- DC

- Microwave PACVD

- Inductively Coupled Plasma

By Substrate Material

- Metals and Alloys

- Semiconductors

- Polymers and Plastics

- Glass and Ceramics

By End-Use Industry

- Microelectronics and Semiconductors

- Transportation

- Cutting Tools and Machining

- Medical Devices and Healthcare

- Energy

- Optics and Consumer Electronics

By Equipment Configuration

- Batch Coaters

- In-line Coaters

- Cluster Tools

By Functional Property

- Wear and Friction Resistance

- Corrosion and Chemical Protection

- Biocompatibility

- Electrical Conductivity

- Optical Transparency and Haze Control

By Service Model

- Coating Equipment Sales

- Contract Coating Services

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in PACVD Based Coatings Industry

- Oerlikon Balzers

- IHI Ionbond AG

- Applied Materials, Inc.

- ASM International N.V.

- Bühler Group

- Jusung Engineering Co., Ltd.

- Lam Research Corporation

- Veeco Instruments Inc.

- Entegris, Inc.

- KLA Corporation

- ULVAC, Inc.

- RÜBIG GmbH & Co KG

- Kurt J. Lesker Company

- Plasma-Therm LLC

- AGC Plasma Technology Solutions

*- List not Exhaustive