Para Nitrochlorobenzene Market Valued at $462.8 Million in 2025 with 4.7% CAGR Driven by Agrochemical Expansion and Dye-Chain Consolidation

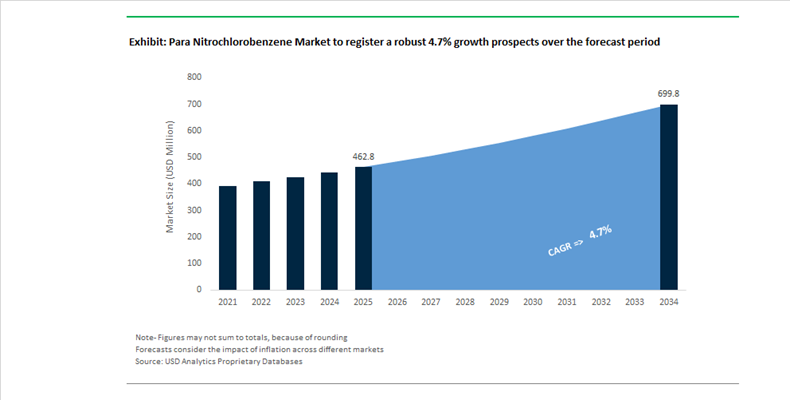

The Para Nitrochlorobenzene (PNCB) Market is valued at $462.8 Million in 2025 and is projected to reach $699.7 Million by 2034, expanding at a CAGR of 4.7%. PNCB is a critical nitro-aromatic intermediate used in the production of dyes, pigments, agrochemicals, rubber chemicals, and pharmaceutical precursors. Its industrial relevance lies in its conversion into para-phenylenediamine (PPD), para-aminophenol (PAP), and other downstream intermediates essential for high-performance pigments, hair dyes, antioxidants, and crop protection molecules. Market growth remains structurally linked to agricultural intensification in Asia, recovery in textile dye exports, and rising automotive tire production requiring advanced anti-degradants. The supply chain is highly concentrated in China and India, with regulatory oversight and feedstock integration (benzene and chlorine) playing decisive roles in capacity expansion decisions.

A major value-chain development occurred in March 2025 when Sudarshan Chemical Industries Limited completed the acquisition of Germany’s Heubach Group. This transaction consolidates one of the largest global pigment portfolios under Indian ownership, reinforcing backward integration into nitro-aromatic intermediates such as PNCB. The move strategically aligns pigment manufacturing with upstream intermediate supply, reducing exposure to volatility in Chinese exports. Similarly, in January 2024, Aarti Industries secured approximately $361 million to expand agrochemical intermediate production. The funding directly supports capacity scaling for nitrochlorobenzene derivatives used in herbicides and insecticides, strengthening India’s positioning as a global supplier of crop protection chemistry.

The dye value chain experienced further consolidation in December 2025 when Kiri Industries finalized a $689 million settlement involving DyStar, transferring full control to Zhejiang Longsheng Group. This development concentrates significant PNCB consumption within Chinese-controlled dye networks, tightening procurement linkages between upstream nitration facilities and downstream colorant producers. In parallel, Silox India announced capital deployment of ₹300–360 crore for its Dahej expansion scheduled for 2026, targeting specialty chemical intermediates that utilize high-purity PNCB as a building block.

Price stability emerged in early 2025, with Chinese PNCB prices averaging approximately $950 per metric ton following supply normalization after late-2024 oversupply conditions. However, regulatory pressures remain influential. In January 2026, the United States Environmental Protection Agency advanced updated risk management rules affecting pigment particulates derived from nitrochlorobenzenes. These developments are compelling manufacturers to modernize nitration, oxidation, and effluent treatment systems to meet export compliance standards. Meanwhile, India’s broader petrochemical expansion strategy—targeting 1.8x capacity growth by 2030—is encouraging domestic nitro-aromatic players to reduce reliance on imported derivatives and establish fully integrated chlorination-nitration complexes. The Para Nitrochlorobenzene market is therefore entering a phase defined by vertical integration, regulatory compliance upgrades, and geographic realignment of dye and agrochemical supply chains.

Structural Trends and High-Value Opportunities Shaping the Para-Nitrochlorobenzene Market

Strategic Capacity Consolidation in China Drives Global Supply Reconfiguration

The global para-nitrochlorobenzene market continues to be anchored in China, but the operating model has shifted decisively from capacity expansion to regulatory-driven consolidation. Under China’s Action Plan for New Pollutants Treatment, p-NCB production is increasingly concentrated within integrated chemical parks, where environmental controls, digital monitoring, and waste management systems can be implemented at scale. Smaller, standalone producers are steadily exiting the market as compliance costs rise beyond viable thresholds.

This transition accelerated in late 2024 when China’s Ministry of Ecology and Environment released its Third Batch of Priority Controlled Substances draft, formally categorizing nitrochlorobenzenes among higher-risk aromatic intermediates. By late 2025, producers are required to deploy refined tracking systems, leakage prevention protocols, and real-time emissions monitoring. These capital-intensive requirements structurally favor large players such as Sinopec Nanjing and Yangnong Chemical, reinforcing industry concentration and tightening effective supply.

At the same time, global buyers are actively de-risking single-country dependence. India’s Production Linked Incentive scheme for bulk drugs has accelerated domestic upstream integration, particularly for paracetamol intermediates. By October 2025, India’s paracetamol API exports had reached more than 70 countries, supported by expanding p-NCB and para-aminophenol clusters in Gujarat and Maharashtra. Short-term price volatility remains a feature of the market. Although Chinese export prices softened in December 2025 due to RMB appreciation and year-end destocking, supply fundamentals remain tight as multiple plants schedule maintenance shutdowns for early 2026, prompting strategic stockpiling by pharmaceutical and dye manufacturers.

Regulatory Pressure Accelerates Substitution in Dye Intermediate Applications

A second defining trend in the p-NCB market is the gradual erosion of its traditional volume base in azo dyes. Global regulatory frameworks are no longer focused solely on finished dyes but on the aromatic amines released during their lifecycle. This shift has materially altered demand patterns for nitro-aromatic intermediates.

In Europe, intensified REACH scrutiny in 2025 has increased monitoring of azo dye chemistries capable of releasing restricted aromatic amines through reductive cleavage. Textile and pigment producers serving eco-labeled fashion brands are now demanding higher-purity, salt-free intermediates and, in some cases, transitioning away from legacy dye systems altogether. Similar dynamics are emerging across Asia-Pacific, where multiple countries adopted updated Globally Harmonized System classifications in 2025. Under these revisions, intermediates with incomplete hazard documentation are increasingly flagged as “hazard pending,” adding administrative risk for downstream users.

As a result, p-NCB suppliers are being forced to reposition from commodity dye intermediates toward higher-specification products with transparent safety data and consistent impurity profiles. While this trend constrains volume growth in traditional dyes, it also improves pricing discipline and accelerates the market’s transition toward regulated, higher-margin end uses.

High-Purity p-NCB Emerges as a Strategic Input for Pharmaceutical API Manufacturing

Pharmaceutical applications represent the most resilient and margin-accretive opportunity for the para-nitrochlorobenzene market. The p-NCB-to-para-aminophenol pathway remains the backbone of global paracetamol production, a medicine classified as essential by the World Health Organization. During 2024–2025, nearly 60 countries introduced national reserve and stockpiling programs for essential APIs, reinforcing baseline demand for this supply chain.

Innovation is further elevating quality requirements. In May 2025, India’s Council of Scientific and Industrial Research published a patent for a continuous, solvent-free paracetamol synthesis process achieving 94% to 97% selectivity. This approach reduces energy consumption by up to 30% but requires ultra-high-purity p-NCB to avoid downstream contamination. By October 2025, India alone reported more than 1,600 active importers of paracetamol API, with premium markets such as France and Ireland demanding tighter impurity specifications. This shift is creating a clear bifurcation between low-margin industrial-grade material and high-value pharmaceutical-grade p-NCB.

Advanced Polymers and Liquid Crystals Open Electronics-Focused Growth Pathways

A second high-value opportunity is emerging in advanced materials for electronics, displays, and automotive coatings. Research published in 2025 highlights the role of p-NCB as a foundational building block for azobenzene-functionalized polymeric liquid crystals used in smart windows, aerospace applications, and adaptive optical systems. These materials rely on the photoresponsive properties of azobenzene structures derived from nitro-aromatic precursors.

Telecommunications infrastructure is reinforcing this demand. The global rollout of 5G and early-stage 6G technologies is driving R&D into high-performance polyimides for flexible printed circuit boards. p-NCB-derived monomers offer high thermal stability and low dielectric constants, both critical for signal integrity in next-generation electronics. In parallel, automotive demand is rising for high-performance pigments used in OEM coatings, particularly for electric vehicles where durability and weather resistance are essential. Following the March 2025 acquisition of Heubach Group by Sudarshan Chemical Industries, renewed investment has flowed into engineering pigment systems derived from p-NCB for premium automotive finishes.

Together, these opportunities signal a structural repositioning of the para-nitrochlorobenzene market. While regulatory pressure is compressing low-end applications, demand is consolidating around pharmaceutical, electronics, and advanced materials segments that value purity, reliability, and traceable supply, supporting long-term stability and improved industry economics.

Para Nitrochlorobenzene Market Share and Segmentation Insights

Standard Grade Para Nitrochlorobenzene Leads Market Demand in Industrial Chemical Intermediate Production

Standard grade para nitrochlorobenzene accounted for 68.40% of the Para Nitrochlorobenzene Market by purity grade in 2025, reflecting its widespread use in large-scale chemical intermediate production. Industrial applications including dye intermediates, agrochemicals, and rubber processing chemicals typically require standard grade material with purity levels between 98% and 99%, making it the most cost-effective option for high-volume manufacturing. The commodity nature of PNCB encourages manufacturers to focus on improving process efficiency in nitration and chlorination reactions. In 2025, process economics optimization in PNCB production is a key industry trend, with producers adopting improved reactor technologies and yield optimization strategies that reduce byproduct formation and enhance production efficiency.

Agriculture Sector Drives Para Nitrochlorobenzene Demand in Agrochemical Manufacturing

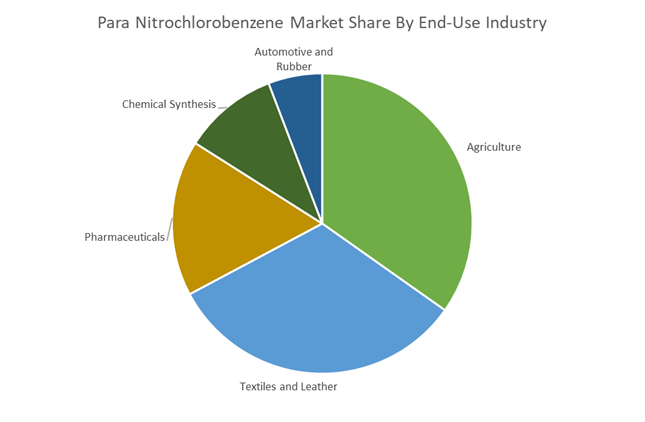

The agriculture sector represented 34.80% of the Para Nitrochlorobenzene Market by end-use industry in 2025, reflecting the important role of PNCB-derived intermediates in crop protection chemical manufacturing. Para nitrochlorobenzene serves as a key precursor in the synthesis of herbicides, fungicides, and insecticides used in large-scale agricultural production. Growing demand for crop protection solutions continues to sustain consumption of chemical intermediates used in agrochemical supply chains. In 2025, the expansion of generic agrochemical production across Asia, particularly in China and India, is strengthening demand for cost-efficient PNCB intermediates used in manufacturing high-volume crop protection formulations supplied to global agricultural markets.

Para Nitrochlorobenzene Market Competitive Landscape

The Para Nitrochlorobenzene (PNCB) Market is defined by backward integration, captive consumption, and regulatory compliance. Leading players are strengthening benzene-to-nitrochlorobenzene value chains, securing long-term supply contracts, and expanding specialty intermediates to mitigate raw material volatility and energy cost fluctuations across agrochemicals, dyes, and pharmaceutical applications.

Aarti Industries strengthens integrated benzene chain with long-term agrochemical supply contracts

Aarti Industries Limited (AIL) is a global leader in the PNCB market, leveraging deep backward integration across the benzene value chain to ensure cost efficiency and supply security. The company secured a $150 million multi-year contract with a global agrochemical major, reinforcing its role in crop protection intermediates derived from PNCB. Its ₹200–₹250 crore investment in backward integration enhances raw material control for nitro-aromatic intermediates. AIL reported strong Q3 FY26 performance with 11% volume growth and 100 bps margin expansion, supported by favorable feedstock spreads. With leadership in hydrogenation and dichlorobenzene production, it converts benzene into over 100 specialty products, with 70% revenue contribution from high-value chemicals. This integrated and contract-driven strategy strengthens AIL’s global positioning.

LANXESS restructures portfolio and pricing to focus on specialty nitro-aromatic intermediates

LANXESS AG is repositioning its business toward high-margin specialty chemicals, including nitro-aromatic intermediates linked to PNCB applications. The company implemented price increases of 15%–50% in 2026 to offset rising energy and raw material costs, protecting margins in volatile markets. Its portfolio transformation, including the divestment of urethane systems and plant closures, is expected to deliver €50 million annual savings by 2027. The FORWARD! program is optimizing production efficiency and streamlining global operations. LANXESS is also advancing digital R&D through platforms like LewaPlus, improving process optimization and customer collaboration. This strategic shift toward efficiency, pricing discipline, and specialty focus enhances its competitiveness.

Atul Ltd strengthens captive PNCB consumption for dyes and pharmaceutical intermediates

Atul Ltd. is reinforcing its position in the PNCB market through strong backward integration and high internal consumption of nitrochlorobenzene derivatives. Its aromatics division produces high-purity PNCB (>99.5%), primarily used in pharmaceuticals such as paracetamol and antimicrobial compounds. The company’s expansion of downstream dye intermediates ensures stable supply of para-anisidine and para-phenetidine, reducing exposure to market price fluctuations. Investments in Zero Liquid Discharge (ZLD) infrastructure across Gujarat facilities enhance compliance with stringent environmental regulations. By integrating production and consumption, Atul mitigates raw material volatility while maintaining consistent quality. This strategy positions it strongly in high-purity and captive-use segments.

Anhui Bayi leverages scale and export pricing to dominate Asia-Pacific PNCB supply

Anhui Bayi Chemical Industry Co., Ltd. is a major Chinese producer with significant influence on global PNCB pricing due to its large-scale nitration capacity. The company temporarily suspended production lines in 2025 to upgrade environmental compliance systems, aligning with stricter regulatory standards. Its export pricing showed a 4.31% decline in September 2025 due to high inventories and weak downstream demand. Anhui Bayi’s production yields approximately 66% PNCB and 33% ONCB, maximizing output efficiency. It plays a critical role in the p-nitrophenol value chain, supporting large-scale pharmaceutical production such as paracetamol. This scale-driven model ensures cost competitiveness in high-volume technical-grade markets.

Kutch Chemical scales chlor-alkali integration to strengthen domestic PNCB supply chain

Kutch Chemical Industries Ltd. is emerging as a strong regional player in the PNCB market, supported by integrated chlor-alkali operations and strategic manufacturing expansion in Western India. Its captive chlorine production enables efficient monochlorobenzene synthesis, ensuring stable feedstock supply for PNCB production. The company supplies high-purity industrial-grade PNCB (>99%) in molten and flake forms, catering to agrochemical and dye manufacturers. Expansion in India’s key chemical hub positions Kutch Chemical close to major downstream consumers, improving logistics efficiency. Its growing presence in rubber chemicals, including antioxidants and stabilizers, diversifies revenue streams. This integration of feedstock control, regional proximity, and product diversification enhances its competitive positioning.

India – Capacity Discipline, Fluorination Investments, and Logistics-Driven Competitiveness

India has emerged as a structurally resilient PNCB manufacturing base, underpinned by disciplined capacity utilization and targeted capital deployment into downstream fluorinated chemistry. In May 2025, Aarti Industries Limited reported sustained high operational utilization across its expanded Nitro Chloro Benzene assets. Half-yearly compliance filings for October 2024 to March 2025 confirmed that Para Nitrochlorobenzene output at its Tarapur and Vapi clusters is operating close to peak Environment Clearance thresholds, indicating both demand stability and regulatory headroom discipline. This operating posture has positioned India as a dependable supplier of PNCB for pharmaceuticals, agrochemicals, and pigment intermediates.

Strategic capital allocation is reinforcing margin quality rather than volume expansion. In 2025, Aarti Industries earmarked approximately INR 10.29 crore for specialized fluorinated aromatic chemical expansion at Maharashtra sites, directly leveraging PNCB as a feedstock for high-value pharmaceutical and agro-intermediates. Domestic pricing dynamics have also stabilized. By Q3 2025, Ex-Mumbai PNCB prices settled near USD 1,014 per metric ton as producers such as Panoli Intermediates and Kutch Chemical Industries optimized catalytic efficiency and yields. On the infrastructure side, the PM Gati Shakti program has reduced lead times from Gujarat’s chemical belts to downstream pesticide formulators by roughly 20%, materially improving working capital cycles. Regulatory rigor remains high. In 2025, the Maharashtra Pollution Control Board enforced tighter Zero Liquid Discharge mandates for nitro-aromatic plants, triggering retrofitting investments across the Thane-Belapur corridor and raising the entry barrier for sub-scale operators.

China – Export Controls, Inventory-Led Price Reset, and Compliance Tightening

China continues to influence global PNCB availability primarily through policy levers rather than incremental capacity additions. Effective April 4, 2025, the Ministry of Commerce of the People's Republic of China and the General Administration of Customs implemented Announcement No. 18, tightening export licensing for several dual-use chemical intermediates. While PNCB was not singularly targeted, the licensing framework indirectly constrained spot-market availability of high-purity grades, particularly for pigment and agrochemical buyers outside Asia.

Market pricing adjusted to domestic inventory conditions. In September 2025, Shanghai export quotations for PNCB declined by 7.29% month on month, ranging between USD 815 and USD 940 per metric ton, reflecting elevated stock levels and cautious global procurement. At the asset level, Anhui Bayi Chemical Industry Co., Ltd. retained its leadership position by completing integration of advanced hazardous waste treatment systems in 2025, strengthening its compliance profile amid tightening environmental scrutiny. Logistical efficiency improved in December 2025 when China Customs streamlined record-filing for maritime exports of Class 6.1 hazardous materials, shortening clearance timelines for European and North American shipments. Looking ahead, RoHS 2.0 requirements effective January 1, 2026 are forcing downstream dye manufacturers to eliminate heavy-metal impurities in azo-pigment synthesis, indirectly raising purity specifications for PNCB feedstocks.

Germany – Specialty Focus and Carbon-Tracked Intermediates

Germany’s PNCB market is characterized by stability rather than expansion, anchored in specialty chemicals and long-term supply contracts. In 2025, LANXESS завершed its portfolio restructuring to focus exclusively on specialty chemicals, with its Krefeld-Uerdingen site remaining a key European hub for benzene-based intermediates used in high-performance coatings and pigments. This positioning insulates PNCB-related demand from short-term volatility in commodity aromatics.

Sustainability differentiation is becoming commercially material. In March 2025, LANXESS extended its Scopeblue labeling to include intermediates, enabling downstream customers to document verified product carbon footprint reductions in the range of 35 to 50% for PNCB-derived pigments. Even amid a weak mid-2025 macro environment, German producers reported relative resilience in aromatic intermediates, supported by long-term pharmaceutical supply agreements that prioritize security of supply and traceable environmental performance over spot pricing.

United States – Regulatory Stringency and Agrochemical Re-Shoring

The U.S. PNCB landscape is increasingly shaped by regulatory compliance costs and strategic agrochemical re-shoring. As of April 2026, the U.S. Environmental Protection Agency finalized its Workplace Chemical Protection Programs for chlorinated aromatics. These rules mandate the most stringent air monitoring, engineering controls, and personal protective equipment protocols to date, materially increasing fixed operating costs for any domestic PNCB handling or downstream processing.

At the same time, federal policy is reinforcing domestic agrochemical supply chains. In May 2025, U.S. government funding programs highlighted pesticides as a strategic resilience priority, favoring PNCB-based broad-spectrum herbicide formulations to mitigate import disruptions. This dual dynamic of higher compliance thresholds and supply-chain security is narrowing the field to well-capitalized producers and formulators capable of absorbing regulatory overheads.

Comparative Snapshot – Para Nitrochlorobenzene Industry by Country

Para Nitrochlorobenzene Market County Level Snapshot

|

Country

|

Strategic Emphasis

|

Policy or Market Driver

|

Structural Implication

|

|

India

|

High utilization and fluorination-led value addition

|

PLI Scheme, ZLD enforcement, logistics corridors

|

Stable domestic supply with rising entry barriers

|

|

China

|

Export control management and compliance upgrades

|

MOFCOM licensing, RoHS 2.0

|

Volatile export availability, higher purity norms

|

|

Germany

|

Specialty intermediates with carbon tracking

|

Scopeblue PCF disclosure, long-term contracts

|

Demand stability and sustainability premium

|

|

United States

|

Regulatory compliance and agrochemical security

|

EPA WCPP, federal pesticide funding

|

Consolidation around compliant, capital-intensive players

|

Para Nitrochlorobenzene Market Report Scope

Para Nitrochlorobenzene Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$462.8 Million

|

|

Market Size (2034)

|

$699.7 Million

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Purity Grade (Standard Grade, High-Purity Grade), By Form (Liquid Form, Solid Form), By Application (Dye Intermediates, Agrochemicals, Pharmaceutical Intermediates, Rubber Chemicals, Other Industrial Applications), By End-Use Industry (Agriculture, Pharmaceuticals, Textiles and Leather, Automotive and Rubber, Chemical Synthesis)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Anhui Bayi Chemical Industry, Aarti Industries, LANXESS, Sinopec Nanjing Chemical Industries, Kutch Chemical Industries, Jiangsu Yangnong Chemical Group, Panoli Intermediates, Liaoning Shixing Pharmaceutical and Chemical, Seymour Chemical Company, Chirag Organics, Sarna Chemicals, Chemdyes Corporation, Hefei TNJ Chemical Industry, Jiaxing Zhonghua Chemical, Seya Industries

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Para Nitrochlorobenzene Market Segmentation

By Purity Grade

- Standard Grade

- High-Purity Grade

By Form

By Application

- Dye Intermediates

- Agrochemicals

- Pharmaceutical Intermediates

- Rubber Chemicals

- Other Industrial Applications

By End-Use Industry

- Agriculture

- Pharmaceuticals

- Textiles and Leather

- Automotive and Rubber

- Chemical Synthesis

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Para Nitrochlorobenzene Industry

- Anhui Bayi Chemical Industry

- Aarti Industries

- LANXESS

- Sinopec Nanjing Chemical Industries

- Kutch Chemical Industries

- Jiangsu Yangnong Chemical Group

- Panoli Intermediates

- Liaoning Shixing Pharmaceutical and Chemical

- Seymour Chemical Company

- Chirag Organics

- Sarna Chemicals

- Chemdyes Corporation

- Hefei TNJ Chemical Industry

- Jiaxing Zhonghua Chemical

- Seya Industries

*- List not Exhaustive