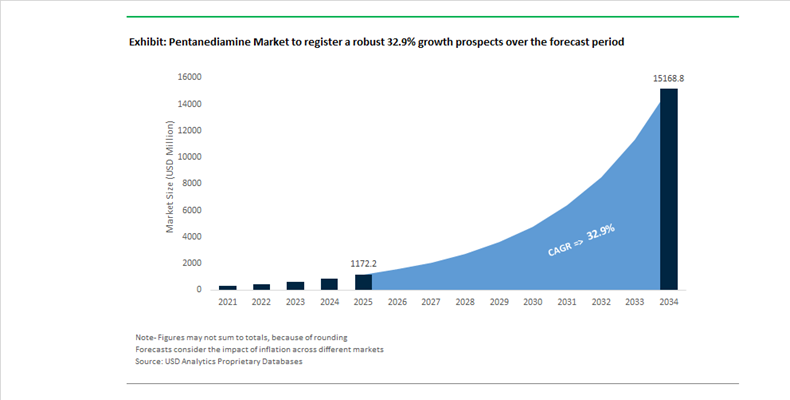

Pentanediamine Market Size 2025–2034: $1,172.2 Million to $15,161 Million at 32.9% CAGR Fueled by Bio-Based Nylon 56 Scale-Up and Fermentation Technology Breakthroughs

The global pentanediamine (1,5-PDA) market is forecast to expand from $1,172.2 million in 2025 to $15,161 million by 2034, registering an exceptional CAGR of 32.9%. This exponential growth trajectory reflects structural substitution of petrochemical diamines with fermentation-derived bio-based pentanediamine, rapid scaling of Nylon 56 production, and deep integration of bio-amines into automotive lightweighting, textiles, specialty coatings, and epoxy curing agents. Pentanediamine has transitioned from a niche bio-intermediate to a core platform molecule within sustainable polyamide value chains, driven by regulatory carbon reduction mandates and performance advantages in moisture absorption, dyeability, and toughness.

Capacity expansion in China is redefining global supply leadership. In late 2025, Cathay Biotech achieved a construction milestone at its Taiyuan production hub in Shanxi, designed to expand its current 50,000 tons per year pentanediamine capacity while integrating 100,000 tons of bio-based Nylon 56 production. Full-scale operations are targeted for mid-2026, reinforcing Cathay’s position as the dominant producer of bio-based 1,5-PDA. In August 2025, the company secured a major A-share capital placement valuing it at approximately $4.79 billion, with proceeds directed toward industrial-scale bio-pentanediamine expansion and development of its Ecotronyl recycled bio-polyamide platform for automotive lightweight applications. This capital reinforcement underscores investor confidence in high-growth bio-polyamide markets.

Technological disruption in fermentation efficiency is accelerating cost competitiveness. In December 2025, Toray Industries introduced an immobilized-microorganism bioreactor platform designed to reduce energy consumption by 80% to 90% compared to conventional chemical conversion routes. Commercial scaling is scheduled for 2026, positioning the technology to materially lower production costs for high-purity pentanediamine and other bio-amines. In January 2026, Toray reported successful completion of a one-year trial of an all-carbon CO₂ separation membrane at a biogas facility, improving biomethane purification for fermentation feedstock. This development reduces energy intensity in large-scale bio-PDA production and enhances the economics of integrated bio-refinery operations.

Global portfolio optimization among specialty chemical producers is reinforcing pentanediamine’s structural importance. In April 2025, Evonik Industries confirmed strategic optimization of its polyamide intermediates portfolio, identifying pentanediamine as a critical input for high-margin specialty nylon grades. The focus on process yield improvements and carbon footprint reduction aligns with European sustainability directives and premium polymer pricing strategies. Meanwhile, in late 2025, CJ BIO expanded cooperation with global textile manufacturers to supply fermentation-derived pentanediamine for Nylon 56 fibers. The initiative targets high-end athleisure and performance textiles, challenging Nylon 66 dominance by emphasizing improved moisture management and dye affinity.

Export acceleration and regulatory alignment are expanding European market penetration. During 2024 and early 2025, Ningxia Yipin Biotechnology reported increased export volumes of bio-based 1,5-PDA and secured new European distribution agreements for epoxy curing agent precursors. These developments align with EU Green Deal chemical mandates favoring renewable feedstocks and lower carbon intensity intermediates. Parallel upstream restructuring occurred in September 2025 when Mitsui Chemicals, Asahi Kasei, and Mitsubishi Chemical formed Western Japan Ethylene LLP to streamline feedstock supply chains supporting high-value downstream derivatives, including bio-based diamines for next-generation eco-friendly plastics.

Industrial applications beyond textiles are gaining traction. Throughout 2024 and 2025, Cathay Biotech and China Merchants Group expanded deployment of pentanediamine-based composite materials in logistics pallets, marking one of the first large-scale industrial applications outside fiber markets. In December 2025, Kiri Industries finalized a $689 million exit from DyStar, redirecting capital toward specialty chemical intermediates. Given pentanediamine’s rising relevance in high-performance dye intermediates and textile chemistry, this capital reallocation is expected to stimulate new R&D investment within Asia’s bio-amine supply chain.

Structural Trends and Growth Opportunities Defining the Pentanediamine Market

Rapid Commercialization of Bio-PDA for High-Performance Bio-Nylon 5X Materials

The pentanediamine market has moved decisively beyond pilot-scale validation into full industrial commercialization, driven by strong demand for next-generation bio-based polyamides. Chemical producers and downstream OEMs are increasingly positioning bio-PDA as the core monomer for odd-numbered nylons such as PA 56 and PA 510. These materials offer a superior balance of moisture absorption, dimensional stability, and thermal performance compared with conventional Nylon 6 and Nylon 66, making them attractive for premium engineering applications.

Industrial scale-up momentum is clearly visible in China. In September 2025, Cathay Biotech announced an extension of its long-term production roadmap, targeting 500,000 tons of bio-based diamine capacity and 900,000 tons of bio-based polyamide capacity by late 2027. This expansion reflects a strategic intent to displace fossil-derived and long-chain aromatic polyamides with renewable pentanediamine-based systems across global supply chains.

Feedstock innovation is reinforcing this trend. Facilities such as the UPM Leuna Biorefinery, operational as of December 2025, have demonstrated the ability to extract high-purity industrial sugars from hardwood residues. These sugars enable fermentation pathways that produce bio-PDA with an estimated 70% lower carbon footprint than petroleum-based equivalents. Crucially, the resulting monomer meets Grade A purity standards required by automotive and electronics manufacturers, removing a key barrier to large-scale substitution.

Captive Supply Chain Formation Through Strategic Biotech Partnerships

As bio-PDA becomes a strategically critical monomer, nylon producers are rethinking procurement models. Rather than relying on open-market sourcing, leading players are forming captive supply arrangements and joint ventures with biotechnology specialists to secure traceable, price-stable supply and to reduce exposure to feedstock volatility.

A landmark example emerged in February 2024, when LG Chem entered into a strategic partnership with CJ CheilJedang to establish a dedicated production line for bio-based nylon. By securing direct access to fermented bio-PDA, LG Chem is building a closed-loop manufacturing ecosystem that bypasses the disruptions and price swings common in merchant chemical markets.

Operational data from late 2025 underscores the value of this approach. Manufacturers integrating PDA production within existing agricultural or biorefinery hubs reported average delivery delay reductions of around 18%. This has accelerated interest in developing localized science and technology clusters across India and Southeast Asia, where access to biomass feedstocks, fermentation expertise, and polymer processing infrastructure can be combined to create resilient, vertically integrated PDA supply chains.

Penetration into Automotive Electrification and Lightweighting Applications

Automotive electrification represents one of the most compelling growth opportunities for pentanediamine-derived polyamides. Electric vehicles place exceptional thermal and mechanical demands on materials used in battery systems, power electronics, and cooling architectures. Bio-nylon 56, synthesized from PDA, delivers a high melting point, strong hydrolysis resistance, and excellent dimensional stability under continuous operating temperatures exceeding 150°C.

Material audits conducted in 2025 indicate that these properties make PDA-based polyamides well suited for EV battery housings, electrical connectors, and fluid management components. In addition to performance benefits, lightweighting potential contributes directly to extended driving range, a key purchasing criterion for EV consumers. From a sustainability perspective, OEMs are increasingly deploying bio-polyamides to meet the EU Chemicals Industry Package requirements and broader net-zero commitments. Incorporating PDA-based components can reduce vehicle-level Scope 3 emissions by up to 40%, improving ESG scores and alignment with the European Green Deal.

Expansion into Sustainable Textile Fibers for Sportswear and Luxury Apparel

Beyond engineering plastics, pentanediamine is gaining traction in the performance textile sector, where brands seek to combine technical functionality with credible plant-based narratives. PDA-derived nylons are increasingly viewed as a disruptive alternative in athleisure and luxury apparel, offering a softer, silk-like hand feel that conventional nylons struggle to achieve.

Product launches showcased in December 2025 at Heimtextil highlighted next-generation textiles integrating bio-nylon with cellulose fibers. Pentanediamine-based PA 56 is being prioritized in sportswear due to its higher moisture regain of approximately 5%, compared with about 4% for Nylon 6. This improvement enhances comfort during high-intensity activity and supports premium positioning in performance apparel.

Traceability and certification are reinforcing value capture. Luxury and sportswear brands are increasingly adopting molecular markers and ISCC PLUS certification to verify bio-content throughout the value chain. Combined with compliance to chemical safety standards such as OEKO-TEX Standard 100, this transparency allows brands to command price premiums of 15 to 20% for responsible-performance apparel. As consumers become more conscious of microplastic persistence and chemical safety, PDA-based textile fibers are well positioned to capture sustained demand growth across both technical and fashion-driven segments.

Pentanediamine Market Share and Segmentation Insights

Bio-Based Pentanediamine Leads Market Adoption with Renewable Diamine Production for Polyamide Manufacturing

Bio-based pentanediamine accounted for 68.40% of the Pentanediamine Market by origin in 2025, reflecting strong industry demand for renewable chemical intermediates used in engineering polymer production. Produced through lysine fermentation, bio-based pentanediamine offers a sustainable alternative to petrochemical diamines while maintaining identical chemical structure and polymerization behavior. Its compatibility with existing polymer manufacturing infrastructure enables manufacturers to incorporate renewable raw materials without altering production processes. In 2025, the drop-in replacement positioning of bio-based pentanediamine is accelerating adoption across polymer value chains, allowing producers of engineering plastics and textile fibers to integrate renewable content while maintaining mechanical strength, thermal stability, and processing performance comparable to conventional nylon materials.

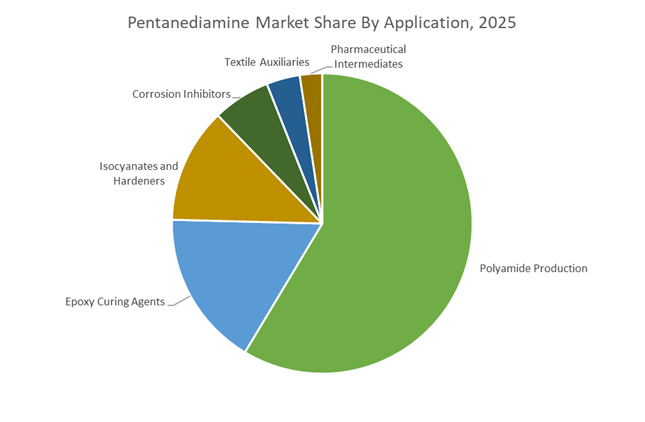

Polyamide Production Drives Pentanediamine Consumption in Bio-Based Engineering Plastics

Polyamide production represented 58.60% of the Pentanediamine Market by application in 2025, making it the dominant use case for this diamine intermediate. Pentanediamine functions as a core monomer in the synthesis of bio-based polyamides such as PA5.6 and PA5.10, which are used in engineering plastics, textile fibers, and specialty materials. These polymers provide mechanical strength, chemical resistance, and thermal stability required in automotive components, consumer products, and industrial equipment. In 2025, the automotive lightweighting trend is strengthening demand for bio-based polyamides, as vehicle manufacturers increasingly adopt sustainable engineering materials for connectors, under-hood components, and interior parts that deliver durability while contributing to reduced vehicle weight and improved environmental performance.

Pentanediamine Market Competitive Landscape

The Pentanediamine Market is rapidly evolving into a bio-based polyamide ecosystem, driven by large-scale fermentation, AI-enabled metabolic engineering, and Nylon 56 (PA56) commercialization. China-centric capacity expansion and renewable carbon integration are reshaping competition, positioning bio-PDA as a sustainable alternative to HMDA in automotive, textiles, and engineering plastics.

Cathay Biotech scales bio-PDA industrialization with AI-driven fermentation and 500 KT capacity target

Cathay Biotech Inc. leads the pentanediamine market through aggressive scale-up of bio-based 1,5-pentanediamine production. Its Shanxi Synthetic Biology Industrial Park targets 500,000 tonnes/year capacity by 2026, primarily for captive use in TERRYL® and ECOPA® polyamides. The company achieved a revenue target exceeding 3.8 billion RMB in FY2025, supported by a 6.6 billion RMB capital infusion. AI-driven strain optimization and high-throughput screening have significantly improved fermentation yield and reduced production costs. Cathay’s DN5 enables Nylon 56 (PA56), offering superior moisture management and flame retardancy compared to Nylon 66. This vertically integrated, full-chain synthetic biology platform positions Cathay as the dominant force in the bio-polyamide revolution.

Toray advances premium bio-polyamide fibers with Ecodear and NANODESIGN precision engineering

Toray Industries, Inc. is focusing on high-value bio-based polymers, leveraging pentanediamine for advanced fiber applications. Its Ecodear™ N510, a 100% bio-based polymer, is entering full commercialization for luxury apparel and performance textiles. The company’s proprietary NANODESIGN™ technology enables precise control over fiber morphology, delivering enhanced softness, durability, and wrinkle resistance. Toray’s breakthrough in bio-based 2-pyrrolidone production further strengthens its biodegradable polymer portfolio. Under its AP-G 2025 roadmap, the company is targeting improved ROIC through high-margin bio-monomers. This integration of materials science and sustainability positions Toray as a leader in premium bio-polyamide applications.

Ajinomoto leverages AminoScience platform and strategic alliances to advance pentanediamine fermentation

Ajinomoto Co., Inc. is utilizing its AminoScience platform to industrialize pentanediamine via advanced fermentation pathways. Its 2025 collaboration with AMSilk enhances large-scale production of nitrogen-rich bio-intermediates, including PDA. The company is actively protecting its intellectual property through patent enforcement in China and Japan, highlighting the strategic importance of amino-acid-based manufacturing. Ajinomoto is expanding its bio-based chemical footprint in Thailand to strengthen regional production capabilities. Its long-standing R&D partnership with Toray provides deep expertise in lysine-derived pentanediamine synthesis. This combination of fermentation leadership, IP strategy, and global expansion strengthens Ajinomoto’s competitive positioning.

Eppen Biotech secures feedstock advantage through lysine integration and downstream material expansion

Ningxia Eppen Biotech Co., Ltd. is a key player in the pentanediamine market, leveraging its dominance in lysine production to ensure feedstock security. With an estimated 5,000 tonnes capacity, Eppen supplies high-purity intermediates for enzymatic PDA production. The company is expanding downstream into curing agents and resin applications, transitioning toward a bio-materials-focused business model. Its vertical integration shields it from raw material volatility and supply chain disruptions. Eppen plays a strategic role in reducing China’s dependence on adiponitrile imports for polyamide production. This feedstock control and integration strategy provide a strong competitive advantage in the bio-based diamine market.

Covestro integrates pentanediamine into circular polyurethane systems for advanced material applications

Covestro AG is incorporating pentanediamine into its circular polyurethane portfolio, positioning it as a renewable alternative for advanced materials. The acquisition of Vencorex assets enhances its global isocyanate infrastructure, enabling scale-up of PDI derived from pentanediamine. The company’s Desmodur® eco product line utilizes mass balance principles to integrate renewable feedstocks into high-performance coatings and adhesives. At CES 2026, Covestro demonstrated applications in lightweight, signal-transparent materials for AI and 5G devices. Its focus on low-VOC, non-toxic polyurethanes aligns with tightening environmental regulations in automotive and healthcare sectors. This integration of bio-based chemistry and advanced applications reinforces Covestro’s leadership in sustainable polymers.

China – World-Scale Bio-Based Capacity and Process Leadership

China represents the structural center of gravity for the global pentanediamine industry, anchored by aggressive scale-up and fermentation-driven process leadership. In September 2025, Cathay Biotech confirmed the strategic expansion of its flagship bio-based materials hub, targeting an ultimate capacity of 500,000 tons of bio-based diamines by late 2027. This expansion builds directly on the successful 2024 commissioning of its 30,000-ton bio-cadaverine unit, currently the world’s largest commercial-scale bio-pentanediamine facility. The scale advantage is reinforced by China’s 2025–2026 MIIT Action Plan, which prioritizes over 5% annual chemical sector growth with explicit emphasis on “high-end supply” of bio-based platform molecules such as pentanediamine.

Technologically, Chinese producers hold a commanding position in metabolic engineering. Domestic firms lead global patent filings using genetically modified E. coli and Corynebacterium glutamicum, achieving conversion efficiencies above 90% of theoretical yield. Industrial development is concentrated in Ningxia and Shanxi chemical parks, where integrated sugar-to-polyamide clusters have reduced pentanediamine logistics costs by an estimated 15%. In parallel, 2025 marked the localization of 99.9% semiconductor-grade pentanediamine, enabling entry into specialty epoxy curing agents for advanced electronics and further elevating China’s role from volume supplier to quality-driven innovator.

Japan – Specialty Integration Through Downstream Derivatives

Japan’s pentanediamine market is characterized by downstream integration rather than bulk capacity leadership. In May 2025, Mitsui Chemicals executed a strategic organizational split to sharpen focus on “Basic & Green Materials,” with pentanediamine-derived chemistries embedded in its globally scaled STABiO™ portfolio. These materials underpin pentamethylene diisocyanate systems used in non-yellowing, high-durability coatings, positioning pentanediamine as a critical enabler of premium performance rather than a standalone commodity.

Fermentation expertise further differentiates Japan. Ajinomoto reported continued investment in advanced fermentation platforms in its November 2025 results, supporting the production of high-purity diamines for pharmaceutical and specialty chemical applications. Adoption has expanded into adjacent sectors, with Japanese aviation logistics in late 2025 integrating Biomass Evolue™ materials for lightweight cargo containers. Regulatory alignment also remains strong, as Japanese producers transitioned pentanediamine derivatives toward ISCC PLUS certification by October 2025, reinforcing export credibility in sustainability-sensitive markets.

Germany – Carbon-Tracked Pentanediamine for Coatings and Mobility

Germany’s pentanediamine industry is shaped by regulatory leadership and carbon transparency rather than scale. In 2025, Covestro commercialized Bayhydur® eco 7190, a hydrophilic polyisocyanate based on bio-based PDI, delivering 66% renewable carbon content. This innovation directly lowers cradle-to-gate emissions in wood and industrial coatings, reinforcing pentanediamine’s role as a strategic building block for low-carbon material systems.

Beyond coatings, Covestro’s February 2025 bio-based aniline pilot in Leverkusen is being leveraged as a technological template for stabilizing long-chain diamine supply in Europe. German producers are also at the forefront of EU Green Deal execution, implementing Digital Product Passports for pentanediamine-containing polymers. This enables automotive OEMs such as BMW and Mercedes-Benz to verify bio-origin content in nylon-5,6 components for 2026 vehicle platforms, embedding pentanediamine into regulated mobility supply chains.

India – Policy-Led Emergence of Domestic Bio-Diamines

India remains an early-stage but rapidly mobilizing market for pentanediamine, driven primarily by policy intervention. The 2025 BioE3 Policy identified bio-based chemicals as a “High-Performance Biomanufacturing” pillar, unlocking subsidies for diamine production from agricultural residues. This has materially improved project economics for domestic fermentation-based facilities and reduced dependence on imports.

Protective measures are also shaping the market. In October 2025, the Directorate General of Trade Remedies initiated safeguard investigations into rising imports from China and South Korea, aiming to shield nascent domestic capacity. On the demand side, Indian specialty chemical players such as SNF Flopam committed more than ₹800 crore during 2025–2026 to facility expansions, targeting pentanediamine-based corrosion inhibitors for oil and gas infrastructure. These moves position India as a future regional supplier rather than a pure consumption market.

United States – Application-Led Uptake in Bio-Nylon and Compliance

The United States pentanediamine market is defined by application pull rather than production scale. Incentives under the U.S. Farm Bill have accelerated adoption of bio-nylon PA56 in textiles and apparel, with major brands transitioning in late 2025 due to superior moisture management and dye uptake versus Nylon 6,6. This has elevated pentanediamine demand as a differentiated monomer in performance fabrics.

Regulatory alignment further supports this shift. In 2025, the EPA finalized updated TSCA risk evaluations for aliphatic diamines, prompting formulators to favor 1,5-pentanediamine for its comparatively lower toxicity profile. As a result, U.S. demand is increasingly concentrated in compliant, high-value end uses such as apparel, coatings, and specialty polymers rather than bulk chemical applications.

Comparative Snapshot – Pentanediamine Industry by Country

Pentanediamine Market County Level Snapshot

|

Country

|

Strategic Position

|

Primary Driver

|

Market Character

|

|

China

|

Global scale and technology leader

|

Fermentation efficiency and capacity expansion

|

Volume and high-purity dominance

|

|

Japan

|

Specialty downstream integrator

|

High-performance coatings and materials

|

Value-added, export-oriented

|

|

Germany

|

Regulatory and carbon transparency hub

|

EU Green Deal and digital traceability

|

Low-carbon, compliant supply

|

|

India

|

Policy-driven emerging producer

|

BioE3 incentives and trade protection

|

Early-stage, capacity-building

|

|

United States

|

Application-led demand center

|

Bio-nylon adoption and TSCA compliance

|

End-use driven growth

|

Pentanediamine Market Report Scope

Pentanediamine Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1172.2 Million

|

|

Market Size (2034)

|

$15161 Million

|

|

Market Growth Rate

|

32.9%

|

|

Segments

|

By Origin (Bio-Based Pentanediamine, Synthetic Pentanediamine), By Grade (Industrial Grade, High-Purity Grade, Semiconductor Grade), By Application (Polyamide Production, Isocyanates and Hardeners, Epoxy Curing Agents, Corrosion Inhibitors, Pharmaceutical Intermediates, Textile Auxiliaries), By End-Use Industry (Automotive, Textiles and Apparel, Electronics, Building and Construction, Pharmaceutical and Life Sciences)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Cathay Biotech, Mitsui Chemicals, Covestro, Ajinomoto, Evonik Industries, BASF, Huntsman, Ningxia Eppens Bioengineering, Solvay, Tokyo Chemical Industry, AK Scientific, Eastman Chemical, Toray Industries, Hebei Chengxin, Meghmani Organics

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pentanediamine Market Segmentation

By Origin

- Bio-Based Pentanediamine

- Synthetic Pentanediamine

By Grade

- Industrial Grade

- High-Purity Grade

- Semiconductor Grade

By Application

- Polyamide Production

- Isocyanates and Hardeners

- Epoxy Curing Agents

- Corrosion Inhibitors

- Pharmaceutical Intermediates

- Textile Auxiliaries

By End-Use Industry

- Automotive

- Textiles and Apparel

- Electronics

- Building and Construction

- Pharmaceutical and Life Sciences

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Pentanediamine Industry

- Cathay Biotech

- Mitsui Chemicals

- Covestro

- Ajinomoto

- Evonik Industries

- BASF

- Huntsman

- Ningxia Eppens Bioengineering

- Solvay

- Tokyo Chemical Industry

- AK Scientific

- Eastman Chemical

- Toray Industries

- Hebei Chengxin

- Meghmani Organics

*- List not Exhaustive