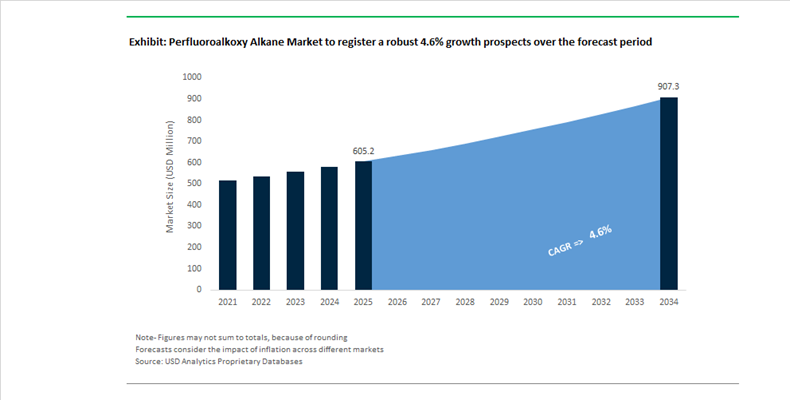

Perfluoroalkoxy Alkane (PFA) Market Size 2025–2034: $605.2 Million to $907.2 Million at 4.6% CAGR Amid PFAS Restructuring and Semiconductor Demand Realignment

The global perfluoroalkoxy alkane (PFA) market is projected to expand from $605.2 million in 2025 to $907.2 million by 2034, registering a CAGR of 4.6%. Market expansion is closely tied to high-purity fluoropolymer demand in semiconductor fabrication, electric vehicle battery systems, advanced medical devices, and chemical processing equipment. PFA, valued for its exceptional chemical resistance, high-temperature stability, dielectric performance, and ultra-low extractables, remains a preferred fluoropolymer in corrosive and ultra-clean applications. However, structural changes across the PFAS regulatory landscape are materially reshaping supply chains, competitive positioning, and capital allocation strategies through 2026.

A defining market shift occurred in 2025 as 3M completed its exit from PFAS manufacturing, including PFA production. By December 2025, 3M had discontinued nearly 25,000 PFAS-containing products, relinquishing approximately $1.3 billion in annual fluorochemical revenue. This withdrawal created immediate supply rebalancing opportunities for established players in Asia and North America, particularly in semiconductor-grade PFA resins and coatings. Parallel portfolio realignments followed in September 2025 when Solvay announced cessation of trifluoroacetic acid and related organics production at its Bad Wimpfen site, effective early 2026. This decision allows Solvay to pivot toward greener fluorinated alternatives and core brazing flux technologies while reducing exposure to persistent PFAS-related regulatory scrutiny.

Strategic capacity expansion in India is redefining global PFA supply flexibility. In August 2025, The Chemours Company entered a strategic production alliance with SRF Limited to expand fluoropolymer manufacturing capacity in India. Benefit realization and incremental global supply flexibility are scheduled for early 2026, specifically targeting semiconductor manufacturing and EV battery insulation markets. Earlier, in October 2024, Chemours established a semiconductor-focused partnership to supply high-purity PFA coatings for advanced fabrication equipment operating in ultra-cleanroom environments. This initiative aligns with Chemours’ “Pathway to Thrive” strategy launched in November 2024, which prioritizes advanced performance materials for data center immersion cooling and electric mobility. By mid-2025, the company reported a sequential 22% increase in Adjusted EBITDA, reflecting improved margin realization in high-performance fluoropolymers.

Indian manufacturers are strengthening their position as alternative suppliers. In 2024, Gujarat Fluorochemicals committed ₹2,500 crore to quadruple fluoropolymer capacity, including PFA grades tailored for semiconductor wafer handling systems and renewable energy components. This expansion positions India as a credible long-term production base amid Western PFAS retrenchment. Complementing this regional scale-up, Daikin Industries invested more than $300 million in PFAS capture technologies in August 2024 to achieve 99.9% process water recovery and confirmed transition of its fluoroelastomer manufacturing to more sustainable technologies by 2025. In September 2024, Daikin acquired additional land in India to expand manufacturing capacity, with a target to double sales by 2025 and use India as an export hub to 100 countries by March 2026.

Application-specific innovation is reinforcing PFA’s premium positioning. In January 2024, Daikin launched an advanced PFA coating engineered for medical devices, focusing on enhanced biocompatibility and resistance to repeated sterilization cycles. This development targets surgical instruments and critical care equipment where traditional coatings degrade under aggressive autoclaving. In early 2025, imec and industrial partners validated PFAS-free patterning materials compatible with advanced semiconductor nodes. This milestone provides a regulatory roadmap for 2nm chip manufacturing while preserving demand for high-purity PFA components in chemical delivery and wafer processing systems.

Corporate portfolio concentration continues across Japan. In December 2025, AGC announced its exit from the Dragontrail specialty glass segment, to be completed by Q3 2026, reallocating capital toward Life Science and Fluorochemical divisions where PFA demand from semiconductor clients remains structurally stronger than glass applications.

Strategic Trends and High-Value Opportunities Reshaping the Perfluoroalkoxy Alkane Market

Strategic Capacity Expansion for Semiconductor-Grade Ultra-High Purity PFA

The Perfluoroalkoxy Alkane market is undergoing a structural upgrade as global semiconductor manufacturing shifts toward advanced nodes and domestic production mandates. PFA has emerged as a mission-critical material for contamination-free fluid handling in semiconductor fabs, where even trace metal ion extraction can compromise yield at sub-5nm process nodes. As chipmakers expand 300mm wafer capacity, demand is accelerating for Ultra-High Purity PFA grades designed specifically for cleanroom environments.

Supply chain sovereignty is a central driver. Chemours, currently the only domestic producer of PFA in the United States, expanded capacity during 2024 and 2025 to support semiconductor reshoring initiatives under the CHIPS Act. Its PFA resins are now classified as critical chemistries by the U.S. Department of Energy, reflecting their essential role in lining pipes, valves, tanks, and wafer chemical delivery systems where zero contamination tolerance is mandatory.

Innovation at the material level is reinforcing this trend. In January 2024, Daikin Industries introduced a new generation of modified PFA grades engineered for semiconductor fluid handling. These materials offer enhanced stress-crack resistance and ultra-smooth internal surfaces that eliminate micro-defect sites where chemical residues and particulates can accumulate. Market data from the Semiconductor Industry Association indicates that capital investment tied to 300mm wafer fabs has lifted demand for UHP PFA components by nearly 20% over the past three fiscal years, materially outperforming standard industrial PFA grades.

Shift Toward Integrated, Life-Cycle-Optimized PFA System Design

Industrial end users are increasingly specifying PFA at the system design stage rather than as a replacement component. This reflects a broader shift toward total cost of ownership optimization in chemically aggressive operating environments. PFA’s ability to withstand continuous temperatures up to 260°C while resisting virtually all industrial chemicals has repositioned it as a productivity enabler rather than a specialty plastic.

In petrochemical and specialty chemical plants, the use of fully integrated PFA-lined transfer systems has reduced corrosion-related maintenance downtime by an average of 22%. This reliability advantage has driven a 34% increase in the specification of PFA for complete fluid handling systems between 2023 and 2025. Engineering, procurement, and construction firms are now standardizing PFA sheets, tubing, and fittings as single-material solutions across entire production blocks to simplify spare-part inventories and eliminate failure risks associated with incompatible seals and joints.

This system-level adoption is translating directly into volume growth. Since 2022, the use of PFA tubing and sheets has risen by approximately 23% as industrial projects prioritize standardized, long-life materials capable of supporting continuous operations in corrosive service. As capital projects grow in scale and complexity, integrated PFA system design is becoming a default specification rather than an exception.

Enabling Advanced Battery Manufacturing and EV Infrastructure

Electrification and energy transition investments are opening substantial growth opportunities for PFA beyond its traditional semiconductor stronghold. In battery manufacturing, PFA’s chemical inertness and thermal stability make it a preferred material for electrode slurry preparation, electrolyte filling, and chemical transfer systems exposed to highly reactive lithium salts.

Between 2024 and 2025, the U.S. Department of Energy committed more than USD 3 billion in grants to domestic battery manufacturing. These programs have indirectly accelerated demand for PFA as a non-reactive polymer that ensures process stability and minimizes contamination risk. In parallel, PFA is gaining traction in high-voltage electric vehicle architectures. Its dielectric strength exceeding 60 kV per millimeter and low dissipation factor support signal integrity in high-frequency power electronics and charging systems.

Thermal management is another emerging application. As artificial intelligence workloads push data centers toward liquid immersion cooling, PFA is increasingly used in secondary refrigerant loops. Its non-leaching characteristics preserve coolant purity, protecting high-value GPU and CPU assemblies from degradation. In 2024 alone, global production of PFA-coated wiring exceeded 10,000 kilometers, underscoring its growing role in EV charging networks, 5G infrastructure, and advanced data center construction.

Standardization in Single-Use Bioprocessing for Biopharmaceutical Manufacturing

The biopharmaceutical industry’s transition toward flexible, single-use manufacturing is creating a high-margin demand stream for PFA. Single-use technologies require materials with ultra-low extractable and leachable profiles to preserve the integrity of sensitive biologic drugs. PFA meets these requirements while offering visual clarity, chemical inertness, and sterilization durability.

Regulatory certainty is reinforcing adoption. In August 2025, the U.S. Food and Drug Administration reaffirmed that large-molecule fluoropolymers such as PFA are very unlikely to pose toxicity risks to patients. This reaffirmation provides biopharmaceutical manufacturers with the confidence to integrate PFA into critical fluid paths for cell culture, fermentation, and downstream processing.

Market demand is accelerating alongside biologics growth. The FDA approved a record 18 biosimilars in 2024, driving rapid capacity expansion across biologic production lines. PFA-based bags, connectors, sensors, and tubing are increasingly specified for these facilities due to their ability to maintain integrity through gamma and ethylene oxide sterilization cycles. Industry estimates suggest that approximately 41% of recent growth in high-purity PFA demand is attributable to pharmaceutical clean-track applications, where zero contamination, regulatory compliance, and operational flexibility are non-negotiable.

Perfluoroalkoxy Alkane Market Share and Segmentation Insights

PFA Tubing and Pipe Lead Market Demand in High-Purity Chemical Fluid Handling Systems

PFA tubing and pipe accounted for 34.80% of the Perfluoroalkoxy Alkane Market by product form in 2025, reflecting strong demand from industries requiring ultra-high purity fluid transport systems. These fluoropolymer components provide exceptional chemical resistance, high temperature tolerance, and low contamination risk, making them critical for semiconductor manufacturing, pharmaceutical processing, and chemical production facilities. PFA tubing and piping systems are widely used for transporting ultra-pure water, corrosive chemicals, and slurry materials where conventional metal or polymer systems cannot meet purity requirements. In 2025, semiconductor fabrication facility expansion across Asia, North America, and Europe is significantly increasing demand for PFA piping networks, as new chip manufacturing plants require extensive high-purity fluid distribution infrastructure.

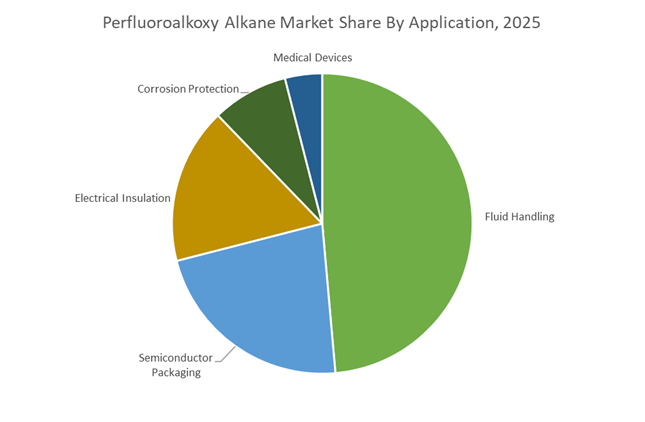

Fluid Handling Applications Drive PFA Material Consumption in Semiconductor and Chemical Processing Facilities

Fluid handling represented 48.60% of the Perfluoroalkoxy Alkane Market by application in 2025, making it the dominant use of PFA materials across high-performance industrial environments. The material’s combination of chemical inertness, thermal stability, and contamination resistance enables reliable transport of aggressive chemicals and ultra-pure liquids in semiconductor fabs, chemical processing plants, and pharmaceutical production facilities. PFA tubing, fittings, valves, and pump components are widely used to maintain purity standards in critical process lines. In 2025, growing chemical mechanical planarization process requirements in advanced semiconductor manufacturing are increasing demand for PFA fluid handling systems capable of transporting abrasive CMP slurries without particle contamination or material degradation.

Perfluoroalkoxy Alkane Market Competitive Landscape

The Perfluoroalkoxy Alkane (PFA) Market is defined by ultra-high-purity resin demand from sub-2nm semiconductor manufacturing and a structural supply shift following 3M’s PFAS exit. Competition centers on contamination-free fluid handling, PFAS capture technologies, and circular fluoropolymer innovation aligned with REACH and TSCA regulations.

Chemours drives high-purity PFA leadership with Teflon portfolio and value-over-volume pricing strategy

The Chemours Company maintains a leading position in the PFA market through its Teflon™ PFA portfolio, widely adopted in semiconductor wet processing and chemical handling systems. In 2025, Chemours reported $5.8 billion in net sales, with its Advanced Performance Materials segment targeting $800–$900 million EBITDA in 2026. The company has adopted a value-over-volume strategy, implementing price increases to offset inflation and regulatory costs. Its PFA materials offer exceptional thermal stability up to 260°C and resistance to aggressive etchants, making them critical for next-generation chip fabrication. Chemours is also investing in emissions reduction technologies, including thermal oxidizers and carbon capture systems. This combination of performance leadership and regulatory compliance strengthens its global dominance.

Daikin advances ultra-pure PFA and PFAS capture with aggressive investment and additive manufacturing innovation

Daikin Industries is expanding its footprint in the PFA market through its FUSION30 strategy, focusing on ultra-high-purity materials for semiconductor and telecom applications. The company is investing over $300 million to achieve 99.9% PFAS capture in manufacturing processes, setting a benchmark for regulatory compliance. Its NEOFLON™ PFA is known for superior melt-processability and stress-crack resistance, supporting complex injection-molded components and high-purity tubing. Daikin is also developing PFA powders for powder bed fusion (PBF) 3D printing, targeting aerospace and medical applications. The company aims to grow its fluorochemicals business by 1.2x by 2030. This integration of sustainability, innovation, and capacity expansion positions Daikin as a key technology leader.

Syensqo accelerates specialty PFA innovation for electrification and hydrogen economy applications

Syensqo has emerged as a focused specialty polymers player, emphasizing PFA applications in electrification and digital infrastructure. Its Hyflon® PFA portfolio supports EV battery systems and hydrogen storage technologies, aligning with energy transition trends. The company is expanding manufacturing capacity in North America and Asia to meet localized semiconductor and clean energy demand. Through its ECHO portfolio, Syensqo is targeting 18% circular product sales by 2030, integrating bio-based and recycled content. It is also contributing to advanced projects like hydrogen-powered aviation through high-performance polymer solutions. With a carbon neutrality target by 2040, Syensqo combines sustainability with high-value application focus.

AGC leverages circular fluoropolymer innovation and semiconductor integration under AGC plus-2026 strategy

AGC Inc. is strengthening its position in the PFA market through circular material innovation and semiconductor integration. The company achieved UL2809 certification for fluoropolymers produced using recycled fluorite, enabling “circular PFA” offerings for ESG-focused customers. Its Fluon® PFA is widely used in wafer handling systems, chemical storage, and EUV lithography components due to its high purity and transparency. AGC is aligning its Electronics and Performance Chemicals segments to deliver integrated solutions for advanced chip manufacturing. Under its AGC plus-2026 plan, it aims for over 50% profit contribution from strategic businesses. This focus on circularity and semiconductor synergy enhances its competitive positioning.

3M exit reshapes global PFA supply chains and accelerates market consolidation among remaining players

3M’s exit from PFAS manufacturing, completed in December 2025, has fundamentally altered the PFA market landscape. The discontinuation of Dyneon™ PFA impacted approximately $1.3 billion in annual sales, creating a significant supply gap. Customers have shifted procurement toward Chemours, Daikin, and AGC, intensifying competition among remaining suppliers. While 3M continues managing legacy PFAS-containing products, it has already eliminated PFAS from nearly 7,000 items. The company is now focused on regulatory compliance and settlement obligations related to environmental liabilities. This exit has accelerated market consolidation and reinforced the dominance of vertically integrated fluoropolymer producers.

United States – Regulatory Reset and Strategic Semiconductor Alignment

The United States PFA industry is entering a structurally reset phase shaped by regulatory resolution and semiconductor-driven demand certainty. In August 2025, leading domestic producers including Chemours finalized an $875 million settlement with New Jersey state authorities, resolving long-standing environmental liabilities tied to legacy PFAS operations. This settlement has materially improved regulatory visibility for PFA resin manufacturing, enabling producers to commit capital toward high-purity fluoropolymer expansions without prolonged litigation overhangs. Concurrently, the U.S. Department of Commerce has formally prioritized PFA-lined fluid handling systems under CHIPS and Science Act funding rounds, effectively designating semiconductor-grade PFA as a national security material critical to domestic fab resilience.

Supply-side dynamics have been reshaped by 3M’s confirmed exit from PFA manufacturing by the end of 2025, removing an estimated $1.3 billion in annual fluoropolymer sales from the global market. This has accelerated long-term contract realignments toward Chemours and Daikin Industries, particularly for aerospace, defense, and advanced electronics customers. Chemours further reported in November 2025 that its Washington Works facility has restored full operational capacity for Teflon™ PFA lines following earlier outages, directly supporting surging demand. Beyond semiconductors, application breadth is expanding into data infrastructure, with Chemours announcing successful qualification of PFA-compatible two-phase immersion cooling fluids with Samsung Electronics in Q3 2025, positioning PFA as a foundational material for next-generation data center thermal management.

Japan – High-Frequency Innovation and Electronics-Centric Evolution

Japan’s PFA market remains anchored in high-value innovation rather than volume expansion, with a strong emphasis on telecommunications, electronics, and mobility. In August 2025, research led by Waseda University in collaboration with domestic industry partners revealed ultralow dielectric loss polymers designed to outperform standard PFA at 80 GHz and above, directly targeting beyond-5G and early 6G infrastructure. While these materials may eventually complement or partially substitute PFA, they underscore Japan’s role in pushing performance boundaries for fluoropolymer applications.

Commercial leadership remains visible through Daikin’s global exhibition strategy, with next-generation Neoflon™ PFA resins showcased at SEMICON Japan 2025 and SEMICON Korea 2025. These grades emphasize thermal stability up to 260°C and ultra-low metal ion contamination for advanced chipmaking. At the corporate level, Mitsui Chemicals completed a strategic reorganization in May 2025, establishing a dedicated Green Materials division to oversee reduced-footprint PFA development for electronics and mobility markets. Adoption is already evident in advanced automotive electrification, as Japanese suppliers unveiled PFA-insulated wiring for 800V EV battery systems at the Automotive Engineering Exposition 2025, leveraging dielectric strengths exceeding 60 kV/mm.

China – Localization Mandates and Export Substitution Momentum

China’s PFA industry is being rapidly reshaped by state-driven semiconductor self-sufficiency policies. In December 2025, authorities enforced a de facto 50% domestic sourcing rule for high-purity fluid handling components in semiconductor fabs, compelling chipmakers to shift procurement toward locally produced PFA tubing, liners, and fittings. This mandate is closely supported by capital deployment from the National Integrated Circuit Industry Investment Fund Phase III, a $49 billion vehicle established in 2024, which has continued funding fluorochemical industrial parks through 2025 to close technology gaps in semiconductor-grade PFA synthesis.

At the same time, Chinese producers are capitalizing on global supply gaps created by 3M’s withdrawal. Companies such as Shandong Hengyi New Material expanded PFA pellet and powder export capacity in 2025, targeting Southeast Asia and the Middle East where qualification cycles are shorter and supply security is paramount. These efforts align with confirmed Made in China 2025 milestones, with authorities stating in November 2025 that domestic content ratios for several key fluoropolymers have reached 70%, placing China within reach of full PFA resin independence over the medium term.

Saudi Arabia – Vision 2030 and Harsh-Environment Localization

Saudi Arabia is positioning itself as a regional manufacturing and application hub for PFA-based systems under its Vision 2030 industrial diversification agenda. In November 2025, Daikin Industries held a groundbreaking ceremony for a new manufacturing facility in Jeddah focused on advanced industrial cooling systems incorporating PFA components. These systems are engineered for extreme temperature and chemical exposure conditions common in desert and petrochemical environments.

The localization push is reinforced by upstream integration strategies. Saudi authorities have actively encouraged collaboration between global PFA producers and SABIC to secure domestic tetrafluoroethylene monomer supply chains. This approach reduces import dependence while anchoring fluoropolymer value chains within the Kingdom, particularly for energy, desalination, and high-reliability industrial applications.

Germany – Portfolio Rationalization and Energy Transition Demand

Germany’s PFA market reflects a selective realignment toward high-performance and energy-transition applications amid broader PFAS scrutiny. In September 2025, Solvay announced a €25 million restructuring of its Bad Wimpfen site. While certain PFAS-related organics will be phased out by early 2026, the site is being repositioned as a global hub for advanced automotive brazing and flux technologies, preserving high-value fluoropolymer competencies within Europe.

Simultaneously, Germany’s hydrogen and renewable energy ecosystems are generating incremental demand for PFA-lined equipment. Industrial clusters increasingly rely on PFA-lined heat exchangers and components in hydrogen fuel cell manufacturing due to the material’s chemical inertness and high-temperature stability. Demand for PFA membranes and linings in renewable energy processing rose by 17% during 2024–2025, underscoring PFA’s role as an enabling material in Europe’s decarbonization infrastructure rather than a commodity fluoropolymer.

Comparative Snapshot – Perfluoroalkoxy Alkane Industry by Country

Perfluoroalkoxy Alkane Market County Level Snapshot

|

Country

|

Strategic Orientation

|

Primary Demand Anchor

|

Market Character

|

|

United States

|

Regulatory reset and CHIPS Act alignment

|

Semiconductors, aerospace, data centers

|

Security-driven, contract-heavy

|

|

Japan

|

High-frequency and electronics innovation

|

6G telecom, EVs, advanced fabs

|

Innovation-led, premium grades

|

|

China

|

Localization mandates and export fill-in

|

Semiconductor fabs, regional exports

|

Policy-driven scale-up

|

|

Saudi Arabia

|

Vision 2030 localization

|

Industrial cooling, petrochemicals

|

Emerging regional hub

|

|

Germany

|

Portfolio rationalization and energy transition

|

Hydrogen, automotive technologies

|

Selective, high-performance focus

|

Perfluoroalkoxy Alkane Market Report Scope

Perfluoroalkoxy Alkane Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$605.2 Million

|

|

Market Size (2034)

|

$907.2 Million

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Product Form (PFA Resin, PFA Powder, PFA Tubing and Pipe, PFA Films and Sheets, PFA Coatings), By Grade (High-Purity Grade, General Industrial Grade, Specialty Grade), By Application (Fluid Handling, Semiconductor Packaging, Electrical Insulation, Corrosion Protection, Medical Devices), By End-Use Industry (Semiconductor and Electronics, Chemical Processing, Aerospace and Defense, Automotive, Renewable Energy, Pharmaceutical and Biotechnology)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Chemours, Daikin Industries, Solvay, AGC, 3M, Hubei Everflon Polymer, Dongyue Group, Zhejiang Juhua, Fluoro-Plastics, HaloPolymer, Saint-Gobain, Shandong Hengyi New Material Technology, Swagelok, Gujarat Fluorochemicals, Zeus Industrial Products

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Perfluoroalkoxy Alkane Market Segmentation

By Product Form

- PFA Resin

- PFA Powder

- PFA Tubing and Pipe

- PFA Films and Sheets

- PFA Coatings

By Grade

- High-Purity Grade

- General Industrial Grade

- Specialty Grade

By Application

- Fluid Handling

- Semiconductor Packaging

- Electrical Insulation

- Corrosion Protection

- Medical Devices

By End-Use Industry

- Semiconductor and Electronics

- Chemical Processing

- Aerospace and Defense

- Automotive

- Renewable Energy

- Pharmaceutical and Biotechnology

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Perfluoroalkoxy Alkane Industry

- Chemours

- Daikin Industries

- Solvay

- AGC

- 3M

- Hubei Everflon Polymer

- Dongyue Group

- Zhejiang Juhua

- Fluoro-Plastics

- HaloPolymer

- Saint-Gobain

- Shandong Hengyi New Material Technology

- Swagelok

- Gujarat Fluorochemicals

- Zeus Industrial Products

*- List not Exhaustive